BJRI - BJ's Restaurants: Limited Margin Of Safety At Current Levels

2023-12-17 20:38:09 ET

Summary

- BJ's Restaurants had a mixed Q3 with softer sales, offset by improved margins and outperformance on cost savings initiatives.

- Unfortunately, the restaurant industry faces a challenging 2024, with some consumers appearing tapped out and sticky wage inflation exacerbated by AB 1228.

- In this update, we'll look at BJ's updated valuation, its recent Q3 results, and whether this rally in the stock is worth chasing after a strong recovery from October.

The Q3 earnings season for the restaurant industry saw mixed results overall, with weak quarters from several casual dining brands like Applebee's ( DIN ), Cracker Barrel ( CBRL ), and Bloomin' Brands ( BLMN ), offset by strong quarters from Restaurant Brands International ( QSR ), Chipotle ( CMG ), and Wingstop ( WING ). Fortunately, BJ's Restaurants ( BJRI ) was one of the better-performing names in the casual dining space during Q3 despite sluggish industry-wide traffic, outperforming its peer group according to Black Box data, and continuing to see solid results from its 2023 class restaurants where sales and margins are well above its system average. In this update, we'll look at BJ's updated valuation, its recent Q3 results, and whether this rally in the stock is worth chasing after a strong recovery from its October lows.

{kind=link}

Q3 Results

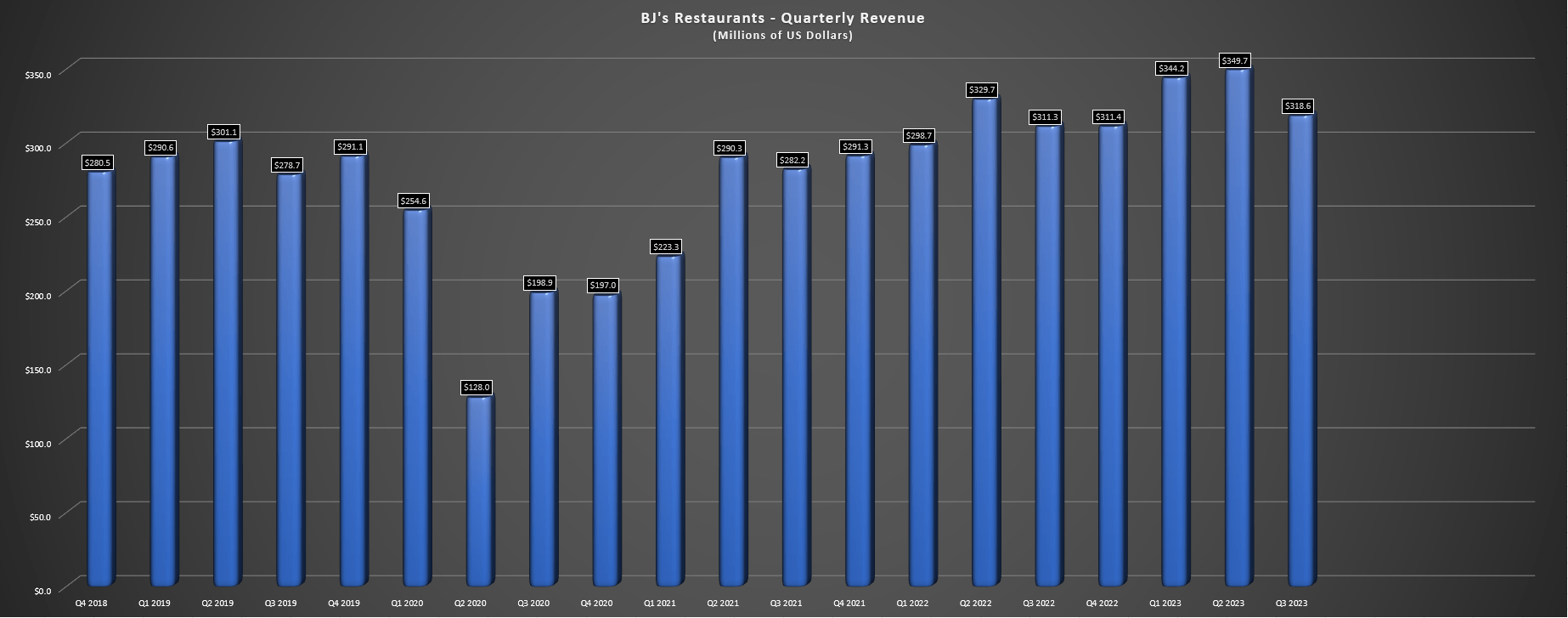

BJ's Restaurants ("BJ's") Q3 results came in softer than I expected, with quarterly revenue of $318.6 million (+2% year-over-year), comp sales of 0.4%, and two-year stacked comp sales growth of 9.3%. And while these sales results might look decent at first glance, new restaurant openings helped revenue while comp sales benefited from roughly 7% effective pricing in Q3. This implies continued traffic declines, although the company beat its peers for the 10th consecutive according to Black Box Intelligence data on a comp sales basis. On a positive note, comp sales improved in October after worsening throughout Q3, and while this was helped by a menu price increase in September (pricing just shy of 8% currently), the improvement in comp sales is a positive development even if up against easy comparisons from a rough September (negative low single digits according to the company).

BJ's Restaurants Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

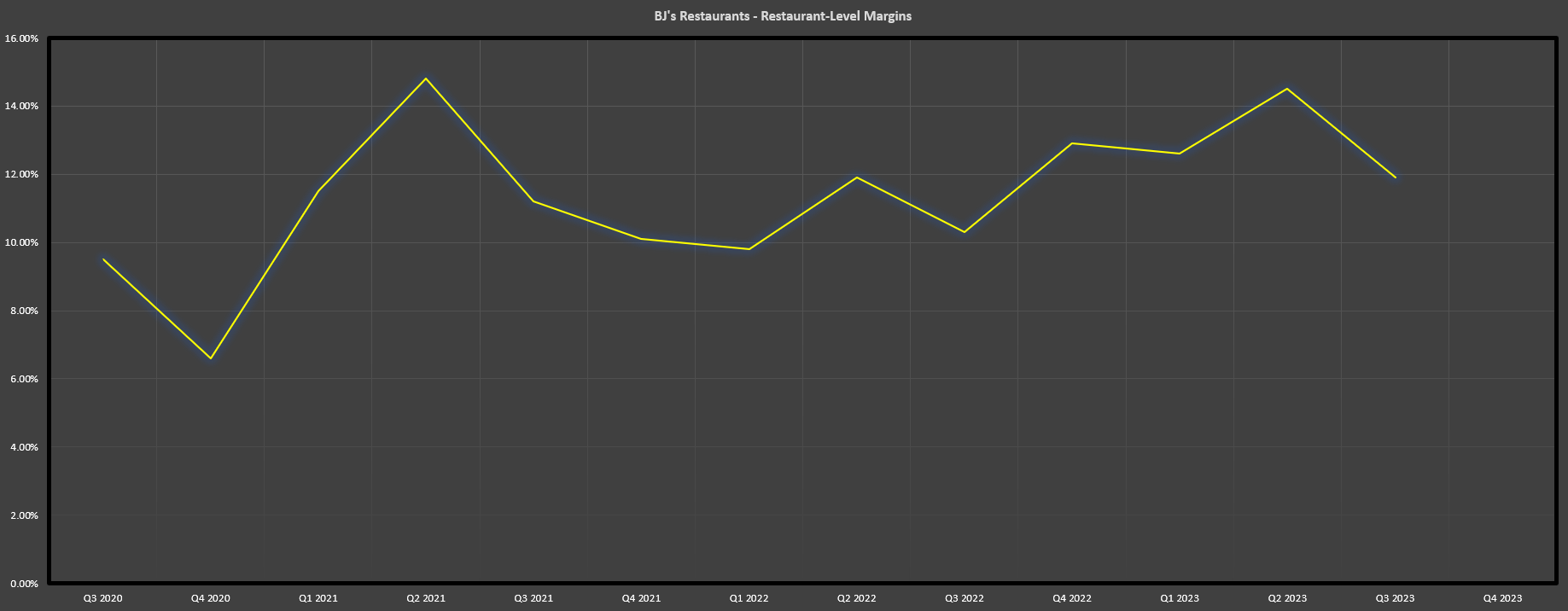

Fortunately, while sales were lower and the company has closed five restaurants over the past year (including another underperforming restaurant in Q3), margins did improve meaningfully. In fact, restaurant-level margins increased 160 basis points to 11.9%, helped by lower cost of goods sold (25.9% vs. 27.3%) and lower labor costs (37.1% vs. 37.7%), offset by a slight increase in occupancy/other costs. BJ's noted that the lower cost of goods sold was attributed to lower commodity costs and cost-savings initiatives as well as the benefit of menu price increases, while labor costs benefited from labor efficiencies (including less kitchen prep hours), offset by wage inflation. Finally, the company noted that its class of 2023 restaurants is enjoying mid- to upper-teen margins and that its remodels are translating to improve traffic.

BJ's Restaurants - Restaurant-Level Margins - Company Filings, Author's Chart

{kind=link}

As for the company's financial results, adjusted EBITDA came in at $19.6 million (Q3 2022: $15.2 million), but the company still reported a net loss of $3.8 million in the period. And while annual earnings per share are expected to improve year-over-year to $0.75 - $0.80 vs. $0.08, annual EPS is still well below pre-pandemic levels and will remain below these levels in FY2024 even with continued earnings growth. Hence, while there is room to grow overall margins/earnings as new restaurants that are outperforming and remodels pull up system averages, it's still a long road to returning to pre-pandemic margins across the system (FY2018: ~17.5% margins).

Recent Developments & Industry-Wide Trends

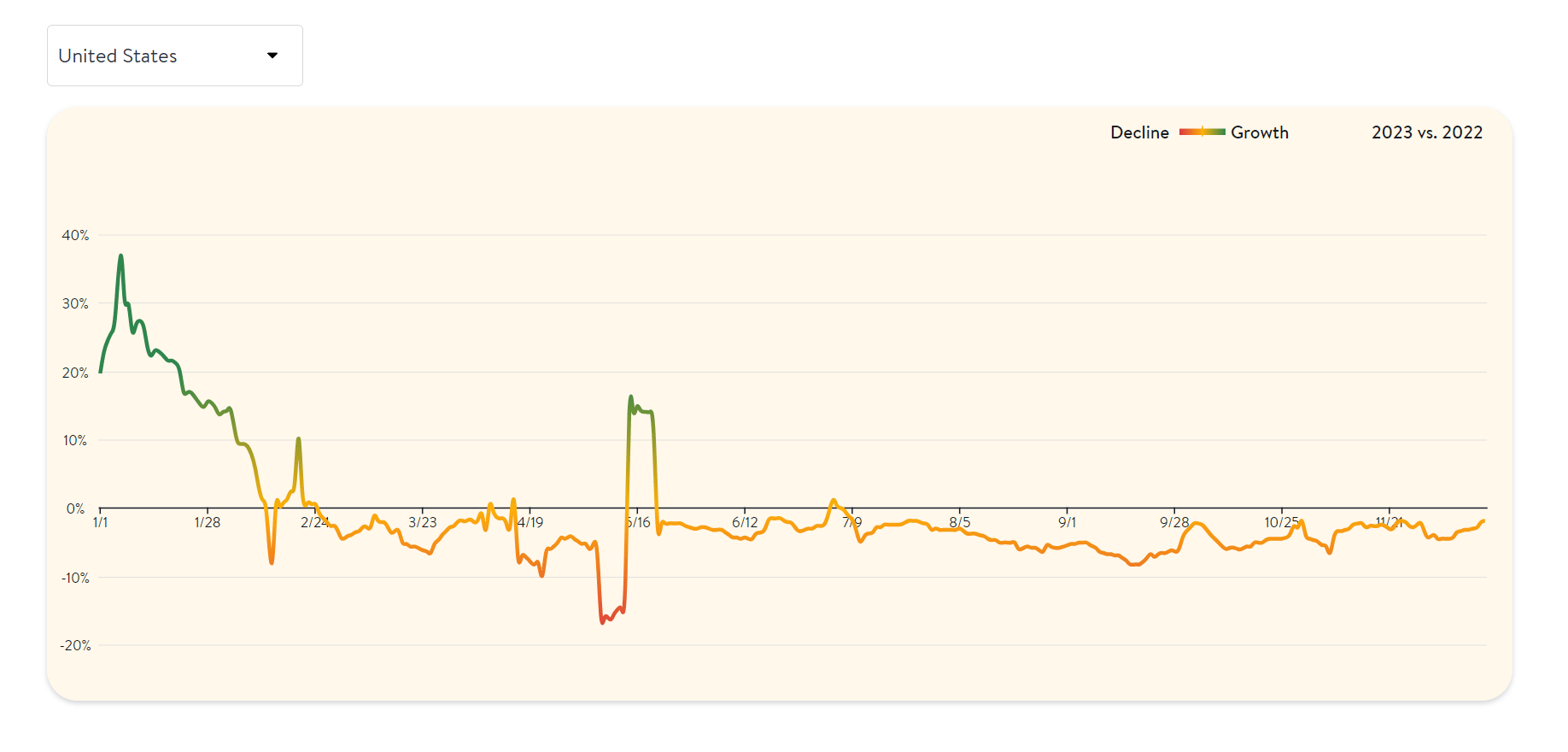

Looking at recent developments and industry-wide traffic, industry-wide traffic continues to be an issue, with traffic growth remaining negative for six consecutive months with no spikes back into positive territory. This is a significant change of character from February through June (once past the easy Omicron comps) when the trend was lower but there were brief periods of seated diners growth, suggesting that some consumers may finally be seeing the pinch and cutting dine-out occasions entirely at full-service restaurants or reducing their frequency.

{kind=link}

Obviously, this data doesn't correlate perfectly with fast-casual and quick-service brands, but we are seeing similar trends across all concepts. In fact, quick-service has seen four consecutive months of declining traffic (a clear change of character with it previously growing due to trading down), casual dining continues to be negative even if BJ's has outperformed its peer group, and we're seeing lower traffic for fine-dining, suggesting that even some more affluent consumers might be pulling back a little and/or trading down. However, with non-existent traffic growth across casual dining, quick-service, and fine-dining, the data would suggest that less consumers are dining out or frequency has been reduced even if there are the odd winners like First Watch ( FWRG ) with improving dining room traffic.

{kind=link}

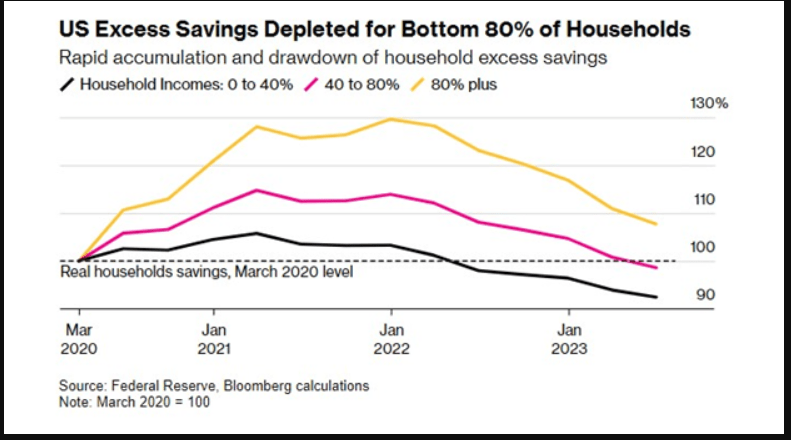

While these results are disappointing on their own and the trend in traffic is clearly not ideal, the alarming statistic is that this choppy and negative traffic in quick-service and full-service restaurants is despite persistently lower gas prices. The reason that this is discouraging is that lower gas prices are often a tailwind as it reduces pressure on consumers' wallets, but this hasn't led to much improvement in industry-wide traffic as it did last year. In summary, it's tough to be overly optimistic about industry-wide traffic heading into 2024, and while menu price increases cooled year-over-year after many high single-digit increases in 2022, more price increases are expected in the upcoming year and it's difficult to know how this might impact guest satisfaction and consumer behavior as average checks are considerably high vs. 2020 levels and savings has gone from excess due to lockdowns to depleted for many consumers.

The second negative worth discussing is that minimum wages are set to increase to $20.00 per hour for fast food restaurants in California as of April 1st, 2024, a negative development from a wage inflation standpoint for BJ's which has ~27% of its total restaurants in the state. Fortunately, the company still has a significant portion of restaurants that will avoid this impact and most of its California employees are already above $20.00/hour with tips, suggesting less impact for BJ's from a need to take pricing and wage inflation standpoint than its quick-service peers at much lower wage rates. Still, this will pressure wages regardless, with the company noting that "labor inflation could tick up to the mid to upper single digits given the added impact of AB 1228, and we do expect some impact " .

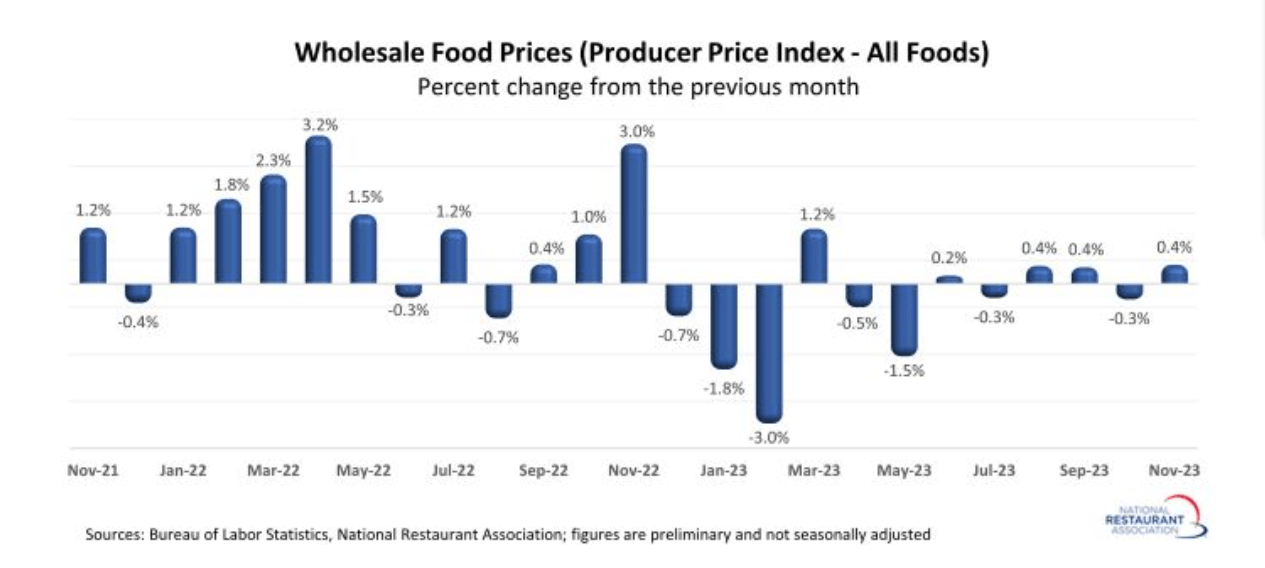

Lastly, the company is not getting much help from a beef standpoint even if it benefited from a cooling of commodity prices and a smaller menu that benefits margins in Q3. This is evidenced by beef/veal prices which were up ~26% in November, significantly above the wholesale food price average which has continued to hover at much lower inflation levels vs. last year, with deflation in many commodities. Hence, while BJ's cost-savings initiatives are helping to mitigate wage inflation and inflation in some commodities, 2024 could be a tougher year from a margin standpoint with the impact of AB 1228, beef prices remaining elevated, and with the company potentially having to be more careful with the magnitude of menu price increases given the delicate environment (low consumer confidence and depleted savings for many consumers).

Wholesale Food Prices - National Restaurant Association, BLS Excess Savings Bottom 80% Of Households - Federal Reserve, Bloomberg, DiversifiedTrust.com

{kind=link}

{kind=link}

As for positive developments, BJ's took advantage of share price weakness to repurchase ~164,000 shares in the quarter at an average price of ~$26.20, reducing its share count by nearly 0.70%. Second, the company noted that it expects to open 4 to 6 new restaurants for its 2024 class, with most under the new prototype with savings of ~$1 million on build costs and better returns on investment. Third, the company's cost-saving initiatives continue to exceed expectations, with $25 million in annual cost savings achieved in Q2, and the company noting that $30 million looks achievable. Last, BJ's is in a better position from a labor standpoint, with hourly team member retention in September back to pre-pandemic levels. And while labor inflation will still be high because of AB 1228, guest satisfaction and speed of service should remain positive with a more experienced roster.

Overall, the negatives arguably outweigh the positives, with the industry in a difficult position. This is because while the industry is working to improve margins after a difficult two years, it's not clear how much room is left to increase pricing before consumers drop the frequency of visits or we see check management. And while BJ's hasn't seen signs of this to date, 2024 could be the year that this changes with excess savings depleted, consumer confidence still relatively low, and a clear trend in change of character from a traffic standpoint, with nearly all concepts seeing lower traffic the past few months, and this even showing up among more affluent consumers. So, while it's positive to see BJ's improving margins with cost-savings, it's difficult to be optimistic about industry-wide sales going into 2024 against an outlook of continued price increases, especially for California restaurants because of the impact of AB 1228.

"So no shifts in those types of metrics that would signal some type of check management or the consumer pulling back."

- BJ's Restaurants, Q3 2023 Conference Call

Valuation

Based on ~23.0 million shares and a share price of $33.20, BJ's trades at a market cap of ~$760 million and an enterprise value of ~$1.26 billion, leaving it trading at ~10.5x FY2024 EV/EBITDA estimates. This is a slight discount to the company's 10-year average forward EV/EBITDA multiple pre-pandemic of ~11.0x, and just below its 5-year average EV/EBITDA multiple of ~13.0x. Meanwhile, BJ's trades at ~25.0x FY2024 earnings estimates of $1.33, a rich multiple for a relatively low-margin and low-growth casual dining name, at least relative to higher-growth franchisors with more iconic brands like Restaurant Brands International at ~21.0x FY2024 earnings estimates. Hence, it's hard to argue that the stock is cheap here after its recent rally.

{kind=link}

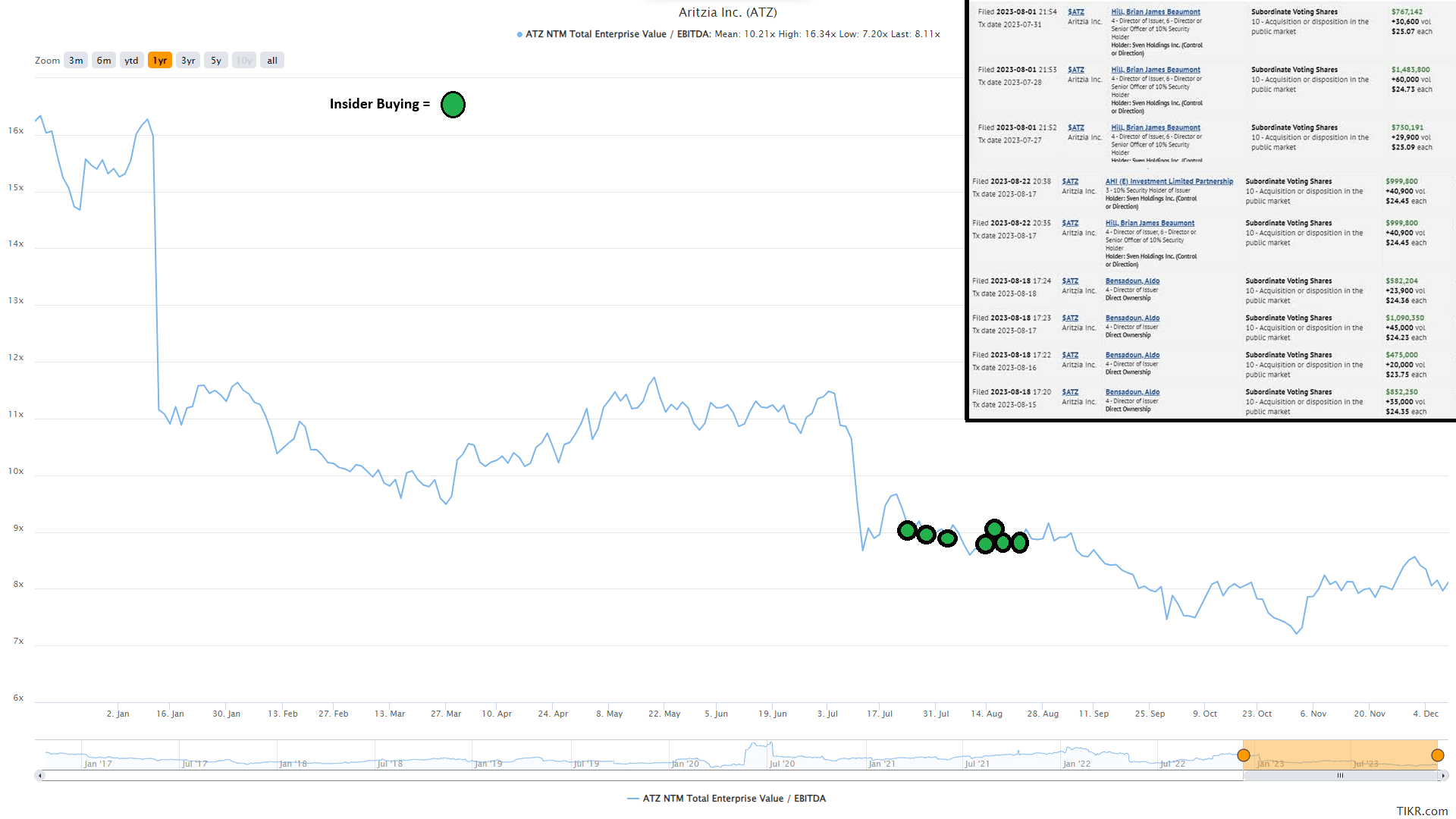

Using what I believe to be a more conservative multiple of 11.0x forward EV/EBITDA (in line with its pre-pandemic average) and ~22.5 million shares, I see a fair value for the stock of $33.80, pointing to a 2% upside from current levels. However, while this suggests a slight upside and the potential for this rally to continue, I am looking for a minimum 30% discount to fair value to justify starting new positions in small-cap names, and especially lower-growth names. After applying this discount to ensure an adequate margin of safety, BJRI's ideal buy zone comes in at $23.70. In summary, I don't see nearly enough of a margin of safety at current levels, and I continue to see far more attractive bets elsewhere in the market. One name that stands out is Aritzia ( ATZ:CA ), which trades at half the FY2024 earnings multiple, has higher unit growth and much higher revenue growth (tripled its sales from FY2018 to FY2023) and has seen significant insider buying.

Aritzia EV/EBITDA Multiple & Recent Insider Buying - TIKR.com, SEDI Insider Filings

{kind=link}

Summary

While BJ's sales were below my expectations in Q3, the company continued to see margin improvement, it shared encouraging stats about its 2023 class of restaurants, and comp sales improved in October (helped by pricing actions in late September). That said, the industry has a tough year ahead, with wage inflation remaining sticky (exacerbated by AB 1228 for California restaurants), and restaurant brands having to be careful with pricing to balance protecting margins vs. potentially pricing some consumers out of casual dining or pushing them to drop frequency/manage checks. And while BJ's new restaurants/remodels are seeing solid sales, its average margins remain quite low, and further softness in traffic/persistently high beef costs could make for a tough 2024 after lapping easier comps in Q3. Hence, if this strength in the stock continues, I would view any rallies above $35.40 before February as an opportunity to book some profits.

For further details see:

BJ's Restaurants: Limited Margin Of Safety At Current Levels