BKLN - BKLN: Risks Skewed To The Downside

2023-03-24 11:51:49 ET

Summary

- The BKLN ETF gives investors a convenient way to invest in a basket of floating-rate senior loans.

- BKLN pays an attractive 6.0% trailing distribution yield.

- A regional banking crisis threatens to tighten financial conditions which could exacerbate weak leveraged loan performance.

- A pessimistic recession scenario could see 15-20% downside risk to leveraged loans.

A while ago, I wrote a cautious article on the Invesco Senior Loan ETF (BKLN), arguing that although the ETF's moderately high distribution yield of 6.0% was attractive, high total returns for the fund requires a specific set of conditions.

My main worry was that stubbornly high inflation was causing the Fed to hike interest rates at an unprecedented rate, with 475 bps of interest rate increases in the past twelve months. With a variable and significant time lag between interest rate hikes and their effects on the economy, it was unclear whether the Fed could achieve a 'soft landing' and bring inflation under control without causing a recession.

Fast forward 6-months, and I believe we are finally seeing the negative impacts of the Fed's 2022 interest rate hikes flowing through to the real economy. In the past few weeks, we have seen multiple regional banks fail and enter FDIC receivership because of a combination of unrealized losses on their securities portfolios caused by high interest rates and deposit flight as depositors flee to either safer institutions (the money center banks JPM, BAC, C, and WFC enjoy implicit government guarantees) or higher yields (money market funds and short-term treasuries are yielding 4 to 5% while deposit accounts pay 37 basis points on average ).

As Fed chair Powell noted in his recent FOMC press conference, "events of the last two weeks are likely to result in some tightening of credit conditions for households and businesses, and thereby weigh on demand", which could be equivalent to one or more rate increases. This is because with deposits fleeing out the door, the response from banks will be to conserve capital and tighten lending conditions.

Tighter lending conditions may exacerbate weak loan performance.

Leveraged Loan Performance Continue To Deteriorate

Beginning in mid-2022, the leveraged loan market have been under increasing pressure, as companies that gorged on debt in the post-COVID zero-interest rate environment suddenly had to deal with rising interest costs and slowing demand. According to Leveraged Commentary & Data , a news service covering the leveraged loan market, the ratio of U.S. leveraged loans downgraded vs. upgraded continued to trend higher, reaching 3.3x in February 2023 (Figure 1).

Figure 1 - Credit downgrades outpace upgrades 3 to 1 (Leveraged Commentary & Data)

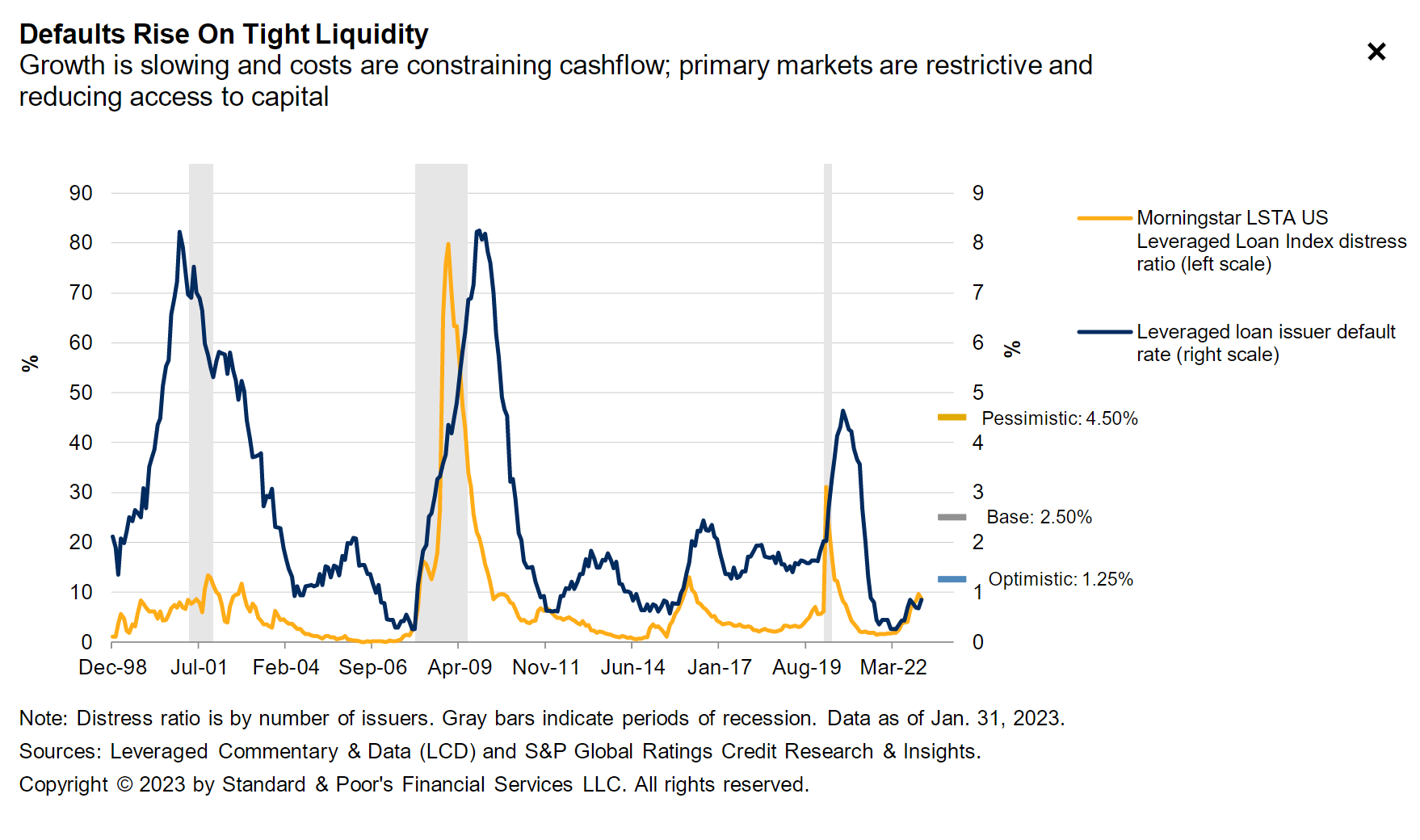

Defaults have also been creeping higher, with Standard and Poor's ("S&P") expecting U.S. leveraged loan defaults to reach 2.5% in the coming quarters under a base case scenario, and 4.5% under a pessimistic recession scenario (Figure 2). Note, a 4.5% default rate would roughly match the default performance during the COVID induced recession.

{kind=link}

On the ground, global corporate defaults have been occurring at the highest year-to-date rate since 2009 (Figure 3). This suggest we have indeed come to the end of the credit cycle and it may soon be time to pay the piper.

Figure 3 - Corporate default rates occurring at the fastest pace since 2009 (S&P)

Expect Poor Returns In The Coming Months From Widening Credit Spreads

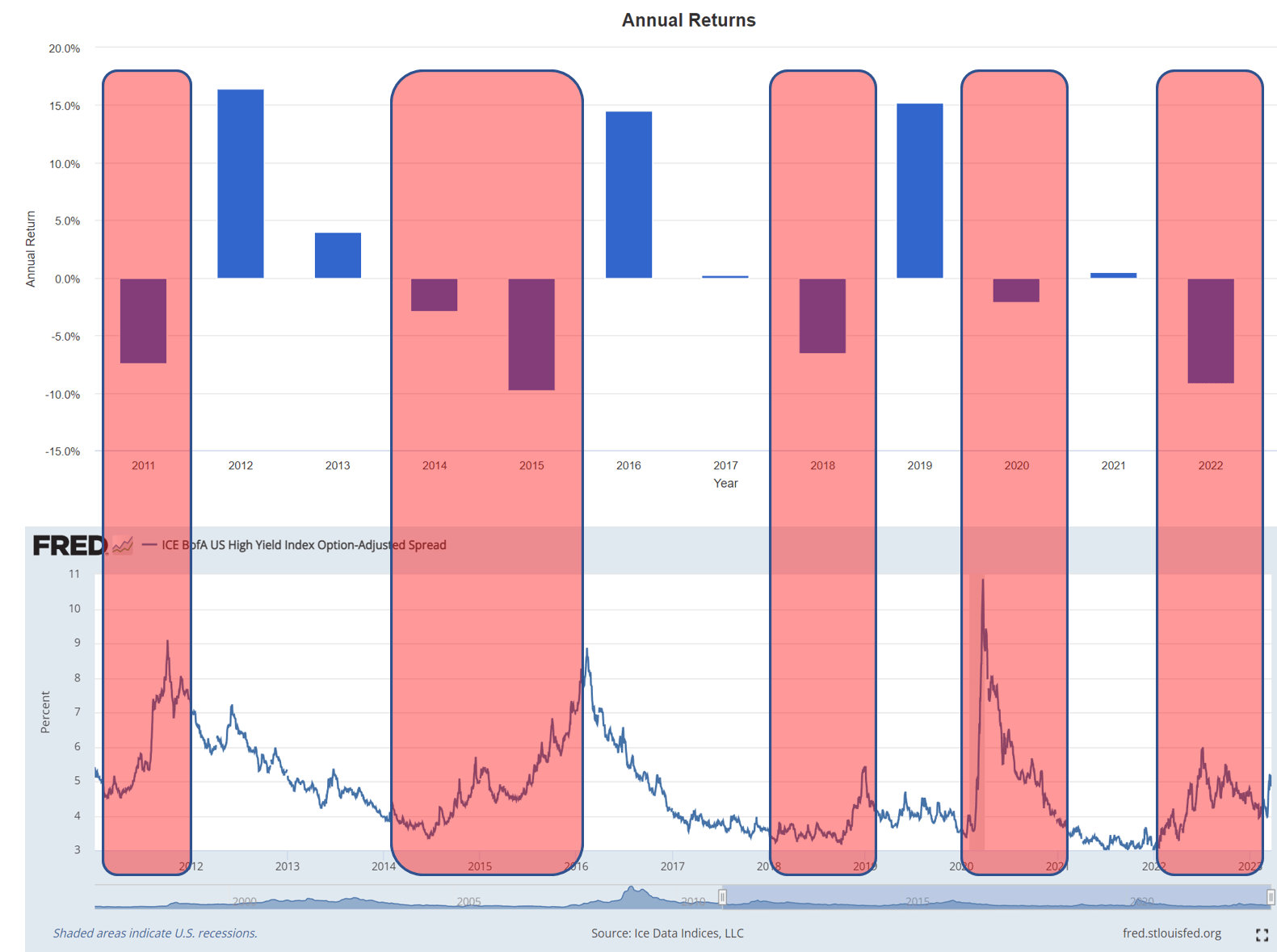

As I showed in my prior article, when credit defaults happen and credit spreads widen, the BKLN ETF usually delivers poor total returns. Unfortunately, with high yield credit spreads widening in recent weeks due to the developing banking crisis, I believe the BKLN ETF could be set to deliver back-to-back negative annual returns, like in 2014/2015 (Figure 4).

Figure 4 - BKLN performs poorly when credit spreads widen (Author created with annual returns from Portfolio Visualizer and high yield credit spreads from St. Louis Fed)

{kind=link}

In fact, if the U.S. economy enters a recession later in 2023, I believe there could be ~15-20% mark-to-market downside risk to the BKLN ETF if loan defaults rise to the expected 4.5%.

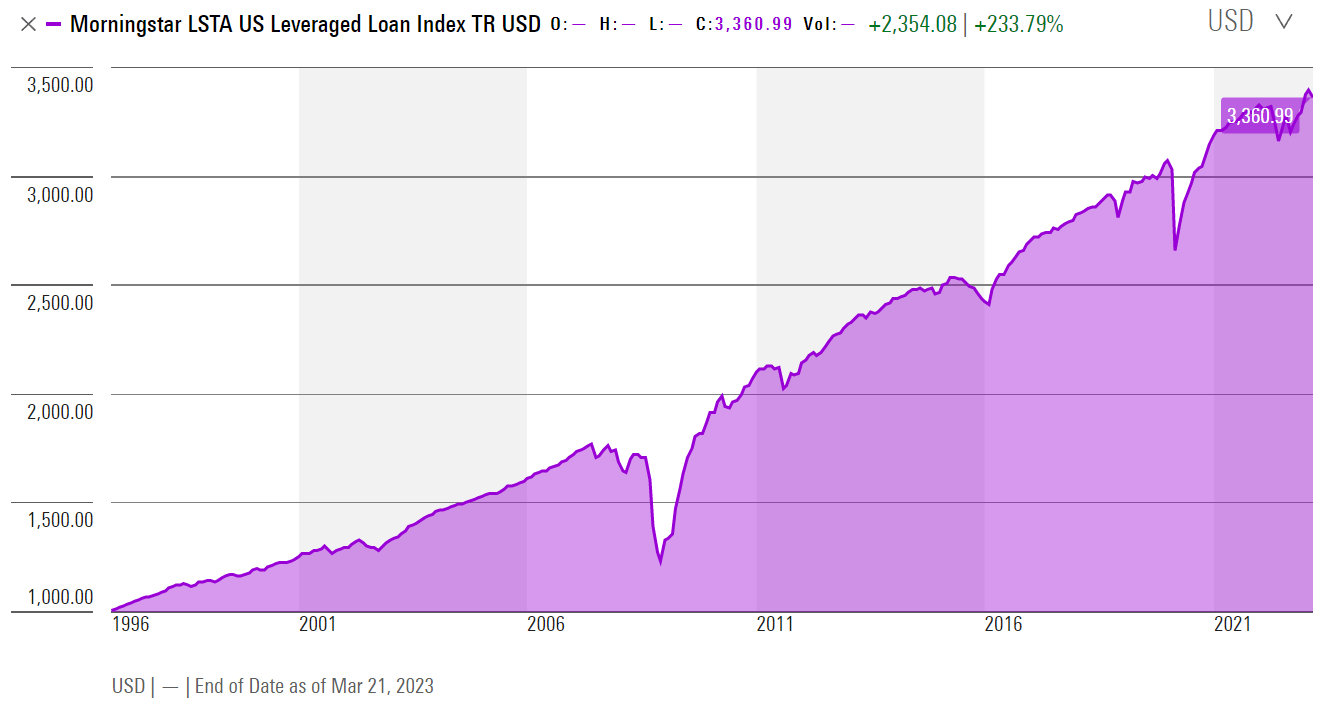

Historically, the Morningstar LSTA US Leveraged Loan Index TR USD suffered a 13.5% peak-to-trough drawdown during the COVID recession (with ~4.5% loan defaults) and a 30.0% peak-to-trough during the Great Financial Crisis (with ~8% loan defaults) (Figure 5).

Figure 5 - Historical leverage loan performance (Morningstar)

{kind=link}

The COVID pandemic drawdown was acute but short-lived, as governments and central banks rushed to rescue the economy and capital markets. The coming recession may be more prolonged than the COVID recession, as I believe there will be widespread pushback against government bailouts, especially with Republicans controlling Congress. Therefore, in the case of a recession, the drawdown in leveraged loan funds like BKLN could be somewhere between the COVID drawdown of 13.5% and the GFC drawdown of 30.0%.

Risks To My Cautious Call

The biggest risk to my cautious call is if the regional banking crisis does not develop into a credit crunch and the U.S. economy avoids a recession. However, even in this 'muddle through' scenario, I think loan defaults are likely to follow S&P's base case and rise to 2.5% and high yield credit spreads may stay elevated. Therefore, there will still be headwinds to the leveraged loan market and the BKLN ETF may not outperform.

In fact, as a potential BKLN investor, I would welcome recessionary credit conditions, as high credit spreads is a necessary condition to generate strong future returns for BKLN (from figure 4 above). The challenge, of course, is whether investors have the patience to wait for a 'fat pitch' where the decks are stacked in investors' favour.

Conclusion

Recent regional bank failures are set to further tighten financial conditions, which could exacerbate the already weak leveraged loan market. I believe there is significant risk of further credit deterioration and mark-to-market price risk to the leveraged loans within BKLN's portfolio. In a downside recession scenario, loan defaults could spike and cause 15-20% downside to BKLN. I believe the risks are skewed to the downside and would avoid most credit funds at the moment.

For further details see:

BKLN: Risks Skewed To The Downside