BIT - BIT: Some Good Things But Distribution Sustainability Is Questionable

2023-05-23 05:25:27 ET

Summary

- Investors are desperate for income today because of the rapidly-rising cost of living.

- BIT invests in a portfolio of traditional fixed-income and alternative credit securities to provide a high level of current income to its shareholders.

- The fund could be negatively impacted if inflation takes off again, and a possible near-term crude oil shortage could be a catalyst for this.

- The fund appears to be overdistributing as its assets have declined over the trailing two-year period, so it may be forced to cut at some point.

- The fund is trading at a discount to the net asset value, but a bigger one would be nice due to the risks here.

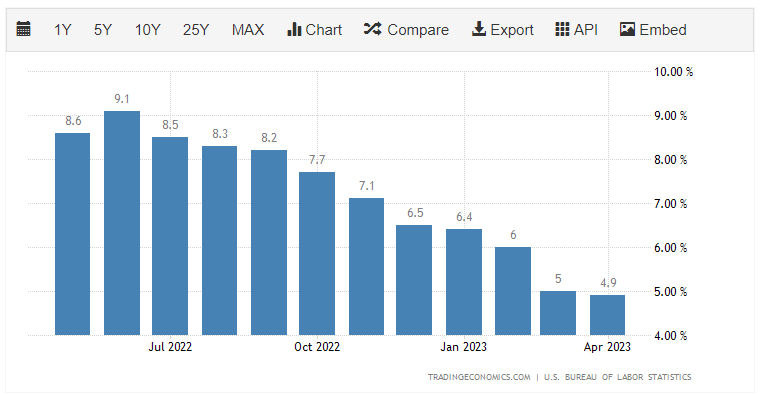

There can be very little doubt that one of the biggest problems facing the average American today is the rapidly rising cost of living in the United States. This is showcased in the consumer price index, which claims to track the price of a basket of goods that the average person regularly purchases. As we can see here, this index has increased by at least 6% year-over-year in ten of the past twelve months:

{kind=link}

While this chart seemingly shows that inflation has been slowing recently, this has been entirely driven by weakening energy prices. In fact, if we were to consult the core consumer price index, which excludes volatile food and energy prices, we would not see the same moderation. I pointed this out in a recent blog post . The fact that much of the increase in the cost of living has been in necessities has resulted in severe strain for people of moderate means, which explains why there has been a surge in second job-holders and why consumer debt levels just hit a record level . Clearly, the average person is searching desperately for ways to increase their income to maintain their living standards.

As investors, we are certainly not immune to the impacts of inflation. After all, we have bills to pay and need to eat just like anyone else. Fortunately, we do have other options available to us that can be employed to obtain the extra money that we need to maintain our lifestyles. Perhaps the best of these methods is to purchase shares of a closed-end fund that specializes in the generation of income. These funds are unfortunately not very well followed in the media and most financial advisors are unfamiliar with them, which makes it difficult to obtain the information that we would like to have to make an informed decision. That is a shame because these funds offer a number of advantages over ordinary open-ended funds or exchange-traded funds. In particular, closed-end funds are able to employ certain strategies that can boost the effective yields of their portfolios well beyond that of the underlying assets or pretty much anything else in the market.

In this article, we will discuss the BlackRock Multi-Sector Income Trust ( BIT ), which is a closed-end fund focused on providing its investors with income. This is made obvious by the fact that this fund boasts a very attractive 10.35% yield at the current price. I have discussed this fund before, but several months have passed since that time so obviously several things have changed. This article will therefore focus specifically on these changes as well as provide an updated analysis of the fund's financial condition. Let us investigate and see if this fund could be a worthy addition to a portfolio today.

About The Fund

According to the fund's webpage , the BlackRock Multi-Sector Income Trust has the stated objective of providing its investors with a high level of current income. This is not especially surprising considering the fund's name and the fact that it is a fixed-income fund. As we can clearly see here, the fund's portfolio consists almost entirely of bonds and preferred stocks:

CEF Connect

We do note here that the fund has a negative allocation to cash. This comes from the fact that this fund employs leverage as a way to boost its effective yield. We will discuss this later in this article. The important thing for our purposes right now is that this is a fixed-income fund.

However, the fund's portfolio does not consist entirely of traditional fixed-income securities. As the fund explains on its webpage,

BlackRock Multi-Sector Income Trust's primary investment objective is to seek high current income, with a secondary objective of capital appreciation. The trust seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its assets in loan and debt instruments and other investments with similar economic characteristics.

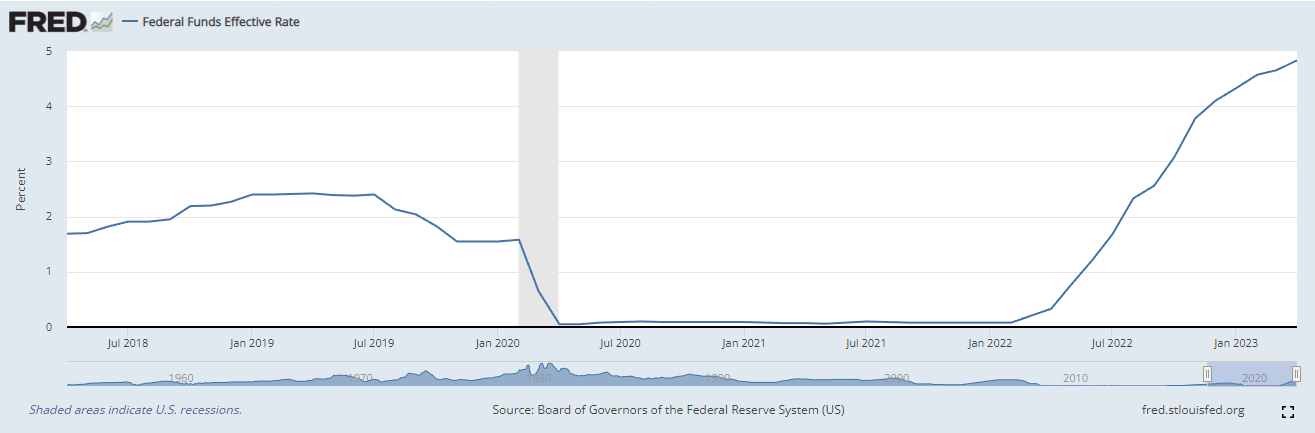

This description implies that this fund can invest in both traditional fixed-income securities and alternative credit, such as floating-rate bank loans. This is a very important factor to consider today since, as I have pointed out in numerous previous articles, floating-rate securities are superior to traditional fixed-income products in today's market. This is due to the relationship that bonds have with interest rates. It is an inverse correlation, so when interest rates go up, bond prices decline and vice versa. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates over the past year to levels that are far beyond the levels that caused the problems in the market back in 2018:

{kind=link}

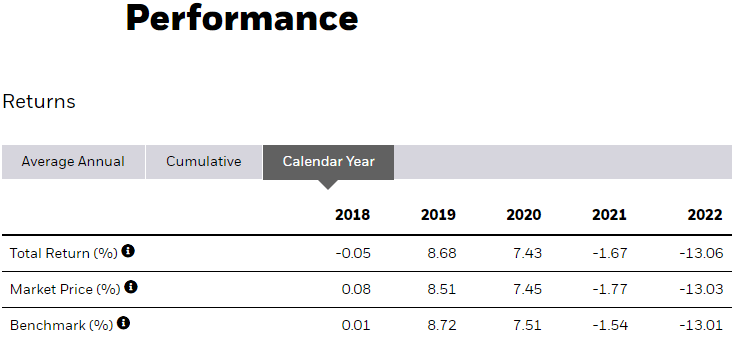

This has had the effect of devastating bond prices. Anyone that was invested in traditional bonds or bond funds over the course of 2022 can attest to this, as the Bloomberg U.S. Aggregate Bond Index ( AGG ) fell by 13.01% in that year:

{kind=link}

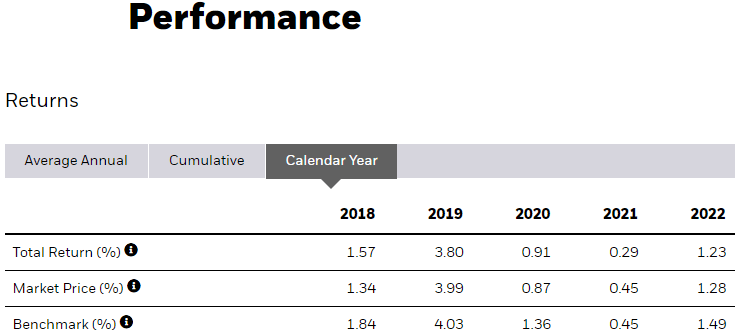

The reason for this is that bonds are issued with a coupon yield that corresponds to the market interest rate at the time of issuance. Thus, a bond that is issued when interest rates were lower will have a lower yield than a bond issued in a high-rate environment based on the bond's face value. As interest rates have risen over the past year, nobody will want to pay full price for an existing bond when they could buy a brand-new one with a much higher yield. As such, the price of existing bonds will need to decline until they deliver a competitive yield-to-maturity as a brand-new bond with identical characteristics. This does not apply to floating-rate bonds, however, as they should keep a relatively stable price since the coupon rate will adjust so that they always deliver a competitive yield. We can see this by looking at the Bloomberg US Floating Rate Note Index ( FLOT ), which delivered a positive total return in 2022:

{kind=link}

The reverse is true in falling rate environments. In such an environment, traditional bonds should outperform floating-rate securities since the traditional bonds will appreciate in price but the floating-rate securities will not. The fact that this fund can invest in both types of debt security thus provides it with the ability to provide its shareholders with acceptable total returns in any interest-rate environment.

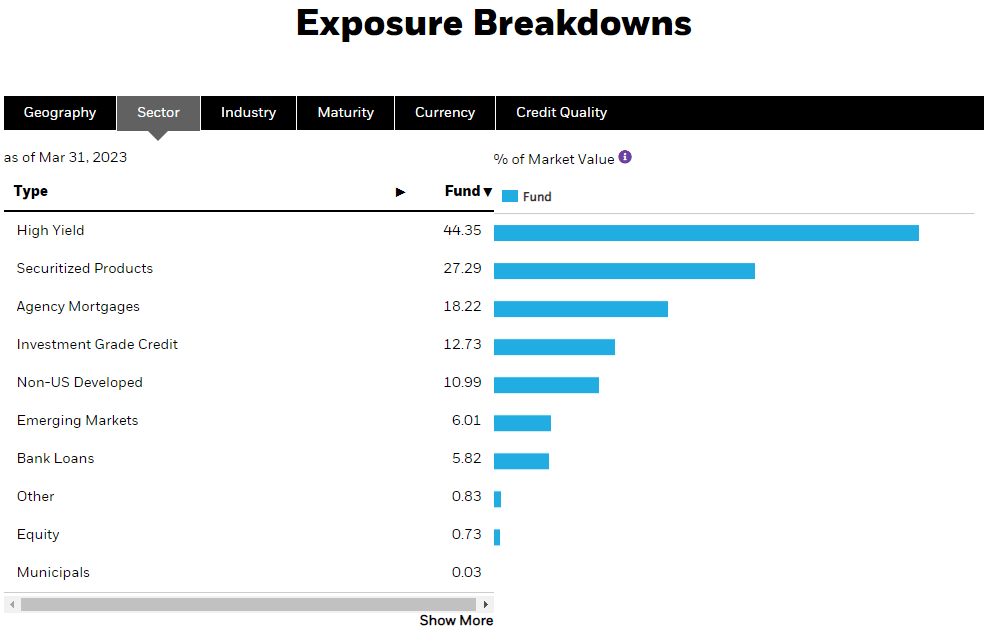

Interestingly, the BlackRock Multi-Sector Income Trust is not heavily weighted to floating-rate securities right now. In fact, high-yield bonds ("junk bonds") currently comprise the largest weighting in the portfolio at 44.35% of total assets:

{kind=link}

The fact that the largest weighting in the fund is high-yield bonds may cause concern among those investors that are concerned with the preservation of principal. After all, we have all heard that junk bonds have a fairly high default risk. They do have higher yields than other bonds to compensate investors for this higher risk of principal loss, however. The high yields could be attractive for a fund like this due to the higher income that these bonds will provide to the fund. That is, of course, assuming that it is appropriately managing the default risk to minimize losses.

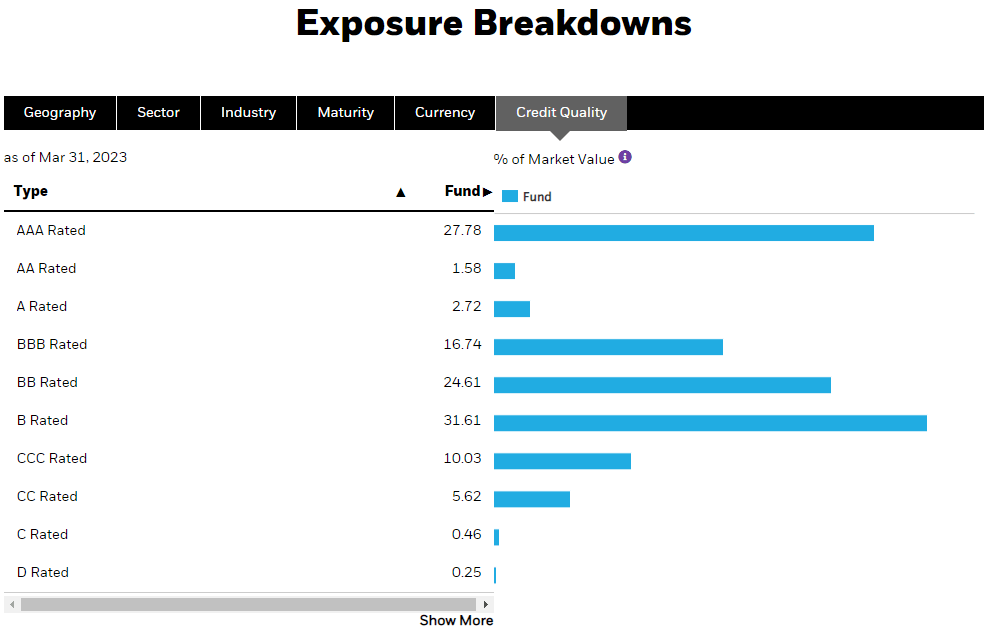

Fortunately, the fund appears to be doing exactly that. We can see this by looking at the ratings of the various securities comprising the fund's portfolio. Here is a high-level overview:

{kind=link}

An investment-grade bond is anything rated BBB or higher. As we can clearly see, that accounts for 48.82% of the portfolio. The remainder is what could be termed junk debt. However, we can see that fully 56.22% of the fund consists of debt securities that have either a BB or B rating. These are the two highest possible ratings for speculative-grade securities. According to the official bond ratings scale , companies with these ratings have the financial capacity to carry their current debt as well as withstand a short-term economic shock without encountering any problems. Thus, these securities should have a very low risk of losses due to default. That combined with the investment-grade securities represents the overwhelming majority of the portfolio. As such, we should be fairly confident that the risk of principal loss here is pretty low. The biggest risk here by far is interest-rate risk.

At this point, it is uncertain where interest rates will be going. The market is currently pricing in an interest rate cut in the second half of the year, but I view that as unlikely. Various Federal Reserve officials have been promoting a "higher for longer" policy, which would preclude any interest rate cuts this year. While inflation has been coming down, it still remains well above the central bank's 2% year-over-year target, and any cuts risk restarting inflation. That will probably make the bank reluctant to cut interest rates. In addition, as I mentioned in the introduction, the year-to-date decline of crude oil and natural gas prices is a major reason why headline inflation has come down. The International Energy Agency is projecting that there will be a global shortage of crude oil by the end of the year. That scenario would almost certainly drive crude oil prices up and reverse much of the progress in the inflation fight so far. It may, in fact, force the Federal Reserve to raise rates more. As such, I think that the worst of the effects of the central bank's tightening is probably behind us, but bonds are not completely out of the water yet. As such, it might be best to dollar-cost average into this fund to limit your risks as its exposure to floating-rate securities is currently not high enough to remove the risk of further rate hikes.

Leverage

In the introduction to this article, I stated that closed-end funds like the BlackRock Multi-Sector Income Trust have the ability to employ certain strategies that can boost their yields well beyond that of any of the underlying assets in the portfolio. One of these strategies is the use of leverage. In short, the fund is borrowing money and using those borrowed funds to purchase bonds and other fixed-income assets. As long as the interest rate that the fund has to pay on the borrowed money is lower than the yield of the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage because that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of its assets for this reason. This fund is unfortunately above this level as its levered assets currently comprise 34.61% of the fund's total assets. With that said fixed-income funds like this one can usually handle higher levels of leverage than can equity funds due to the lower volatility of their assets. This fund is also not much above that maximum leverage requirement, so it is probably okay in this respect. The balance between risk and reward appears to be acceptable.

Distribution Analysis

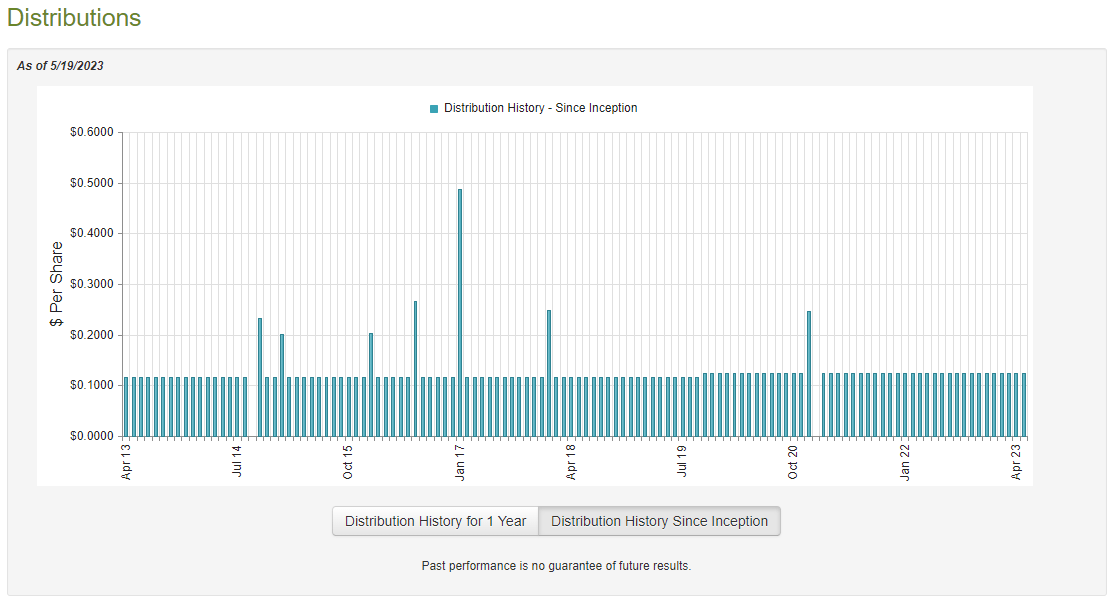

As stated in the introduction, the primary investment objective of the BlackRock Multi-Sector Income Trust is to provide its shareholders with a very high level of current income. In order to accomplish this task, the fund invests in a combination of fixed-income and alternative credit instruments, including junk bonds. As many of these assets have fairly high yields, we can assume that this fund will have a respectable yield itself. This is especially true when we consider that the fund is using a layer of leverage to boost the effective layer of leverage. This is certainly the case as the fund pays out a monthly distribution of $0.1237 per share ($1.4844 per share annually), which gives it a 10.35% yield at the current price. The fund has a very long history of consistency with respect to its distribution over the years:

{kind=link}

As we can see, this fund has never cut its distribution over its lifetime. In fact, its distribution has only been changed once and it was an increase. This is very different from nearly every other fixed-income fund, as most funds have a distribution that varies with interest rates. While this fund's consistency will certainly appeal to those investors that are seeking a safe and secure source of income to use to pay their bills and finance their lifestyles, we want to pay special attention to its finances so that we can determine how it has been able to pull off a feat that no other fixed-income fund has managed to accomplish.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. The fund's most recent financial report corresponds to the full-year period that ended on October 31, 2022. As such, it will not include any information about the fund's performance from the past six months. That is unfortunate since the bond market has strengthened somewhat since the start of this year, which likely allowed the fund to secure some gains. With that said, this report is more recent than the one that we had available to use the last time that we discussed this fund and so should give us a better idea of how well the fund handled the extremely challenging conditions in the bond market during 2022. During the full-year period, the fund received $1,591,245 in dividends along with $49,399,461 in interest from the assets in its portfolio. When combined when a small amount of income from other sources, the fund reported a total investment income of $51,055,768 during the period. It paid its expenses out of this amount, which left it with $38,948,323 available for the shareholders. This was unfortunately not nearly enough to cover the $55,884,385 that the fund paid out to its investors in distributions over the full-year period. At first glance, this is something that is likely to be concerning as the fund's net investment income was not nearly enough to finance the distributions.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distributions. For example, it might have capital gains that could be paid out to the shareholders. As might be expected considering the challenging market conditions for bonds, the fund failed miserably at this task. During the period, the fund achieved net realized gains of $5,527,115 but this was more than offset by net unrealized losses of $113,608,350. Overall, the fund's assets declined by $123,839,140 over the full-year period after accounting for all inflows and outflows. Clearly, that is not nearly enough to cover the distribution. The fund did manage to cover its distributions in the prior year, but it still failed to accomplish this task over the two-year period. On November 1, 2020, the BlackRock Multi-Sector Income Trust had total assets of $662,853,265 but this figure had fallen to $552,552,245 on November 1, 2022. Thus, the fund has been overdistributing and it may have difficulty sustaining its current distribution if things do not improve for it shortly.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the BlackRock Multi-Sector Income Trust, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. This is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. That is fortunately the case with this fund today. As of May 19, 2023 (the most recent date for which data is currently available), the BlackRock Multi-Sector Income Trust had a net asset value of $14.44 per share but the shares currently trade for $14.27 each. This gives the shares a 1.18% discount to net asset value at the current price. This is much better than the 0.07% premium that the shares have had on average over the past month. Thus, the current price appears to be reasonable, although I would like to see a bigger discount considering the risks to the distribution.

Conclusion

In conclusion, the BlackRock Multi-Sector Income Trust provides a solution for those investors that are seeking a high level of income today. The fund employs a leveraged portfolio of bonds and alternative credit issued by a variety of sectors that should provide diversification to a portfolio and reduce default risk. Unfortunately, it appears that this fund is over-distributing and may be forced to cut its payout soon if it cannot generate substantial gains in the near future. This seems unlikely given the current likely path for interest rates. As such, it may be best to either slowly accumulate or wait for a bigger discount before buying in.

For further details see:

BIT: Some Good Things, But Distribution Sustainability Is Questionable