VNQ - Billionaire Commercial Real Estate Investor Says 'The Worst Is Yet To Come'

2023-09-14 06:53:10 ET

Summary

- Commercial real estate market is just beginning to experience the pain of the correction, according to billionaire investor Jeff Greene.

- Office buildings are expected to be the hardest hit, with declining leasing volume and potential defaults on loans.

- Retail, industrial, and residential real estate are expected to fare better, with little risk of oversupply and high occupancy rates.

- I explain why REITs are a good buy here even with the prospect of further pain to come for the commercial real estate sector.

We're just in the first inning of this correction.

That's the bottom line takeaway about the commercial real estate market from billionaire commercial real estate investor and developer Jeff Greene from a recent CNBC interview .

According to Greene, the commercial real estate market, or at least parts of it, have only just begun to endure the pain that is coming to it. Because of high interest rates as well as the fizzling out of pandemic-era fiscal stimulus measures, Greene sees commercial real estate prices going lower before they see any relief.

Let's discuss some key quotes from that interview. Afterward, I'll make the case for why, paradoxically, publicly traded real estate investment trusts ("REITs") are a fantastic buy today despite the pain being felt in commercial real estate.

Billionaire Jeff Greene's Frontline Perspective On Commercial Real Estate

Jeff Greene is a real estate entrepreneur who built a commercial real estate empire from scratch by developing high-rise buildings in Los Angeles, New York City, and Florida over his 40-year career.

He also identified the housing bubble forming in mid-2006 and benefited from the eventual crash by trading credit default swaps. After the housing market crash in 2008-2009, Greene began buying perhaps the most hated type of asset, sub-prime mortgage-backed securities, at 20-30% yields.

Today, Greene is developing what will become the two tallest towers in Palm Beach, Florida -- one for residential use and the other for hotel and office use. The office segment is expected to account for 200,000 of the towers' 1.2 million total square feet.

In that CNBC interview, Greene, who is still clearly very long commercial real estate through direct ownership of properties, gave his view of the CRE market right now, starting with the worst off sector: office.

I think commercial office space globally is going to go through a major change. What we've seen during the pandemic is that people have adapted to a different work style where they can use Zoom and Teams and other methods to get the same amount of work or more done without going to an office. So there's no question that there's going to be less demand for office going forward.

We've already seen this playing out in declining leasing volume at all of the major office REITs such as Boston Properties ( BXP ), SL Green ( SLG ), Vornado Realty ( VNO ), Hudson Pacific Properties ( HPP ), Douglas Emmett ( DEI ), Kilroy Realty ( KRC ), and Cousins Properties ( CUZ ).

Over half of these REITs have cut their dividends, and several of them have significant debt maturities coming in the next few years.

For example, a whopping 25% of SLG's non-JV debt is maturing in 2024, and that's on top of the ~7% of total debt maturing in the remainder of this year.

SLG Q2 2023 10-Q

Granted, many of SLG's buildings are iconic staples of the NYC skyline, so some lender out there will come forward to extend financing. But at what interest rate? And many of SLG's office towers are very old buildings -- some around 100 years old. What kind of capital expenditures will be required in the future to make these buildings attractive enough to get tenants in there?

In fact, the vast majority of the pain in commercial real estate is expected to remain concentrated in office buildings, precisely because this is the sector having most difficulty refinancing debt at reasonable rates.

Consider some of the major office tower loan defaults seen in the last year from some of the biggest names in the industry.

- In mid-February, Brookfield ( BN , BAM ) defaulted on a loan for two major downtown Los Angeles office properties worth a combined $784 million.

- Days later in late February, PIMCO's Columbia Property Trust defaulted on $1.7 billion in loans for seven office properties in NYC, San Francisco, Boston, and Jersey City.

- In early March, Blackstone ( BX ) defaulted on a 531 million Euro bond for Finnish office properties.

- Pearlmark Real Estate "sold" office property Tower56 to its lender for roughly the value of the remaining debt after being unable to refinance.

- The loan for 555 California Street, the 4th largest building in San Francsico jointly owned by Vornado Realty and the Trump Organization, has been put on a loan servicer watchlist for potential default.

- Scott Rechler's RXR Realty is negotiating with the lender to convert two NYC office buildings into multifamily.

By all accounts, this wave of defaults has only just begun. A recent report by Cushman & Wakefield forecasts that by 2030, the US will have 1.1 billion square feet of vacant office space (~20% of total office space).

Jeff Greene foresees a sharp bifurcation between the best trophy properties (not just Class A but Class A+) and the rest of the office sector.

There will be office buildings with no tenants whatsoever. In markets with brand new buildings like the ones we're building in West Palm Beach, we'll get the tenants because we'll be the new, tallest building in Palm Beach County with all kinds of great amenities. And some of the older buildings just won't have any tenants at all.

What Greene is describing here is the "flight to quality."

In the office sector and perhaps also retail and industrial, Greene sees the newest, highest quality, and best located buildings continuing to attract tenants and retain their market values. But the rest of CRE, certainly anything sub-Class A, will suffer lower tenant demand and falling property values.

When it comes to the [Class] B and C properties, the worst is yet to come.

Personally, I can't envision retail, industrial, or residential real estate suffering much going forward, each for their own reasons.

There has been and continues to be so little retail real estate built that there is no risk whatsoever of an oversupply situation.

Industrial has such massive demand from e-commerce, onshoring, and increased trade with Mexico that it's difficult to see even a wave of new supply putting much of a dent in high occupancy rates.

Finally, the existing stock of residential real estate should remain strong going forward, even if newly delivered apartments struggle to lease up, because high mortgage rates are keeping would-be homebuyers in the rental market.

The Depleted Tailwind of Fiscal Stimulus

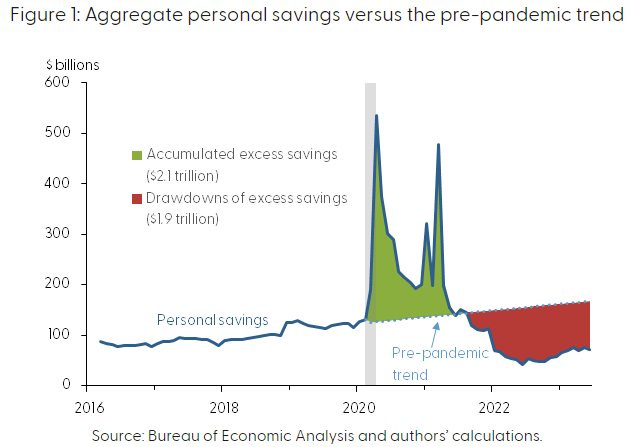

Greene also made the point in the interview that the massive, one-time stimulus spending during COVID-19 gave a huge boost to consumers and commercial real estate alike for years after it ended. But now, the pent-up savings from that stimulus spending has been depleted.

At the end of the pandemic, which wasn't that long ago, there was an extra $2.1 trillion in people's savings accounts. In March [2023], it was $500 billion. Now it's $190 billion. As that disappears and completely evaporates from people's bank accounts, there's going to be a lot less money to spend. So what's that going to mean for demand for everything, retail, office, apartments, every aspect of real estate is going to get whacked. It's just the first inning.

{kind=link}

This is an underappreciated point. People have been spending money and supporting the economy not just from their paychecks but also from the huge amount of money saved during the pandemic -- from stimulus checks, enhanced unemployment benefits, and foregone spending because of lockdowns.

The depletion of that excess savings goes a long way in explaining the rise of retail theft (especially of essential items like bread, meat, baby formula, and over-the-counter drugs) and the soaring credit card debt:

Many consumers' savings have run dry, and credit card balances are getting run up. This will inevitably mean consumer spending will pull back.

Indeed, it already has. After two straight years of elevated growth in retail and food service spending, growth in this area of consumer spending is now back to pre-pandemic levels.

As Greene put it:

In the real world, for most Americans, their wages have gone up a lot... before the pandemic, they were making $16, $18 an hour, after the pandemic they were making $26 an hour with signing bonuses. Well, all of that happened because of the trillions and trillions of dollars that was thrown into the economy. As that goes away, you're going to have unemployment. You're going to have people making less money.

High Mortgage Rates Have Cut Off Cross-Country Migration

During the pandemic, facilitated by the widespread ability to work remotely, people moved out of cities (especially dense, expensive coastal cities) en masse and into suburbs and more affordable Sunbelt cities.

While the trend of migration into the Sunbelt preexisted COVID-19 and seems likely to continue into the future, it has currently been halted, says Greene, by "return to the office" calls and high mortgage rates.

... I'm the biggest believer in West Palm Beach and Palm Beach County, but I can tell you, the demand we've seen there is a direct function of what happened during the pandemic.

As you know, the feeder cities to Florida, New York, Boston, Philadelphia, those cities had to close down during the pandemic because people have to ride subways and live close together in high rise buildings. People from those cities were going to go to Florida.

When the interviewer asked Greene if he thinks that the pandemic-era migration of people from the Northeast to Florida is over, Greene responded:

Absolutely. Because people could sell that house in Greenwich and buy a house in Palm Beach with a 3% loan. Now they have to sell that house in Greenwich with the 3% loan and buy one in West Palm Beach with a 7% loan. So of course it's going to slow.

Long term, I love South Florida. But the next few years, it's going to be very tough, and we're very overbuilt.

Unfortunately, in many Sunbelt markets, developers greenlit a huge wave of new real estate projects, expecting the pandemic-era migratory trends to continue indefinitely. But they've stopped, at least temporarily. That is likely to result in some slow years for Sunbelt multifamily REITs like Mid-America Apartment Communities ( MAA ), Camden Property Trust ( CPT ), Independence Realty Trust ( IRT ), NexPoint Residential ( NXRT ), and BSR REIT ( OTCPK:BSRTF ).

The market knows this, which is why Sunbelt apartment REITs have uniformly underperformed their coastal peers like AvalonBay Communities ( AVB ) and Equity Residential ( EQR ) over the past year, although in some cases not by much.

Although Sunbelt apartment landlords have more new supply to contend with over the next few years, I think it is possible that coastal cities with lots of empty office buildings could suffer more supply pressures in the long run from office-to-multifamily conversion projects.

Why REITs Are A Good Buy Even Now

So, commercial real estate is in for some further pain, even after all that has already occurred.

Why in the world would REITs be an opportunistic buy today in the face of this?

Answer: Because REIT prices are forward-looking and front-run future pain, while the market prices of real estate properties themselves lag real-time increases in interest rates and economic weakness.

REIT prices and property values do not always move in the same direction at the same time.

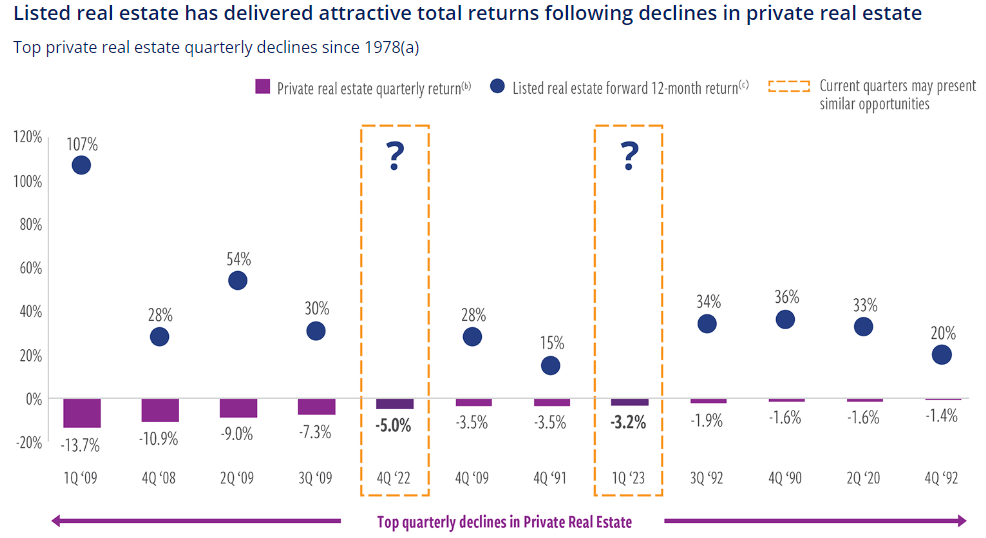

Consider the cases of every instance of falling private CRE property values over the last 30 years. In every case (so far), REITs have generated double-digit returns in the 12 months after drops in CRE property values.

{kind=link}

Why? Because REITs priced in the drop in advance. And when the drops actually occurred, the market then began to look forward to the recovery.

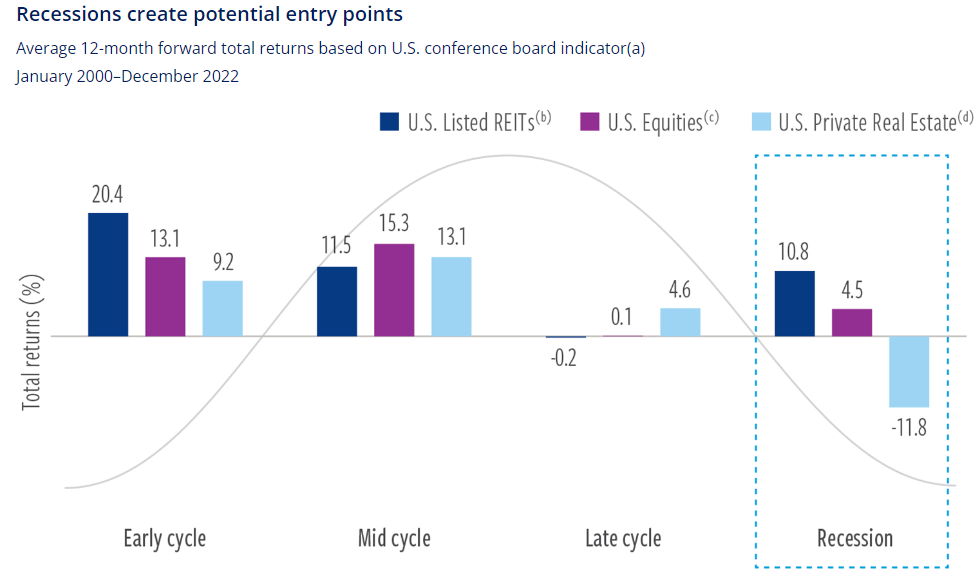

This year has basically been the "late cycle" part of the business cycle, when interest rates are rising but the economy has not yet hit recession. It is during this phase of the cycle that REITs perform most poorly, not the recession itself .

{kind=link}

Recessions are when CRE property values are falling. But historically, over the course of the recession, REIT stock prices actually rebound -- again, because they had already priced it in during the late cycle period.

Using the Vanguard Real Estate ETF ( VNQ ) and SPDR S&P 500 ETF ( SPY ) as our proxies, we can see that during the current "late cycle" period in 2023, REITs have underperformed, as expected.

And given the degree to which interest rates rose during this late cycle, it's unsurprising to see how much REITs have underperformed.

But no matter who you ask, it is widely the consensus view that the Federal Reserve is at or very close to the end of its rate-hiking cycle.

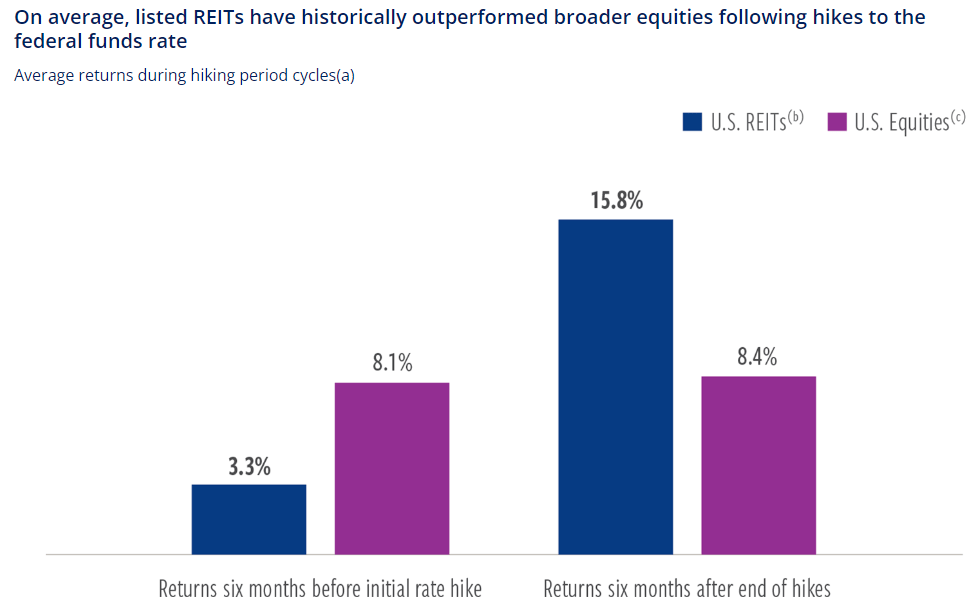

What do REITs do in the six months following the definitive end to a Fed rate-hiking cycle? They massively outperform.

{kind=link}

Historically, interest rates don't reach a subtle peak and then gently drift lower again once the Fed is done raising rates. Instead, it is almost always the case that the Fed's rate hikes cause something to break in the economy that then necessitates a quick drop in interest rates.

That is a big reason why REITs have so often outperformed in the six months following the end of the rate-hiking cycle.

Bottom Line

Jeff Greene is a smart, no-nonsense investor who became a billionaire largely from having a deep understanding of commercial real estate. When he speaks, investors would be wise to listen.

But Greene's gloomy forecast for further pain to come in CRE will not necessarily translate into further downside for REITs. It could , of course. But historically, REITs have begun to price in the eventual recovery once the market can see light at the end of the tunnel.

That's why I continue to buy high-quality REITs at rare discounts, as I described in " REIT Meltdown : 3 Rarely Discounted Buying Opportunities."

For further details see:

Billionaire Commercial Real Estate Investor Says 'The Worst Is Yet To Come'