XBI - BioXcel Therapeutics: Igalmi's Commercial Uncertainty Remains Downgrading To A Hold

Summary

- BioXcel Q2 Earnings: Igalmi's 120mcg & 180mcg dosage forms are available for order through wholesalers starting from early July.

- SERENITY III pivotal trial studying the at-home usage of BXCL501 in agitation associated with schizophrenia and bipolar disorder is expected to start in 2H 2022.

- Key clinical catalyst expected in 1H 2023.

- Company is well financed and valuation looks modest.

- Downgrading to a hold for now.

{kind=link}

BTAI company source

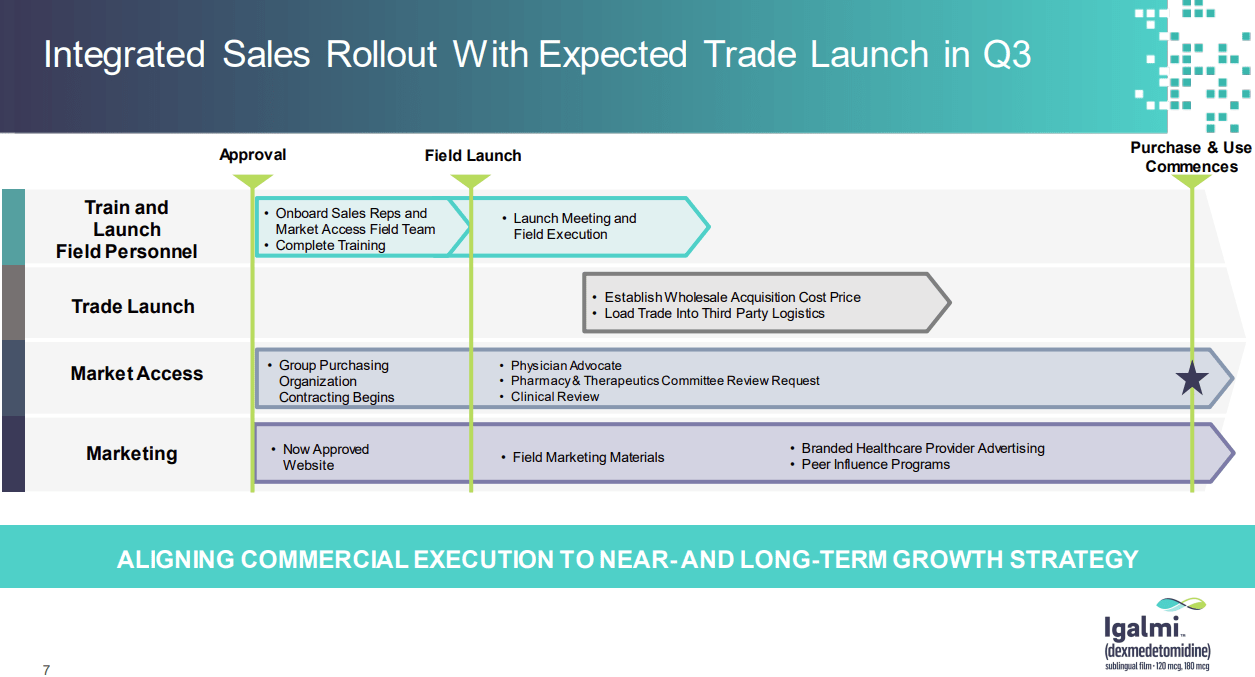

Igalmi US market launch is ongoing, but some uncertainty remains regarding P&T decisions.

BioXcel Therapeutics (BTAI) announced during the Q2 earnings call that the 120mcg and 180mcg formulations are available for order through wholesalers starting from early July and the management assured investors that the sales team has been on the field during the last two months preparing for a smooth market launch. We like the fact that i) BTAI's sales force is in place at the majority of hospitals, ii) BTAI has launched peer-to-peer speaker programs designed to educate healthcare professionals regarding the importance of early intervention to reduce agitation episodes, and iii) the company's concerted effort for digital marketing, where the importance of digital marketing has grown post COVID-19 due to decline in in-person detailing with MDs.

We emphasize that, in the US, P&T decisions are pivotal for launch success, as if the drug is not reimbursed, no revenue can be generated. P&T process usually takes 6-12 months normally for a broad reimbursement to take place, and that is when we can expect meaningful growth in revenue. For now, we do not have enough data to build a high degree of conviction on the drug's ramp due to the paucity of available information.

Pharmacy and Therapeutics (P&T) is a committee at a hospital or a health insurance plan that decides which drugs will appear on that entity's drug formulary. Source: Wikipedia

Furthermore, the company is looking for a commercial partner in the EU and Rest-of-world (ROW) at the moment; any BD partnership can be a short-term catalyst moving forward.

The key upside for Igalmi is in the at-home setting, but it will take at least 1 year before they receive that label extension.

Considering the narrow label of Igalmi where the drug is only indicated in the hospital setting, not including the at-home setting, the key inflection point of the sales will likely be after the label extension. The lukewarm interest in hospital only label can be seen by the wholesale acquisition cost ( WAC ) for IGALMI of $ 105 /film which was lower than what the sell-side and the company expected previously. During the Q2 earnings call, the management indicated the ongoing SERENITY 3 pivotal trial is expected to start soon (2H 2022), but we believe the catalyst is likely to take place in 1 year at the earliest, making it less relevant for short-mid term investors.

The financial situation looks robust.

The company announced a 2Q net loss of $37.7MM, or ($1.35) per share due to i) an increase in R&D expenses of $17.9MM and ii) SG&A expenses of $18.4MM. We highlight the robust cash runaway of the company with the cash runway until 2025. At the end of 2Q, the company had around $233.5M in cash, which does not include the $30 million of contributions from the $260MM in interest/royalty financing that was announced in April. Especially, in this historical biotech bear market, we believe BTAI's cash runway is a huge plus, and we build a high degree of comfort based on it moving forward.

Key risks to BTAI

Key risks to BTAI include i) clinical risk from its ongoing trials and RWE studies, ii) commercial risks from potential competitors, iii) reimbursement risk from payer negotiations, and iv) financing risk.

Conclusion

We initiated BTAI back in March 2022 before the then-upcoming PDUFA date with a BUY rating; however, we downgrade the rating to HOLD due to a lack of short-term catalyst during 2H 22 and our low degree of conviction on the short-mid-term sales ramp of Igalmi. However, we are a fan of the drug's label extension into at-home usage and dementia, which will allow the company to enjoy significantly larger market potential.

For further details see:

BioXcel Therapeutics: Igalmi's Commercial Uncertainty Remains, Downgrading To A Hold