BILS - BILS: Rolling 4 Months T-Bills In An ETF Format

2023-10-13 06:43:58 ET

Summary

- BILS is an ETF that tracks the Bloomberg 3-12 Month U.S. Treasury Bill Index, investing primarily in U.S. Treasury Bills with maturities between 3 and 12 months.

- BILS serves as a cash parking vehicle, offering a slightly higher duration compared to its competitors.

- It has an AUM of $2.8 billion, a 30-Day SEC Yield of 5.2%, a low expense ratio of 0.135%, and a duration of 0.38 years.

- Investors have various alternatives for their cash, including outright T-Bill purchases, bank CDs, and short-term corporate bond funds.

- BILS is positioned as a simplified operational alternative for rolling 4 months T-Bills outright.

Thesis

The SPDR Bloomberg 3-12 Month T-Bill ETF (BILS) is a fixed income exchange traded fund. The vehicle seeks to provide investment results that correspond to the price and yield performance of the Bloomberg 3-12 Month U.S. Treasury Bill Index (the "Index"). The index aims to provide investors with exposure to U.S. Treasury Bills that have remaining maturities between 3 and 12 months, and is rebalanced monthly.

BILS is a cash parking vehicle, but one that runs a duration profile that is just slightly higher than its competitors:

Duration (Author)

While the other funds invest mostly in T-Bills under 3 months, BILS takes the longer end of the 1-year curve. That will translate into the fund offering a higher yield once the Fed starts cutting. Similarly to the other two cash parking vehicles, BILS is made-up of AAA assets only:

Holdings (Fund Fact Sheet)

There is no credit risk to be had with this fund, just a slight duration risk. As rates stay higher for longer, the 30-day SEC yields for the above cohort is going to converge. SGOV for example, currently has a 30-day SEC yield only 8 bps higher than BILS.

If we look at the cohort's total return profile in the past year we can see very small total return differences:

BILS lags SGOV by 34 bps in the past year due to the slightly higher duration it ran during a tightening cycle. Expect the small differential to slowly narrow as rates stay higher for longer, and then revert once the Fed starts cutting.

Analytics

AUM: $2.8 billion.

Sharpe Ratio: -2.53 (3Y).

Std. Deviation: 0.63 (3Y).

Yield: 5.2% (30-day SEC yield).

Premium/Discount to NAV: 0%.

Z-Stat: n/a.

Leverage Ratio: 0%

Expense Ratio: 0.135%

Duration: 0.38 years

Composition: T-Bills

Alternatives for your cash balance

If we look at the U.S. Treasury curve we can observe it has flattened in the front end:

Yield Curve (Investing.com)

There are only small differences among the various tenors in the yield curve, thus the above mentioned ETFs are all very fungible currently. Buying BILS is akin to rolling 4 months treasuries, while buying SGOV is more akin to rolling 1-month treasuries. When rates stay at the same levels, the total returns for the instruments tend to converge.

Alternative 1: Outright T-Bill purchase

Some investors who do not mind the operational burden can purchase T-Bills outright via their brokerage accounts. Most brokerages offer services where they present the laddered T-Bill yields, and investors can purchase a CUSIP outright.

However, in this case a retail investor needs to be careful with the liquidity aspect. Many off-the-run T-Bills offer very poor liquidity, and if said investor wants to sell the holding before the maturity date, they might get very poor bid/ask levels that would greatly reduce their yield. It is thus preferrable to roll T-Bills (i.e. wait until their maturity date).

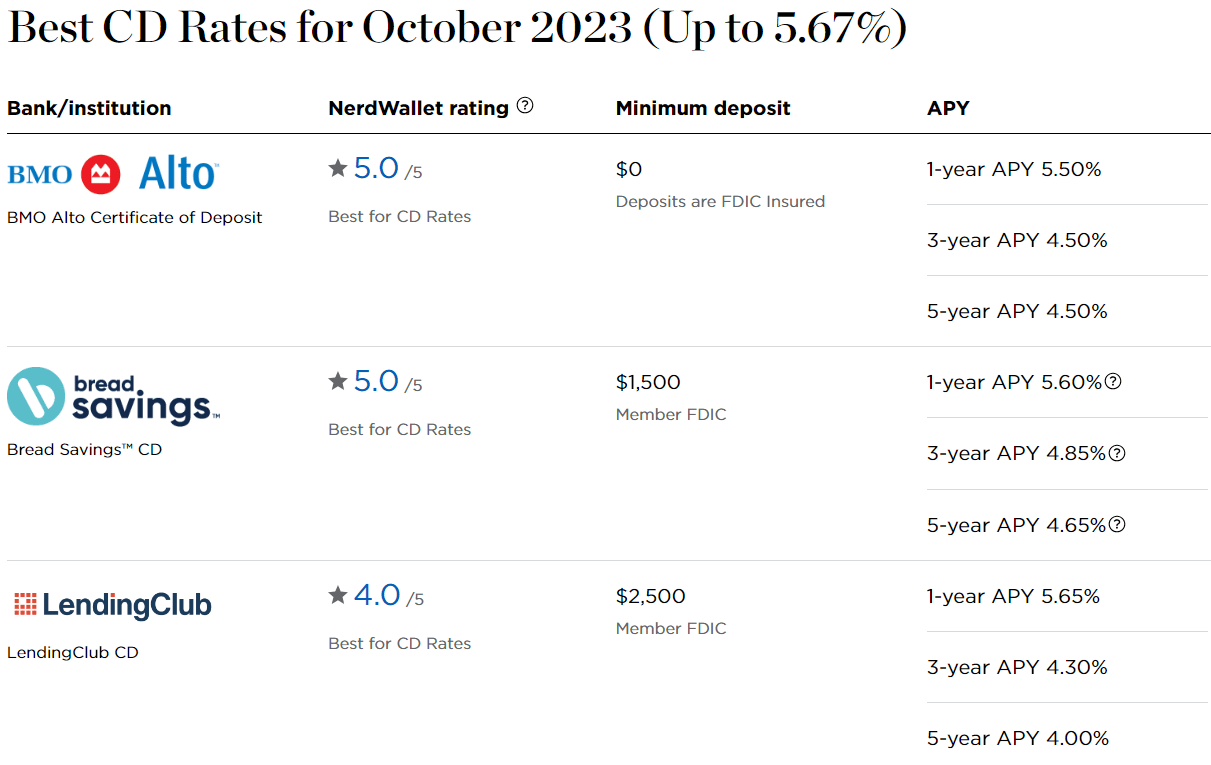

Alternative 2: Bank CDs

As the curve flattens and expectations mount for the Fed to start cutting mid-next year, bank CD levels have become less and less attractive:

{kind=link}

We can notice from the above table that 1-year bank CD levels are hovering around 5.5% to 5.65%, which is virtually in-line with the levels on T-Bills.

A retail investor should never purchase a bank CD if there is no risk premium to risk free assets. In a high rates environment we would expect at least 50 bps of premium.

Bank CDs are usually not redeemable early, and the need for cash and the unwind of the CD might end up with a full loss of interest on the instrument. Furthermore bank CDs are FDIC insured only up to $250,000:

Certificates of deposit (CDs) work like a savings account as a place to put specific amounts of money that will earn interest during a fixed period of time, often ranging from 30 days to five years. As with other bank accounts, the money in the CD is insured for up to $250,000 if the bank is a member of the Federal Deposit Insurance Corp. (FDIC).1

Alternative 3: Short Term Corporate Bond Funds

For retail investors who do not shy away from some default risk, one has the short term corporate bond fund alternative. We have covered some of these names before:

- PIMCO Enhanced Short Maturity Active Exchange-Traded Fund (NYSEARCA: MINT ) covered here

- The PGIM Ultra Short Bond ETF (NYSEARCA: PULS ) covered here

These funds offer 30-day SEC yields that are 50-80 bps higher than T-Bills, but also take some moderate corporate default risk. Their total return profile is slightly different, with a higher volatility and drawdown. BILS has a standard deviation of 0.63%, which represents a very low potential volatility.

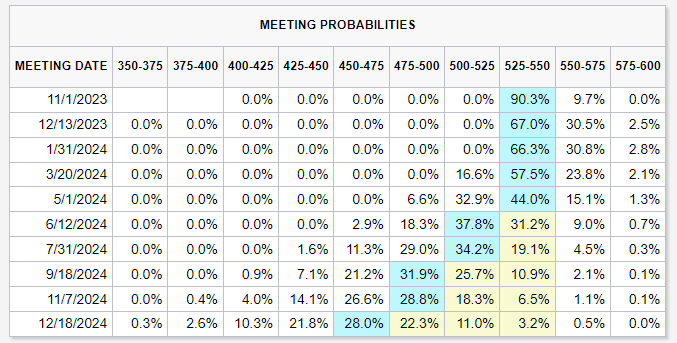

Where are rates going?

Another item to keep in mind when parking cash, is the distribution probability for higher rates. Many people are now talking about terming out their yield generating assets via longer dated treasury purchases. The market is currently telling us Fed Funds will stay elevated until mid-2024:

{kind=link}

The first potential Fed cuts are priced in for June/July now. Until that point in time, if the Fed does not raise rates again, expect BILS to produce a very high dividend yield, consistent with front rates.

Investors looking to get a risk-free treasury yield for many years to come, should look at longer dated alternatives, such as 5-, 10- and 20-year treasury bonds that can be purchased outright. These are ideal dividend generating instruments for investors just looking for cashflow, rather than factoring in duration and potential capital gains when rates move lower

Conclusion

BILS is an exchange traded fund. The vehicle invests in T-Bills with 3 to 12 months maturities, and represents a cash parking vehicle. The fund has a slightly higher duration than its peers BIL and SGOV, but as Fed Funds have plateaued, the 30-day SEC yield differential has narrowed in the cohort.

Expect BILS to keep paying a dividend yield close to Fed Funds until the Fed starts cutting rates. The fund will have a better lag than SGOV or BIL in producing larger yields once the Fed cuts due to its duration profile.

Retail investors have a number of alternatives at hand for their cash, with the article discussing the pros and cons for each one. We like BILS here and feel the fund represents a simplified operational alternative to rolling 4 months T-Bills outright.

For further details see:

BILS: Rolling 4 Months T-Bills In An ETF Format