BIO - Bio-Rad: How Efficient Is Its Capital Management? A Deep Look With Technicals

Summary

- Punishment of both Bio-Rad Laboratories, Inc. and Sartorius AG continued throughout the final stages of 2022.

- Bio-Rad Laboratories had an equally challenging Q3, setting up Q4 and FY22 numbers as key inflection points.

- Questions arise on whether it is the more efficient use of capital to hold the equity risk with Sartorius, or can it be deployed elsewhere.

- Net-net, there are promising signs for long-term value, but more evidence is needed to advocate for an immediate buy for Bio-Rad Laboratories, Inc.

Investment Thesis Summary

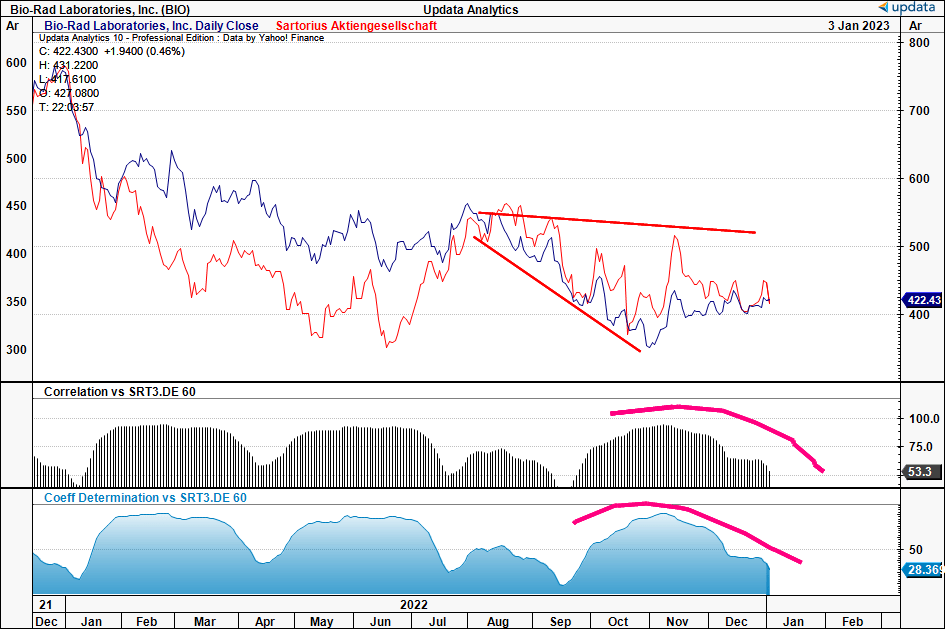

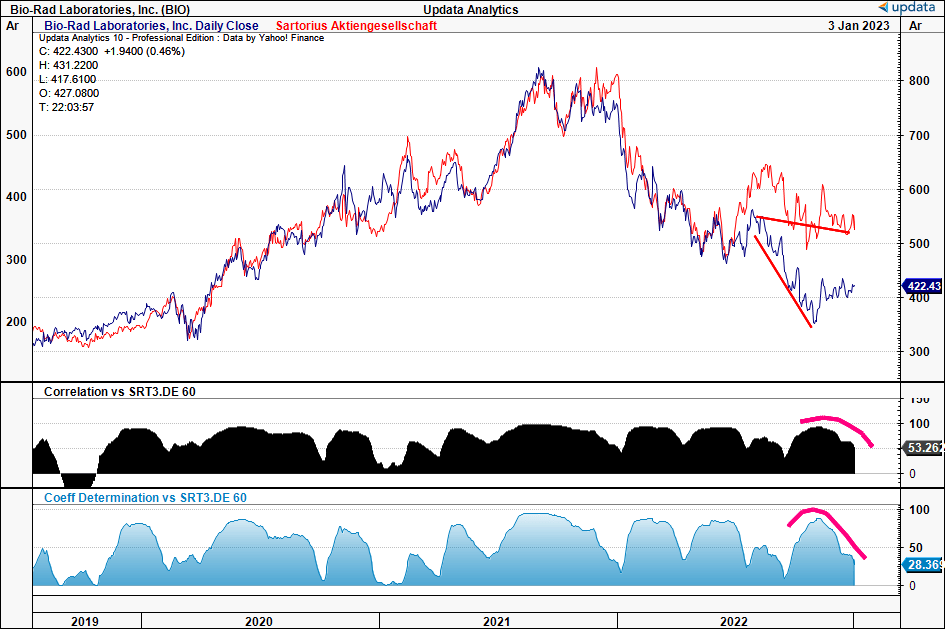

Since our last publication on Bio-Rad Laboratories, Inc. ( BIO ) investors have continued the selloff in its equity. Added to that, the key factor underpinning its appreciation these past few years, the equity position it holds in Sartorius AG (the "Sartorius Position"), has copped equally as heavy punishment over in the European markets. You can see the covariances between the two corporate securities in Exhibits 1 and 1a, taking note of the price distributions, correlations, and rolling R-squared.

BIO was and still is an interesting play for life sciences investors in our opinion. There's another potential source of embedded alpha in its share price, via the compounder/multiplier obtained from the Sartorius position. Problem is, over these past 12-18 months, the effect of this has been seen in reverse. Both stocks trade back in line with FY20 ranges, as investors repriced BIO to the sub-$345 mark at the lowest of range. BIO also missed consensus estimates last earnings, and the slowdown in COVID-related revenue has resulted in sharp declines in quarterly numbers. There's also the newfound debt position, combined with a 200bps revenue guidance. Still, the BIO share price has since snapped-back ~20% to its current levels. We wonder, has the market already priced in most of these hurdles?

By the way, I've covered BIO extensively here on Seeking Alpha. Check out the last 4 publications here:

- Long-term stance remains

- Gains 16.2%, bullish outlook strong

- Bio-Rad: Sartorius key portfolio differentiator

- Bio-Rad/Sartorius arb trade unwound for now .

Exhibit 1. Short-term price distributions, correlations, rolling r-squared [FY22-date]

{kind=link}

Exhibit 1a. Long-term price distributions, correlations, rolling r-squared [FY19-date]

{kind=link}

Question now turns to whether BIO is appropriately priced or not and whether there is valuation upside combined with downside protection from any volatility in Sartorius. Here, I'll run through our thinking on BIO moving forward and how we look to aggressively position against the name if it were to rally again. For very patient investors, we are very constructive on BIO. But there's a bit to learn in this story yet. First is how will it manage the Sartorius position looking ahead. Is it the most efficient use of capital? Or can that capital be deployed elsewhere. Net-net, we continue to rate BIO a hold.

Q3 earnings run-down exemplifies the situation

There were several hurdles BIO faced in Q3. This will serve as a good benchmark for the company leading into its next earnings. Here are our findings:

- We saw the company generated net sales of $680.8mm, down from $747mm, representing a decline of 8.9% YoY . Management attributed the decrease to the downturn in COVID-related sales. This, coupled with the base effect from the $32mm settlement for bank royalties from 10x in the same quarter last year. Moving down the P&L, operating income slipped to c.$93mm and the blowout from the loss on Sartorius was marked at $6.2Bn for the YTD by the end of September 30, 2022. It, therefore, booked a net loss of $164mm or $5.52 per share, down from an EPS of $131.75 last year. Without the unrealized gains, EPS was still negative $0.04.

- On the other hand, it's essential to note that management also estimated COVID-related sales for the current quarter still totaled $17mm. This was underlined by particularly strong demand in APAC, due to ongoing outbreaks in China. Hence, when excluding COVID-related sales and the 10x settlement, its core revenue for the current quarter increased by 6.1% YoY [constant currency, " cc "]. Still, this doesn't offset the loss at the bottom line.

- On a geographical basis, the company experienced revenue upside in Europe and Asia [cc], as mentioned. Meanwhile, core revenue in the Americas remained largely unchanged due to supply chain constraints that have persisted throughout the past year.

- With the divisional highlights, the company's Life Science Group recorded sales of $317.9mm in the third quarter of 2022, a decrease of 14.9% on a reported basis [11% on a cc basis]. Ex-10x settlement, the division's sales decreased 6.9% YoY, 2.3% cc. Revenue was driven primarily by Western loading, qPCR, process media, and antibody products.

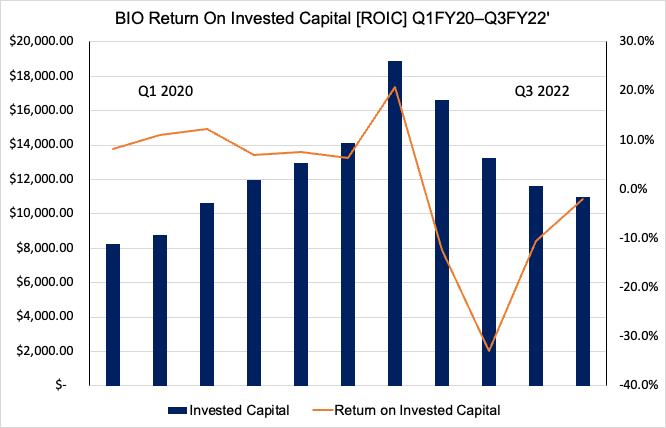

It's equally important to analyze these financial results against the underlying economics of BIO's capital budgeting in our opinion. Specifically, we investigated the return on its invested capital, when including all its capital at risk. Namely, factoring in its marked position for Sartorius. You can see below that the position makes up a large portion of BIO's capital pool. Even though these are supposed unrealized gains, the substantial re-rating has impacted earnings at a similar magnitude. Given the hurdles seen in its Q3 numbers, question now turns to whether this is the most efficient use of capital looking forward.

Exhibit 2. BIO Quarterly Invested Capital breakdown, factoring all capital at risk.

Data: Author, BIO SEC Filings

Looking at the outcome of it all, you'll notice the drawdown in BIO's return on invested capital as a result of the capital positioning above [Exhibit 3]. A more than 30% ROIC loss in Q1 FY21, as Germany experienced another wave of Covid-19, aided by the onset of the conflict in Europe. This has continued until the present day, riding out the 2022 period on a substantial loss. It will be key to observe how this affects management's thinking down the line, and also the company's FY22 numbers.

Moreover, the YTD CFFO also settled at $104mm, off the $498.5mm by Q3 FY21'. Added to that, YoY net cash generation narrowed to $47mm in the 3 quarters, down from $197.4mm by the same time last year.

Exhibit 3. Return on the investments has been a major headwind to BIO's profitability on an ongoing basis.

{kind=link}

BIO technicals add little price visibility

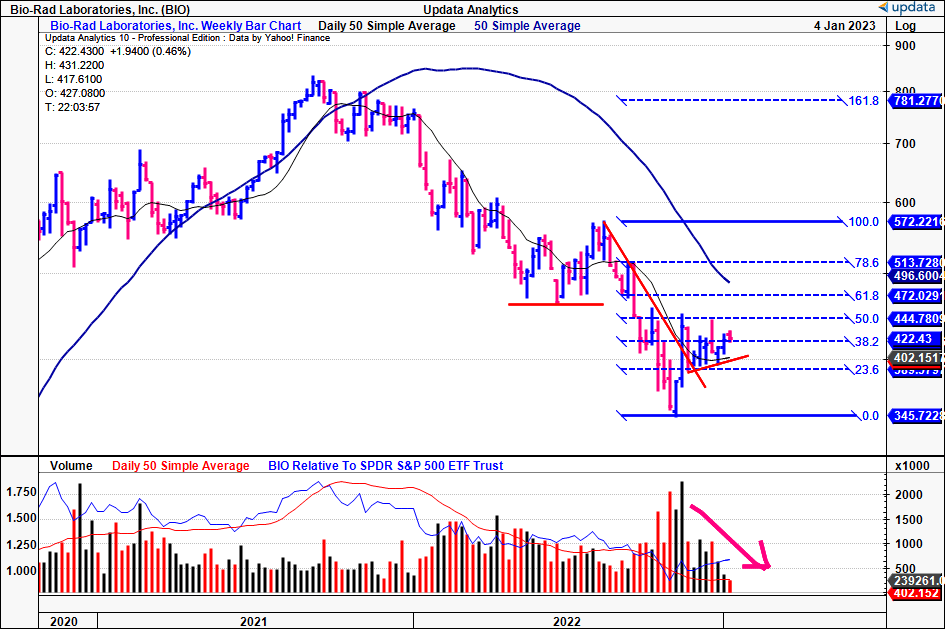

Various technical studies for BIO are seen below. First, you'll note the key Fibonacci levels shown from its August 2022 highs.

In its latest relief rally, it needs to push to $444 then $472 after taking out the $422 target. We aren't seeing the corresponding weekly volume to back this up, however. Another volume spike would be needed to shift the data here.

Exhibit 4. BIO key fib levels, needs to confirm $444 then $472 before advocating immediate buy

{kind=link}

In terms of trend indicators, we can see shares breaking through the cloud below, after trading sideways throughout December. The lag line hasn't quite confirmed the trend yet, however. On balance volume has also levelled, and would need to shift higher to suggest more longer-term accumulation from larger funds. Keep in mind, these larger fund managers won't be allocating in large allotments if the daily/weekly volume has narrowed in terms of dollar value. So, the purchases are done over longer periods of time to fulfil even a small position, let alone a larger one. This is where and why these studies come in handy.

Exhibit 5. Lag-line needs to lift up through the cloud to imply more bullish stance

Data: Updata

To cap this off, we also have upside targets to $595, after the $440 and $445 downside levels were previously taken out. You'll also notice the downside target to $225, however, and so the breadth in price action could see us level off to a smaller upside target. Nevertheless, this could be constructive. Not enough evidence to enter just yet, though.

Exhibit 6. Upside/downside targets to $595/$225; wide breadth.

Data: Updata

Valuation and Conclusion

Bio-Rad Laboratories, Inc. stock is trading at 18.9x forward EBITDA [using market cap to separate out the impact to EV with the sartorius position], still a substantial premium of 43% to the sector. Moreover, revenue growth is tipped to be flat in the subsequent years [Exhibit 7]. At managements forecasts of $715mm in FY22 adjusted EBITDA, this derives a target of $453. Hence, we believe there is scope for Bio-Rad Laboratories, Inc. stock to re-rate towards these targets. Yet, this isn't the only primary driver of BIO's share price. We need to factor the impact of its other investments, and on this basis, further evidence is needed to corroborate an immediate buy for Bio-Rad Laboratories, Inc. We encourage investors to remain very constructive on Bio-Rad Laboratories, Inc. stock, nonetheless.

For further details see:

Bio-Rad: How Efficient Is Its Capital Management? A Deep Look, With Technicals