BIO - Bio-Rad And Its Real Value

2023-05-16 06:18:15 ET

Summary

- Bio-Rad previously experienced a significant jump in sales due to Covid-19 testing.

- However, with Covid-related sales falling off, the overall revenue has also been reduced in 2022.

- Bio-Rad has experienced wild volatility in recent months, which has investors waiting for the business fundamentals to normalize.

- This article focuses on the fundamentals, the real value versus the current share price, and whether BIO stock is worth investing in.

Bio-Rad Laboratories, Inc. ( BIO ) has experienced a rise in revenue growth in recent years thanks to strong sales of its Western Blotting, Digital PCR, and Process Media life science products. Several of these products were employed in Covid-19 research and testing, while increased utilization in lab operations supported clinical diagnostics sales. However, the first half of 2022 has seen a drop in revenue by 3.6% due to a reduced contribution from Covid-19-related sales and forex headwinds.

Despite periods of Bio-Rad’s steady revenue growth, the company’s operating margin has exhibited great volatility. It rose from 6.6% in 2017 to an astounding 185.4% in 2021 before experiencing a sharp fall to -91.4% in the most recent twelve-month period. This fluctuation can be attributed to changes in the fair market value of equity and debt securities, drastically impacting the company’s profits.

In May 2023, Bio-Rad experienced its biggest selloff in 36 years after disappointing earnings results. The stock price dropped 17.5% from its previous close.

While the company experienced negative earnings growth of -185.57% in the past year, this year has seen a positive growth of 8.74%. The projected earnings growth for the next five years is around 17%, which suggests a positive outlook for the company’s future.

When considering these current stories about BIO, we need to determine which news topics will have a long-term and ongoing effect on the company and its share price. Despite the management taking appropriate measures and exerting maximum effort to enhance and transform their business models, management may still need regain investors’ trust due to the company’s weak performance and volatility.

While current news stories, good or bad, can sway our opinion about investing in a company, it’s good to analyze its fundamentals and see where it’s been in the past and in which direction it’s heading.

This article will focus on the company’s long-term fundamentals, giving us a better picture of the company as a viable investment. I also analyze the company’s value versus the price and help you determine if BIO is currently trading at a bargain price. I provide various situations which help estimate the company’s future returns. In closing, I will tell you my opinion about whether I’m interested in taking a position in this company and why.

Snapshot of the Company

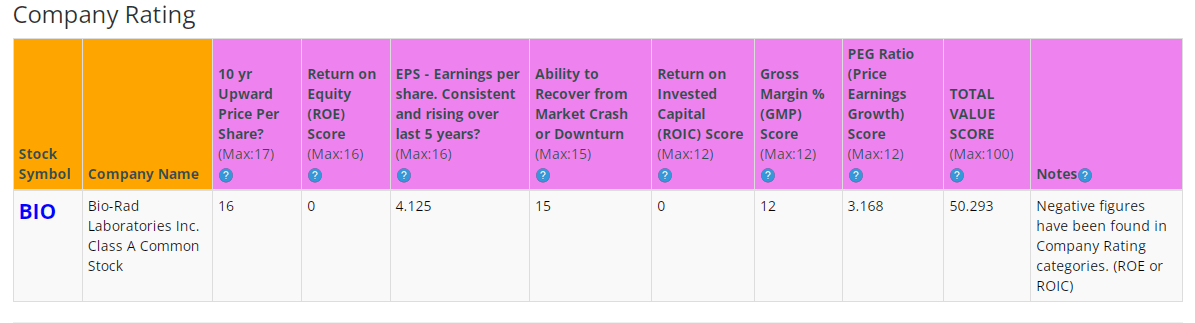

A fast way to understand the business’s condition is to use the BTMA Stock Analyzer’s company rating score. BIO’s overall value score of 50 out of 100 tells us that there are likely serious issues with this company.

{kind=link}

Before jumping to conclusions, we must look into individual categories to see what’s happening.

Fundamentals

Analyzing the share price over the years, we can observe a steady increase from 2014 to 2021. Afterwards, share price has fallen in 2022 and 2023 as Covid-related revenues have dropped off.

Overall, the share price average has grown by about 286.3% over the past 10 years or a Compound Annual Growth Rate ((CAGR)) of 16.2%. Even with the recent share price decline to around $380, the stock has still experienced an annual growth of 13.5%.

BTMA Stock Analyzer

Earnings

In a similar fashion to the price per share, earnings have also increased continually until 2022 when earnings fell as Covid-related revenues dropped off.

The most earning growth happened from 2019 to 2020 when the company doubled its earnings. This was due to increased COVID cases and an urgent need for medical supplies.

The good news is that aside from COVID-19-related sales, revenues increased 3.1% over last year, as there has been increased demand for diagnostic instruments related to blood typing and diabetes.

Also on a positive note, Bio-Rad’s poor recent earnings performance isn’t as bad as it looks. There were multiple non-recurring items that affected Bio-Rad’s recent earnings. For example, Bio-Rad experienced “a negative impact to its quarterly results of $17.5 million related to a change in fair market value of equity securities holdings related to its ownership of Sartorius shares .”

BTMA Stock Analyzer

Since earnings and price per share don’t always give the whole picture, it’s good to look at other factors like gross margins, return on equity, and return on invested capital.

Return on Equity

Bio-Rad’s Return on Equity shows great volatility within the past 5 years. For instance, ROE began around 10%, jumped to about 50%, and has recently fallen to about -31%.

BTMA Stock Analyzer

I will argue that the past 5 years have not been a normal time period for Bio-Rad. Because of Covid, earnings and therefore ROE values have been greatly skewed.

This has caused the 2019 to 2021 values to be greatly exaggerated on the upside, then after Covid sales fell in 2022, the ROE was exaggerated in the opposite way.

To get a better idea of the normal ROE of Bio-Rad, let’s look at the past 10-year history.

{kind=link}

The period of 2013 to 2018 shows a more normalized look at ROE for Bio-Rad. We can see that typically, the company has an ROE of 4% to 8%.

When analyzing companies, I look for an average return on equity of 16% or more. This means that in a more normal situation, Bio-Rad would not pass my ROE requirement.

Return on Invested Capital

The ROIC also has the same exaggerated effect in the past 5 years because of Covid.

BTMA Stock Analyzer

But if we examine the past 10-year history, we can see that the typical ROIC is about 7% to 10% from the non-Covid era of 2013 to 2018.

{kind=link}

When analyzing companies, I look for an average ROIC of 16% or more. Therefore, Bio-Rad fails my ROIC requirement as well.

Gross Margin Percent

The GMP from 2018 to 2022 remained within the mid 50 percent range. Actually, for the entire 10-year history, Bio-Rad’s Gross Margin Percent has stayed around 55%.

I typically look for companies with gross margin percent consistently above 30%. Therefore, Bio-Rad easily passes this test and proves that it has the ability to maintain impressive margins over the long term.

BTMA Stock Analyzer

Financial Stability Indicators

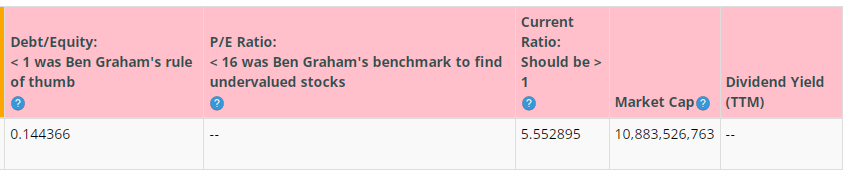

Looking at other fundamentals involving the balance sheet, we can see that the debt-to-equity is less than 1. This is a good sign, meaning that the company owns more than it owes.

Additionally, the company has a very strong current ratio of 5.5, which means that the company can easily pay off its short-term liabilities with its available cash.

According to the balance sheet, Bio-Rad is a very healthy and stable company.

Bio-Rad does not pay a regular dividend.

{kind=link}

This analysis would only be complete by considering the value of the company vs. share price.

Value Vs. Price

Estimating the actual value of this specific stock can be challenging due to its unreliable valuation. The unreliable valuation is a result of volatile earnings and losses caused by Covid-related sales.

{kind=link}

For more detailed valuation purposes, I will use a pre-COVID conservative EPS from 2018 of $12.10. I’ve used various past averages of growth rates and PE Ratios to calculate different scenarios of valuation ranges from low to average values. The valuations compare growth rates of EPS, Book Value, and Total Equity.

In the table, you can see the different scenarios, and in the chart, you will see vertical valuation lines corresponding to the table valuation ranges. The dots on the lines represent the current stock price. If the dot is towards the bottom of the valuation range, this would indicate that the stock is undervalued. If the dot is near the top of the valuation line, this will show an overvalued stock.

BTMA Wealth Builders Club BTMA Wealth Builders Club

This valuation analysis assumes that Bio-Rad is able to settle back into its more normalized pattern of business, with annual earnings of $12.10, which were the pre-Covid levels of 2018.

The most recent non-GAAP quarterly earnings of $3.34 would indicate that four quarters of this pace of earnings would produce annual earnings of $13.36, which is very similar to the 2018 earnings.

From my observation, this earnings level is within reason. Nobody knows when Bio-Rad will return to its norm. But in my opinion, using the above earnings estimates gives a more reliable indication of what the stock is worth during a normal situation.

Otherwise, if we try to determine a valuation based off its 2022 negative GAAP earnings of $-129.79, it will be too unreliable.

Overall, the most valuation models that I’ve used have indicated that Bio-Rad is overpriced.

Summarizing the Fundamentals

To sum it up, Bio-Rad’s fundamentals are lacking. Earnings are volatile and management and investors can make up excuses as to why the company’s earnings aren’t as good as they should be. But the simple truth is that earnings are not consistently increasing, and the stock is unpredictable.

Return on Equity and Return on Invested Capital are not at sufficient levels now and actually, they haven’t been great over the past 10 years.

The main strengths I see with Bio-Rad are its impressive Gross Margins and balance sheet. The company is heavy on equity and cash. It’s a stable business, but difficult to value.

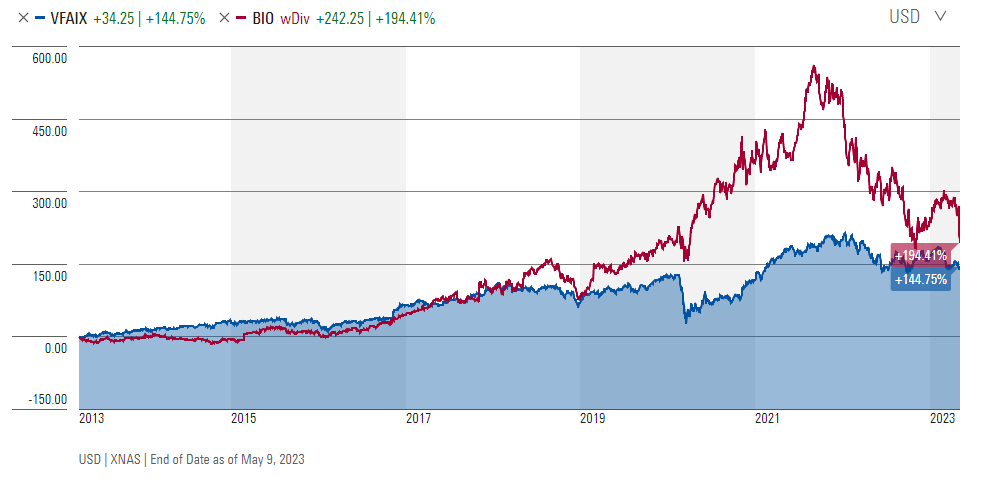

BIO Vs. The S&P 500

Let’s see how BIO compares to the US stock market benchmark S&P 500 over the past 10 years.

As depicted in the chart below, Bio-Rad has slightly underperformed against the S&P 500 benchmark in normal situations. But when Covid boosted sales, the company outperformed the benchmark. As Covid-sales fell, so did the share price.

We can’t rely on future pandemics to boost earnings. Therefore, we need to focus more on the normal times (pre-Covid). These normal times tell us that in most cases, an investor would experience a slightly better return investing in the S&P 500 instead of putting their money into Bio-Rad. Additionally, the S&P 500 offers more diversity and safety than investing in this one unpredictable company.

{kind=link}

Forward-Looking Conclusion

Over the next five years, analysts are expecting it to see its growth to an average annual rate of 17.80%. A 17.80% gain per year would be substantial and if it really does happen, that could mean that there might be money to be made with Bio-Rad. But the uncertainty of the company leaves an investor open to added risk.

Does BIO Pass My Checklist?

- Company Rating 70+ out of 100? No (50.2)

- Share Price Compound Annual Growth Rate > 12%? YES (16.2%)

- Earnings history mostly increasing? No

- ROE (average 16% or greater)? No (4% to 8%)

- ROIC (average 16% or greater)? No (7% to 10%)

- Gross Margin % (5-year average > 30%)? YES (55.2%)

- Debt-to-Equity (less than 1)? YES (0.14)

- Current ratio (greater than 1)? YES (5.5)

- Outperformed S&P 500 during most of the past 10 years? No

- Do I think this company will continue to successfully sell the same main product/service for the next 10? YES

BIO scored 5/10 or 50%. Therefore, BIO shouldn’t be an option worth considering for most investors.

Is BIO currently selling at a bargain price?

- Price Earnings less than 16? YES (3.16 or less)

- Is the estimated value greater than the Current Stock Price? No ( Unrealistic valuation)

In conclusion, Bio-Rad is a healthy company in terms of its balance sheet, and it proved to be a profitable investment during the Covid outbreak. However, as Covid-related sales have fallen, the company will eventually return to a norm that is less profitable. In my opinion, there are more profitable companies available to invest in that offer more consistent and improving fundamentals. I’ll seek out those more reliable and less risky investments, which can outpace the market.

For further details see:

Bio-Rad And Its Real Value