BCRX - BioCryst Is Not Currently Uncovering The Full Value Of ORLADEYO

Summary

- BioCryst's main value driver, ORLADEYO, is already profitable in its second year on the market and generated over $250 million in revenue in 2022.

- ORLADEYO is successfully differentiating itself in a multi-billion dollar market and is on track to achieve blockbuster status in a few years.

- On the other hand, BCRX has so far failed to develop new product candidates with even greater potential, despite high investments.

BioCryst's ( BCRX ) valuation has often divided investors in recent months. On the one hand, there is the conservative and marketed product ORLADEYO, which is already profitable and is expected to reach blockbuster status in the coming years. On the other hand, there are the early Factor D inhibitors, which have enormous potential but also require huge investments and are still in early clinical development.

After the first Factor D inhibitor was discontinued at the end of 2022 due to safety concerns, the company is now scaring investors with hidden safety concerns in their quarterly report about its successor BCX10013. While the company itself is not yet clear on the impact of the observations in the safety studies regarding the further path to approval, many investors are pulling the rope due to the uncertainties.

As a result, many investors currently have a rare opportunity to buy BioCryst as a company based on its main value driver, ORLADEYO. Assuming that the market has written off BCX10013, today's market cap fully reflects the value and potential of ORLADEYO . Therefore, in this article I will discuss the potential value of ORLADEYO and introduce BioCryst as a company.

Business & Pipeline of BioCryst Therapeutics

BioCryst is a commercial-stage biotechnology company based in Durham, North Carolina, focused on the development of novel oral therapies designed to treat rare diseases. The company is leveraging its unique structure-driven drug discovery process to identify and develop new compounds that target the three major signaling pathways and the terminal signaling pathway to control dysregulations in the complement system.

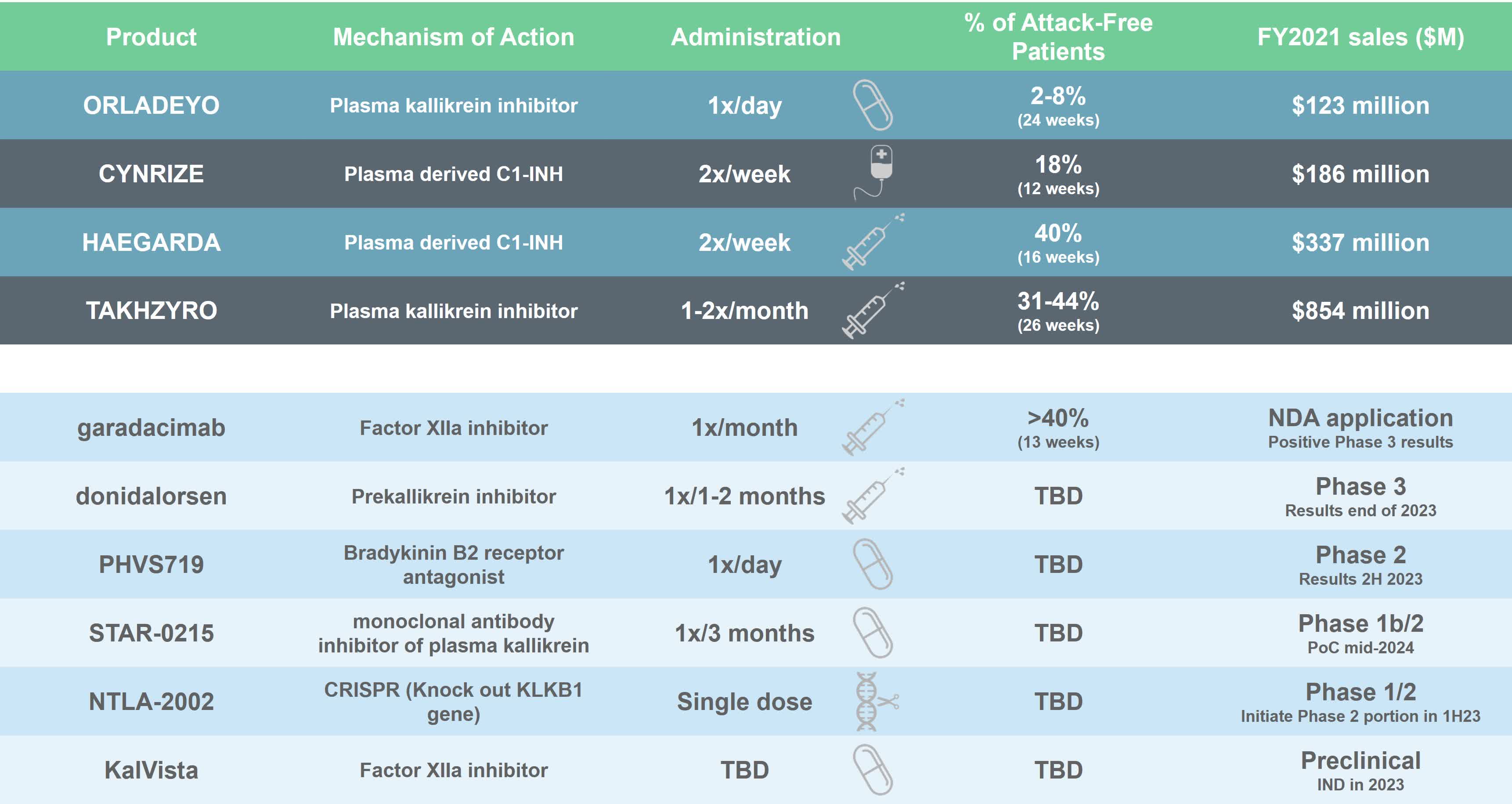

The backbone of the company is ORLADEYO, a plasma kallikrein inhibitor approved for the prophylactic treatment of HAE . HAE is a rare and potentially life-threatening genetic disease characterized by recurrent, severe and unpredictable episodes of swelling in various parts of the body. It occurs in 1 in 10,000 to 1 in 50,000 people, with the first symptoms usually appearing by the age of 12. Both the frequency and severity of HAE attacks are highly variable and unpredictable and do not correlate. Attacks can lead to hospitalization and, although rare, airway swelling can lead to death. The standard of care for HAE has evolved to on-demand and prophylactic therapies, and with the exception of ORLADEYO, all currently marketed therapies are administered by injection.

BioCryst is commercializing ORLADEYO in the United States and major European markets. The global rollout will be covered by distributors, while in Japan a dedicated collaboration has been established with Torii Pharmaceutical ( TRXPF ).

In addition to ORLADEYO, the company markets another product for the treatment of acute uncomplicated influenza, Rapivab . The product is sold to the government under a procurement contract and generates single-digit millions in annual sales. Rapivab is a nice additional source of revenue for the company. However, the product can be sidelined due to its low and limited potential.

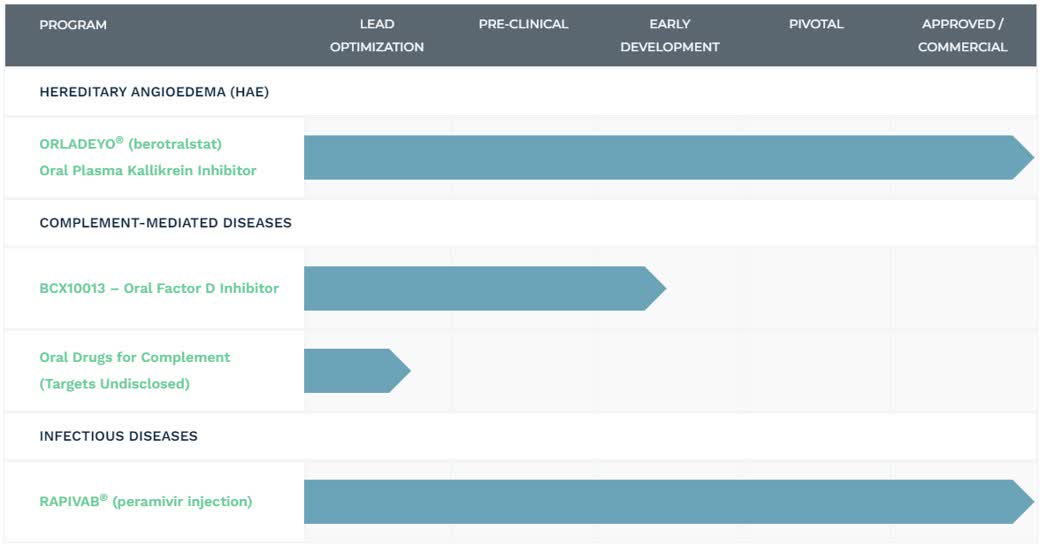

Overview of BioCryst's pipeline (Source: Company Homepage)

{kind=link}

BioCryst's pipeline has been significantly reduced and prioritized over the past year. As a result, the pipeline currently contains only one promising early-stage product candidate, the potential best-in-class Factor D inhibitor BCX10013. The product candidate is currently in a Phase 1 study to confirm safety, optimal dosing and once-daily profile. Results are expected by mid-2023, after which BioCryst plans to evaluate the product candidate in pivotal trials in multiple indications.

BCX10013 is a potential product in a pipeline that can be used in many rare diseases due to its broad therapeutic effect. The potential of BCX10013 far exceeds the potential of ORLADEYO and, if successful, BCX10013 will address multi-billion dollar markets. However, BCX10013 is still at a very early stage of development. There is no proof of tolerability or proof of concept, and as the example of BCX9930 shows, investors should not place too much value on the product at this stage. Especially considering that BCX10013 may also face safety concerns at higher doses .

BCX10013 follows the path of BCX9930, BioCryst's first Factor D inhibitor. This program was discontinued at the end of 2022 after its commercial competitiveness was questioned due to safety issues. Prior to its discontinuation, BCX9930 was in pivotal trials in patients with PNH and in patients with C3 glomerulopathy, immunoglobulin A nephropathy and primary membranous nephropathy.

In the third quarter, the company also discontinued its studies with BCX9250 for the ultra-rare disease FOP. This decision was also made after a review of the competitive landscape.

Despite these setbacks, the Company is confident that it will not only advance BCX10013 to regulatory approval, but also identify several new oral drugs that target the various pathways of the complement system.

Sales Performance of ORLADEYO

Sales progress has been impressive. ORLADEYO is already profitable in its second year on the market, even though the majority of sales are generated in the US. Each quarter, the patient base has continued to grow and profits have increased with a consistent pattern of linear growth. In the coming months, in addition to deeper penetration of the US market, international revenues are expected to play an increasing role. Currently, ORLADEYO is commercially available to HAE patients in 15 countries around the world, with more to follow in the coming months. According to management, this success comes as no surprise and confirms the blockbuster status of ORLADEYO with peak sales in excess of $1 billion.

It shouldn't be surprising given the excellent safety, efficacy, and once-daily oral profile. We are consistently hearing from patients that ORLADEYO is changing their lives.

ORLADEYO is very popular with patients due to its convenience and efficacy and is the most requested HAE prophylaxis drug. Not surprisingly, physicians expect the percentage of their patients treated with ORLADEYO to increase more than any other HAE therapy over the next 12 months. In addition, BioCryst has expanded its sales team to further accelerate its impact on key physicians and to support them in seeking payer authorization for HAE therapies.

After more than $122.6 million in 2021 and more than doubling to $251.6 million in 2022, BioCryst expects net sales from ORLADEYO to be at least $320 million, which would represent a further increase of nearly 30%. In addition, the Company expects to be able to sustain these growth rates into the future.

With our sales performance in 2021 and 2022 and our guidance in 2023, you now have three data points to get a sense of the slope of the ORLADEYO launch.

At these growth rates, BioCryst should generate over $450 million in ORLADEYO revenues in 2024, just under $650 million in 2025, and approximately $900 million in 2026.

Prophylactic HAE: Hyper-Competitive Landscape

As described above, the HAE market can be divided into on-demand and prophylactic therapies. This is partly due to the fact that even prophylactic treatment of HAE does not guarantee complete protection. Studies show that 70% of patients use both prophylactic and on-demand therapies . In addition, although prophylactic treatment reduces the attack rate, patients are still affected in their lives. Many patients do not feel 100% secure and often make lifestyle changes to avoid potential attack triggers.

Overall patient satisfaction is often related to the efficacy of the medication. However, many patients complain about the psychological and physical burden of injections and infusions. Overall, injections and infusions present a hurdle for patients because, despite their effectiveness, they can cause pain at the injection site, are time-consuming to administer, and are difficult to store.

People living with HAE actively switch products, seeking improvement in efficacy, safety/tolerability, and convenience (Source: Pharvaris Company Presentation)

{kind=link}

BioCryst is using this fact to successfully differentiate itself from the competition. ORLADEYO is the only approved once-daily oral therapy on the market. Research has shown that 93% of HAE patients would be willing to switch to an oral therapy for the same efficacy.

Overall, the HAE prophylaxis market is extremely competitive There are many companies seeking to achieve greater efficacy with a simpler and less frequent route of administration. The following chart provides an overview of approved products and potential future competitors.

An effective, simple and infrequent treatment that can normalize the lives of people with HAE remains an unmet need. (Source: Author's Chart)

{kind=link}

Currently, BioCryst is very well positioned with its product candidate ORLADEYO and differentiates itself primarily through the oral route of administration. However, I see a big risk that this differentiation could be lost in the future. The big advantage, however, is BioCryst's pioneering role; in my opinion, the next oral drugs will not reach the market until 2026 at the earliest. With a similar profile, it should be difficult for these product candidates to gain market share as ORLADEYO has been established for years.

The other threat I see from emerging competition is potential downward pressure on prices. Currently, ORLADEYO's annual treatment cost is about $485,000 , which is cheaper than comparable drugs such as Takeda's ( TAK ) Takyzyro at about $566,000 or CSL's Haegarda at $510,000. Nevertheless, this is still a high price and a potential differentiator for new product candidates.

Market Opportunity

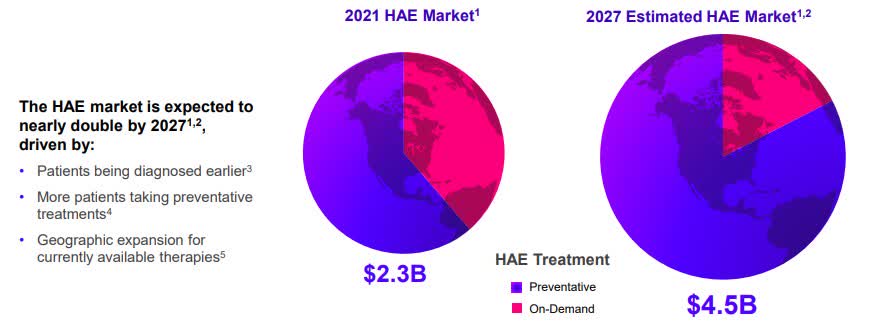

According to forecasts, the HAE market will show tremendous growth in the coming years, reaching 4.5 billion in 2027. The market will focus more and more on the prophylactic treatment, nevertheless patients will always need a back-up solution in case of an attack. It is therefore not surprising that the competitive pressure in this indication is so high. However, because of the size of the market, I believe that several approved drugs can coexist and that ORLADEYO will achieve its own claim to blockbuster status with associated sales of more than a billion dollars.

Global HAE Treatment Market is Substantial and Growing (Source: Astria Company Presentation)

{kind=link}

BioCryst continues to gain market share in the coming months (Source: Company Presentation)

In the most important market, the United States, BioCryst expects increasing market penetration in the coming months. This trend can be seen in the feedback from patients and prescribers as well as in the steadily increasing number of patients. Given the chronic nature of HAE, it is important not only to attract new patients, but also to gain market share from existing therapies.

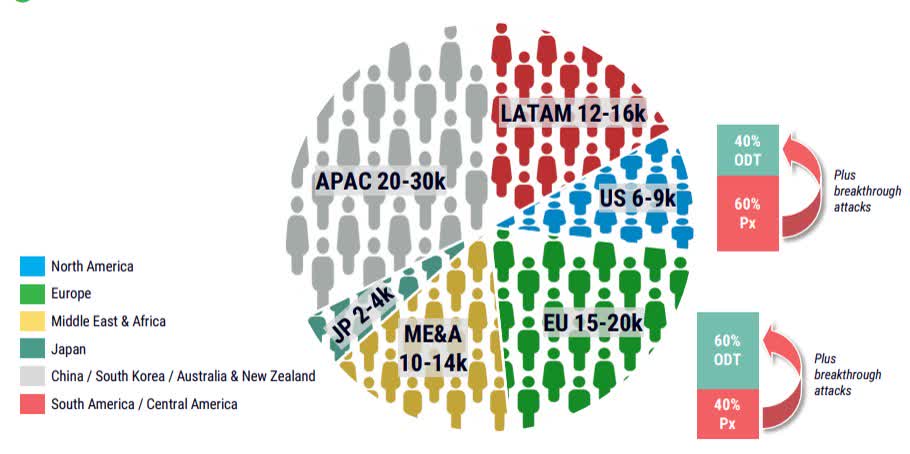

BioCryst expects more than 80% of its peak sales of over $1 billion to be generated in the US, with only 20% coming from EX-US markets. This is surprising as many other rare disease players have generated a much larger share of their sales outside the US. The top performers generated almost 50% of their revenues from ex-US markets after only 2 years on the market . Given the global patient population, I think the company may be too conservative in these estimates.

Potentially up to 100,000 people living with HAE worldwide (Source: Pharvaris Company Presentation)

{kind=link}

Financials

In addition to the future prospects of the pipeline, the financial position of a company is another important element in the investment decision. The financial position provides an indication of the ability to realize future potential.

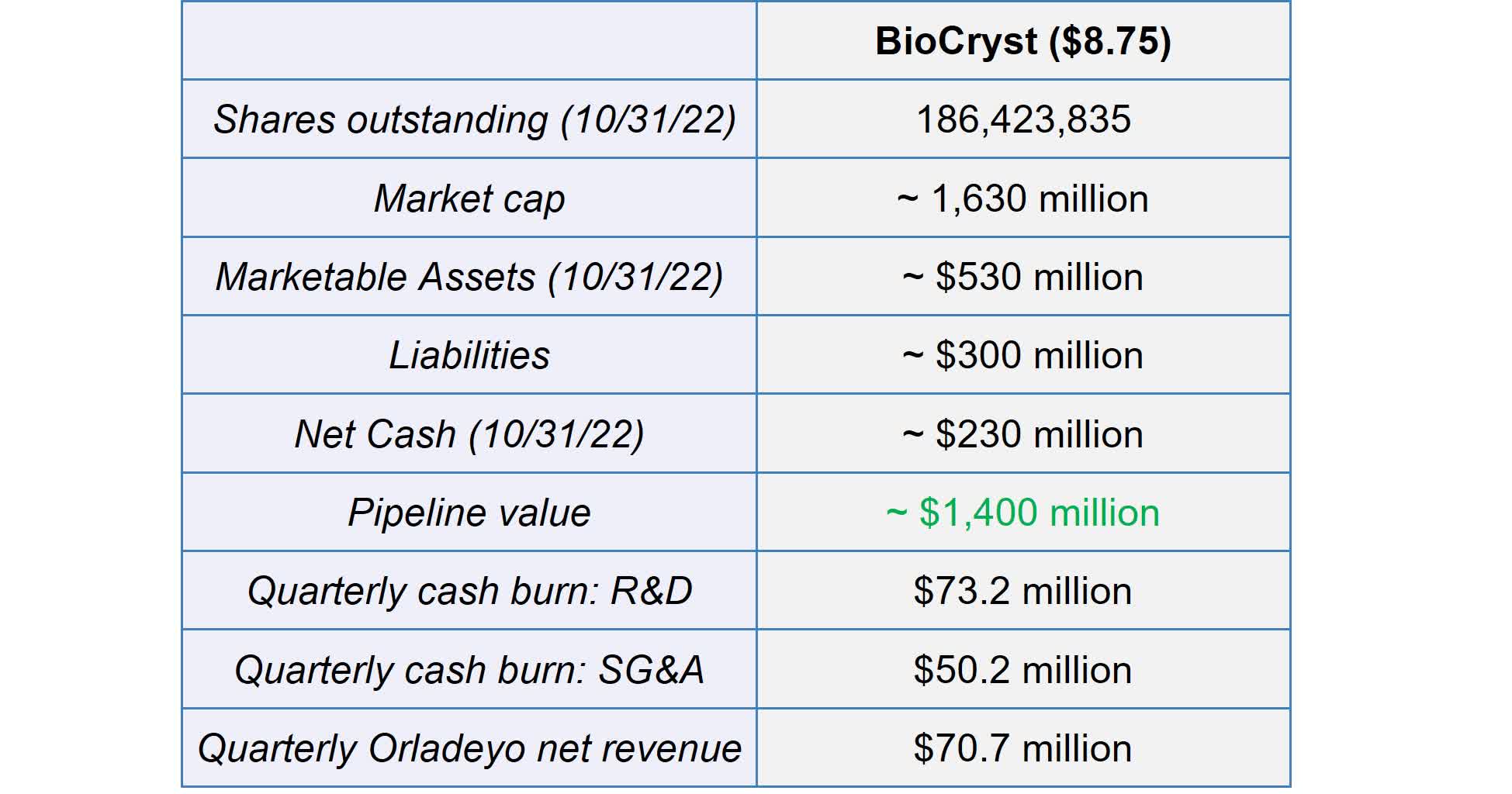

Overall, BioCryst is in a strong financial position. With a strong cash position of approximately $530 million, the company can continue to advance the commercialization of ORLADEYO as well as identifying and advancing new product candidates.

Overall, I believe that research and development costs are far too high and not proportional to the pipeline. However, these high costs are almost offset by relatively low distribution costs and high product sales. I also expect BioCryst to reach the milestone of quarterly profitability this fiscal year. Therefore, I am willing to overlook the high R&D costs at this point.

At the current market cap of about $1,630 million, $1,400 million is attributable to the pipeline. This puts BioCryst's trailing twelve-month sales multiple at ~4.4. While I don't think these comparisons are very meaningful, significantly higher multiples have been paid for comparable transactions in the past (of approx. 8.5x NTM revenues).

Financial Overview of BioCryst (Source: Author's Chart)

{kind=link}

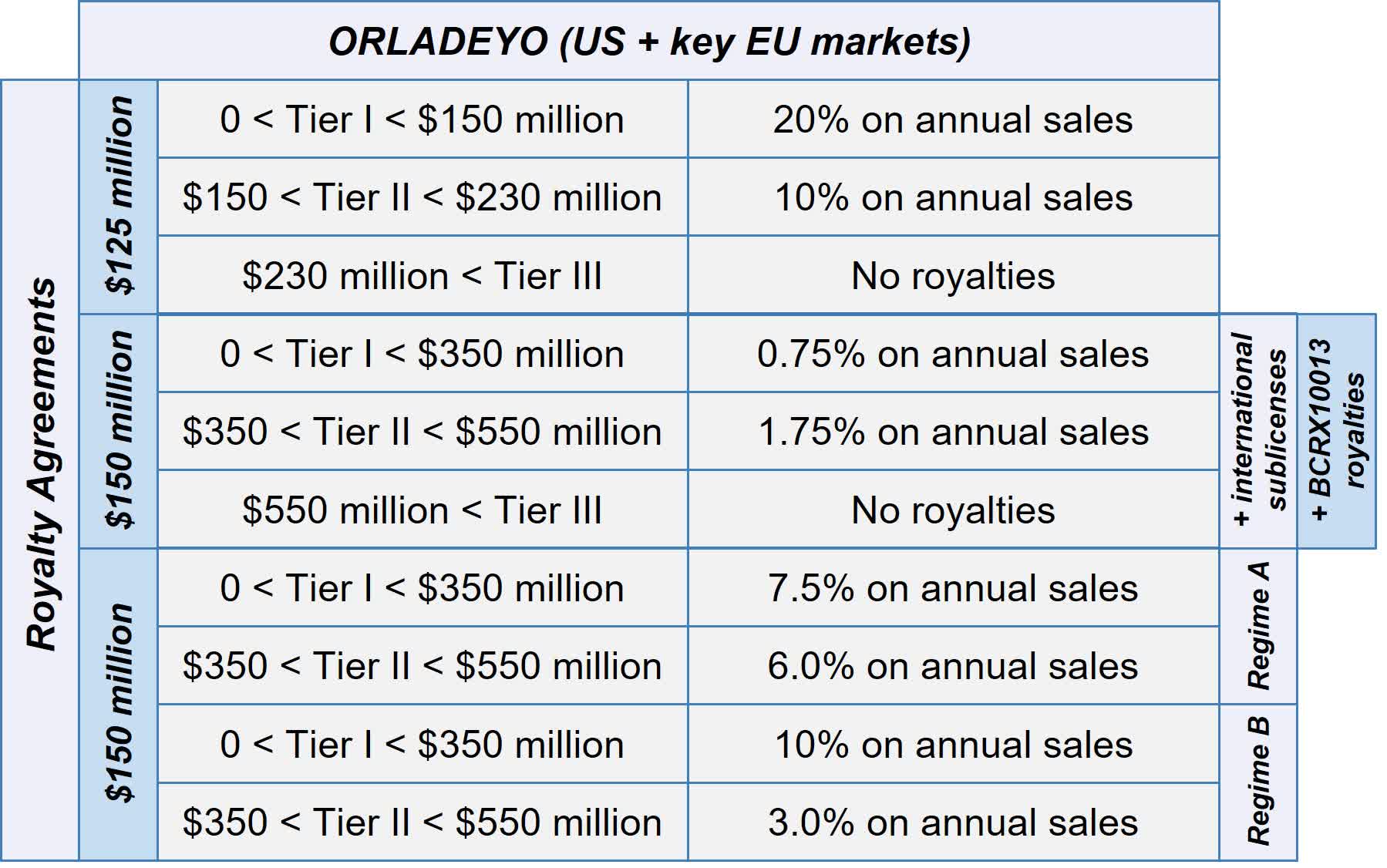

The high cash balance was secured in previous financial transactions. In addition to the royalty sale, debt was also raised. In total, BioCryst received $200 million in debt and $425 million from the sale of royalties. The following figure provides an overview of the three license agreements entered into .

Overview of the royalty arrangements (Source: Author's Chart)

{kind=link}

The royalties sold relate primarily to ORLADEYO product sales in the territories where BioCryst is responsible for commercialization. Based on these transactions, BioCryst is required to pay up to 30.75% of the revenues to its partners in subsequent years.

While the first two transactions with Royalty Pharma ( RPRX ) are uncapped, the payments of the third transaction to Omers are capped at 1,425x to 1,550x of the original amount. Both the final amount and the royalty distribution are tied to the level of worldwide net sales of ORLADEYO in 2023. In addition, royalty payments will not begin until January 1, 2024 and could be repaid in just over five years.

The debt has a relatively high interest rate (LIBOR + 8.25%) considering the date of the transaction. Repayment of the entire amount, including accrued interest, is due at the end of 2025 . If the company continues to be successful in its sales activities, repayment of the debt should not be a major problem.

Risks

Overall, BioCryst is in a comfortable position and I see the company well prepared for the future. However, I would like to highlight the risks that I currently see. In my opinion, the biggest risk is the commercialization of ORLADEYO and the enormous competitive pressure. While BioCryst is successfully differentiating itself today, there are several other oral therapies in development. In some cases, these therapies also have a better profile, e.g. due to lower dosing frequency. If these product candidates succeed in demonstrating a similar or even superior efficacy profile, BioCryst will face significant challenges in the future and lose market share.

The other risk I see is related to the early-stage development candidates. BioCryst invests a lot of money in its R&D department, but the results have not been positive so far. As a result, the company has not yet been able to reach the profitability threshold despite high product revenues. In the coming months, the company will have to prove that its heavy investment in R&D is justified. This sentence in the latest news regarding BCX10013 is cause for concern, not optimism.

Recent dose-related observations in an ongoing BCX10013 nonclinical study will delay the clinical program.

Source: Company News Release

Summary

In summary, I think BioCryst is a very promising and attractive company. With ORLADEYO, the company has a product that is well on its way to blockbuster status in a few years. Because of its oral form of administration, it is superior to competitors at similar efficacy. In addition, all potential serious competitors are still in early development and several years away from approval.

Nevertheless, despite high product revenues, profitability has not yet been achieved due to the large royalty payments and the huge investments in research and development, and the company continues to incur losses. I don't understand how a company with only one approved product and one early-stage compound and a small sales infrastructure, which is common for a rare disease, can have annual operating expenses of $375 million. Last but not least, the Company has exhausted its ability to raise non-dilutive capital.

If the company is able to successfully advance its product candidates to the point where the large investments pay off, or adjust its strategy, I am confident that this current dilemma will be resolved and BioCryst will achieve a fair valuation. But especially in the current market environment, I believe there are more promising stocks with both less (external) risk and significantly more upside. Therefore, I will remain on the sidelines for the time being.

With the pipeline failures, the likelihood of BioCryst being acquired obviously increases. Considering only ORLADEYO, BioCryst is perfect as a bolt-on acquisition for larger companies to secure long-term external growth.

For further details see:

BioCryst Is Not Currently Uncovering The Full Value Of ORLADEYO