BIRDF - Bird Construction: A High-Flying Pick For Canada Construction

2024-01-17 10:46:42 ET

Summary

- Bird Construction is a leading contractor in Canada, serving institutional, industrial, and commercial sectors.

- The company's Q3 2023 earnings show strong sales and higher margins, indicating positive growth trends.

- Low debt to equity ratio, strong balance sheet, and focus on safety mean Bird Construction is well-positioned for continued success.

- With c. 26% upside from current prices, I rate this stock a "Buy"

Bird Construction Inc. ( BDT:CA ) is one of the leading (top 10) contractors in Canada . According to the company website, it serves three core customer segments: Institutional (43% of 2022 revenues), Industrial (42% of 2022 revenues) and Commercial (15% of 2022 revenues). It also has a partnership with Stack Modular , which describes itself as “a leading manufacturer of large scale, steel frame modular construction projects across North America”. The company has been in operation for over 100 years, which is definitely something to admire.

In this article I present a view on BDT’s post-Q3 2023 earnings, going into FY earnings to be announced in early March 2024. I also assess the company’s operating performance and present an outlook for 2023 full year and beyond.

In preview, despite the c. 65% increase in the last 12 months, I believe BDT is trading significantly below fair value (+26% potential upside). At this level I believe the stock presents a favorable risk/reward opportunity.

Overview of Bird Construction and 2023 Q3 results

In its 2022 annual report , BDT describes itself as

“a construction and maintenance company providing a comprehensive scope offering and a diversified portfolio of services to industrial, institutional, and commercial markets including: new construction and retrofits; industrial maintenance, repair and operations ("MRO") services, shutdowns and turnarounds; civil infrastructure construction; mine support services; utility contracting; fabrication; steel modular construction; and specialty trades” .

With that in mind, for construction companies, the 4 main indicators I like to review are 1) project execution; 2) orderbook (or backlog) size and mix; 3) balance sheet strength and 4) safety record.

Project execution

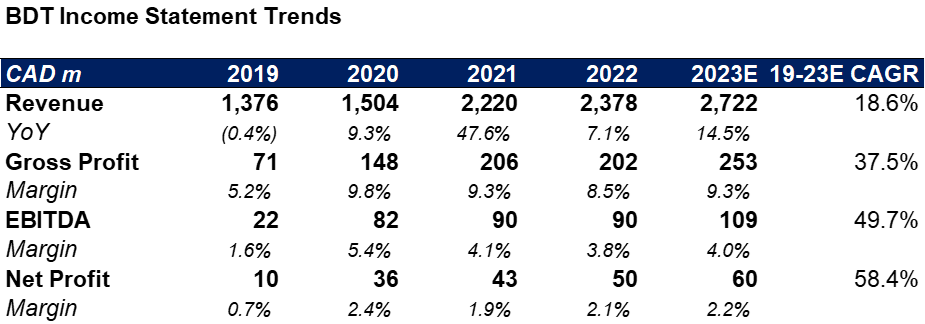

Project execution is the fundamental skillset of a contractor. What I mean by this is the ability to deliver projects at the budgeted cost for the contractor, without cost overruns or delays (which could expose the firm to liquidated damages). While it is not very common for contractors to report on this metric, as a proxy, I generally look at margin stability or expansion. This is definitely not a perfect proxy but can give an indication. What I like to see is (of course) revenue expansion, but if I see gross margin declines, this hints at problematic projects or execution issues.

With contractors it is important to note however that the timing difference of when projects end and payment milestones on ongoing projects are achieved can have a significant impact on the income statement, making revenue and profit recognition potentially lumpy. This is more apparent in firms that rely on a small number of large projects, whereas for firms like BDT which have achieved massive scale, this is less of an issue as different projects and payment milestones are achieved on an ongoing basis, meaning that for most years, revenue and earnings growth is relatively smooth and when looking at the firm's financials one doesn’t need to be too concerned with ‘normalizing’ the figures.

Rather than looking at normalized figures, I prefer to look at the trends over the last few years.

{kind=link}

Based on the trend I’m seeing, and the strong YTD for 2023, I expect 2023 to look significantly better than 2022, continuing the upward trend. This in my view is one of the several contributing factors to BDT’s stellar returns over the past 6 months. Revenue growth and margin expansion is partially driven by acquisitions (e.g., in 2020 the company acquired Stuart Olson Inc. – a contractor and industrial services outfit), and partially due to strong project execution (delivering projects without cost overruns or delays). The strong revenue growth of almost 19% CAGR is good to see, but even better is seeing the higher revenues are translated into even higher Gross Profit, EBITDA and Net Profit growth, as can be seen through significant margin expansion. All in all, these trends give me some confidence going forward. Gross Profit margins look to be relatively stable in the low 9’s, which I am comfortable with.

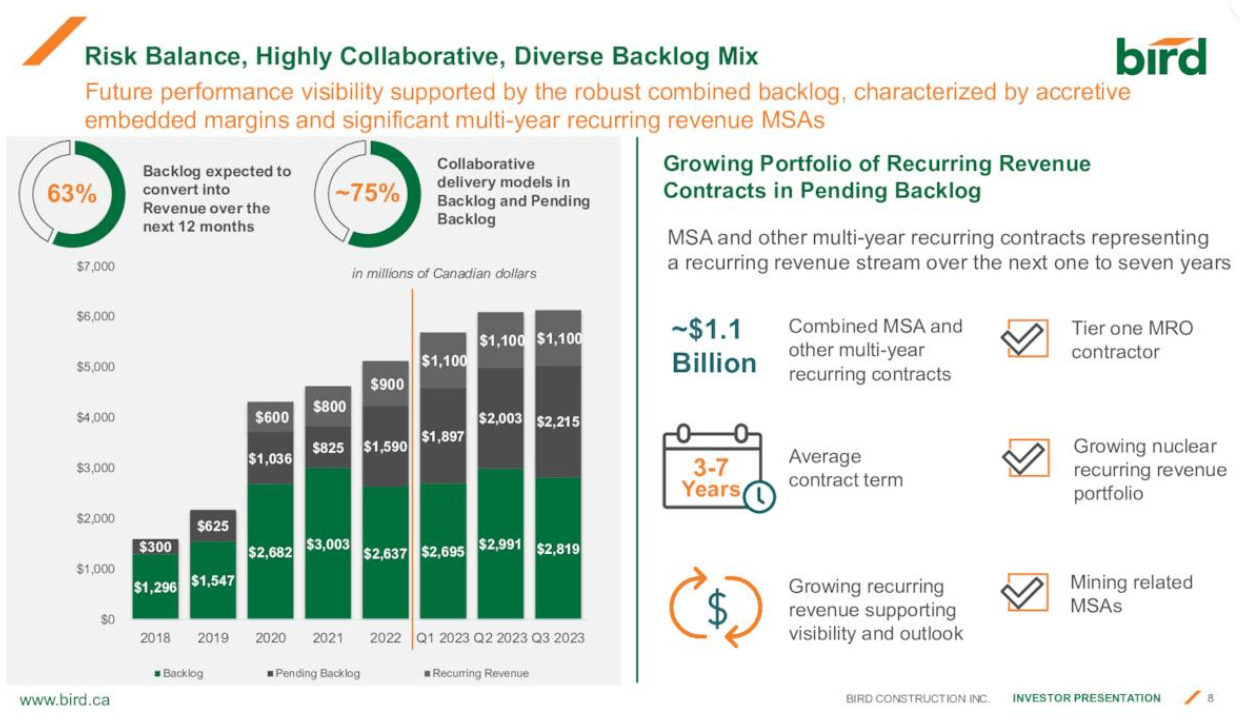

Orderbook

The second performance indicator I review for contractors is their orderbook (or backlog), looking at both sizes, mix and growth over time. As most construction projects are multi-year projects, the orderbook shows how much work-in-hand a contractor has going into the next year(s). This is important as a low orderbook shows that the company is likely going to show significant revenue decline going forward (going idle), whereas an orderbook that is abnormally large can mean the firm is over-extended and taking on too much risk.

Generally, the size of the orderbook for large contractors like BDT (which do a lot of government and large commercial projects), is correlated with the general health of the economy. When the economy is doing well, spending is on new projects tends to be higher and more work is available. When the economy is doing poorly, there is generally less work available (fewer new and large projects started by either the public or private sector), which also means that competition for remaining projects intensifies. This can result in margin compression. In addition, each project a contractor takes on involves risks, what is not great to see is if a firm keeps growing its revenue (and gross profit dollar amount), without margin expansion. If there is revenue and gross profit growth, but no margin expansion, this indicates that the firm is taking on increasing risk (trading risk for dollars in revenue / gross profit).

Mix of the orderbook is also critical, as different types of projects tend to have different levels of profitability associated with them. A shift to higher value projects (e.g., those in the nuclear energy space) can lead to higher margins without the firm needing to take on significant additional risk.

BDT reports its backlog, but also adds a ‘pending backlog’, which it defines as

“T he total potential revenue of awarded but not contracted projects including where the Company has been named preferred proponent, where a contract has not been executed and where the letter of intent or agreement received is non-binding.” - 2022 Annual Report

{kind=link}

While it is always helpful when management provides more information, I choose to ignore this and focus on the actual backlog only. As reported in the Q3 results, 63% of the backlog is expected to be converted into Revenue over the next 12 months. This is on the high side for me, and I will be closely monitoring their full-year announcement to see what the backlog looks like going forward. It is however very encouraging to see that the backlog has been steadily growing from 2018 through 2023 Q3.

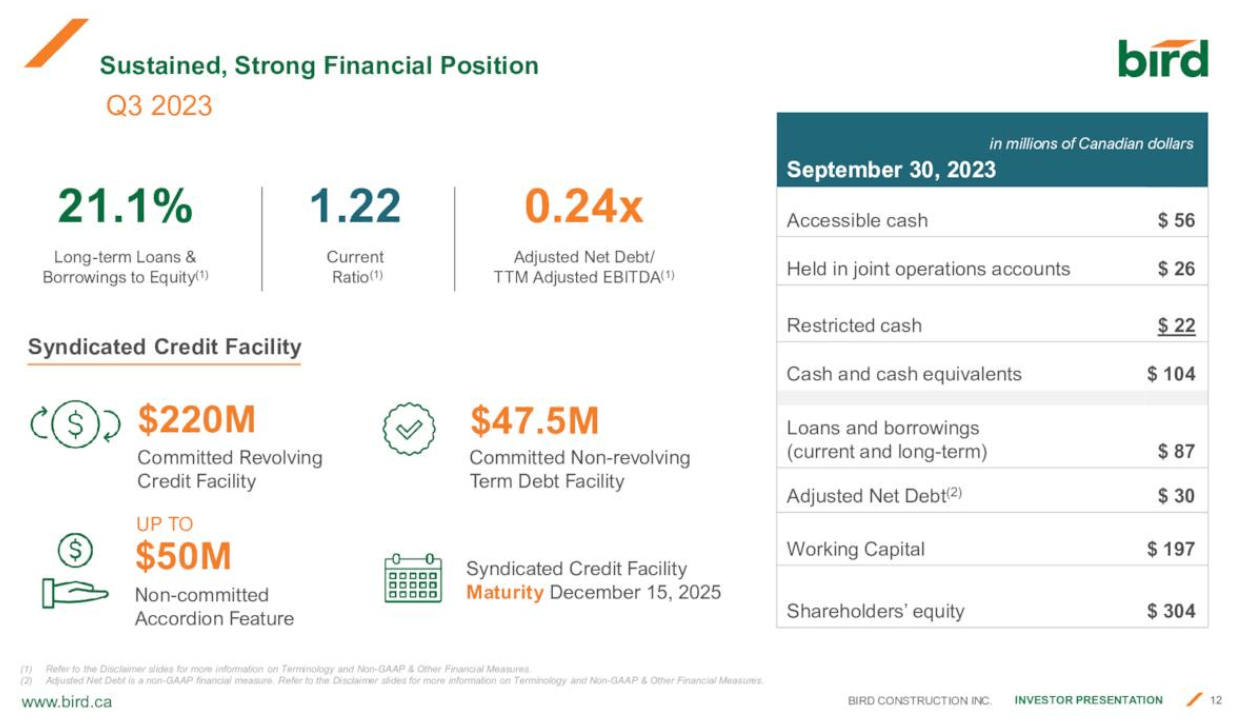

Balance Sheet Strength

Running a successful construction business is essentially all about managing the balance sheet. As such, having a strong balance sheet is critical for firms to succeed and thrive. Looking at BDT’s balance sheet, I am very encouraged to see a very low long-term debt to equity ratio of 21.1%. This is low compared to the 35.2% average long-term debt to equity ratio of the top 32 construction & engineering stocks on Seeking Alpha. It has a current ratio of 1.22 meaning I’m not worried about solvency, and a 0.24x Net Debt to EBITDA ratio. All in all, a huge tick for me.

{kind=link}

Safety Record

Last but not least, the safety record is key for any major contractor. Unfortunately, as long as humans are needed on construction sites, it remains a risky business. Critical for winning future contracts (not to mention being eligible to bid on most government contracts) is a strong safety record. While it is more difficult to measure or quantity, it is encouraging to see that on their website and in their annual report, a lot of attention is paid to safety. A simple google search also did not find any reputational issues in this instance, so while I would keep monitoring this area, I do not see any cause for concern for BDT.

As a result, overall BDT looks promising based on these four criteria for assessment.

Macro Growth Drivers

I always like investing in industries that have strong (and common sense) growth drivers. For the construction industry, I am somewhat concern since the major macro drivers paint a very muted growth picture. Macro growth drivers for this sector include:

Economic Growth & Interest Rates

As mentioned above, with strong economic growth, investment in commercial and government projects is likely to increase. Investment in new projects is also facilitated by lower interest rates driving investment. According to Statista , Canada’s GDP is forecast to grow on average by 1.8% from 2024-2028. This does not really inspire a lot of confidence in high growth going forward.

Infrastructure Spending

Beyond economic growth and interest rates, which generally fuel private sector investment, government spending on infrastructure is also a major driver for the construction industry. According to Mordor Intelligence , this is set to grow by over 4% CAGR from 2024-2029. This is somewhat more positive, but still not explosive.

Sustainability Trends

Construction is one of the ‘dirtiest’ industries when it comes to climate change, contributing nearly 40% of global CO2 emissions . Increasingly, focus on global net zero and adapting our urban environments to climate change is a key topic for legislators and the private sector. This is a major trend that can drive growth in the construction industry for those with capabilities and expertise in this area.

I would sum up the macro trends as providing a relatively muted outlook in the short-term, with possible longer-term tailwinds.

Outlook – 2023 and beyond

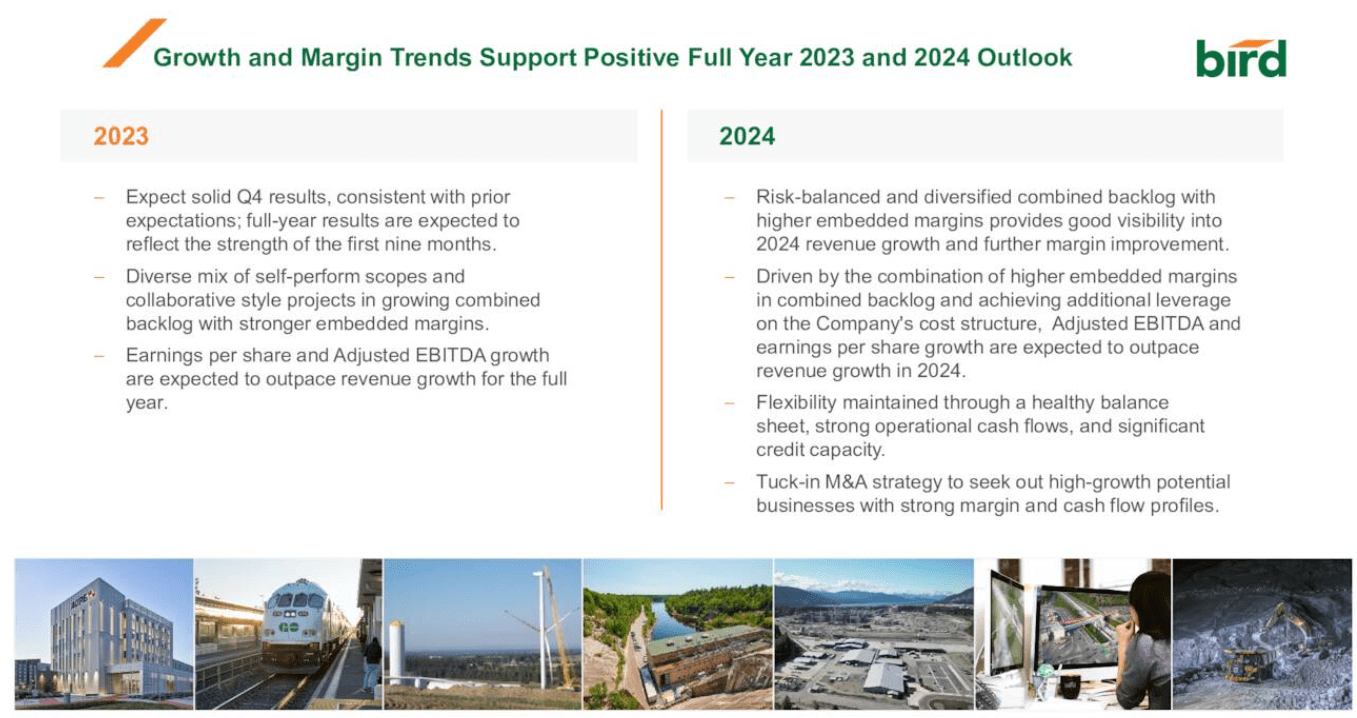

Looking ahead at 2023 full year and 2024, I believe the outlook for BDT is strong. The same trends reported in 3Q23 are likely to persist – strong sales and higher margins being converted into higher earnings. I expect overall revenues to increase by 14-15% for 2023 FY.

{kind=link}

As per the 2024 guidance, I believe 2024 could be another strong year with close to double digit (8-10%) revenue growth with higher margins due to orderbook mix.

Taking a long-term view and looking beyond 2024, I believe the future of BDT’s success will depend on a few key factors:

Project execution

As in most businesses, it all comes down to execution in the end. BDT needs to continue its disciplined cost management to ensure it protects margins and does not lose money on major projects. Most importantly is delivering projects to the highest quality standard, without delays. Liquidated damages on major projects can add up extremely quickly and be ruinous financially. It only takes one major project delay to wipe out company profits, so a key focus is on execution.

Perhaps equally, if not more important, is their continued focus on safety. It takes years to build a reputation, but only seconds to ruin it. BDT has a strong industry reputation for safety, and it is imperative it does not damage this with accidents on their construction sites.

Securing its orderbook

BDT will need to continue to replenish and grow its orderbook every year, making sure it has enough work-in-hand for the future. Especially as it continues to look for M&A opportunities, with the growth in scale of their business, it is important they grow their order book accordingly.

Orderbook mix is also extremely important going forward, especially BDT’s ability to position itself to win in high-growth and high-margin sectors relating to the energy transition. So far it has done a great job, but it is important that it keeps on securing high-profile reference projects that reinforce their reputation as leaders in this sector.

Operational efficiency

Wage and raw inflation plague virtually every industry, as such it will be important for BDT to mitigate these cost increases as much as possible to protect their margins and to avoid margin compression.

Macroeconomic risk

As mentioned above, the industry’s fate is closely tied to generally healthy economic activity. Should there be major shocks (recession, war, other) this can have a major impact on BDT (and its competitors) going forward.

Overall, I am bullish about BDT’s future in the next 1-2 years, as I believe BDT is well positioned to deliver above market-growth, while improving its orderbook mix thus translating into higher margins. My major concern remains the long-term growth prospects of this industry (mainly due to lackluster GDP growth). Should that concern be alleviated, I think BDT is well positioned to be a great pick for income seeking investors.

Valuation and Shareholder Value

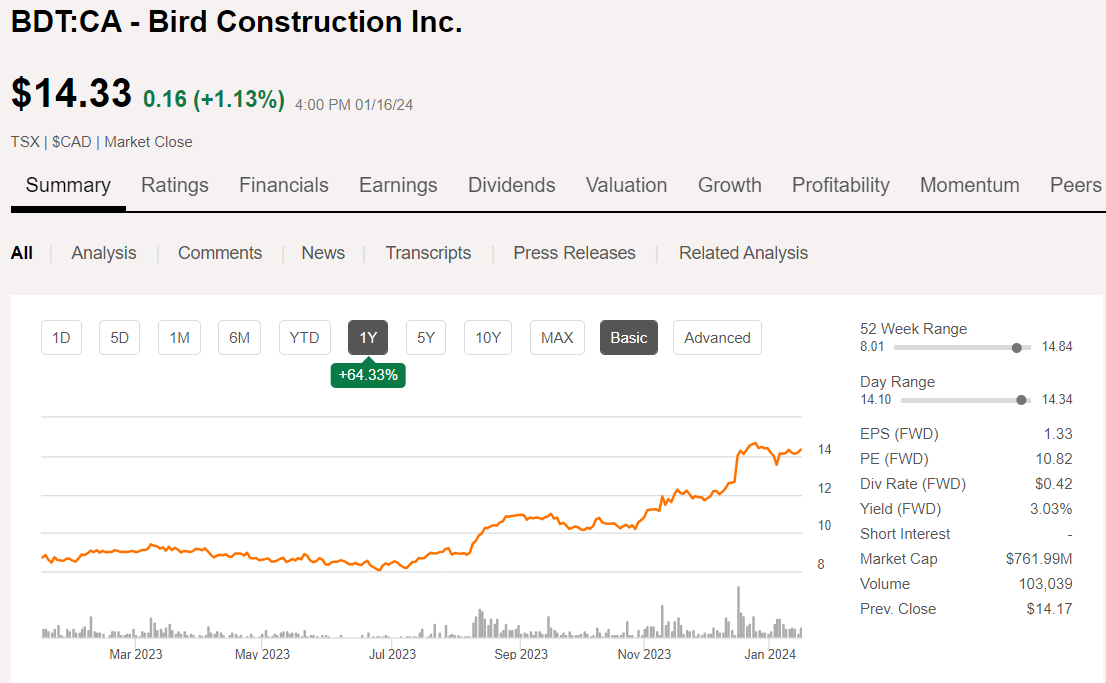

BDT’s shares are up 64.3% in the last year closing at 14.33.

{kind=link}

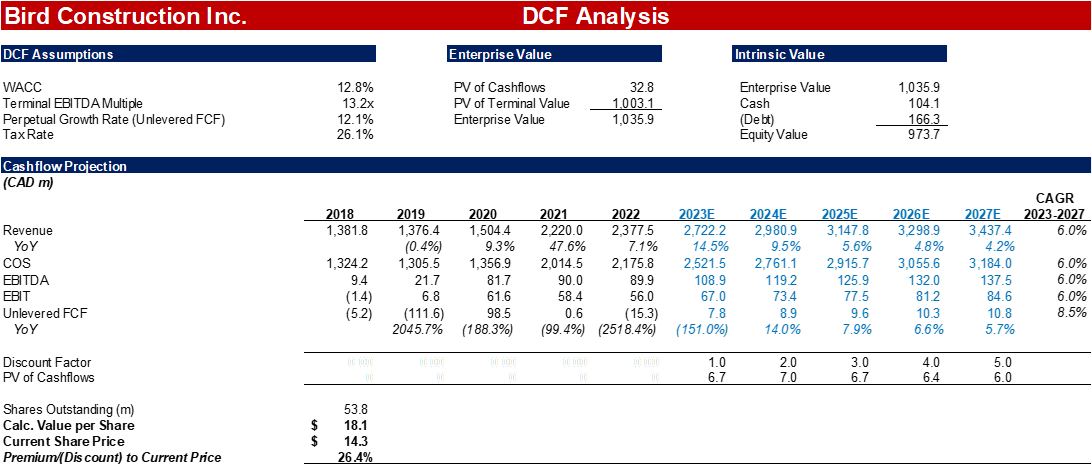

Over the last 5 years, shares are up 115.5%. Looking ahead I am positive about future earnings, mainly due to management’s track record of execution, its growing orderbook size and mix change to higher value sectors. I think some of this has already been priced in over the last 12 months, but believe some upside remains. Based on my DCF model, I have a long-term price target of c. 18.1, indicating a potential upside of 26%.

{kind=link}

In addition, BDT currently pays a monthly dividend with a 3.03% yield – I consider this an attractive yield, especially since the dividend was raised by 30.4% in December. I believe dividend increases will continue as earnings increase and margins improve, though don’t expect another drastic hike like the previous one.

Unfortunately, BDT is not covered by the quant ratings, but Wall Street rates it as a “Buy”. I concur and think this is an interesting time to start a position in the stock.

Takeaway

Based on my DCF analysis, I believe BDT is currently trading 26.4% below its intrinsic value, while offering a monthly dividend of 3.03% and thus believe the stock is a "Buy".

Management has done a great job over the past few years to grow revenue, expand margins and strengthen the orderbook in terms of size and mix, all while maintaining an exceptional balance sheet and raising the dividend. All of these are big ticks in my book. The only caveat I have here is the correlation the construction industry has with the strength of the economy. As economic growth in Canada is somewhat muted for the next few years, this poses a headwind for future growth. That said, due to its over 100 years in existence, I believe Bird Construction is well positioned to capture growth going forward. At this level I believe the stock presents a relatively favorable risk/reward opportunity for those looking to start a position.

For further details see:

Bird Construction: A High-Flying Pick For Canada Construction