BJRI - BJ's Restaurants: Patience Required

2023-10-08 10:42:14 ET

Summary

- BJRI has underperformed the market and its industry group, sinking 20% and suffering a ~30% drawdown at its recent low since its Q1 highs.

- And while the company's Q2 results were better than expected, it will be difficult to beat estimates in H2-23 due to softness in industry-wide traffic and a more promotional environment.

- In this update, we'll look at industry-wide trends, BJ's progress on clawing back lost margins & whether the stock is offering enough margin of safety after a violent ~65% correction.

Just over eight months ago, I wrote on BJ's Restaurants (BJRI), noting that there was no way to justify paying up for the stock above $31.30 per share. This is because the stock was trading well above its historical earnings multiple into what would be a difficult macro environment, suggesting the potential for sales to moderate as the year progressed after lapping the easy Omicron (January/February 2022) comps. Since then, BJ's has significantly underperformed the market and its industry group, sinking 25% and suffering a ~30% drawdown at its recent low. And while the company put together a better Q2 than I expected given the choppy industry-wide traffic, it will be even more difficult to beat estimates in H2-2023 given the deceleration in industry-wide traffic witnessed in August through September, with this likely to persist into Q4. Let's take a closer look below:

{kind=link}

Recent Results & H2 Outlook

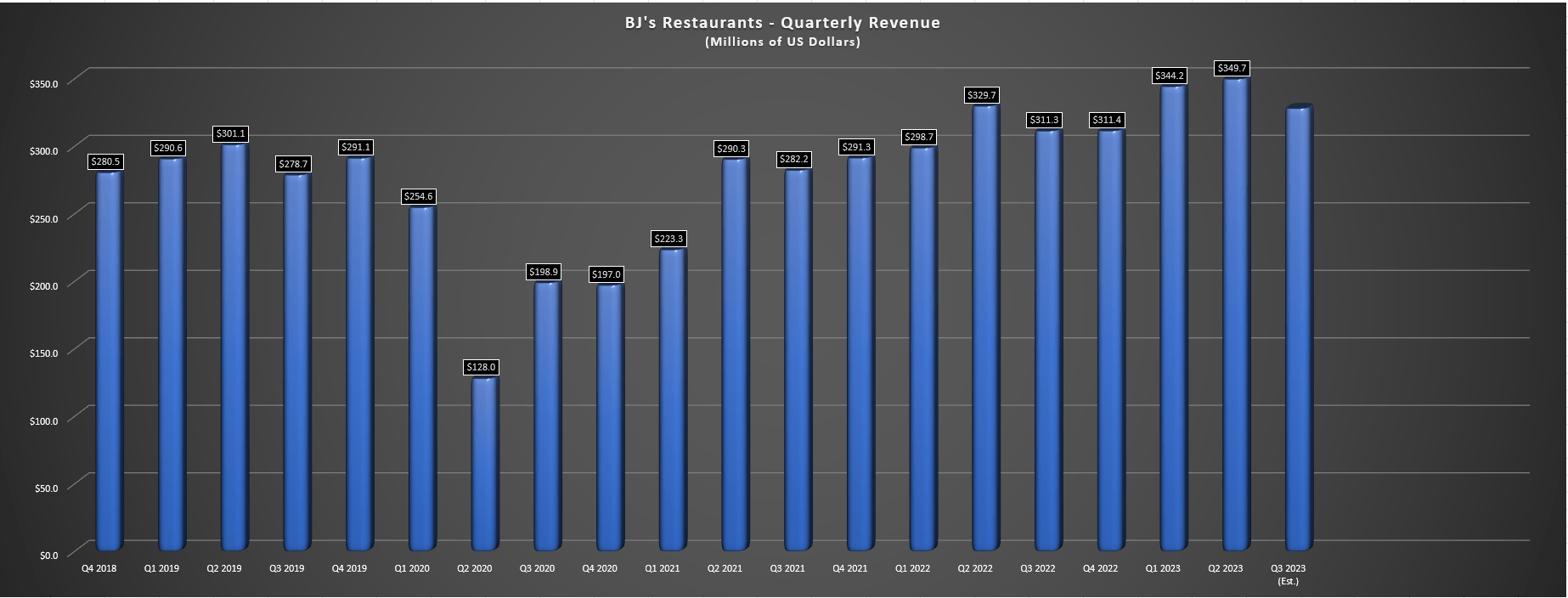

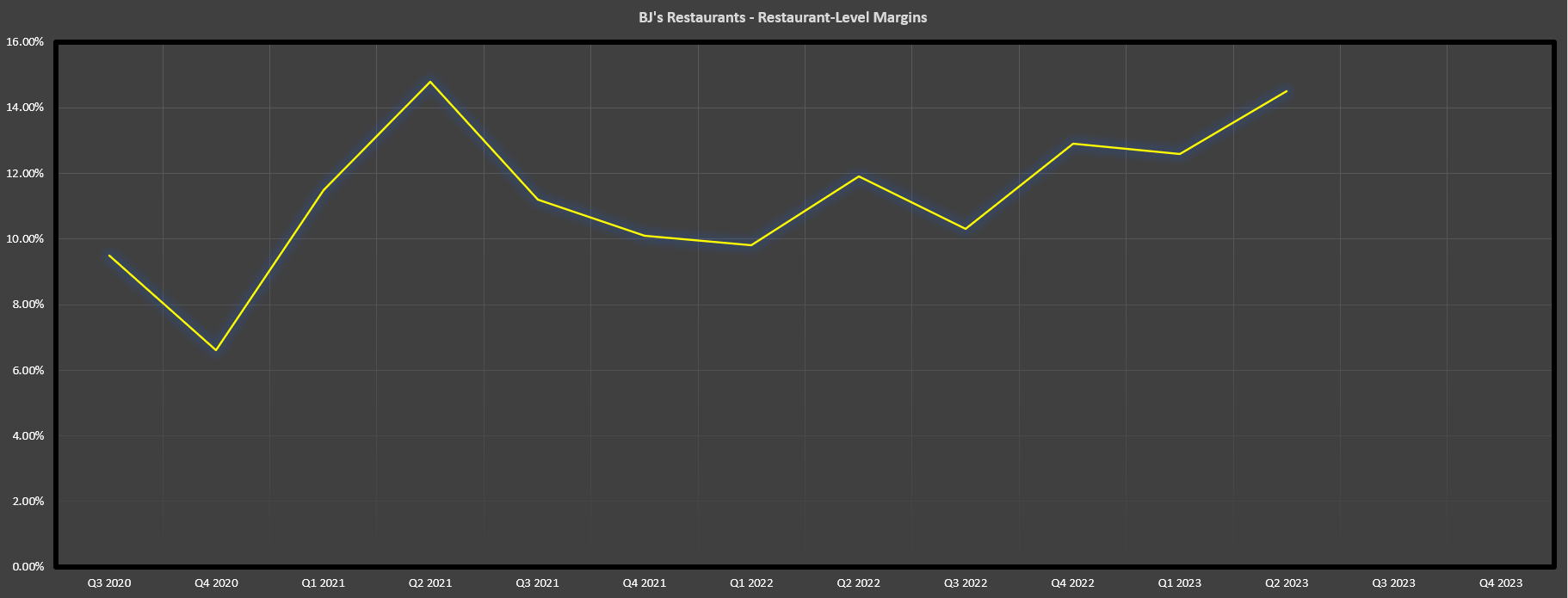

BJ's Restaurant ("BJ's") released its Q2 results in late July, reporting revenue of $349.7 million, a 6% increase from the year-ago period. This was driven by net restaurant growth and 4.7% comparable sales growth, with the company beating the industry according to Black Box Intelligence from a sales/traffic standpoint. Still, while comp sales growth was up, traffic was still down low double digits when factoring in the near 8% pricing in Q2. Meanwhile, although restaurant level margins rebounded to 14.5% and their best levels in two years, they are still well below the 19.0% margins enjoyed pre-COVID-19 with no clear path to clawing back these lost margins. Plus, these margins are despite leaning on price at above historical levels, a lever that may not be as available in what looks to be a more promotional environment with hints of some check management according to Darden ( DRI ), with the largest operator discussing less entrée and alcohol attachment in its Q1-24 results.

BJ's Restaurants - Quarterly Revenue - Company Filings, Author's Chart BJ's Restaurant Level Margins - Company Filings, Author's Chart

{kind=link}

{kind=link}

Looking ahead to Q3, BJ's noted that it would be opening three restaurants of its five planned for the year (~2% unit growth), helping to boost revenue slightly. However, the company guided for just ~$330 million in revenue at the beginning of the quarter with it set to roll off some pricing, which would translate to just ~6% revenue growth if it manages to meet this figure. Given the traffic softness, I would be surprised to see it meet the $330 million estimate for sales and depending on traffic, the company may have to be a little more careful when it comes to pricing for its Q3 price hike given that other brands have called out a more promotional environment and consumers are already strained, evidenced by credit card debt hitting all-time highs in the United States and Canada and consumers continuing to get hit from all angles (gas, mortgage/rent, utilities, grocery) ahead of an expensive holiday season.

On a positive note, though, BJ's has managed to capture $25 million in cost savings to benefit restaurant margins as discussed last year, surpassing this goal in the most recent quarter. It also noted that it believes it has room to realize additional savings, and the company appears encouraged by the impact of its remodels which are helping to drive additional sales with 20%+ ROIs. That said, although cost of sales saw moderate gains year-over-year as a percentage of sales, labor has remained elevated at over 36% (up 80 basis points on a 5-year basis), and occupancy & other expenses (including marketing) was up yet again to 23.6%, up 20 basis points year-over-year and over 300 basis points vs. Q2 2018 levels, offsetting any benefiting from its cost of sales line. So, although BJ's is making progress, returning to high teen margins is proving more difficult than some investors might have hoped.

Industry-Wide Trends

Starting with the positives, we appear to be seeing better turnover rates industry-wide, with Darden ((DRI)) and Denny's ( DENN ) calling out improved turnover rates, and BJ's noting a similar trend, with its restaurant manager retention better than 2019 levels, and hourly team member retention rates trending back towards pre-COVID-19 levels. This will not only provide a benefit from reduced overtimes and hiring bonuses and training costs during periods of higher turnover and labor shortages, but it will also benefit productivity and likely customer satisfaction as well, with more experienced team members and managers able to work more productively and with fewer mistakes to ensure guests are getting a great experience. So, while full-service restaurants may still be one segment that's 4% below pre-COVID-19 levels for staffing levels , there are green shoots at some brands, including BJ's.

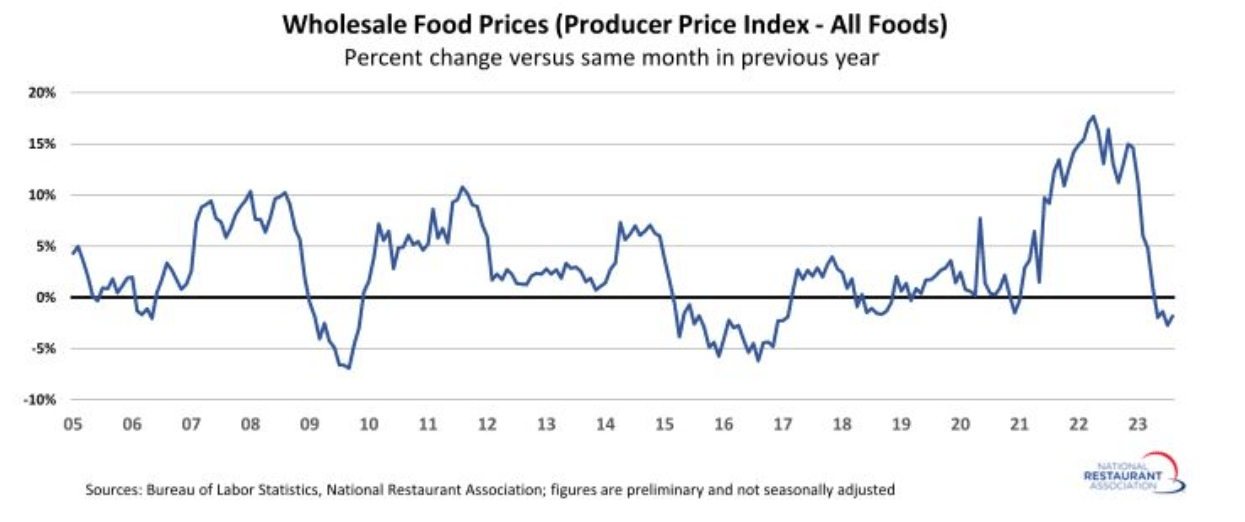

Wholesale Food Prices - National Restaurant Association, BLS

{kind=link}

The second positive worth noting is that the double-digit commodity inflation that wreaked havoc on margins last year has finally dissipated, with many brands noting that they could see minor commodity deflation in the back half of the year or low single-digit inflation. This is another win for the restaurant industry that was having to price at well above historical levels and still struggling to hold the line on margins. That said, the unfortunate offset is that labor costs (which make up a higher portion of overall costs) continue to run at mid-single-digit levels, so even if staffing/retention levels are improving, it's coming at a cost, and especially for those with much of their system in higher wage-rate states like California (28% of total restaurants). So, while the productivity improvements and more normalized commodity environment are positive for margins, I remain skeptical that BJ's can push its margins back into the high-teens (18%+) any time soon with margins in steady decline since FY2016 (19.3%).

{kind=link}

Moving over to the negatives, they may be short term, but they are significant. As shown in the chart above, seated diners in the United States according to OpenTable have continued to trend lower since late July, decelerating throughout Q3 and turning lower once again to start Q4 last week. This suggests that BJ's commentary on its Q3 call that consumer demand was stable throughout Q2 and that "these same trends continued into the first 3 weeks of Q3" may have come just before industry-wide traffic moved into a slump for the rest of the quarter. And given the higher gas prices vs. Q2, which are further pinching already tight wallets combined with what some brands have called out as a more promotional environment, it's difficult to be optimistic about BJ's Q3 and Q4 top-line performance, suggesting we could see a steep drop in margins in the back half of the year.

{kind=link}

For long-term investors interested in BJ's, the slowdown may not seem relevant given that they're focused on the big picture, which is the potential for 300+ restaurants domestically, higher AUVs due to remodels, and a return to 16% plus margins. However, while short-term traffic may not matter to the big picture if the company can execute, it does matter to the share price short-term, and the goal should be to protect against drawdowns when the outlook is foggy, even if one is taking a 30,000 foot view for their investment.

And while a case can be made to disregard the noise if significant negativity is already priced into a stock, I'm not sure this is the case yet for BJ's. This is because while it may be cheap on a trailing ten-year basis compared to historical multiples (an environment dominated by low rates and a significant wealth effect), it's difficult to argue that there's an adequate margin of safety yet when adjusting for the current rate environment, the company's relatively low unit growth, and the reality of pre-COVID-19 margins likely being a distant memory for most restaurant concepts.

Valuation

Based on ~22.6 million shares and a share price of $23.40, BJ's trades at a market cap of ~$530 million and an enterprise value of ~$1.03 billion. This is a significant haircut from the company's more recent peak market cap of ~$1.50 billion in 2021, but with a slow recovery in annual earnings per share [EPS] relative to its peers, the stock still doesn't look like it's offering any near enough of a margin of safety for investors. This is because it's still trading at ~17x free cash flow estimates of ~$60 million in FY2025 on an enterprise value basis, which may be cheap for a low interest rate environment, but not nearly enough margin of safety for the current environment. And this is especially true when there are more recession-resistant businesses available at lower multiples, like Pet Valu ( PET:CA ) which trades at a lower multiple (16.0x FY2025 free cash flow estimates) as a mostly franchisor model.

So, what's a fair value for the stock?

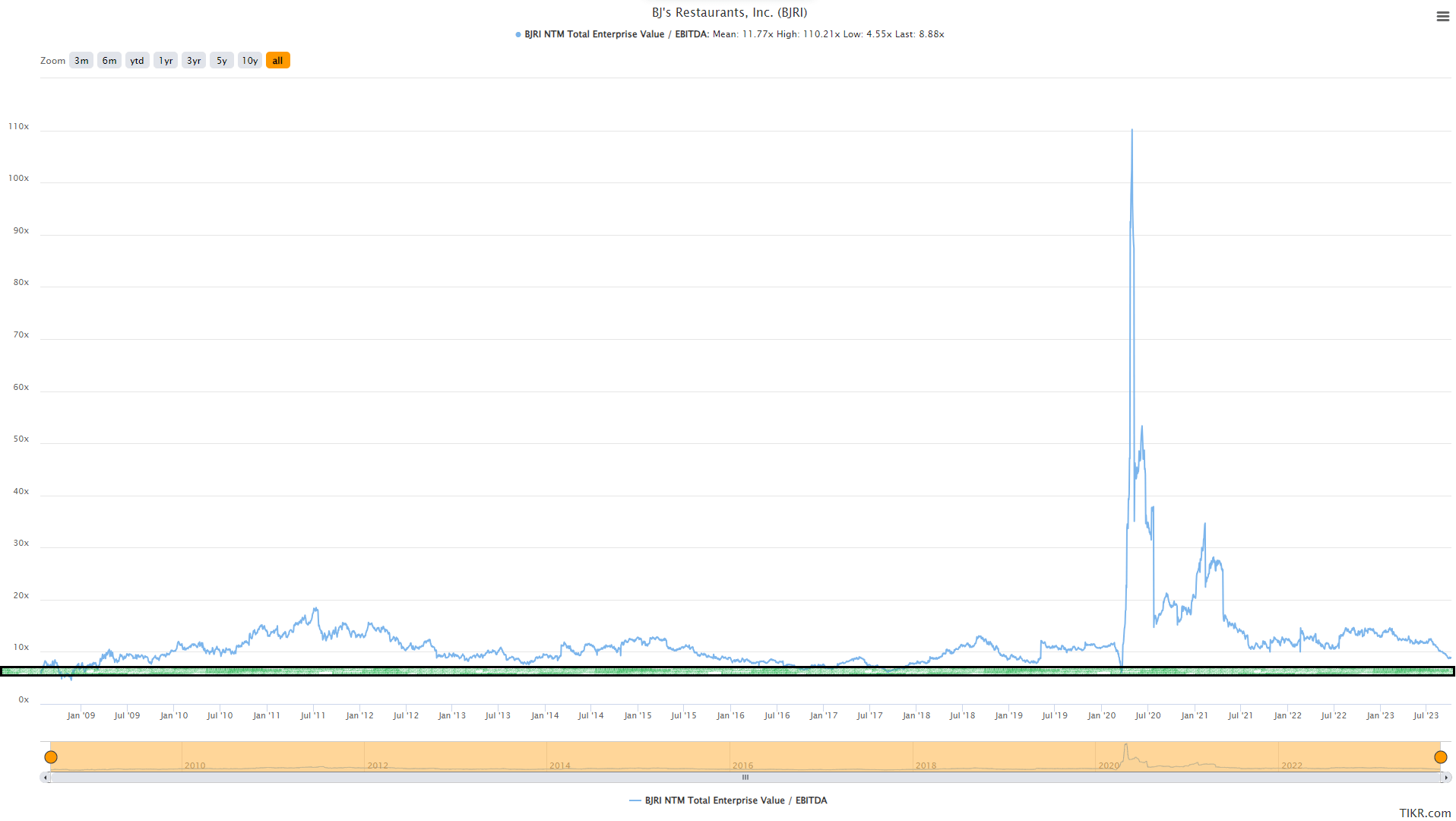

BJ's Restaurants - NTM EV/EBITDA & Historical Multiple - TIKR.com

{kind=link}

Using what I believe to be a more conservative multiple of 9.0x FY2024 EV/EBITDA to adjust for the current environment (~4.8% risk-free rate) and the backdrop of a much weaker consumer, I see a fair value for BJ's of $28.50, pointing to a 23% upside from current levels. However, when it comes to small-cap names, I am looking for a minimum 30% discount to ensure an adequate margin of safety, especially in an environment where some small-cap names are the most detached from fundamentals they've been in years. So, if we apply this required discount to fair value for BJRI, the stock's ideal buy zone comes in at $19.95 or lower, suggesting the stock still hasn't reached what I would consider being a low-risk buy zone.

Summary

BJ's Restaurants had a better Q2 than I expected and the company has done a decent job of delivering on cost savings to help claw back lost margins. That said, it looks like it could be another tough couple of quarters ahead for the restaurant industry judging by sales trends, and while BJ's may benefit from being somewhat of a value occasion relative to brands like Texas Roadhouse ( TXRH ), Outback ((BLMN)), and Cheesecake Factory ( CAKE ), even brands known for value are struggling, evidenced by the sales results from brands like Cracker Barrel ( CBRL ), and Denny's ((DENN)). Hence, I think it's difficult to be optimistic about BJRI beating estimates in Q3 or Q4, and without a beat I'm not sure what the catalyst is for the stock to move substantially higher. In summary, while I would get more interested in BJRI below $20.00 from a swing-trading standpoint, I continue to see more attractive reward/risk bets elsewhere currently.

For further details see:

BJ's Restaurants: Patience Required