BIO - Bio-Rad: Aggressively Buying In FY 2023

2023-04-13 11:12:23 ET

Summary

- Bio-Rad is back on the table as an attractive value proposition once again.

- The firm is well-positioned to unlock tremendous value for shareholders looking ahead, in my estimation.

- Profitability is a standout, and the Sartorius equity position is an embedded source of alpha.

- Net-net, rate buy at $526 valuation.

Investment summary

Following my last publication on Bio-Rad Laboratories, Inc. ( BIO ) several key updates have occurred. First, it posted FY'22 earnings with an interesting set of numbers. Equity markets have also caught a reasonable bid as well, where the January rally has maintained strength into Q2. Further, with the latest numbers, and the firm's profitability, I see BIO attractively priced at 19x forward EBITDA using consensus estimates and 1.4x book value. And finally, the Sartorius AG position has begun to revert to the mean as well.

Collectively, there's enough data on the table to "aggressively position against the name" once again, as I mentioned in the last publication. My numbers have baked in 5.6% revenue growth in FY'23 pulling down to a 7.8% YoY growth in operating income to $525mm (14.3% margin). Management also forecast ~$180mm in CapEx this year, and NWC increased by ~$360mm YoY in FY'22, but a $130mm CapEx isn't unreasonable in my estimates either. With favourable NWC changes, this could generate $678mm in cash for equity holders. In that vein, I see BIO fairly valued at $526 at the time being or ~24x my FY'23 earnings estimates or ~30x forward EBITDA. Net-net, rate buy.

Sartorius normalizing to range

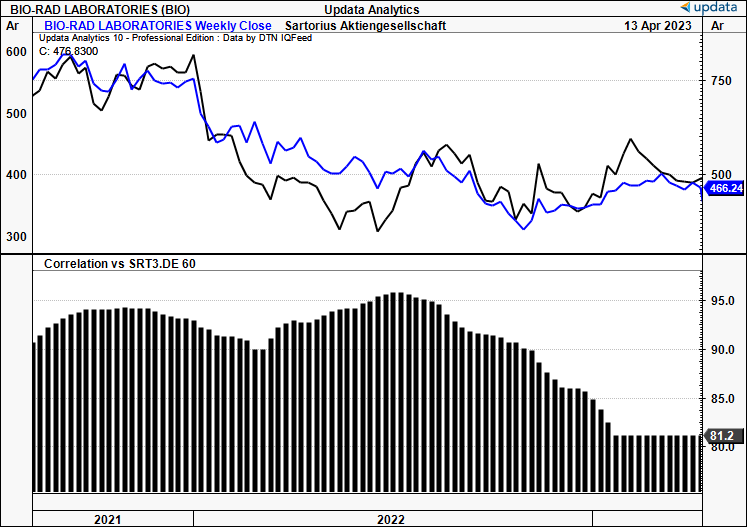

Key differentiator in the BIO investment debate is the equity position it holds in Sartorius AG. I've spoken about this at length in all 5 previous publications on BIO. As of December 2022, it held ~13mm common shares and ~9.6mm preferreds bringing its position to 37% of shares outstanding. It was marked at $8.47Bn in the firm's 10-K, down from ~$14Bn the year prior. You can see the correlation and performance in Figure 1.

Fig. 1

{kind=link}

The equity position BIO holds is reverting to a longer-term range after incurring the $5.2Bn unrealized loss in FY'22. This resulted in a reported net loss of ~$3.6Bn, however, this is a poor reflection of its operating performance. BIO's accounting gets tricky below the EBIT line given it books equity investment gains and losses above profit before tax on the income statement. So it's best to look at EBIT as a cleaner measure. I'd also point out a loan receivable tied to Sartorius of ~$980mm booked as non-operating income as well.

Two additional points to consider with this embedded source of alpha:

- It is an embedded source of alpha in BIO's stock price . One can't discount this investment as a way BIO will continue unlocking value into the future. The risk is on the downside, that's for sure - but high risk/high reward in this respect. For example, any 10% appreciation would result in a $0.85Bn gain in the marked value of its equity securities (as reported in FY'22). Same on the downside. Both shares have performed well this YTD and BIO has rallied 24% in the last 6 months with Sartorius' performance. Sartorius has a consensus price target at €460 and the stock is currently trading at €323.

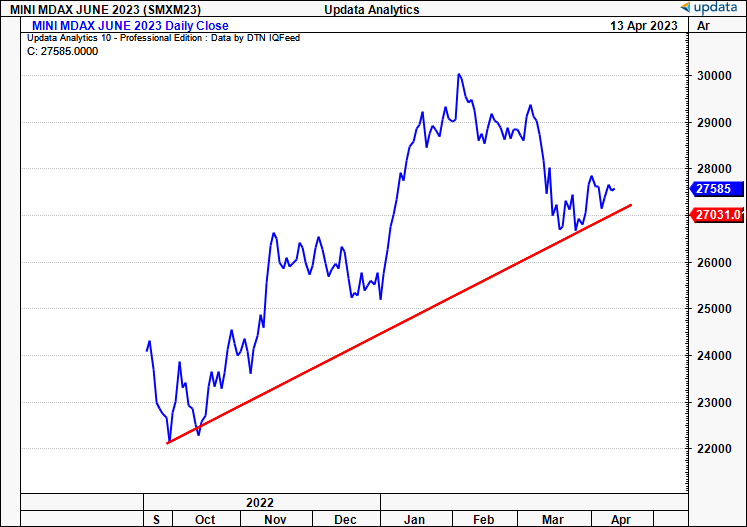

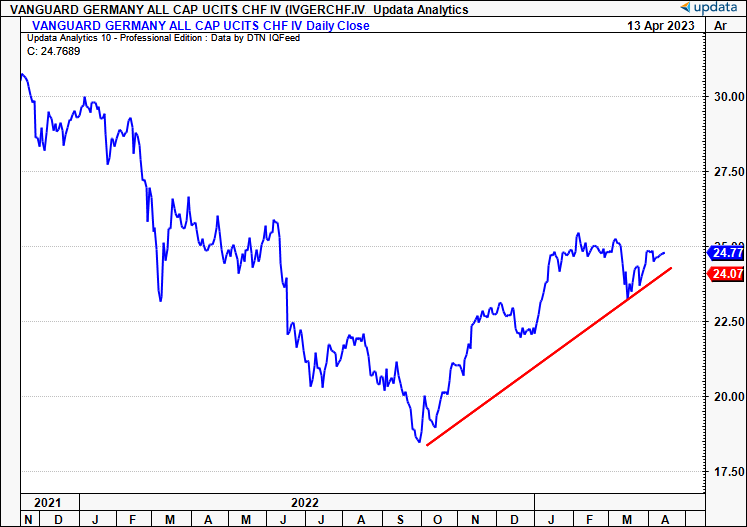

- The Germany situation has regained control as well after Covid-19 breakouts, inflation, and energy volatility have plagued its economy for the last 2 years . The EU's finance committee forecasts 0.2% real GDP growth in FY'23 and 1.3% in FY'24, revised up from a -0.6% forecast made last year. Inflation is expected to revert to 2.4%. Such has been the positive reaction for the revisal, DAX mini futures expiry for June has been on a tear since last year, along with the Germany all-cap index.

Fig. 2

{kind=link}

Fig. 3

{kind=link}

BIO to compound owner earnings

I've mentioned in the past that BIO is a long-term compounder that throws off high amounts of cash for its equity holders (not to mention the unrealized gains to create further value). In FY'22 it printed $194mm in operating cash flow - way below historical averages - after making several cash payments to interest, tax, and operating expenditures. Moreover, NWC requirements intensified by ~$360mm as cash collection was tighter and the firm expanded its inventory base. Further, it made another $112mm in net CapEx and I estimate it reinvested ~16% of its post-tax earnings for growth this year.

Operating leverage

Revenue growth slowed to negative 4.1% last year, with $2.8Bn booked at the top-line last year on gross margin of 56%. Segment performance wasn't brilliant, given the large pullback in Covid-19 related turnover and higher OpEx tied to cost inflation and manufacturing (Figure 4).

Fig. 4

Data: Author, BIO 10-K

Nevertheless, consider these points:

- Excluding last year, BIO has continuously produced strong operating leverage whereby each turn in revenue growth has ratcheted up operating profit at tidy multiples since FY'17 at least.

- Hence, the more business it does, the more operating profit it generates on a marginal basis as well.

- This is critical in the BIO investment debate as, using first principles, it's best to analyse the company's operations at the EBIT line and above, to separate out the Sartorius factor.

- Looking ahead, my numbers call for 5.6% in revenue growth in FY'23, which could lift operating income by 7.8%; 4.6% and 15.5% in FY'24 respectively, at 1-1.4x operating leverage.

Fig. 5

Data: Author, BIO 10-K

Return on growth capital (investments) is a competitive advantage

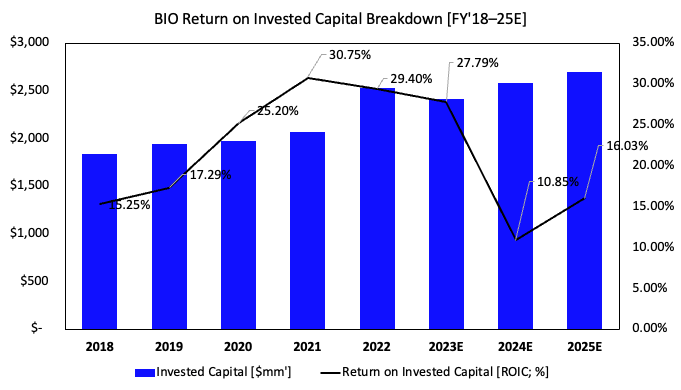

Further to the core of it, BIO continuously generates substantial returns on the capital it invests for growth. Even with a tough year in respect to growth and its equity holding, the firm generated 29% ROIC.

Here, I've capitalized its R&D investment that is expensed on the income statement, meaning BIO generated $743mm in NOPAT for the year. I believe this is the correct way to treat the R&D investment as it is invested to generate additional revenue and earnings growth in the future.

Given the ROIC was above the cost of capital, the following points are relevant:

- It was still a very profitable year for BIO's shareholders. You can see from Figure 6 the economic profit (ROIC less WACC charge) it has generated for shareholders these last years.

- My estimates point to further economic profitability into FY'25, with 22% ROIC/WACC spread this year. This bodes in well with BIO's growth route and would generate shareholder value in my estimation.

- Given the estimates for economic profits, BIO's organic growth potential is certainly accretive to its valuation, in my estimation. This is excluding the Sartorius factor.

Fig. 5

{kind=link}

Fig. 6

Data: Author, BIO 10-K

Incremental Effects of competitive advantage

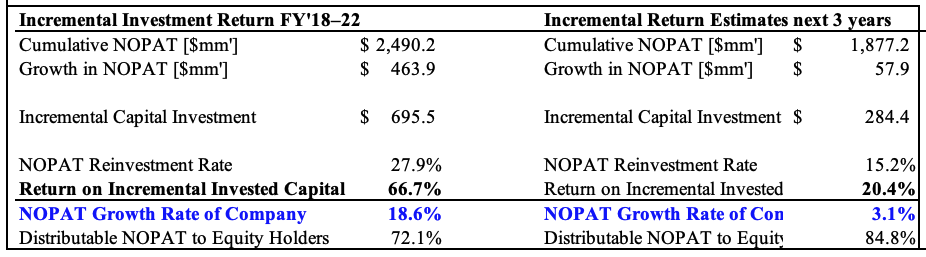

The incremental effects of this profitability since FY'18 have been tremendously constructive as well. I opt to use this window given it spreads 2 years prior to the pandemic, and 2 years after, and 1-year with the macroeconomic impact. This gives a normalized result, by estimate. Over this time, the firm has generated profitable revenues while throwing off plenty of cash to shareholders.

To illustrate, from FY'18-22', the firm invested an additional $695mm towards growth capital. This equates to ~28% of post-tax earnings. It also generated a cumulative $2.5Bn in NOPAT, reflecting the operating leverage raised above. These capital investments generated a 67% incremental rate of return, at a 28% cost to shareholders (see: Figure 7).

As a reminder, a firm generates more cash and value for its owners when it generates an economic profit. Typically, this occurs when the return on its growth investments is above the cost of capital. But the frictional costs to investors (i.e., reinvesting a percentage of the profits) shouldn't come at too high a cost to shareholders.

With that in mind, consider the following:

- BIO reinvested at 28% for a c.67% return, meaning there was a net gain in owner earnings over this time.

- The company's growth over this time was 18.6%, meaning it could expand at this rate sustainably.

- Further, as owner earnings, ~72% of reported earnings were attributable to shareholders - this is a solid conversion in my opinion.

- This bodes in tremendously well for the future outlook for equity holders.

In addition to that, the firm hasn't required more than $150mm in additional CapEx per annum to generate its profit growth over the last 5 years. Even during Covid-19, capital requirements were between $108 and $133mm, coming to $112mm last year. As equity investors, we want to be in a company where capital doesn't produce the profits, or if it does, it's only required in small amounts. So the relatively low CapEx and Invested Capital requirements are extremely attractive in BIO's business economics - it doesn't require a large investment into maintenance or new capital in order to grow profits for shareholders.

Growth factors to consider + Valuation

Valuing BIO on a merit of its own characteristics, i.e., less the Sartorius factor, comes down to the contribution from its current operations and contribution from growth.

With respect to the growth contribution, as seen in Figure 7, looking ahead I believe BIO can unlock tremendous value for shareholders. Along with a shift towards higher-margin income (due to no Covid-19 revenue) I opine this to reduce its capital intensity and therefore BIO will require less capital to generate its profits. This touches on the points raised just earlier.

Fig. 7

{kind=link}

There are three major facts that must be considered to BIO's growth contribution and valuation upside:

- For the next 3-years, my numbers suggest that BIO could pare back its reinvestment rate to 15% to generate a 20% incremental return on new capital. Whilst company growth will likely slow from this, BIO could likely throw off 85% of its post-tax earnings ($1.6Bn) as free cash to equity holders at this time. Herein lies the main value I foresee in the BIO investment debate, as it will attract a higher market multiple in my opinion.

- The firm will continue growing inventories as it transitions manufacturing operations to Singapore. This means more cash tied up in NWC but I see this offset by two main reasons. One, the higher cash collections and a reduction in accounts receivable from this year. Two, the fact BIO will likely keep up with demand and work through its backlog at a faster pace. Hence, I see a decrease in NWC requirements to hit $~$2.95-$3Bn in revenues. The move could potentially equal higher CapEx than what I've estimated, ($127mm vs. $180mm forecast from management) but the ROIC will be above the cost of capital in my estimation anyway.

- The firm has a strong pipeline across a number of its major markets for the QX600 assay. This is coupled with a positive growth outlook for its Droplet digital PCR portfolio this year. Collectively, the firm is well-positioned to deliver many conversions from its pipeline over the next 12-24 months.

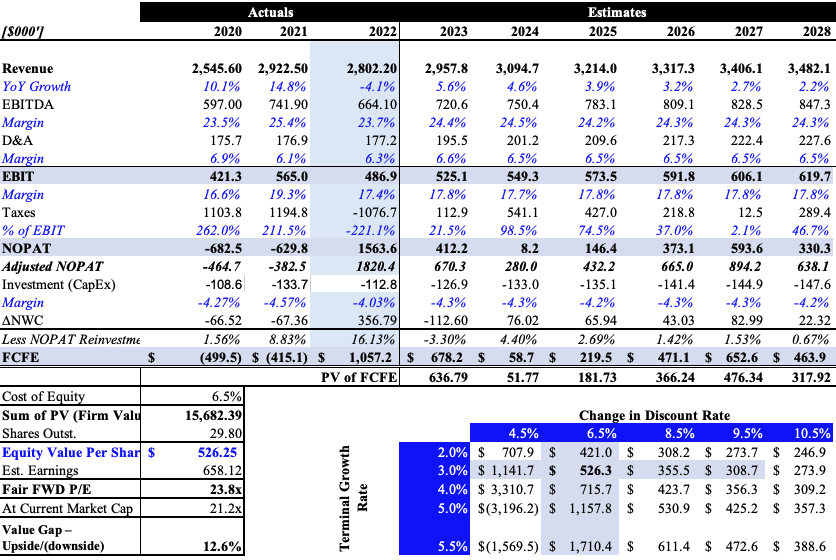

Looking out to the next 5 years, my estimates point to $3.3Bn in top-line revenues by FY'26 and BIO to continue driving owner earnings. The stock trades at 19x forward EBITDA and comes in at a premium to the sector, but is attractively priced at 1.4x book value in my opinion given the Sartorius factor.

My conclusions with BIO's valuation, that project owner earnings to FY'28 to reduces forecasting risk, is as follows:

- The stock is valued at $526 per share on a discount rate of 6.5% (current WACC hurdle) and 3% terminal growth rate. Adding a higher risk premium for Sartorius at an 8.5% hurdle rate compresses the valuation substantially, same with reducing it to 6%.

- At my FY'23 earnings and EBITDA estimates, this gives me a ~24x fair P/E and ~21x EBITDA. Without adjusting for R&D, this would be 29x EBITDA.

- To generate these multiples, the company would have to benefit from a $112mm reduction in NWC requirement and ~$127mm in CapEx, as mentioned.

- Keep in mind, these numbers exclude the Sartorius impact. With this in mind, there's scope for BIO to rate even higher.

Fig. 8

{kind=link}

In short

BIO continues to present with compelling value. My estimates show that it can continue creating future value for shareholders, with its Sartorius position creating an embedded source of alpha. Should it convert on this, I see BIO valued at $526 today or ~21-29x forward EBITDA (depending on how you treat R&D). As such, this warrants a buy rating and I look forward to providing further coverage.

For further details see:

Bio-Rad: Aggressively Buying In FY 2023