NVTA - Bionano's Balance Sheet Challenges: History Repeating Itself

Summary

- BNGO reported preliminary Q4 results, showing acceptable core business performance.

- Aggressive expansion into capital-intensive markets could put significant pressure on BNGO's balance sheet.

- Recently-introduced LDTs will likely have a limited impact on revenue growth.

Investment Thesis

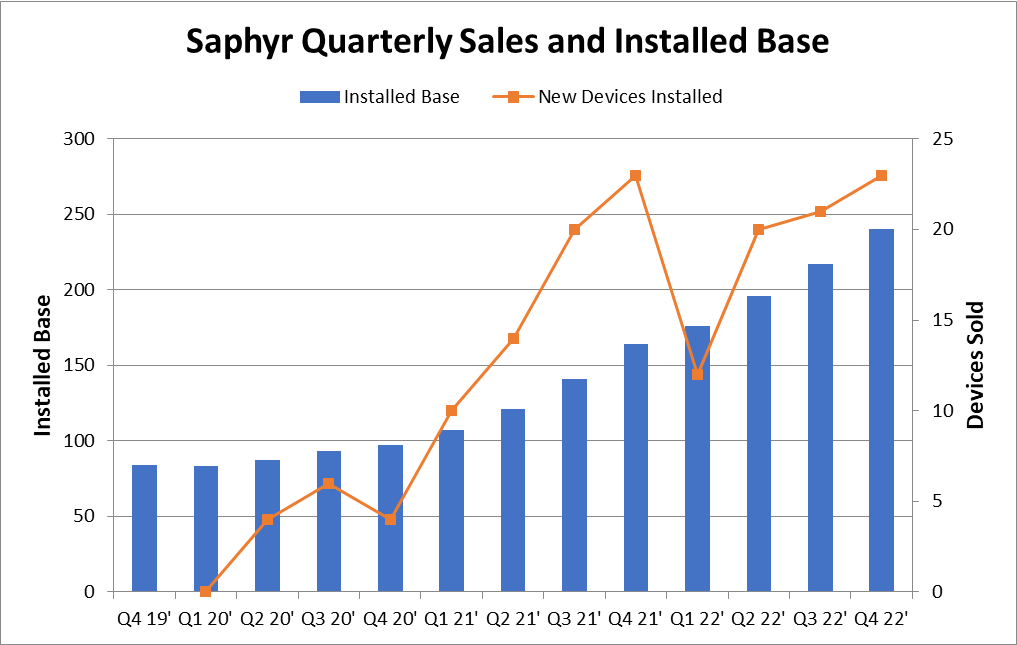

Bionano Genomics ( BNGO ) released its preliminary Q4 and FY 2022 results on January 5, 2023. The report shows acceptable core business performance. Revenue is expected to increase between 29% - 33% ($1.8 - $2.1 million) over the fourth quarter of last year. In Q4, the company installed 23 new Saphyr systems, bringing the total installed base to 240, up from 217 in the prior quarter and 164 in Q4 2021.

Saphyr Quarterly Sales and Installed Base (Author's estimates based on BNGO filings)

{kind=link}

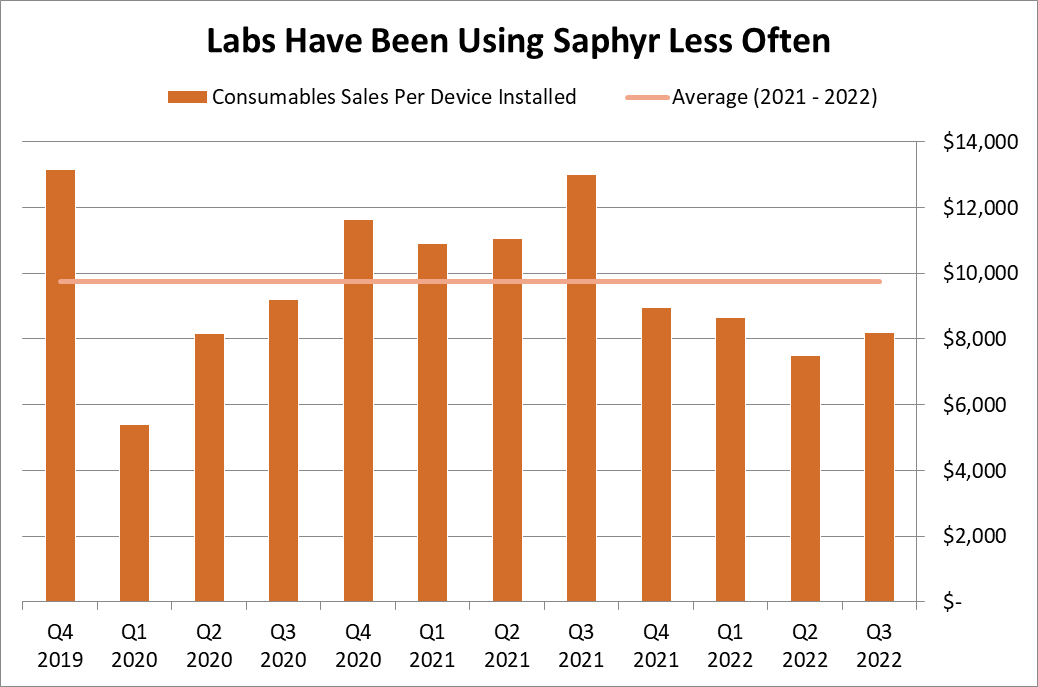

In the previous quarter, we saw a decrease in Saphyr use, mirrored in the number of consumables sold for each device installed. The company is selling more devices due to an increase in the amount of money spent on sales and marketing, but laboratories were utilizing the Saphyr system less frequently. Lower utilization could indicate that BNGO is pushing its Genome Mapping technology to an unprepared market that is not ready yet to fully embrace its product. It would be interesting to see if Q4 brings about a change of direction, but we'll have to wait until management releases its full Q4 and end-of-year report to find out. BNGO has historically released its full-year and Q4 results in late February or early March.

The graph below shows consumable sales per device installed.

Consumables Sales per Device Installed (Author's estimates based on BNGO filings)

{kind=link}

What is more important is the state of the company's balance sheet. BNGO has been branching into new markets, including Bioinformatics (Biodiscovery acquisition Q4 2021), Clinical Laboratory Services (Lineagen acquisition in 2020), and sample preparation (Purigen Biosystems acquisition in Q4 2022), all of which are markets characterized by high capital requirements. Our sell rating mirrors the expected balance sheet challenges as BNGO pursues a vertical expansion approach to enhance the market position of its core business.

The Device

Saphyr is BNGO's flagship product (and, until recently, the only one) and, to my knowledge, the world's first and only OGM system. It found its footing in the market because of its Structural Variant "SV" detection capability, which sets it apart from NGS systems. None of the genomic analysis platforms on the market today can reliably detect all genetic diseases, and each instrument has its strengths and weaknesses. BNGO's pitch is that combining OGM and NGS will yield better patient results.

Saphyr (BNGO)

The question that comes to mind is if Saphyr is a good product, why isn't it rising to its potential; the $3.5 billion in annual sales management cited in its investors' prospectuses? In a good year, BNGO sells 6 - 7 devices each month, a small amount compared to Illumina ( ILMN ), which has thousands of machines installed worldwide. Why isn't BNGO selling more reagent kits?

Well, it is all about how comfortable its end users are in using the new device. OGM is an emerging technology with limited literature to support any findings derived from its data. In response to these challenges, management spends millions each year sponsoring academic research that utilizes the device and advertises these publications on earnings calls and press releases.

Clinical pathology is BNGO's biggest market opportunity and is where most of the company's efforts to sell its products are focused. The fact that the FDA hasn't approved Saphyr for medical use is a challenge, especially in international markets, where regulatory approval in the home country is one of the requirements for imported health tech. Currently, BNGO derives half of its revenue from international markets, in line with the industry average. However, the primary use of Saphyr remains limited to research purposes, namely non-human specimens such as bacteria, plants, and other organisms.

In the US, things are a bit more complicated. Contrary to popular opinion, the primary barrier to clinical adoption is not FDA-approval or lack thereof but rather commercial and public payors' reimbursement decisions. In an era of Value-Based Care, your physician will likely order a reimbursable traditional cytogenetic test, which gives the same result as Saphyr.

Most molecular diagnostic tests on the market today in the US enjoy a CLIA waiver from a 1988 law that allows labs to offer "homebrew" tests without FDA approval. Today these tests (also called Laboratory Developed Tests "LDT") are sold on a national scale, which is why the FDA has been wrestling with Washington to extend its regulatory arm over this sector, as mentioned in previous articles.

For now, all a lab requires to sell its tests to the market is a CLIA certificate, which BNGO's lab possesses. Establishing commercial viability is a grinding process. Before the Center of Medicare and Medicaid "CMS" and commercial payors begin reimbursing suppliers for the test, they must first review a dossier of all the research and publications, like those cited during BNGO's earnings calls and press releases, and clinical trials, like BNGO's multi-center trial .

Convincing physicians to prescribe and use the device is another story. It involves working with Key Opinion Leaders to change the standard of care practice and healthcare providers to change their operating workflow. After that, it is also helpful to obtain a CPT code from the American Medical Association to streamline the reimbursement process.

This month, management provided an update on its multi-site clinical study that compares OGM to gold-standard cytogenetics techniques, including FISH, Microarray analysis, and karyotyping. Preliminary results show that OGM is at least as good as these methods in detecting SVs.

I am not aware of any Premarket or 510-k application in progress as of the time of this writing. However, in March of Last year, BNGO's CEO stated that the company would be pursuing FDA approval for the recently introduced version of Saphyr, a new device with small tweaks and enhancements of throughput. This would be a tedious process and will require a lot of cash.

Last week, BNGO announced the introduction of a new LDT called OGM-Dx HemeOne that diagnoses a set of blood and bone marrow malignancies, including Multiple Melanoma and B-Cell Lymphoma, among others. The test competes with the current standard of care for blood and bone marrow cancers diagnostics, including urine, blood, and x-ray imaging, to detect different biomarkers, including abnormal proteins produced by cancerous cells.

What BNGO doesn't tell investors is that neither OGM-Dx HemeOne nor any of its other LDTs (about a half-dozen in total, including EpiPanel Dx and NextStep Plus, among others) have a clear reimbursement path with healthcare payors, which is a key factor in a diagnostic test's commercial success. To sell OGM-Dx HemeOne as a clinical diagnostic test, BNGO needs to demonstrate its clinical utility through trials and show how it adds value to the healthcare diagnostic process.

This is why Molecular Diagnostic Companies such as Invitae ( NVTA ), Guardant Health ( GH ), Exact Sciences ( EXAS ), Natera ( NTRA ), Myriad Genetics ( MYGN ), NeoGenomics ( NEO ), and many others spend hundreds of millions of dollars on clinical trials verifying their diagnostic tests, and more on marketing and awareness campaigns to Physicians and KOLs.

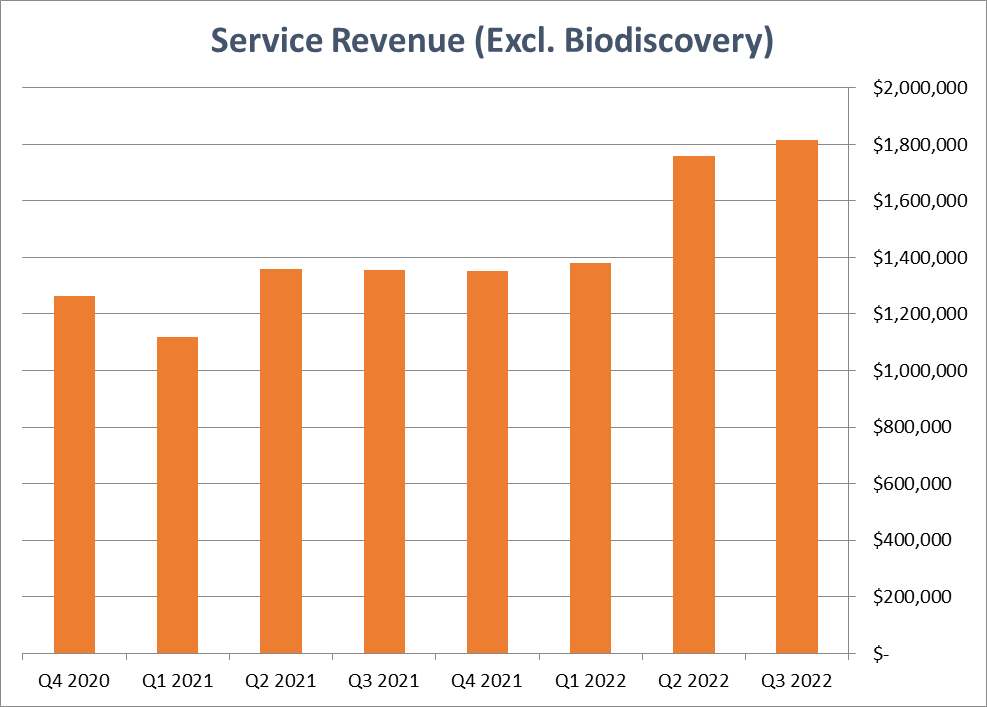

BNGO's previous LDT launches have yet to translate to meaningful revenue growth, despite running at a very low base, as shown in the graph below.

BNGO Services Revenue (Author's estimates based on company filings)

{kind=link}

Balance Sheet

In recent years, BNGO branched into new markets with high capital requirements. I was hoping management would mention the company's cash balance in its preliminary Q4 earnings preview. The latest data from the September quarter show $180 million in cash and cash equivalents. The current cash burn stands at $30 million, so the company has about twelve months before it runs dry. This includes a $32 million cash payment for the acquisition of Purigen Biosystems announced in Q4 but excludes the potential $32 million remaining balance conditional to certain milestones.

Although it might seem that BNGO has the financial flexibility to adjust its spending, which mainly consists of marketing and selling expenses, historically, its profit margin wasn't enough to cover its overhead costs. This problem is exacerbated by the high capital requirements needed to market its LDT products sold via its Linagen segment, its R&D efforts to remain relevant in the Bioinformatics space (Biodiscovery operations), and R&D expenditure to fund its clinical trials necessary to establish a market position for its OGM devices including Saphyr and Iconic (the newly acquired sample prep system sold under the Purigen Biosystems brand).

Historically, BNGO was forced to borrow at unfavorable rates to cover its operating losses and raise equity at highly dilutive valuations to continue operations. In 2019, it was in technical default on its loans and failed to meet the NASDAQ listing requirements after its stock traded below $1 per share for more than three months. I fear BNGO is headed in this direction, as the profitability path remains unclear.

Summary and Final Thoughts

I remember an old adage goes something like this; a good product sells itself. This might be true for most products but not healthcare diagnostic devices. Beyond regulatory approvals, the US healthcare system presents challenges to product introduction because of its disjointed frameworks of interconnected subsystems encompassing payors, insurers, providers, government programs, academic institutions (key opinion leaders), and suppliers. Saphyr is a good product; if management puts its mind to it, FDA approval could be obtained.

However, the device is sold as a Research Only Use "ROU," and most of the Saphyr installed base is utilized in non-human genomic analysis applications such as bacteria, plants, and animals. Pacific Bio ( PACB ) was the same size as BNGO ten years ago and remains unprofitable today. Introducing new technology to the market is a grinding process. It requires patience and a lot of cash, which probably means further dilution (if BNGO is lucky to find investors willing to pour money into this speculative venture.)

For further details see:

Bionano's Balance Sheet Challenges: History Repeating Itself