BOIVF - Bireme Capital Q1 2023 Quarterly Report

2023-06-28 05:15:00 ET

Summary

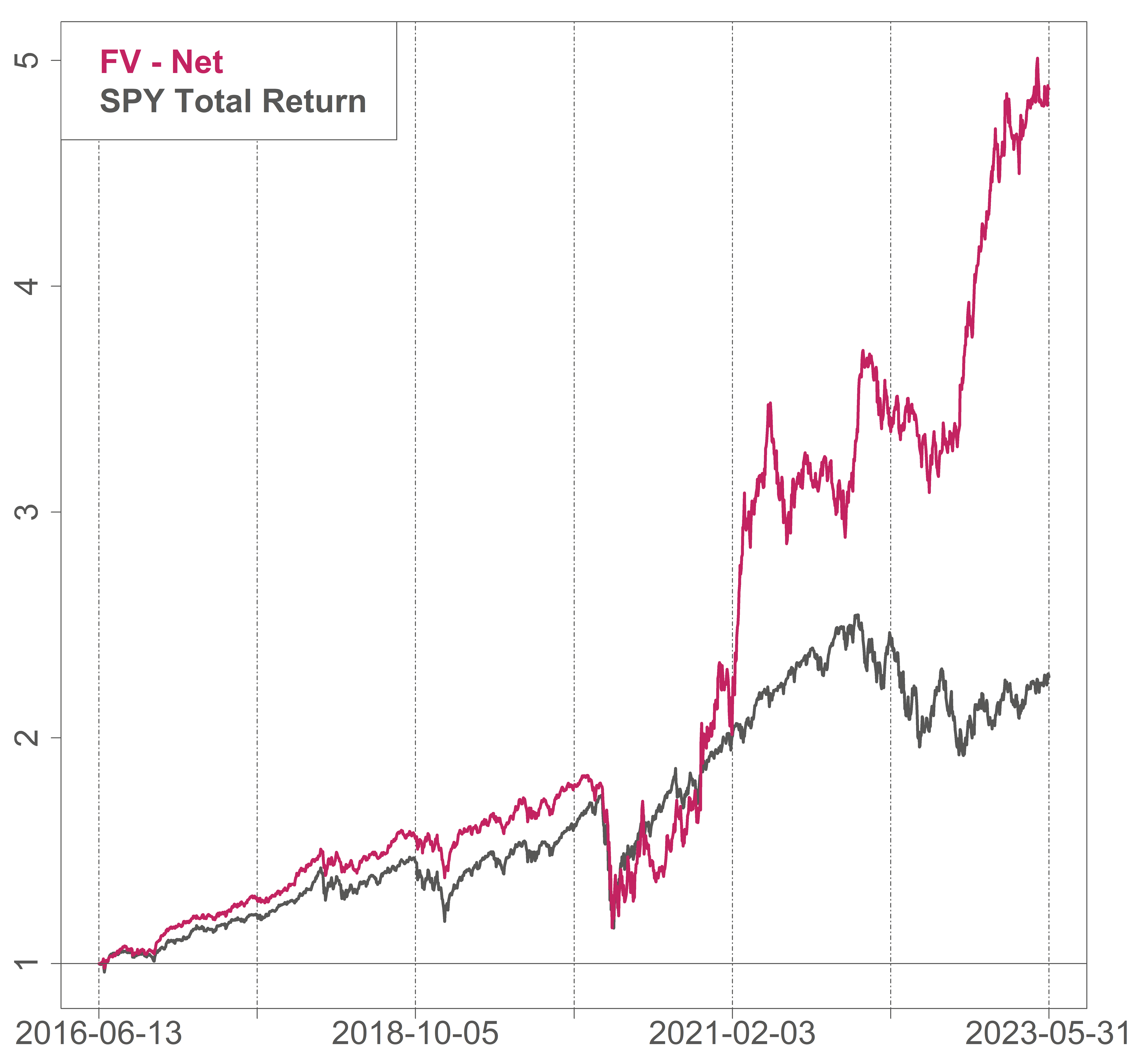

- Bireme Capital's Fundamental Value returned 8.0% net of fees in the first 5 months of 2023, slightly trailing the S&P 500.

- Equities are priced for a Goldilocks economic scenario: not too hot, not too cold.

- Bireme Capital initiated a significant new investment in Airtel Africa and added a short position on Sunrun Inc.

Fundamental Value returned 8.0% net of fees in the first five months of 2023, slightly trailing the S&P 500's 9.7% return. The strategy has compounded at 25.5% net annualized in the seven years since inception, besting the market by 13% a year. 1 For monthly performance see our tearsheet .

{kind=link}

{kind=link}

Market commentary

A year and a half ago, we had just finished our “Everything Bubble” series, and the path ahead seemed remarkably clear to us. We predicted severe declines for the most speculative growth names, strong relative performance for value stocks, and the rise of interest rates due to the return of inflation. We wrote :

Extreme valuations presage real returns that investors will find severely disappointing -- and likely negative -- for many asset classes over years to come.

That script played out largely as we expected. Speculative securities have been decimated, the fed funds rate is now 5% higher, the real yield on TIPS has gone from nearly -1% to over 1.5%, and analyst estimates for 2023 S&P 500 earnings have come down -6%.

Yet equity indices remain eerily resilient. We wrote last quarter :

Since we published Part III: Apex of a Bubble on September 21st 2021, we’ve seen the largest reduction in fiscal stimulus on record, the fastest spike in real yields, the worst annual performance for Treasuries, the fastest pace of monetary tightening in generations, and the reversal of a decade of quantitative easing and zero interest rates.

Despite the S&P's bubble-like valuations in 2021 and the subsequent upheaval in many corners of the financial markets, the S&P is up 3.5% since Apex of a Bubble. Thus, the equity risk premium remains perilously thin.

Equities are priced for a Goldilocks economic scenario: not too hot, not too cold. A hot economy with stubbornly elevated inflation is a problem for valuations. A cold economy with recession is a problem for earnings. Our personal view is that the too-hot scenario is the most likely -- the labor market and hence the consumer remains extremely strong -- but either outcome seems possible.

The Goldilocks "just right" economy -- where inflation falls rapidly back to the Fed's 2% target without significant pain for corporations, consumers or credit -- is possible as well. However, this feels like wishful thinking.

We have just seen the end of various multi-decade trends in interest rates and inflation. And in just the last few years, we've seen the greatest monetary policy experiment of all time, with negative real interest rates and trillions of dollars of quantitative easing, and the greatest fiscal policy experiment of all time, with record transfer payments supporting the economy. Virtually overnight, these distortionary impulses were withdrawn.

We should expect some dislocations.

Fundamental assumptions will be challenged. For the past forty years -- most investors' entire careers, and our entire lives -- interest rates have been declining. A trend that persists for so long inevitably becomes ingrained into investor psychology.

This is perhaps best illustrated by the notion of the "Fed put," the assumption that the Federal Reserve will step in to rescue the equity market should it decline. We have argued that, due to the new inflationary environment, there is now a "Fed call," a limit to how much investors can make rather than how much they can lose, as the Fed will need to stomp on the brakes whenever the market and economy get too hot. After many years of pushing on a string, distorting financial markets to try to bring strength to the real economy, the Fed is now attempting the reverse. The string has a lot of slack that needs to be reeled in before we see real economic effects.

Another area of concern is commercial real estate. There are obvious economic headwinds due to work-from-home. But there's also risk due to the pernicious assumptions ingrained in investor psychology after forty years of declining rates: that refinancing is always possible, that new debt will be issued at a lower rate than old debt, and that cap rates are perpetually declining. Prior to 2022, there had been fewer than five months since 1980 when the 10-year Treasury was not lower a decade later. Thus, if you issued debt, it was a virtual certainty you'd be able to reissue it again down the road at a lower interest rate, or sell the property at a lower cap rate than you paid. When it becomes apparent this is no longer true, it may cause a step change in CRE valuations.

These are but two examples of potential fallout from unspoken assumptions as economic reality changes. There have been some dislocations already. The demise of Silicon Valley Bank was in a way a story of assuming away interest rate risk: mistaking the historical accident of declining rates for economic reality. But it is hard to predict where further fallout will happen in advance. As David Foster Wallace memorably said , fish don't notice the water in which they swim: "the most obvious, important realities are often the ones that are hardest to see and talk about."

In an environment of change and uncertainty, what can you do to protect yourself? You can own reasonably-valued assets with inflation protection and little refinancing risk. For us, that means a conservatively positioned portfolio of companies with pricing power, without an onerous debt load, with visibility to sufficient free cash flow such that we would be happy to own it forever if valuations fall.

It’s not too late to join us at Bireme. Please reach out.

Portfolio commentary

Our biggest winner through May 2023 has been Meta Platforms ( META ). The stock is up 120%, with business results surprising to the upside on both revenue and expenses. On expenses, the company announced two large layoffs since we initiated our position last year: 10,000 in Nov and 11,000 in March. The impact of these layoffs has been dramatic. Our initial estimate of 2023 expenses made back in early 2022 was nearly $100b, but we now forecast 2024 expenses of just $85b. And it is not just near-term expenses that are getting cut: Zuckerberg told employees in April to expect ongoing employee growth of 1-2% per year. This is far below previous levels of 20-30%. Given our estimates of mid-single-digit revenue growth, Meta could exhibit material operating leverage going forward and $20 in core EPS is in sight.

Cogeco Inc ( CGO:CA ), our Canadian broadband investment, has been a material loser with the stock down 20% YTD. Shares have now lost 10% over the past five years, significantly trailing the broader market. This is despite earnings growing from 6 CAD per share in 2017 to over 9 CAD per share last year.

While earnings have grown, investors have become concerned about a decline in near-term free cash flow. This metric has fallen from CAD 487m in FY2021 to CAD 362m on a trailing 12-month basis. Cogeco has explained that this is due to CAD 200m of network expansions, and that otherwise free cash flow would be flat this year. Still, even flat earnings and FCF are concerning due to the growth capex being spent: earnings should be expanding. That being said, any short-term concerns about free cash flow appear overly discounted in the stock, which trades at a PE ratio of around 5x.

Our basket of small community banks, initiated in 2020, has been the position we have pondered most this year. After much contemplation we increased our size in multiple banks.

Our community banks enjoy multiple advantages over larger regional peers like SVB, First Republic ( FRCB ), and PacWest ( PACW ) in the current economic climate. The first is little exposure to depositors with ties to Silicon Valley, whose deposit balances are highly correlated with the economy and with each other. When the economy was roaring, startups were flush with cash, and many flocked to these regional banks. As funding dried up, deposits were drawn down, and then fled for the exits at the first sign of trouble. In contrast, our banks have a diverse depositor base with most balances below FDIC insurance limits. This makes bank runs unlikely. In fact, our banks added deposits in Q1 despite the market turmoil.

Second, our banks have little exposure to the “held to maturity” bonds which put gaping holes in SVB’s balance sheet when the Fed raised interest rates. Greater than 99% of the earning assets of our banks are cash, loans, and marked-to-market securities, leaving little danger of opaque losses that suddenly hit headlines and drive deposit flight.

There are plenty of other things to worry about though, and the scale of the increase in the fed funds rate may crimp net interest margins over the next few years. But the magnitude of the likely earnings drop has been dwarfed by stock price moves. Our banks generally trade at 5-6x 2023 earnings, more than compensating for earnings risk. And, contrary to expectation, we may even see a more profitable era of banking in the relatively near future. Historically, periods with 4-5% fed funds rates have been a great time to be a bank investor, with higher-than-average NIMs of 3.5%-4% in these environments.

| |

| Source: Bloomberg's BRATNIMT Index |

We are sticking with our bet, although for risk management purposes we are keeping the size of the basket below 10% of NAV. This means that any individual bank failure cannot directly cost us more than 2% of NAV.

In April we made a significant new investment in the company Airtel Africa ( AAFRF ). Airtel is a leading mobile wireless operator in Sub-Saharan Africa, with operations in 14 countries and #1 or #2 market share in nearly all of them. Their business has exhibited consistent revenue growth as subscribers and pay-per-gigabyte data usage grow exponentially. Operating income has doubled since FY 2019. Airtel also operates a leading peer-to-peer payments network which did over $300m in EBITDA last year. This business has been growing at double-digit rates for years as unbanked Africans switch from cash to digital payments, typically provided by their mobile operator. Airtel is likely to facilitate more than $100b in transfers this year.

Despite this secular growth story, the stock trades at 8.5x earnings and an even lower multiple of maintenance free cash flow. We think that the stock is suffering from familiarity bias, the tendency for investors to focus on stories they know and understand well. Airtel’s operations are across 14 African countries, but it trades in London, reports in US dollars, and is majority owned by an Indian telecom operator. This makes a natural investor base hard to find. Contrast this with Airtel’s peer MTN, which is one of the premier firms listed locally on the Johannesburg Stock Exchange and has historically traded at a substantially higher multiple.

Given that Airtel has tripled EBIT since 2018, in contrast to MTN’s mere 50% growth in USD, we are happy to own Airtel as long as the discount persists and the business continues thriving. Our average price is around 115 GBP per share. You can read our full Airtel write-up here .

Our portfolio holding Bollore ( BOIVF ) has had multiple major updates since the start of the year. First, on March 14, the company announced a tender offer whereby they would buy back 288m shares – about 20% of the adjusted float according to our calculations – for 5.75 EUR per share. We don’t plan to tender any shares. Then, in April, the company announced that it had received an offer for the Bollore Logistics business for 5.5b EUR. If they end up finalizing that deal, the board has agreed to improve the tender offer to 6.00 EUR per share. We feel this still undervalues the stock by a wide margin, given the net assets of the post-sale firm will be more than 13 EUR per share when treasury shares are properly accounted for.

It looks increasingly likely that Bollore will emerge from these transactions with a war chest of $6-8b of net cash, $7b worth of UMG and $3b of Vivendi shares at current market prices. Given the current market cap of just under 8b EUR we intend to continue to hold the shares we’ve owned since 2016. In fact, we've added to our position this year despite shares rising about 10%.

We've added a short position: Sunrun Inc. ( RUN ) Sunrun is one of the most cash-destructive businesses we’ve ever come across, with the solar installation firm burning more than $1b every year since 2019 to put panels on roofs. The company claims that GAAP accounting – which tallies negative retained earnings of around $70m since the birth of the company — cannot quite comprehend the economic value the company generates. Instead, management stresses mark-to-model accounting that reminds us of Enron .

Unsurprisingly, Jim Chanos, one of the most vocal Enron short sellers, is all over Sunrun as well. As he and Carson Block of Muddy Waters point out, the only way for the company to show positive unit economics is to make very favorable assumptions about contract renewals and maintenance costs. Muddy Waters estimates that the true economic value of the company’s contracts is up to 90% lower than described by management. We would also add that higher interest rates are not likely to help the economics of solar installations, and should lead to much lower net subscriber values. Our average price for the short position was $23.14.

We are grateful for your business and your trust, and a special thank you to those who have referred friends and family. There is no greater compliment.

Bireme Capital

Footnotes

1 FV performance is shown net of a 1% management fee and 10% performance fee. Available for Qualified Clients only as SEC rules do not permit performance fees for nonqualified investors. Fee structures and returns vary between clients. FV inception was 6/14/2016.

Advisory fees and other important disclosures are described in Part 2 of Bireme’s Form ADV. The performance in the table is the performance on a dollar-weighted average of the securities in the Fundamental Value L/S model portfolio from inception through the end date specified above. Past performance is not indicative of future results. Different types of investments involve varying degrees of risk and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. The SPY ETF seeks to track the performance of the S&P 500 Index, and the performance described includes both fees and the reinvestment of dividends and other distributions. Performance is shown net of a 1% management fee and 10% performance fee. Available for Qualified Clients only as SEC rules do not permit performance fees for nonqualified investors. Registration does not constitute an endorsement of the firm, nor does it indicate that the advisor has attained a particular level of skill. See biremecapital.com/disclaimer for important disclosures.

Sources: Bloomberg Finance LP, Interactive Brokers LLC, S&P Compustat, Bireme Capital LLC.

For further details see:

Bireme Capital Q1 2023 Quarterly Report