BJRI - BJ's Restaurants: Decent Rebound Growth Story But Overvalued

2023-05-03 11:48:35 ET

Summary

- BJRI hit an all-time high revenue in 2022, but profitability hasn't returned to pre-pandemic levels.

- This is a decent growth story for the next few years as the industry rebounds.

- The price is simply too high on a multiples and intrinsic basis for this much growth.

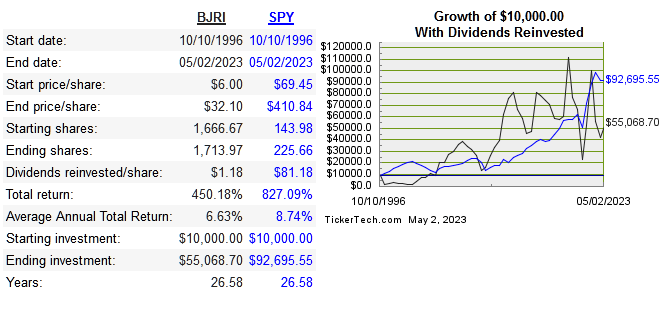

BJ's Restaurants ( BJRI ) has been publicly traded since the early 80’s, and operates 216 casual dining restaurants in 30 states. All locations are corporate owned. Below is the long term share price performance:

{kind=link}

dividend channel

The company hit an all-time high in revenue of $1.2 billion in fiscal 2022, but margins haven't yet returned to previous levels. Below are the return on capital metrics:

| Company |

| Revenue 10-Year CAGR |

| Median 10-Year ROE |

| Median 10-Year ROIC |

| EPS 10-Year CAGR |

| FCF/Share 10-Year CAGR |

| BJRI |

| 6.1% |

| 10.5% |

| 6.9% |

| -17% |

| n/a |

| 3% |

| -27.2% |

| 16.9% |

| 3.3% |

| -8.2% |

| 5% |

| 32.7% |

| 14.4% |

| 5.9% |

| -4.1% |

| 2.7% |

| 0.8% |

| 0.4% |

| n/a |

| n/a |

| 1% |

| 50.2% |

| 7.1% |

| 8.9% |

| 5.4% |

| 0.7% |

| -8.8% |

| 5.9% |

| -2.9% |

| -6.1% |

Capital Allocation

BJRI paid dividends from 2017-2020 and suspended them due to the lock downs. They had a somewhat consistent history of making repurchases, but the pandemic led them to raising funds via dilution, offsetting the previous reduction of share count. Below we take a look at how cash flow was used:

| Year |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Operating Income |

| 24 |

| 35 |

| 63 |

| 65 |

| 62 |

| 38 |

| 49 |

| -86 |

| -17 |

| 1 |

| FCF |

| -22 |

| 12 |

| 41 |

| 29 |

| 26 |

| 34 |

| -3 |

| 22 |

| -27 |

| Dividends |

| 2 |

| 10 |

| Repurchases |

| 100 |

| 96 |

| 95 |

| 67 |

| 83 |

| 15 |

| 2.3 |

| Debt Repayment |

| 67 |

| 487 |

| 1,132 |

| 2,130 |

| 996 |

| 1,279 |

| 1,123 |

| 700 |

It will be worth watching to see if the dividend is reinstated as cash flows normalize.

Risk

There is no major risk in this story other than the cyclical nature of the company, which leads to price risk, which we will get into shortly. There is still a decent runway of expansion in spite of not having the highest returns versus peers. In 2013 they had 130 restaurants in 13 states, which is now 216 locations in 30 states.

Long term debt is current at $493 mil, but I’m not worried right now due to FCF normalizing over time. They've also shown the ability to deleverage quickly when needed.

The biggest risk would be ignoring the foundational fact that this is a cyclical business, and not suitable as a long term buy and hold stock.

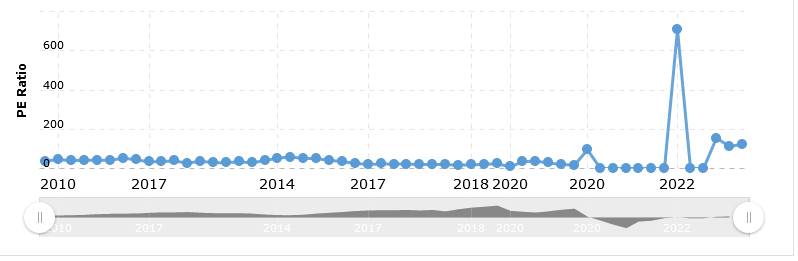

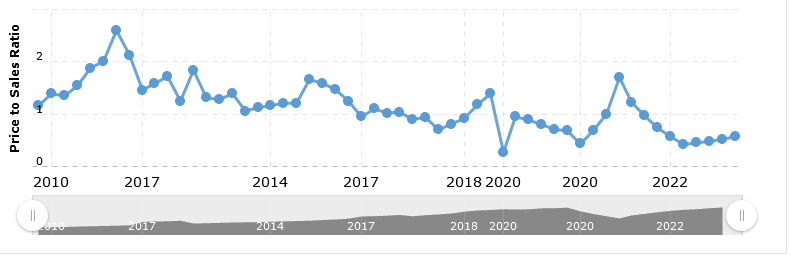

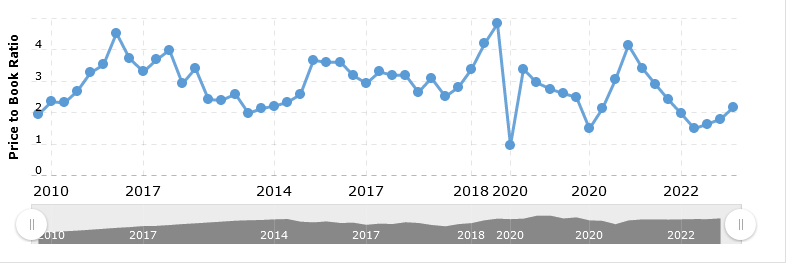

Valuation

This is a decent growth story, due to the rebounding of the industry post- Covid . The price to pay for decent growth is another issue though. I'm alright with a slower growth story if the price is very cheap, but that's not quite the case here. Below are the multiples vs peers:

| Company |

| EV/Sales |

| EV/EBITDA |

| EV/FCF |

| P/B |

| Div Yield |

| BJRI |

| 0.6 |

| 11.2 |

| -28.9 |

| 2.2 |

| n/a |

| EAT |

| 0.7 |

| 8.8 |

| 65.9 |

| -6.6 |

| n/a |

| RUTH |

| 1.1 |

| 7.2 |

| 26.8 |

| 4 |

| 3.9% |

| RRGB |

| 0.3 |

| 6.2 |

| 60.8 |

| 38.7 |

| n/a |

| BLMN |

| 0.7 |

| 5.7 |

| 16.8 |

| 7.9 |

| 3.8% |

| DIN |

| 2.2 |

| 9.2 |

| 27.8 |

| -3.3 |

| 3.2% |

Next are the historical multiples:

{kind=link}

macrotrends

{kind=link}

macrotrends

{kind=link}

macrotrends

Below is the DCF model, assuming EPS grows to pre-pandemic levels over five years:

money chimp

So on a pricing basis, the multiples don’t indicate much of a discount, and on an intrinsic basis I definitely see the stock being overvalued today. Last July would have been the optimal time to buy at around $21/share. I also can't ignore the fact that cyclicality inherently makes the DCF less useful. Expect moderate growth fundamentally, but low returns if buying at today's share price.

Conclusion

In spite of a very cyclical run as a publicly traded company, BJRI is a decent business with a likewise decent growth path ahead of it for the next few years. There isn’t much danger from a fundamental business perspective, so paying too much would be the biggest potential risk an investor faces.

On that front however, the price is too high, even assuming EPS normalizes to pre-pandemic levels. I think it will be worth paying attention to a potential reinstatement of the dividend, and this could be a better chance to get in assuming a lower share price around the time of this event. There is just nothing special about this enterprise that makes it okay to pay such a high price today.

For further details see:

BJ's Restaurants: Decent Rebound Growth Story, But Overvalued