BKLN - BKLN: Leveraged Loan Defaults Rising; Caution Warranted

2023-06-08 03:53:39 ET

Summary

- The leveraged loan market has seen a deterioration in credit quality, with an increase in the number of issuers rated B and CCC since the COVID-19 pandemic.

- Rising short-term interest rates may lead to higher default rates for leveraged loans, potentially surpassing junk bond defaults during the current credit cycle.

- The Invesco Senior Loan ETF has experienced a subtle shift in credit quality, which could impact its performance as interest rates continue to rise.

This article can be thought of as a companion piece to a recent article I wrote on the fixed-term high yield bond fund, the Invesco BulletShares 2026 High Yield Corporate Bond ETF (NASDAQ: BSJQ ).

In my BSJQ article, I mentioned a recent podcast from Wayne Dahl of Oaktree Capital discussing his views on credit markets. Mr. Dahl was constructive on high yield bonds because he believes high yield bonds yielding 8-10% offer attractive total returns to investors, if the bonds can avoid defaults. The recent COVID-19 pandemic flushed out weak companies (i.e. those rated CCC were forced into bankruptcy) while formerly investment grade companies were downgraded into 'junk' territory. Furthermore, post-the COVID-19 pandemic, many high yield issuers were able to take advantage of rock-bottom interest rates to refinance their high-yield bonds, so many are cashed up and may be able to weather any upcoming economic storm.

In the same podcast, Mr. Dahl was more cautious on the leveraged loan market, as the business dynamics that were beneficial to the high yield bond market appear to be flipped for leveraged loans.

For example, while high yield bonds have seen an increase in the number of issuers in the higher quality BB credit rating category, the exact opposite is true for leveraged loans. Since the COVID-19 pandemic, the leveraged loan market have seen an increase in the number of issuers rated B and CCC, as low interest rates kept many weak issuers alive (if barely).

Furthermore, there is a subtle difference between high yield bonds and leveraged loans that many investors are not considering. From the perspective of the issuer, if interest rates increase dramatically, an issuer of high yield bonds are relatively unaffected until they need to refinance their debts (and the astute issuers took advantage of rock-bottom interest rates to refinance their high yield bonds). On the other hand, leveraged loans generally pay floating interest rates, so from the perspective of the loan issuer, the debt servicing costs may have increased dramatically as the Federal Reserve have raised short-term interest rates by more than 500 bps in the past year.

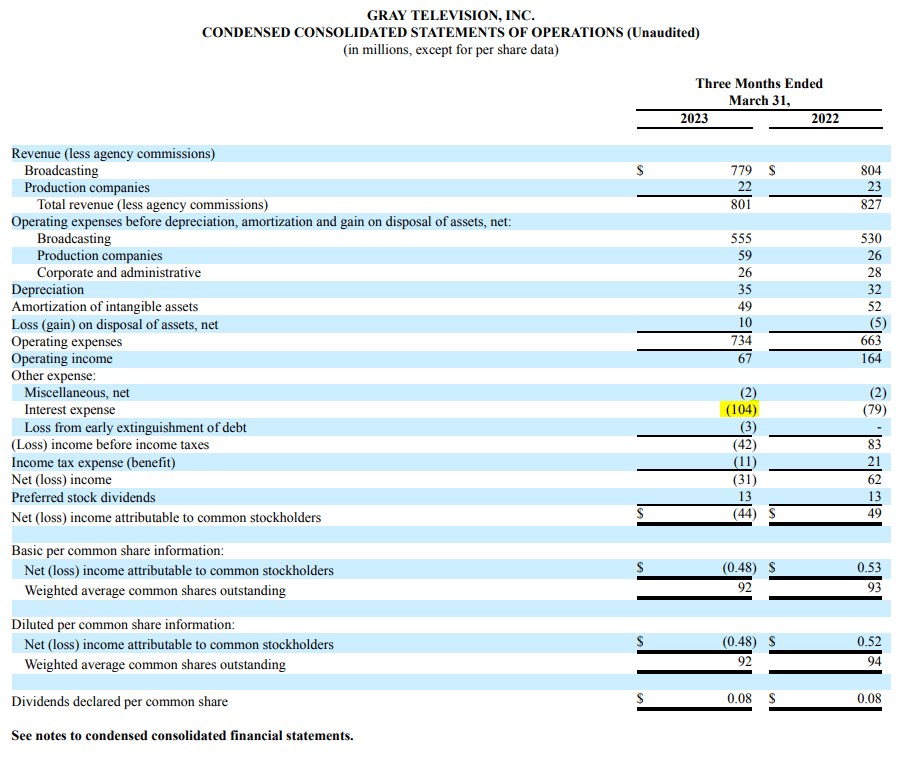

For example, one company that I analyzed recently, Gray Television Inc. ( GTN ), took out billions in term loans to help finance its acquisition of competitors. In Q1/2022, its interest expense on $6.7 billion in long term debt and loans was $79 million, or 4.7% annualized. However, by Q1/2023, its interest expense had risen to $104 million or a 32% YoY increase (annualized 6.7% rate), despite total debt being reduced to $6.2 billion (Figure 1).

Figure 1 - GTN saw interest expenses rise 32% YoY despite lower total debt (GTN Q1/23 10Q report)

{kind=link}

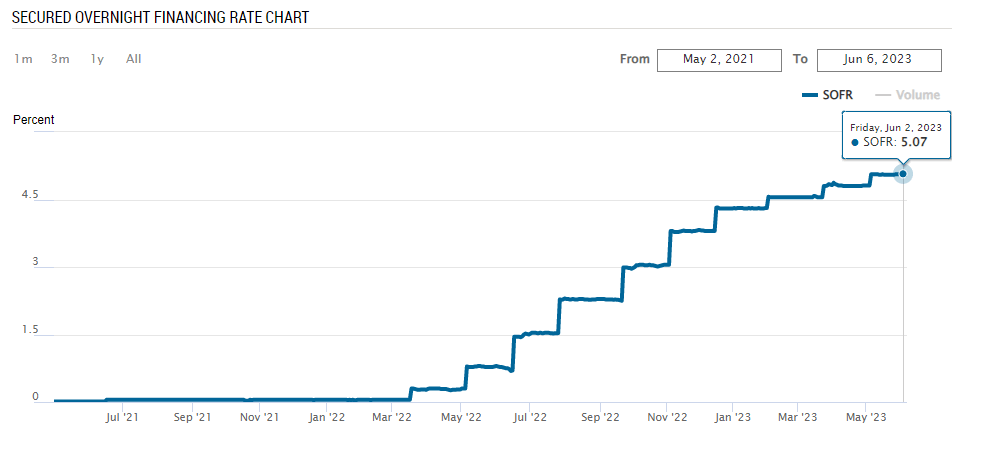

For context, GTN only had $2.7 billion in term loans that repriced higher with higher short-term interest rates. Imagine the pain issuers who primarily relied on leveraged loans must be facing. Companies that were paying all in debt costs of 2-3% when the Secured Overnight Financing Rate ("SOFR") was zero are suddenly finding themselves paying 7-8% in debt costs with the SOFR rate above 5% (Figure 2).

Figure 2 - SOFR rate have risen by over 500 bps (newyorkfed.org)

{kind=link}

This has important implications for the leveraged loan market and investment vehicles focused on leveraged loans like the Invesco Senior Loan ETF ( BKLN ).

Brief Overview of BKLN

The BKLN ETF tracks the investment results of the Morningstar LSTA US Leveraged Loan 100 Index ("Index"). The Index is a passive index that tracks the market value weighted performance of the largest institutional leveraged loans. To be included in the Index, leveraged loans must be senior secured, denominated in USD, and have a minimum initial term of 1 year and $50 million par value.

The BKLN ETF has $3.8 billion in assets and charges a 0.65% expense ratio.

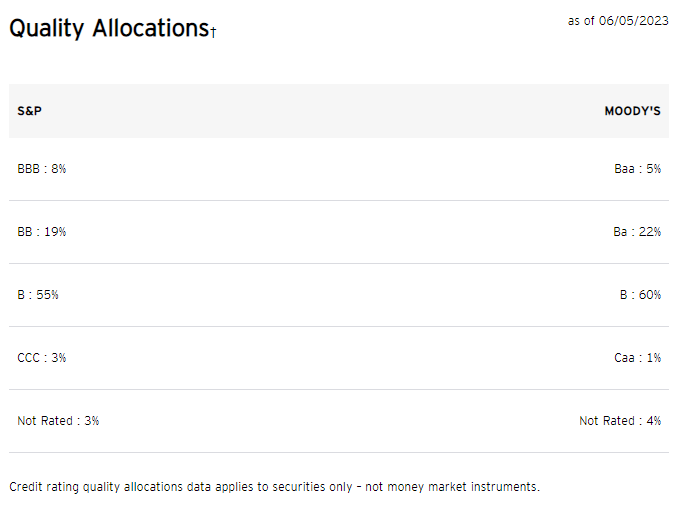

Credit Quality Deteriorating In BKLN

Since I first wrote about the BKLN ETF in September 2022, we have seen a subtle shift in the credit quality of the loan portfolio. Figure 3 shows the credit quality allocation as of September 19, 2022.

Figure 3 - BKLN credit quality September 2022 (invesco.com)

In a recent snapshot on June 5, 2023, we can see that securities rated B by S&P and Moody's have increased to 55% and 60%, respectively, from 51% and 52% back in September (Figure 4). For a passive investment fund, this is a worrisome deterioration in the credit quality of the portfolio within a short-period of time.

{kind=link}

Could Leveraged Loan Defaults Surpass Junk Bonds?

Historically, leveraged loans are considered safer credit instruments compared to junk bonds as they have first-lien senior secured claim on a company's assets.

As I mentioned in my prior article on BKLN, Standard & Poor's expects leveraged loan default rates to reach 2.5% in a base case scenario and hit 4.5% in a pessimistic recession scenario (Figure 5).

Figure 5 - S&P expect leveraged loan defaults to rise (Standard & Poor's)

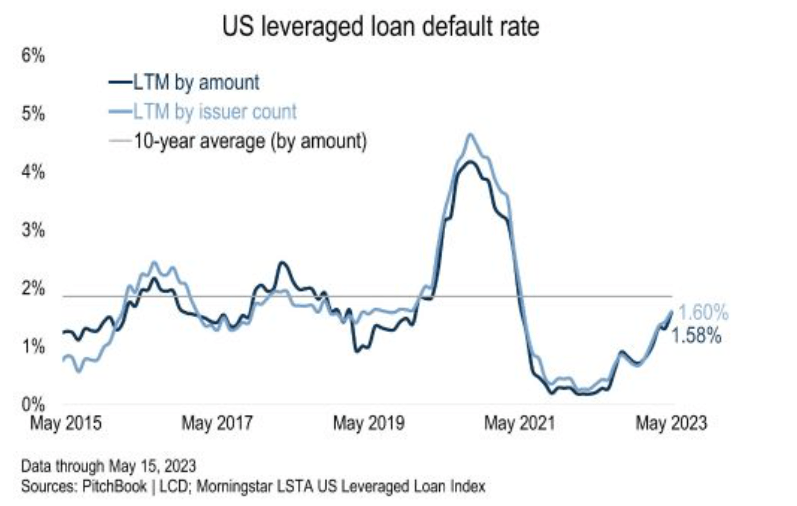

Since S&P's article in March, we have seen leveraged loan defaults rising, with the recent default of 3 issuers on 1 day in May pushing the default rate to 1.60% by issuer count, the highest in 2 years (Figure 6).

Figure 6 - Leveraged loan defaults now at a trailing 1.6% (Morningstar / Pitchbook)

{kind=link}

Leveraged loan default rates are actually not far behind junk bond default rates, which reached 1.80% in April, according to Fitch . If short-term interest rates continue to ratchet higher, we may actually see loan defaults surpass junk bond defaults during the current credit cycle, which will be unprecedented.

Central Banks Surprising With More Rate Hikes

In the past week, we have seen global central banks surprise investors by raising interest rates unexpectedly. First, the Reserve Bank of Australia ("RBA") surprised investors by raising Australian interest rates to 4.1% on June 6th, in addition to signaling additional rate increases may be necessary to quell inflation. Ahead of the meeting, investors were only pricing in a 40% probability of a rate increase.

Similarly, the Bank of Canada ("BoC") raised its short term interest rates to 4.75% on June 7th, surprising markets that were giving an interest rate hike less than a 50/50 probability.

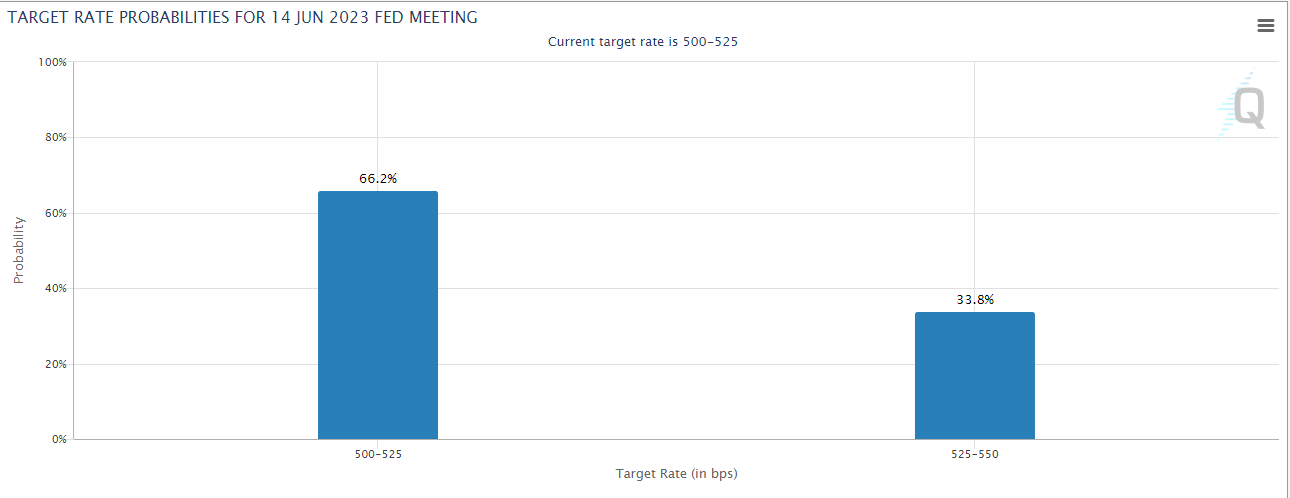

When we look forward to the Federal Reserve's upcoming FOMC meeting on June 14th, will we see the Fed follow its global peers and increase interest rates further? Currently, traders are pricing in a 2/3 probability of an interest rate hike next week (Figure 7).

Figure 7 - Markets pricing in 2/3 probability of a Fed hike (CME)

{kind=link}

The more central banks raise short-term interest rates, the more stress there is for leveraged loan issuers.

Higher Interest Rates Lead To Higher Yields

On the flip side, if the Fed continues to raise interest rates, the immediate impact will be higher yields earned by the floating rate BKLN ETF. Currently, the fund is paying a trailing 12 month distribution yield of $1.41 / share or 6.8% (Figure 8). In fact, the BKLN ETF has a 30-Day SEC yield of 8.8% and its latest monthly distribution annualized is 8.8%.

Figure 8 - BKLN paying an annualized 8.8% distribution yield (invesco.com)

{kind=link}

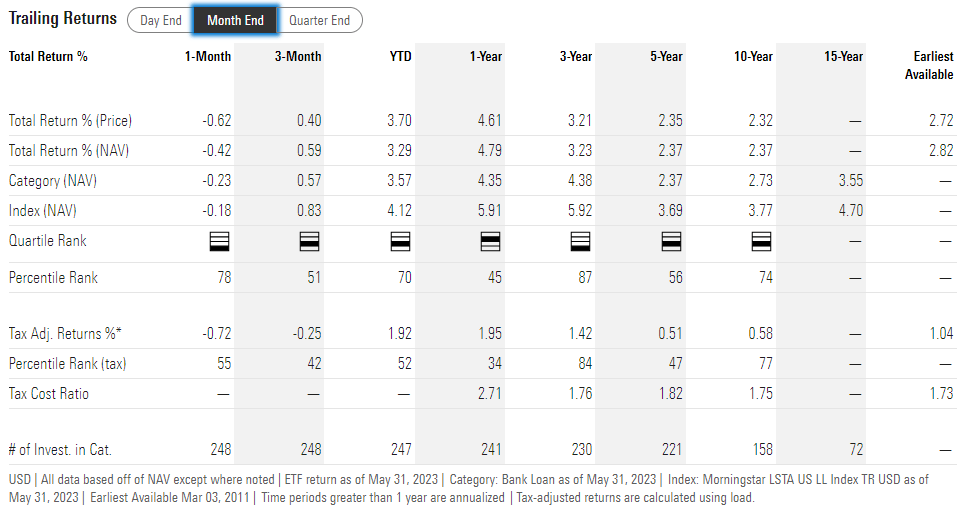

Balanced against this higher yield will be higher defaults from distressed issuers. Investors should note that although the BKLN ETF pays a 6.8% trailing yield, its total returns have only been 4.8% over 1Yr and 3.2% over 3Yr (Figure 9).

{kind=link}

This suggests that BKLN's portfolio may be suffering from increasing defaults (as noted in Figure 6 above) as well as widening credit spreads on its leveraged loans.

Conclusion

Overall, I remain cautious on the BKLN ETF, as I believe a recession is highly likely in the coming months. Furthermore, after hearing Mr. Dahl's comments regarding the leveraged loan market, I believe the default experience with leveraged loans may be worse than currently expected by market participants.

The ideal time to buy the BKLN ETF will be during the depths of the coming recession when credit spreads blow out and loans trade at steep discounts that more than cover their risk of default.

For further details see:

BKLN: Leveraged Loan Defaults Rising; Caution Warranted