BIO - Bio-Rad: Business Returns Aren't Economically Valuable Sartorius Now A Hindrance

2023-10-24 22:33:48 ET

Summary

- Bio-Rad Laboratories' investment returns are expected to be hindered by economic and technical factors.

- The company's large ownership in Sartorius AG has been a hindrance due to the latter's poor performance and high correlations between the pair.

- Bio-Rad's business returns are not attractive nor economically valuable, leading the market to push its equity value further to the downside.

Investment update

Forward investment returns for Bio-Rad Laboratories, Inc. ( BIO ) look to be hampered by a number of economic and technical factors, as will be discussed in this report.

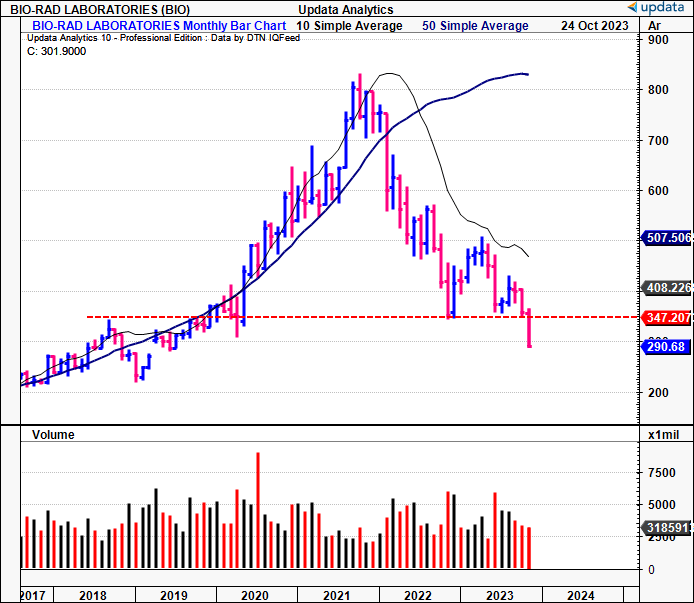

The thesis laid out in my April publication has not played out as one would have hoped, and its stock price has sold off nearly 38% to the downside as I write. It has now broken a key support level and trades below its 2019 range. Entry multiples are still hefty, and investors are asking ~24x forward earnings and 19x forward EBIT to sell BIO today, without the economic characteristics to back this premium up.

BIO faces a number of fundamental headwinds that must be dealt with in order to show conviction as a buy rating. Here, I will lay out the reasoning as to why I've revised BIO to a hold, having taken a small loss on the position. Net-net, revise to hold.

Figure 1. BIO long-term returns, now broken key support levels (monthly bars shown).

{kind=link}

Background of BIO ratings

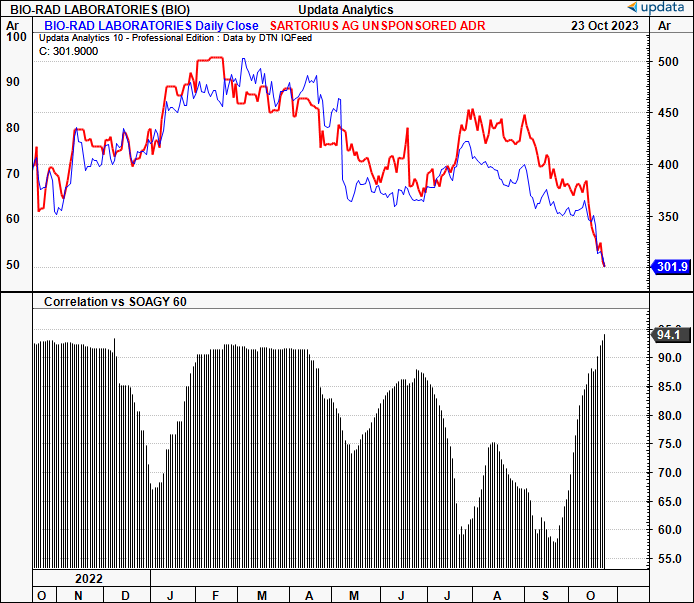

A critical factor in the BIO investment debate is its large ownership in German listed medical + biotech process technology company Sartorius Aktiengesellschaft ("AG"). As of Q2 FY'23, the company owned 38% of the common equity in Sartorius AG and 28% of the preferreds outstanding, which is booked under "gains/losses in equity securities" on the income statement. It therefore books unrealized gains/losses as profit or loss to net income. For reference, the Sartorius family owns the remainder through its family trust.

This had been a key differentiator for BIO while equity markets were bullish. Since markets have corrected, however, it has been a large hindrance, given (i) the poor performance of Sartorius' equity on the DAX, and (ii) the high correlations between both securities, as shown in Figure 1a. According to BIO's Q2 FY'23 10-Q:

Losses from change in fair market value of equity securities and loan receivable [all related to Sartorius] was $1.61 billion and $5.88 billion for the first half of 2023 and 2022, respectively. The change in the fair market value primarily resulted from the recognition of lower holding losses of $1.60 billion in the first half of 2023 compared to holding losses of $5.73 billion in the first half of 2022 on our position in Sartorius AG.

I had argued extensively back in 2020 about the importance of analyzing BIO on its own merits and this is the reason why. A c.$6Bn loss on equity investment impacting earnings is now well received by the market.

In addition to these points:

- The company is now heavily indebted, with $1.8Bn in long-term debt on the balance sheet,

- The bulk of its gross asset value—61% to be exact—is comprised of the Sartorius equity ownership,

- This has proven to be volatile, and is not a productive asset to BIO's business returns,

- Stripping this out, total assets cover liabilities just 1.3x, and the company's equity value drops from $8.44Bn in Q2 to ~$1.13Bn.

Each of these factors paints a mediocre picture when thinking of the current macroeconomic and geopolitical climate.

Figure 1a. BIO-Sartorius correlations, now back at nearly perfect correlation.

{kind=link}

Critical facts pattern to revised thesis

1. Price implied expectations

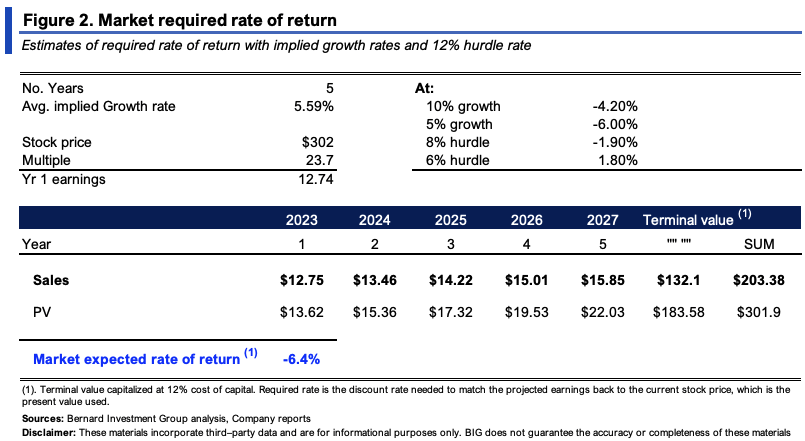

At a market value of ~$302/share ($8.86Bn market cap) and trading at 23.7x forward earnings , the market expects $12.75/share in FY'23 earnings, an 11.6% decrease. It sells at 19.1x forward EBIT and 3.12x sales. Consensus earnings growth expectations average 5.6% out to FY'25, which I believe is fair to continue out to FY'28. The market also expects:

(i). FY'23-'24 sales of $2.84Bn, ~1.3% YoY growth. Management is eyeing 80bps YoY sales growth,

(ii). FY'23-'24 pre-tax earnings of $463.8mm, a 4.7% decrease from FY'22,

(iii). Based on the implied earnings figures, the market expects a return of negative 6.4% on BIO over this time, ranging from negative 6.4% to a positive return of 1.8%, depending on various scenarios (Figure 2). The market's expected rate of return is the discount rate needed to match the projected earnings back to the current stock price (the present value).

BIO is also priced at 2.2x EV/invested capital, and produced ~8% trailing ROIC last period (discussed later). The implied ROIC by the market is thus 3.5% going forward (1/(2.2x7.9%) = 3.5%). The market expects BIO to further divest capital from the business, at a rate of ~75% of expected pre-tax earnings, otherwise ~$347mm. Based on this calculus, it expects a reduction in intrinsic value of ~2.6% moving forward (3.5% x -75% = -2.6%).

{kind=link}

2. Economic value drivers

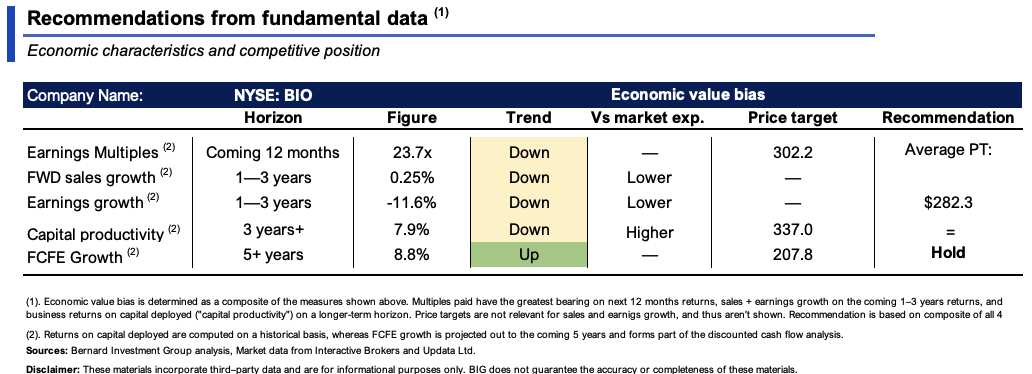

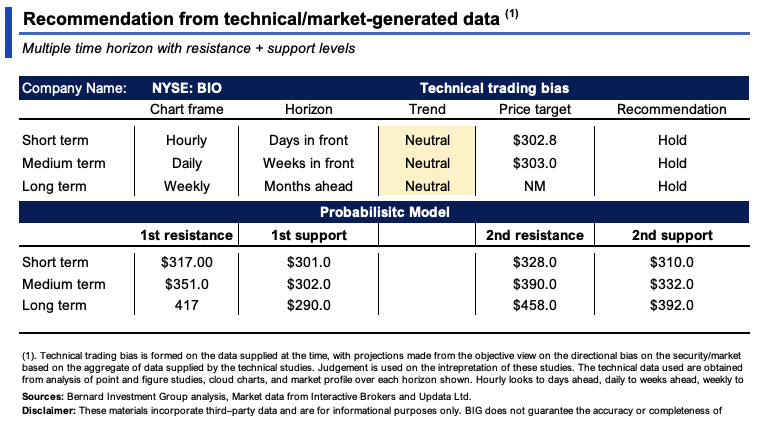

Shown below are the recommendations over short to long-term investment horizons based on the culmination of BIO's economics + fundamentals.

Figure 3.

{kind=link}

The most important investment facts to these ratings are the following:

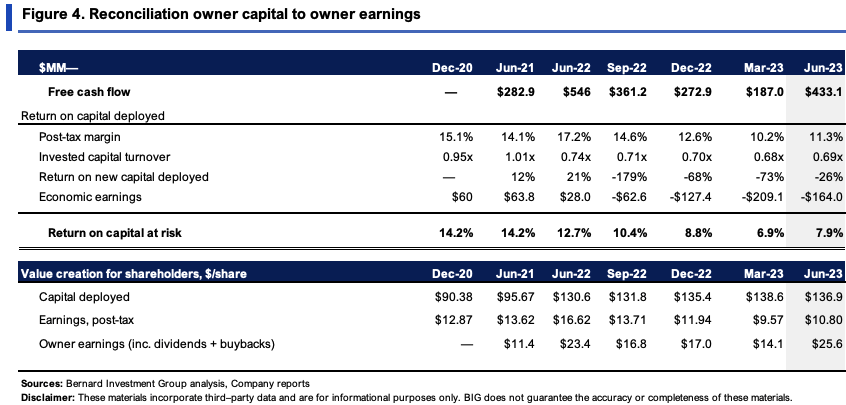

- BIO is producing no growth in business returns. It had ~$137/share of capital invested directly in the business as of Q2. This produced $10.80/share in trailing NOPAT, just a 7.9% return on investment. Note that this excludes the Sartorius investment. The numbers are much tighter with its inclusion.

- Both post-tax margins and capital turnover are unattractive, suggesting poor business economics. The former came in at 11.3% last period, the latter at 1.01x. Both are trending down (Figure 4).

- In the last 3 years, sales have compounded at 80bps per period, on operating margins of 19%. But each $1 in new sales required over $5.78 of investment to get there. The major capital allocation is to NWC—$4.70 on the dollar for each $1 in sales growth. Flat growth on a growing capital base isn't attractive economics. Again, this excludes any Sartorius figures.

- Should it continue at this steady state—which is fair in my view, based on management's forecasts—it could do $478mm in pre-tax earnings, statistically in line with the market's view. It would spin off 8–9% ROIC, above what the market implies, but would compound its intrinsic value at ~80bps, not a wide margin from the implied expectations from earlier.

- In addition, it could grow the cash thrown off to shareholders by 8-9% over the coming years, not enough to corroborate a buy rating at this stage.

Regarding value creation from operations, BIO is not creating economic value for its shareholders. We use a 12% threshold for business returns across all equity holdings. As seen in Figure 4, it has not met this mark since 2022. Hence, the company's post-tax earnings are not economically valuable, and these trends look set to continue.

{kind=link}

3. Technical considerations

Market-generated data is equally unsupportive of a bullish view. The summary of ratings + key levels is seen in Figure 5.

Figure 5.

{kind=link}

Support for these ratings is observed in the following data sets. Related to Figures 6 and 7:

(1). Tracking BIO's quarterly market profiles from Q1–Q3, it is clear the bulk of distribution was in the $370–$400 region. With the break to ~$300, a new area of usage has been formed.

(2). Markets tend to move from pockets of high usage to low usage, and there is a clear pocket of low usage in the current region of price distribution.

(3). It is reasonable to therefore expect this zone to be filled, pointing to a range of $300–$350, an unfavourable risk/reward at the current entry points. Figure 6a illustrates the breadth of distribution more clearly.

(4). As a result, we have price targets in the $302–$303 region, in line with where the stock currently trades. These are confirmed on the point and figure studies across all time frames (the daily is shown in Figure 7). The P&F studies have captured each move well, adding validity to their use.

Figure 6.

Data: Updata

Figure 6a.

Data: Updata

Figure 7. Targets to $303 on the medium-term horizon, in line with where stock currently trades.

Data: Updata

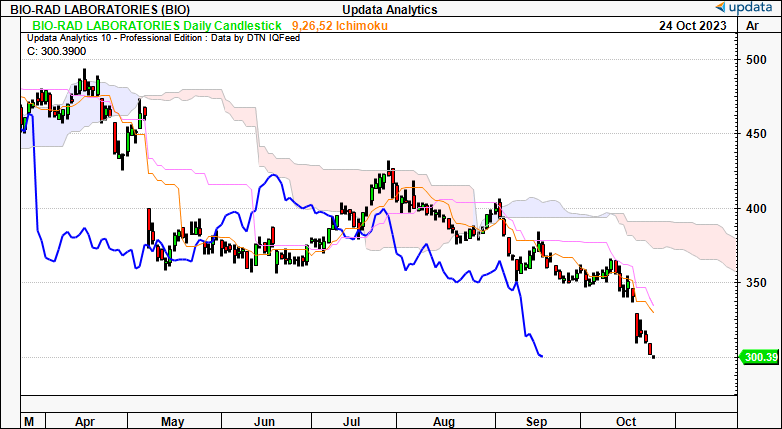

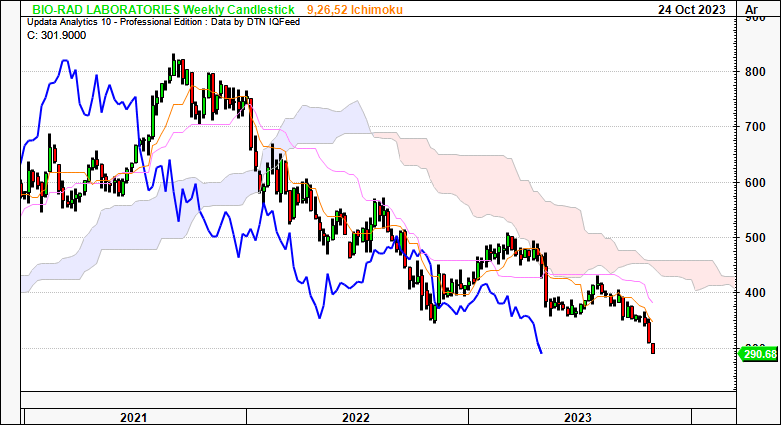

Meanwhile, trend action is not seen and both medium and long-term time frames point to a period of either congestion sideways or further downside. Figures 8 and 9 depict this on the daily and weekly cloud charts respectively.

Price levels have been capped at resistance, and 2x attempts to break through the cloud top have been rejected quite severely. We need a move and nudge above $350 to suggest a bullish reversal. So with prices gapping further to the downside from this level, this is a major technical hurdle to overcome.

Figure 8. Daily cloud chart

{kind=link}

Figure 9. Weekly cloud chart

{kind=link}

Valuation and conclusion

Based on findings thus far, it would appear there are multiple layers of evidence supporting the market's pricing of BIO. The stock still sells at ~23-24x forward earnings and 19x forward EBIT, multiples I cannot wrap my investment cortex around given the economics outlined here.

Added to this:

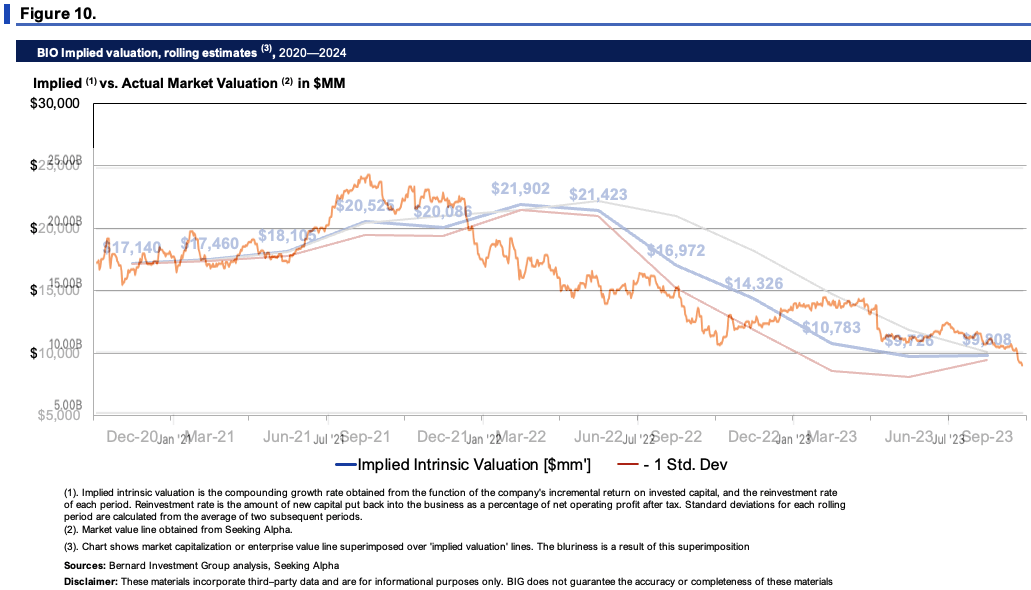

- Compounding BIO's intrinsic value at the function of its ROIC and reinvestment rates to date shows the market has been an accurate judge of the company's fair value (Figure 10, top chart),

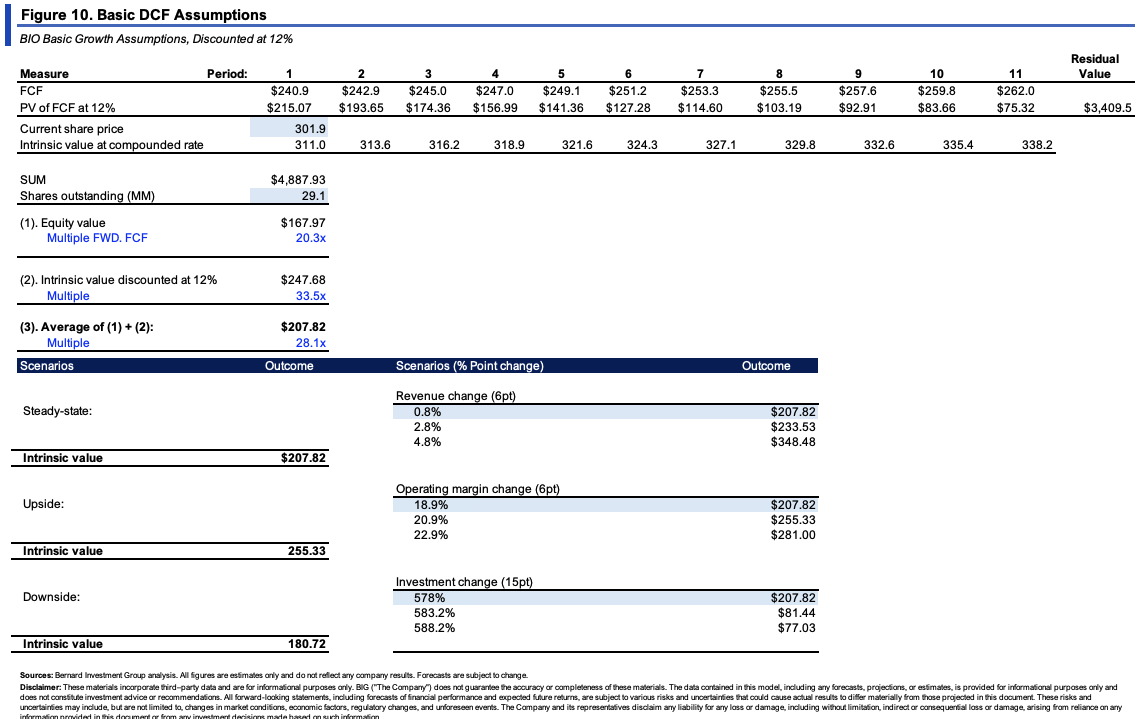

- Projecting the company's FCF out to FY'28 at the steady state of growth discussed earlier, then discounting at our 12% hurdle rate, exhibits underwhelming valuation support for BIO at these current levels—in the realms of $207–$280/share depending on various scenarios (Figure 10, bottom chart).

Each way I've looked at it the conditions have changed for BIO, and a buy rating can no longer be supported with the available data.

{kind=link}

{kind=link}

In short, multiple inflection points suggest BIO's investment rating does not support a buy at this stage. Without the business economics to support current multiples, paying 24x forward with flat business returns just isn't worth it in my opinion. Hence, based on the factors raised here today, I am revising my outlook on BIO to a hold, in search of more selective opportunities.

For further details see:

Bio-Rad: Business Returns Aren't Economically Valuable, Sartorius Now A Hindrance