GLNCY - Bitten By The FAANGs? Try My CCLANGs Instead!

Summary

- The FAANG companies have left some pretty bloody marks on those who held… and held… and held this year.

- The best-managed of these will recover their former glory; those with a payoff far in the future and those with inept management will not.

- I offer no such list of *companies* in what follows. I provide something better.

Something better? Yes. Rather than tout some particular company, I offer a discussion of the 6 essential elements that are currently necessary to create the power source for a Battery Energy Storage System ("BESS") as well as for battery electric vehicles ("BEVs").

I will provide, in follow-on articles over the next few days, my favorites in each area. I believe the shortages of these key elements and the increasing demands of both grid and transportation electrification will provide wonderful profit opportunities for those who choose wisely. For those who prefer a one-stop investing choice that gathers all of these, my final article in this series will show my thinking for which exchange-traded funds ("ETFs") are best.

For now, let me introduce you to my friends The CCLANGs:

C obalt

C opper

L ithium

A luminum

N ickel, and

G raphite

These are the elements that, thus far, have proven to be the most efficient to provide what a battery needs to do, which is basically to convert chemical energy into stored electrical energy. Whether this electrical storage vessel we call a “battery” is for a massive BESS that is able to store electricity at the community or regional level or that little teeny-tiny battery in your smartphone, the idea is the same.

This type of energy storage is not a new idea. The first battery was developed 223 years ago. In 1799, the Italian chemist Alessandro Volta took two metal plates, one made of copper and one of zinc and placed a piece of salt water-soaked cardboard in between them, creating electricity. (Hence the words volt, voltage, voltaic, overvoltage, photovoltaic, etc.) This was an amazing invention. It was, I believe, the first human-made apparatus to provide a source of electricity and it led to the later discovery of electromagnetism and so much more.

The battery’s basic structure hasn’t changed since Volta’s invention. A battery, any battery invented this far, has two electrodes (the anode and the cathode) dipped in a conductive solution (the electrolyte) with a separator that controls the flow of the electric charge back and forth. One direction discharges, the other recharges.

The current “leader of the pack” is the Lithium-ion battery (Li-ion or LIB) used in most EVs and BESS systems today. However, there is extensive research being done in universities and private companies to provide even safer, cheaper and more efficient batteries. Our current technology is not the end-point of battery development! It is merely an iterative stage leading from Signor Volta’s discovery to whatever the next generation battery will be.

The Li-ion battery is the one you care about as an investor today. If you own the companies or funds that provide the essential resources for Li-ion batteries, you can profit from the ever-increasing demand for them.

Did you know that Exxon invented lithium-ion batteries?

It’s true. In the early ‘70s, the big fear was that oil was about to run out. Without today’s 4-D imaging, seismic technology, and hydraulic fracturing, oil companies were bringing in more and more expensive dry holes. Then came the 1973 Arab-Israeli war and the OPEC oil embargo on the U.S. and others that supported Israel. Rather than wither on the vine, the well-capitalized oil companies began to research new energy sources like nuclear, solar, synthetic fuels, electric motors, and rechargeable batteries.

One of those researchers was an Exxon (XOM) chemist named Stanley Whittingham (who belatedly won the Nobel Prize for Chemistry in 2019.) He and his team built the first rechargeable lithium-ion battery. Its cathode was titanium sulfide and the anode was lithium metal. Exxon began scaling up the project shortly thereafter. But the 1979 Iranian revolution and the following recession forced Exxon to cut its research budget. The company never released a commercially viable battery. Wow. If Exxon had stuck to this and gained various patents, it could be an oil, gas, and battery giant. Not that Exxon is hurting today…

On to investing

Let’s address the following questions and provide the best answer we can for the investing opportunities we are seeking:

Why Lithium-ion?

What materials are needed for a LIB?

Which are likely to see the highest demand versus their current supply? (Greater demand than supply = increase in price).

Which companies are most likely to benefit?

Why Lithium-ion?

Lithium-ion batteries are rechargeable and can be recharged safely and for a few thousand times.

Lithium-ion batteries have a low self-discharge rate. Every battery, including your household batteries, will lose their charge when they're not being used. That is why they have expiration dates. Lithium-ion batteries just last longer.

Lithium-ion batteries have a very high energy density -- both a lot of energy per unit volume and a lot of energy per unit mass. This makes them smaller and lighter than most other battery technology.

Another reason we use lithium-ion technology is because the Lithium-ion batteries have a good temperature operating range. Their ideal “preferred” range is about the high 40s to somewhere around 100 or so degrees Fahrenheit. They can handle weather extremes beyond these parameters; it just does not store as much energy when being recharged and could create more internal resistance over time.

Lithium-ion batteries are relatively compact.

What materials are needed for a LIB?

Answering this question is easy. Just remember “CCLANGs” – Cobalt, Copper, Lithium, Aluminum, Nickel and Graphite .

The cathode in an LIB contains different combinations of various materials, some in very small quantities, but the CCLANGs are there in rather greater quantity. These include, among others, for the cathode, lithium iron phosphate, lithium nickel manganese cobalt oxide, and lithium cobalt oxide. The current collector within is usually a special type of aluminum foil. The anode is usually battery-grade graphite or other soft carbons, with its current collector being copper foil. Copper and aluminum are also used in numerous applications to enhance connectivity, reduce weight and, perhaps surprisingly, be combined with other chemicals and metals to perhaps create even lighter, safer, and faster rechargeability going forward.

In short, Li-ion batteries are composed of lithium, nickel, cobalt, copper, and graphite, with aluminum also a wild card for the next-level battery. It is also, of course, renowned for its strength and weight versus steel for auto chassis and auto body, as well as auto battery, applications. The lighter the weight, the longer the range between charges.

Which of these are likely to see the highest demand versus their current supply?

Ay, there’s the rub:

Quite possibly, every one of them. It isn’t that the materials needed are disappearing from the face of the earth. It is, instead, that miners are having to travel farther, dig deeper, use more expensive methodologies and, in some cases, deal with autocratic or kleptocratic regimes.

Some people envy certain other nations for having gained the march on the rest of the world in gaining control of these essential resources. If you are willing to force children as young as 10 or 11 to do the dangerous and backbreaking work in a toxic environment, you too can get these materials more easily. Our first material, cobalt, is a prime example of this.

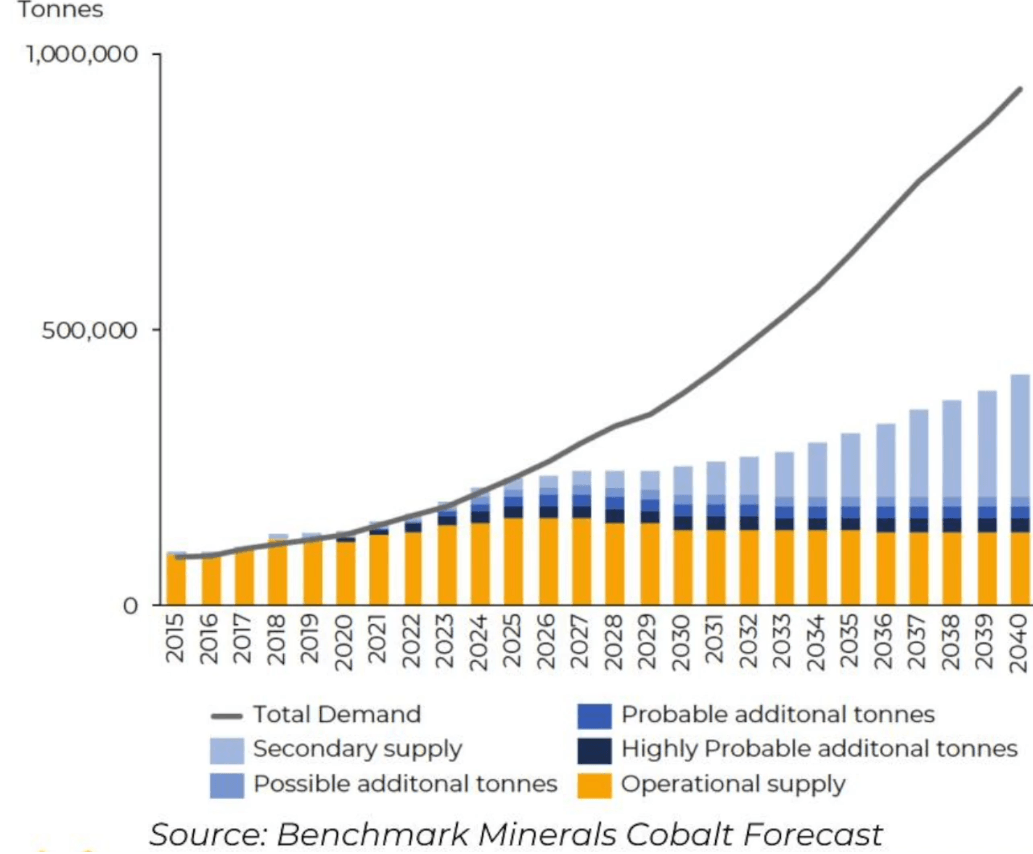

Cobalt

The biggest source of raw cobalt, with 120,000 tonnes (metric tons) of cobalt produced in 2021, is the Democratic Republic of Congo. More than 70% of the world’s cobalt comes from that nation. No other place in the world supplies even 10% of that amount.

USGS (United States Geological Survey)

{kind=link}

Compare the production above with the demand curve below from Benchmark Minerals Intelligence:

Benchmark Minerals Intelligence

{kind=link}

Benchmark Minerals’ highly-respected research team predicts 2023 and 2024 to be the last year of supply and demand equilibrium *if* all sources of secondary supply, "probable additional tonnes" (metric tons,) "highly probable additional tonnes" and "possible additional tonnes" all come to fruition! The odds of that happening are not good. 2023 seems to me to be the ideal time to buy this material. Depressed prices for securities and good odds of a supply/demand imbalance create a perfect storm.

Copper

Copper is the third most-used metal in the world, after only iron and aluminum. Building construction is the single largest market for copper, followed by electronics and electronic products, transportation, industrial machinery, and consumer and general products – with new demand from electric vehicles and energy storage systems growing by leaps and bounds. According to the Copper Development Association, a typical internal combustion car of today has around 20 to 50 pounds of copper in it. Battery electric cars have about 180 pounds of copper. As the famed auto analyst Bob Dylan wrote, “You Don't Need A Weatherman To Know Which Way The Wind Blows.”

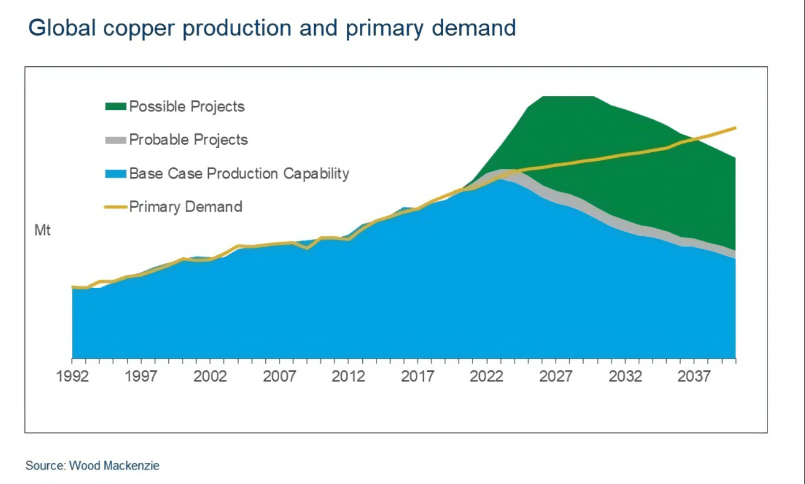

In addition, copper is used in virtually every green project . Whether in solar photovoltaic panels, wind power generation or EV production, copper usage will be increasing. Chile is the world’s largest copper producer, followed by Peru. Many mines in both countries, however, are Chinese owned and operated. Here is Wood Mackenzie’s forecast for the supply/demand situation:

{kind=link}

I again draw your attention to that point at which demand outstrips supply, at least at the “probable projects” level of production. (The green above is all “possible projects.”) Any uptick in demand from housing, other construction projects, or wind and solar will likely mean a deficit. Again, this is predicted to occur in 2023.

Lithium

The whole world is turning up the burners to find lithium. I have written often about lithium, some of which is available on Seeking Alpha by searching under my name. I will provide greater detail when I write exclusively about the metal in this series of new articles. According to the US Geological Survey, Australia produced the most lithium in 2021. The problem with such statistics is that they do not show the ownership of mines, just the region where the mines are located. Chile has the world’s largest reserves, complemented by the other nations in the “lithium triangle,” which includes Argentina and Bolivia as well.

This does not mean that the production is owned by, or the primary profits made by, local companies. Again, China has bought large chunks of these markets. (China also dominates Li-ion battery production, producing about *two-thirds* of the world’s Lithium-ion batteries.) They have huge control over the raw resources from both foreign and domestic entities, as well as having all the manufacturing that is required to make lithium-ion batteries.

Much more investment in new lithium projects will be required to keep up with demand. Existing operational supply is in place to meet demand in 2022. After this year, not likely.

Benchmark Minerals

The same dynamic is in evidence here. From 2023 forward, we are likely looking at depending on – hoping that – probable and possible supply will all come on board.

I seriously doubt it. I live a couple hours down the mountain from Lithium Americas’ site at Thacker Pass. I have watched first-hand the tacky performance by allegedly aggrieved parties that prevented mining there --since placated by various types of legal pay offs to those parties. I have also closely followed the slew of lawsuits brought by various environmental groups. I donate to some of these every year because I care about conservation in their other dealings, but in this they have brought great shame upon themselves.

Has anyone else noticed that it is the exact same people who are demanding the end to all fossil fuels in favor of electric who then demand that there be no mining for the essential materials absolutely necessary to be able to go electric? Electricity, at least in the quantity needed, does not come from flying a kite with a metal key attached to it, nor from rubbing two balloons together. Lithium, too, will see shorter supply than demand, especially in litigious America.

Aluminum

Or, as the British today and my Irish grandmother used to call it, "aluminium." Aluminum is the most abundant metallic element In the Earth's crust. It is also the third most abundant of all elements (after only oxygen and silicon.) There is no way aluminum could have a supply deficit, right?

Wrong. First, because much of that aluminum is not easy to get to economically. Second, because almost all metallic aluminum is produced from bauxite, to which it is bound. This requires mining and manufacturing to separate the two. Third, we are using more of this metal than ever before. And fourth, aluminum is almost always alloyed with other metals like copper, zinc, silicon, magnesium and others, which adds yet another step.

At last we find a Lithium-ion battery material that is not in as dire supply/demand straits as the others:

{kind=link}

As long as the predicted “probable projects” are funded and built there should be no violent upward price movement. Except that other uses of aluminum are climbing more rapidly than originally predicted.

Using aluminum rather than steel in at least some vehicle components reduces weight markedly, while providing greater survivability in crash scenarios much more likely. The fiberglass and plastic going into many cars today, whether ICE or BEV, cannot say that.

There are just two cars in my family. The one nearly as old as me has a steel body but an aluminum hood and trunk. This makes for greater speed and better gas mileage. (Since I noted the difference in the British spelling of aluminium, as a courtesy I should also note that this is a British car. Substitute hood and trunk with bonnet and boot and we are now speaking a common language. Of sorts.)

We still need to produce considerably more aluminum than we do now for automobiles, trucks, railway cars, airplanes, ships, cans, foil, building and construction, roofing, wire, conductors, motors, cooking utensils, pipes, machinery, tools and more. There is also a possible challenger to Li-ion batteries using aluminum and air. There might be some exciting news on the horizon. If this proves out, it will upend a lot of current thinking and make aluminum even more in demand. For this reason, aluminum will be my next article in this series.

Nickel

Unlike aluminum’s good news, nickel is a potential train wreck. The likelihood of too few new projects highlight a probable gap in global Nickel production to meet the necessary BEV ramp-up. The projected deficits you see below are alarming. Nickel is too important to the LIB to take it for granted. If we do not see more production, we will see a serious increase in the price of these batteries.

{kind=link}

It has happened that nickel demand slowed temporarily this year (as differentiated from the Wood Mackenzie forecast above.) With luck, this will result in miners and producers taking the time when plants are not running full-out to consider future demand and do their CapEx now. If Wood Mackenzie is right, the projects planned for 2023 (there is that critical date again) and beyond are on the decline – precisely at the time that demand is rising. This should mean that positions taken in major nickel companies will see rising prices, greater revenue and higher earnings.

Graphite

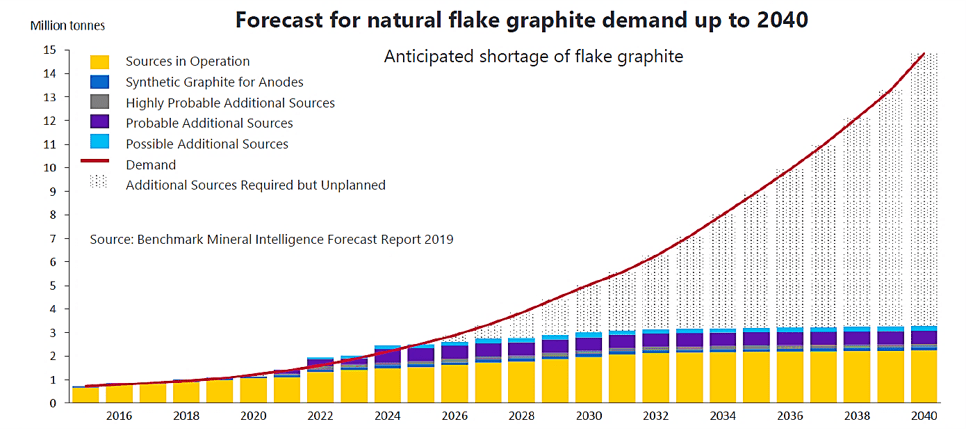

Graphite is the prime element used as the anode material for Li-ion batteries. That is a big load to carry. Regrettably, the USA is running late to make certain this country has enough of this essential material. China is the biggest producer, followed by India and Brazil. The BIC countries.

Graphite has been used in batteries for quite q while now, and not just for BESS and EV usage. My electric drill, CD player, laptop, smartphone and tablet all have graphite as one of their materials for their internal batteries.

Graphite demand rose as we discovered the dangers of asbestos. Graphite become the replacement of choice for heavy duty brake linings and brake shoes. However, nowadays there are other synthetic substances that do just as well. Graphite lubricants are popular, as are graphite pencils (beginning in the 1500s.) Right now I am reminded there is graphite in the headphones I have on to soothe the savage beast I become when I have been writing too long!

Here is what the future supply/demand matrix looks like for graphite. It is a familiar sight. Looking at this, I believe that 2023-2024 is an ideal time to begin to accumulate graphite companies.

{kind=link}

This has been your introduction to the CCLANGs. Perhaps you do not agree with all, just as you may not have bought all the FAANGs. Six materials discussed, to be followed by six daily follow-on articles. I leave you with some of the bigger publicly listed companies and ETFs for the CCLANGs.

None may be construed as recommendations. In each of my next six articles, I will delve into what I believe are the best ways to buy into the CCLANG future. Some I already own, others I might buy as I do deeper research. In each case I will narrow the field to one or at most two companies that I can suggest for your own due diligence.

Until then, here are just some of the big companies you might want to review in this arena: BHP Group ( BHP ), Rio Tinto ( RIO ), Glencore ( GLNCY ), Teck Resources ( TECK ), Albemarle ( ALB ), Livent ( LTHM ), Lithium Americas ( LAC ), SQM ( SQM ), Freeport-McMoRan (FCX), and Vale ( VALE ).

I will write an article each day for the first six days of the “real” 12 days of Christmas – Dec 26 until Dec 31. Until then, I wish all a Merry Christmas, Happy Hanukkah, Dhanu Sankranti, or any other blessing for a quiet time the next couple weeks and a not-so-fond adieu to this year in the market!

Great investing,

Author

For further details see:

Bitten By The FAANGs? Try My CCLANGs Instead!