DDCCF - Billionaire Investor Says 'Buy REITs': Our Top Picks

2023-11-11 09:00:00 ET

Summary

- Barry Sternlicht is very bullish on REITs.

- Valuations are the lowest in years, and he is buying.

- We present three of our Top Picks to profit.

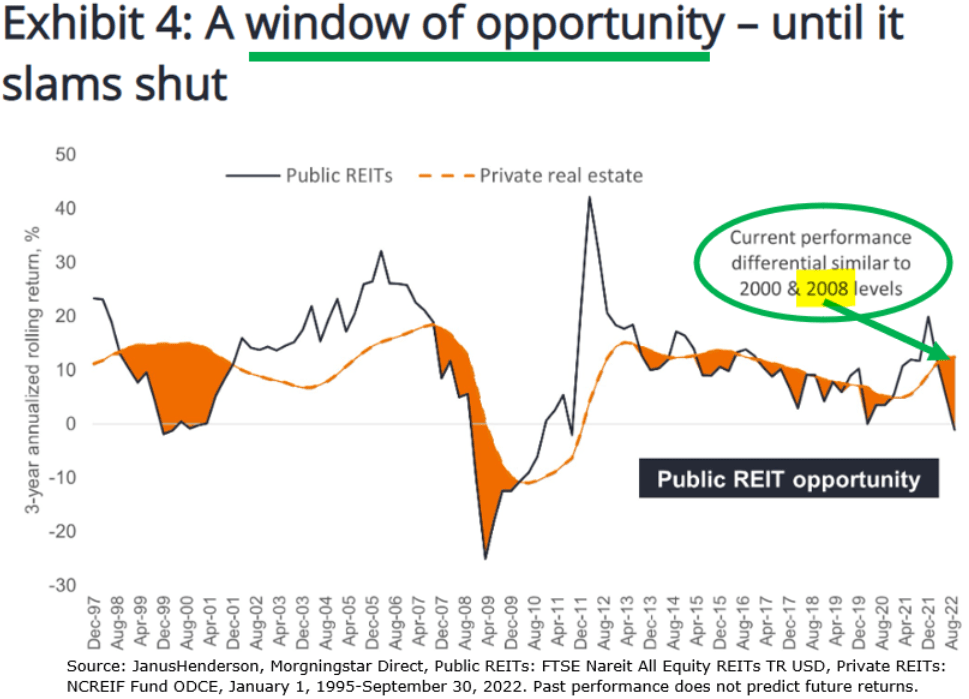

For months now, I have repeatedly said that real estate investment trusts ("REITs") are offering a historic opportunity. That's because they are priced at their lowest valuations since the great financial crisis. The investment firm Janus and Henderson noted in a late 2022 report that REITs were priced at a 28% discount on average, and since then, prices have dropped a lot more:

{kind=link}

Moreover, the ~30% discount is just the average of the sector. There are many individual REITs trading at up to 50% discounts to their net asset value. This essentially means that you get to buy real estate at 50 cents on the dollar through the REIT market.

Why are they suddenly so cheap?

The REIT market has crashed due to fears of rising interest rates.

But these fears are overblown. REIT balance sheets are today the strongest they have ever been with LTVs at just 35% on average and long debt maturities. Moreover, interest rates only surged because inflation was hot and this has resulted in significant rent growth across most property sectors.

This explains why REIT cash flows and dividend payments have kept rising despite the surge in interest rates. The impact simply isn't that significant in most cases and this is why I believe that REITs are today undervalued.

But don't take it just from me:

Barry Sternlicht was recently interviewed on Bloomberg and there were many interesting takeaways for real estate and REIT investors ( VNQ ).

In case you are not familiar with Barry Sternlicht, he is a self-made billionaire and the founder of Starwood Capital Group, which is one of the biggest private equity firms in the world, rivaling Blackstone ( BX ), Apollo Global Management ( APO ), KKR ( KKR ), and Brookfield ( BAM ).

Today, Starwood is better diversified, but for most of his career, Barry Sternlicht was a real estate investor and his track record puts him among the best in the world.

So when he talks... we listen... and his most recent interview with David Rubenstein for Bloomberg Money was particularly insightful. I would add that the interviewer, David Rubenstein, is himself the co-CEO of The Carlyle Group ( CG ), which is a major private equity firm and so he really knew what questions to ask.

Below, I first present the three main takeaways for real estate and REIT investors, and I then discuss some of our Top Picks to profit.

Takeaway #1: REITs are deeply undervalued

I want to highlight this first because I have spent the last year aggressively accumulating REITs, thinking that they were deeply undervalued.

Barry Sternlicht agrees. He talks about seeing some "very good buys" in the public REIT market and explains that he plans to launch a special situation fund to capitalize on these opportunities. He did the same thing early into the pandemic after REITs crashed by 40% and made a killing in the recovery:

"I think REITs in general look very interesting in here. During the pandemic, we raised a special situations fund and bought 15 names in the REIT sector and we were up like 70% at one point. We are going to do that again. I think that if you take a long term view, some of these good companies... They are good companies but with the wrong interest rate environment... I wouldn't even say that they have the wrong balance sheet, but they are so out-of-favor... Everyday, you pick the news, and it is real estate, real estate, real estate... but there are some very good buys out there." Barry Sternlicht

The reason why he thinks that REITs are so cheap is, of course, because they have crashed by nearly 40% since the beginning of 2022 even as their cash flows kept on rising.

A lot of individual REITs have dropped by closer to 50% or more and now trade at huge discounts to their net asset values. A good example is Camden Property Trust ( CPT ), an apartment REIT that Starwood recently added to their portfolio.

Investors like Barry Sternlicht understand that buying good real estate at 60-70 cents on the dollar will likely produce strong returns over the long run and this is why he is now buying REITs.

Takeaway #2: Office REITs are very opportunistic in Europe and Asia

Another interesting takeaway is that the office market is performing a lot better in some parts of the world. He explains that work-from-home is mostly a U.S. phenomenon and people are back in the office in Europe and Asia.

He uses Germany as an example:

"The work-from-home phenomenon is a US thing. If you go to England or Germany, we have some investments offshore and rents are up, vacancy rates in the top German markets, Berlin, Frankfurt, Munich, and Hamburg... are less than 5%. People are back in the office. You and I go to the Middle East... They are full. We have offices in Asia and they are full. So this is a US situation." Barry Sternlicht

Here, the interesting thing is that office REITs are just as heavily discounted in Germany as in the U.S.

To give you a few examples: German office landlords like alstria office REIT (ALSRF) and Branicks Group ( DDCCF ) are priced at massive 50-70% discounts to their net asset values, even as their rents keep on growing.

Alstria Office REIT

I think that this could be a generational opportunity.

The valuations of office REITs are at rock-bottom levels worldwide.

They are the lowest ever in some cases.

But the fundamentals of office landlords in some parts of the world are actually quite strong, at least relative to their valuations.

We own one specific office landlord in Germany and we are actively looking for more opportunities. I would note also that Brookfield also bought out 3 European office REITs in 2022 and paid large premiums in all three cases.

Takeaway #3: Some heavily leveraged REITs could present asymmetric risk-to-reward prospects because lenders don't want to force a bankruptcy

Barry Sternlicht explains that banks are doing what they can to avoid taking possession of office buildings. Starwood knows this best as they recently returned the keys to some office properties back to their lenders.

Barry explains that lenders are not prepared to manage them so they are trying their best to work out solutions with landlords whenever possible to allow them to get past today's crisis and not force them into bankruptcy situations.

"We were going to give back an office building... and the bank said "well not so fast, if you want, we are going to restructure the loan... we will cut the loan in half... and you will put the money in here and we will take this as a junior note because the banks don't want the assets back. They are not set up to carry these assets. They then have to go hire someone. Do the leasing themselves. It is not their business. They would have rather have a GP hold on the assets and try to work it out.

Right now, we have an unusual situation in the real estate market because everyone is sort of looking at the yield curve and it says that rates will be lower later. Everyone says survive till 2025. Hold on to your assets and sell later." Barry Sternlicht

With all of that in mind, the best opportunity today could be highly leveraged European or Asian office REITs.

They are, of course, very risky, but they are priced at huge discounts as if they were going through an existential crisis and likely facing bankruptcy. However, the fundamentals of office buildings are actually quite strong in some European and Asian markets, and since lenders don't want to gain possession of these properties, they will likely be flexible with borrowers in the near term in case they breach some covenants.

Therefore, their rock-bottom valuations may not be justified and could lead to enormous upside in the future as we get past this crisis.

Our Top Picks

Based on these findings, here are three REITs that we are accumulating at the moment:

BSR REIT ( BSRTF /HOM.U) - I mentioned earlier that Barry Sternlicht's Starwood had recently bought shares of the apartment REIT Camden Property Trust. We like CPT, but we slightly prefer one of its smaller peers called BSR REIT. Both of them focus on strong sunbelt markets, but BSR is more focused on Class B affordable communities, which I expect to be less impacted by new supply hitting the market. Moreover, BSR is slightly cheaper, trading at a 50% discount to its net asset value, and the management is focused on share buybacks to create value for shareholders. The dividend yield is also attractive at 5% and it has historically been classified as "return of capital" to defer taxation.

BSR REIT

Branicks Group , mentioned above, is our Pick for office exposure in Europe. Just like Sternlicht, we think that there is an opportunity here. Branicks owns a portfolio of industrial and office properties in Germany. While we are not big fans of office, we are fans of Branicks Group's valuation. It is today priced at an estimated 70% discount to its net asset value due to its exposure to office properties. But those are actually performing quite well, and it owns even more industrial assets, which are today in high demand. Branicks is planning to sell some assets to pay near-term debt maturities and unlock value for shareholders. We think that the market will be surprised by Branicks' ability to monetize assets. Vonovia ( VONOY ), which is the biggest landlord in Europe, has been able to raise billions in asset sales this year alone. We think that Branicks could present more than 100% upside potential from here.

Branicks

The Macerich Company ( MAC ): Finally, we want to discuss a REIT that's become opportunistic because it is too heavily leveraged. It owns great assets, mainly Class A malls, but its 8.7x Debt-to-EBITDA is concerning the market and it is causing it to trade at a 60% discount to its NAV. But The REIT is making great progress deleveraging and expects its Debt-to-EBITDA to come down below 8x by the end of 2024. The REIT is also massively cash flow positive and retaining a bit chunk of it for deleveraging. What's the likelihood that lenders won't work with Macerich? I think that it is smaller than what's implied by its heavily discounted valuation. Lenders don't want to take possession of malls and Macerich's situation isn't that bad anyway. The upside potential could be very significant from here as Macerich keeps deleveraging its balance sheet.

Macerich

Bottom Line

Barry Sternlicht is seeing some " very good buys " in the REIT sector and is planning to launch a special situation fund to capitalize on these opportunities.

We are doing the same.

We have built a portfolio of what we believe are the best 25 opportunities in the REIT sector - aiming to maximize returns in the recovery - all while mitigating risks via diversification.

For further details see:

Billionaire Investor Says 'Buy REITs': Our Top Picks