BKT - BKT: Harnessing The Power Of Agency-Backed Mortgages For Reliable Returns

2023-10-12 12:25:54 ET

Summary

- BlackRock Income Trust offers investors access to high-quality agency-backed mortgages, providing impressive returns with fewer fluctuations and risks than mortgage REITs.

- BKT has a long track record and has outperformed passive MBS indices, offering higher Sortino and Sharpe ratios.

- The fund's active management strategy allows it to hedge against rate changes and capitalize on new mortgage issuances, providing potential for consistent returns, utilizing institutional tools like swaptions.

Introduction

For those investors wanting a shelter from the roller-coaster ride of mortgage REITs, turning to government-insured mortgages, often referred to as agency-backed mortgages or securities, might be a smart move. These mortgages are either held outright or bundled into securities by one of the major government-sponsored entities, and they come with the backing or full ownership (as in the case of Ginnie Mae) of the US government's Department of Housing and Urban Development. Between Fannie Mae ( FNMA ), Freddie Mac ( FMCC ), and Ginnie Mae, there's a broad spectrum of securitized mortgages available to investors. These high-quality investment options can deliver impressive returns with fewer fluctuations and risks than your typical mortgage REIT.

The BlackRock Income Trust ( BKT ), a closed-end fund investing in mortgage-backed securities and government-sponsored entities, presents itself as an appealing pick for those investors wanting to increase the yield of their standard fixed income portfolios with the inclusion of agency-backed securities. These mortgages offer access to higher yields without risking default risk, falling in line with recent trends described as a "flight to quality."

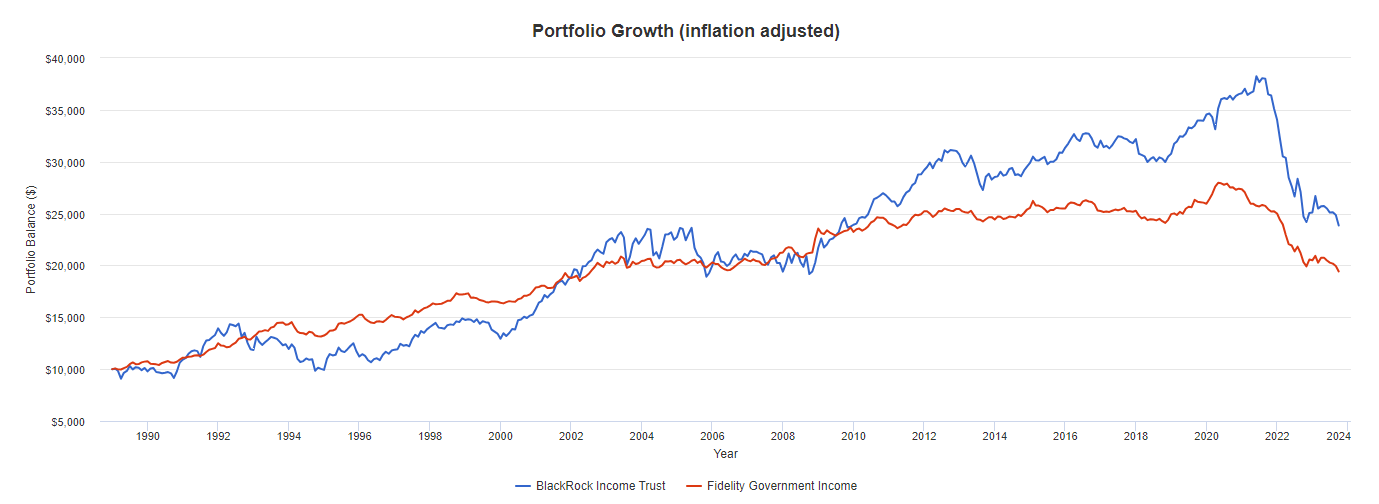

Founded in 1988, BKT has had a long track record. Below is an all-time performance graph of the BlackRock Income Trust (blue) ((BKT)) against the Fidelity Government Income mutual fund (red) ( FGOVX ). Both funds have the same credit rating, since they are both insured by the US government; both are actively managed, and both are run by tenured managers investing across asset classes.

34Y Performance (Portfolio Visualizer)

{kind=link}

Brief Overview

At a glance:

-

Price: $11.21.

-

Distribution Rate:9.44%.

-

Premium/Discount: (4.77)%.

-

Dividend Per Share: $1.0177.

-

Beta: 0.16.

-

Volatility (1Y): 11.44.

-

30-Day Trading Volume: 554,603.

-

Market Cap: $254,785,203.

Description: As per BlackRock -

BlackRock Income Trust, Inc.'s ((BKT)) (the 'Trust') investment objective is to manage a portfolio of high-quality securities to achieve both preservation of capital and high monthly income. The Trust seeks to achieve its investment objective by investing at least 65% of its assets in mortgage-backed securities. The Trust invests at least 80% of its assets in securities that are (i) issued or guaranteed by the US government or one of its agencies or instrumentalities or (ii) rated at the time of investment either AAA by S&P or Aaa by Moody's. The Trust may invest directly in such securities or synthetically through the use of derivatives.

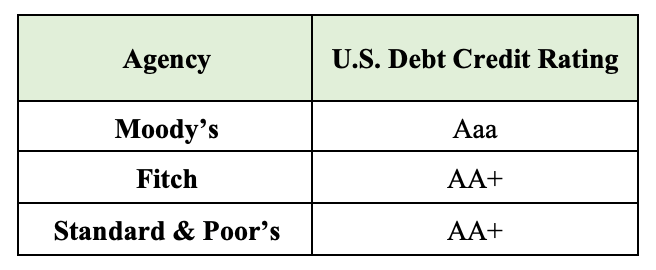

Note: The US government currently has an S&P credit rating below the fund's standard due to a recent downgrade . The fund's objectives allow it to purchase government debt regardless of the government's credit rating, but it is noteworthy nonetheless.

Current US Government Ratings (US House Budget Committee)

{kind=link}

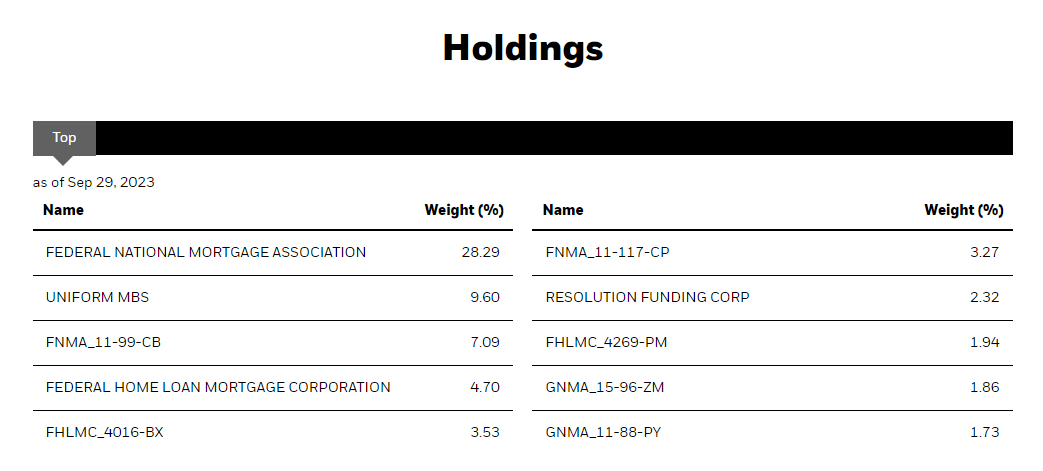

BKT employs a mixed asset strategy, holding stock as well as MBSs on their books. They hold about 33% stock, split between the two publicly traded agencies. Within that 33%, the two are split 85% ((FNMA)) and 15% ((FMCC)). The other 67% of the fund's holdings are MBSs, both uniform and not. Because of this split, distributions paid to investors enjoy nice tax treatment: 40% of distributions are income while 60% are return of capital. This varies from year to year, but the distributions are normally split close to these ratios.

BKT Holdings (Blackrock, Inc.)

{kind=link}

While the high ER of 1.17% on gross assets might raise eyebrows at first, it's worth noting that the fund's managers compensate for it by generating extra returns using leverage. Currently, the fund leverages 30% of its assets, but this ratio might shift as time goes on. The calculated use of leverage plays a pivotal role in securing those added returns in the MBS market. Part of the leverage also includes "swaptions," over-the-counter derivatives only available to institutional investors. Currently, 5.65% of the fund is overwritten by swaptions.

BKT distributes dividends monthly, with ex-dividend dates around the middle of the month, and payout dates toward the end of the month. Currently, the distribution rate is at 9.44% and has a yield-to-worst of 5.53%.

The fund trades at a discount of 4.77%, although this may change and go down further at times. The fund typically trades at a discount to NAV.

Comparing Agency-Backed and Non-Agency Backed Mortgages

If you're familiar with ABS and MBS, skip down to the next bolded section.

In the realm of real estate financing, understanding the distinction between agency-backed and non-agency backed mortgages is crucial. These two types of mortgages have unique characteristics, advantages, and potential pitfalls.

1. Origin and Definition:

-

Agency-Backed Mortgages: These are mortgages that are either guaranteed or issued by government-sponsored entities (GSEs) such as Fannie Mae, Freddie Mac, or Ginnie Mae. They conform to the standards set by these agencies and are, therefore, considered less risky.

-

Non-Agency Backed Mortgages: These mortgages are not guaranteed by any government agency. Instead, they are issued and backed by private lenders and financial institutions. They are often referred to as "private-label" securities.

2. Risk Profile:

-

Agency-Backed Mortgages: Given the government backing, these mortgages are perceived as having a lower risk. If a borrower defaults, the guaranteeing agency will cover the loss, ensuring that investors receive their due payments. This comes at the cost of lower interest rates for borrowers, meaning lower yields for investors.

-

Non-Agency Backed Mortgages: Without government backing, these mortgages come with a higher risk. If a borrower defaults, the loss is borne by the investor or the issuing institution. This risk often translates to higher interest rates for borrowers, leading to higher yields for investors.

3. Borrower Requirements:

-

Agency-Backed Mortgages: These mortgages have strict qualifying criteria , such as a minimum FICO of 620 for borrowers. Borrowers need to meet specific debt-to-income ratios and loan amount restrictions as well. These standards ensure the quality and safety of the loan.

-

Non-Agency Backed Mortgages: The criteria can be more flexible since private institutions set them. They might cater to borrowers with unique financial situations, like those with a higher debt ratio or those seeking jumbo loans exceeding agency limits.

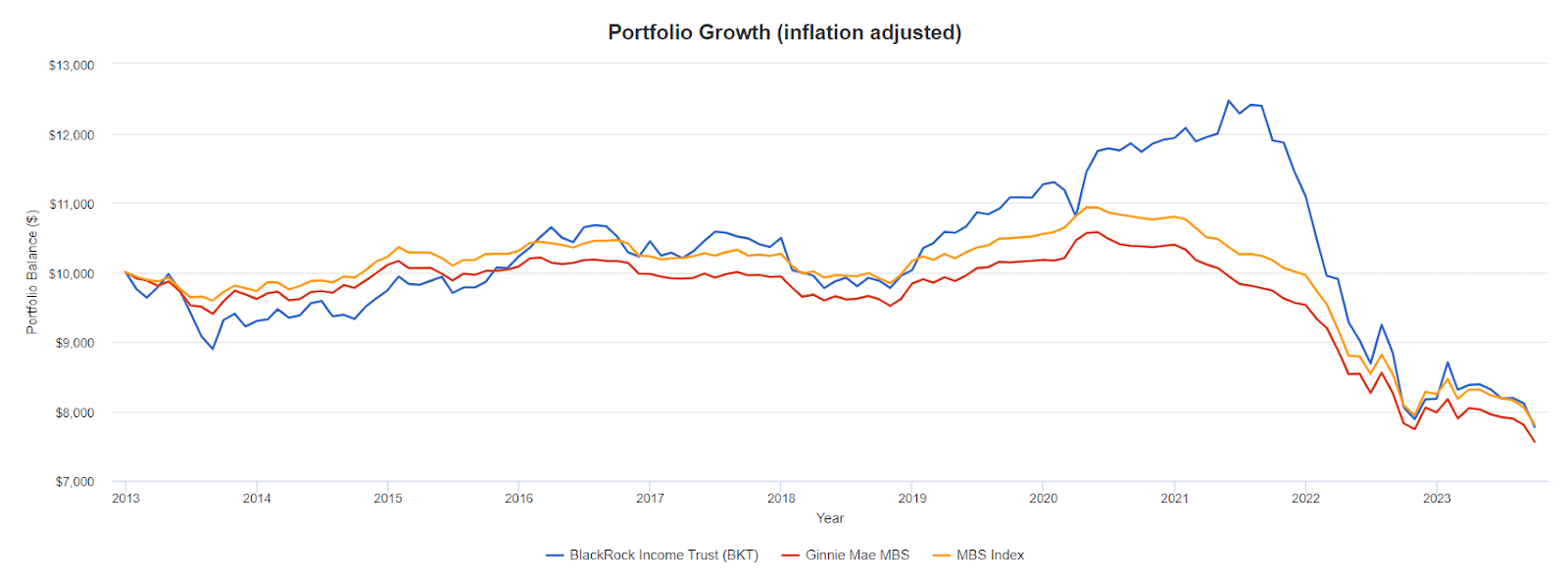

Compared to Ginnie Mae issues (red), and a passive MBS index (yellow), BlackRock Income Trust (BKT, blue) has shown its ability to add reward with little extra risk. It has a much higher standard deviation, 7% vs. the index's 3%, but BKT has had higher Sortino and Sharpe ratios for the last ten years because of its ability to capitalize on the upside with similar downsides to the index. Note: returns shown here are inflation-adjusted returns, assuming all dividends are re-invested at the time of distribution.

10Y Performance (Portfolio Visualizer)

{kind=link}

Rising Rates and New Issues

One of the most distinguishing features of BKT is its active management strategy. Because of the fund's ability to utilize leverage and swaptions, rate changes can be better hedged. This is exemplified in the return graph above where BKT was able to avoid falling below the return of non-leveraged MBS indices while rates shot up to historic highs.

Passive funds, by design, lack the flexibility and responsiveness that BKT's management team brings to the table. The ability to hedge rates with swaptions (similar to Simplify's golden child, PFIX ) was critical in navigating the last year. Now that rates have started to level off and we see projections of lowering rates going forward , mortgages with significantly lower default risk will become more and more attractive.

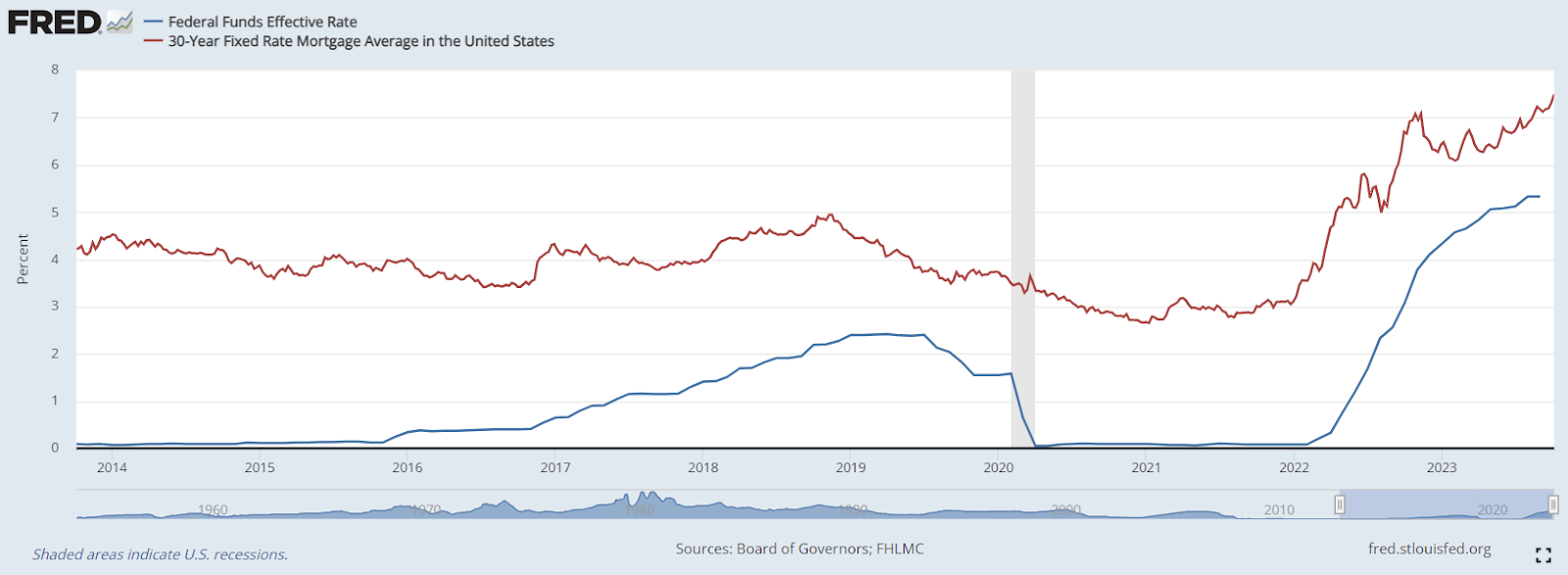

Most of these mortgages are fixed-rate loans, meaning that most funds, and all passive indices, are locked in at the low rates of the last decade. BKT is able to pivot to newly issued mortgages, and with the current fixed rates at 7.5%, investors should be welcoming of active management moving into these near-par mortgages. This kind of yield should allow for BKT to de-leverage themselves and still provide their target distribution rate of 10% going forward.

Fed Funds Rate & Average Mortgage Rate (Federal Reserve Bank of St. Louis)

{kind=link}

Should we be wrong (from a comment I left the other day: "Friends don't let friends fight the Fed!" ) and rates are still going to climb, BKT should be able to weather the storm with their swaptions.

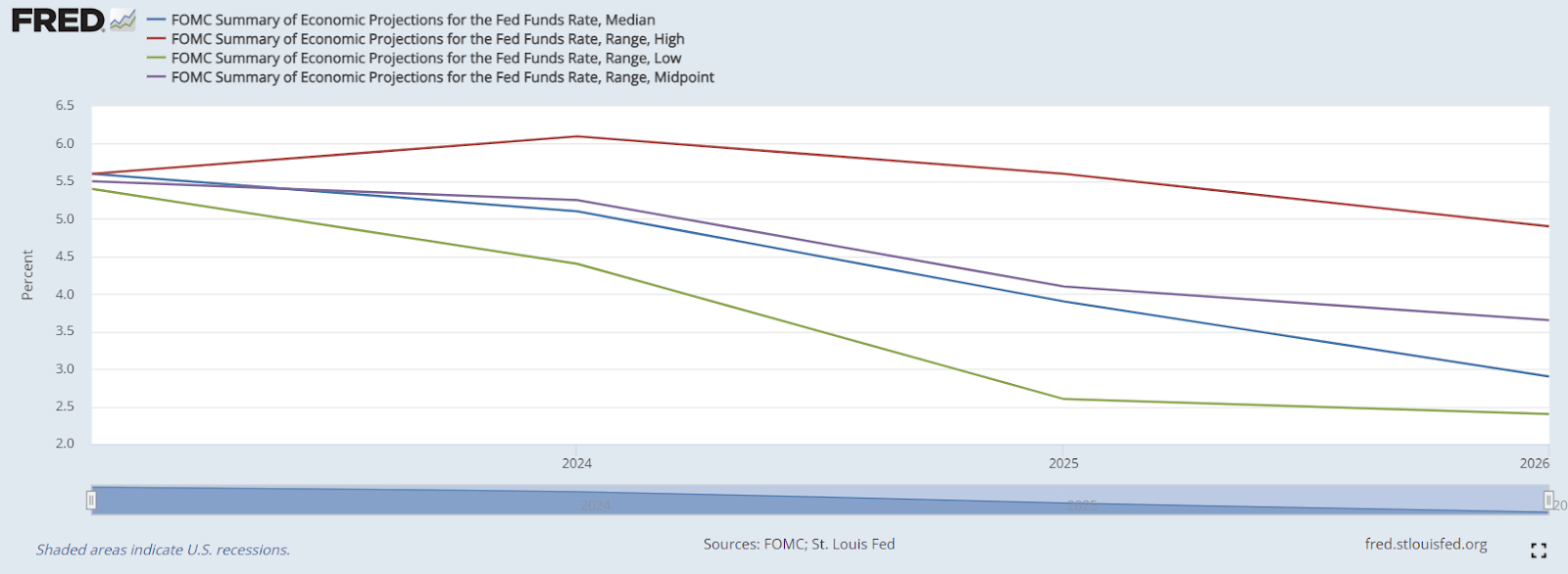

Projections high and low have rates lowering past next year, giving investors time to load up on mortgages while rates are high. As rates rise, mortgages become more risky, and more will be bundled into agency-backed securities until rates begin to fall again. Lenders do not want to take on borrowers with default risk in an uncertain economic environment .

FOMC Projections (Federal Reserve Bank of St. Louis)

{kind=link}

Growth of ABS Fuels Future Yields

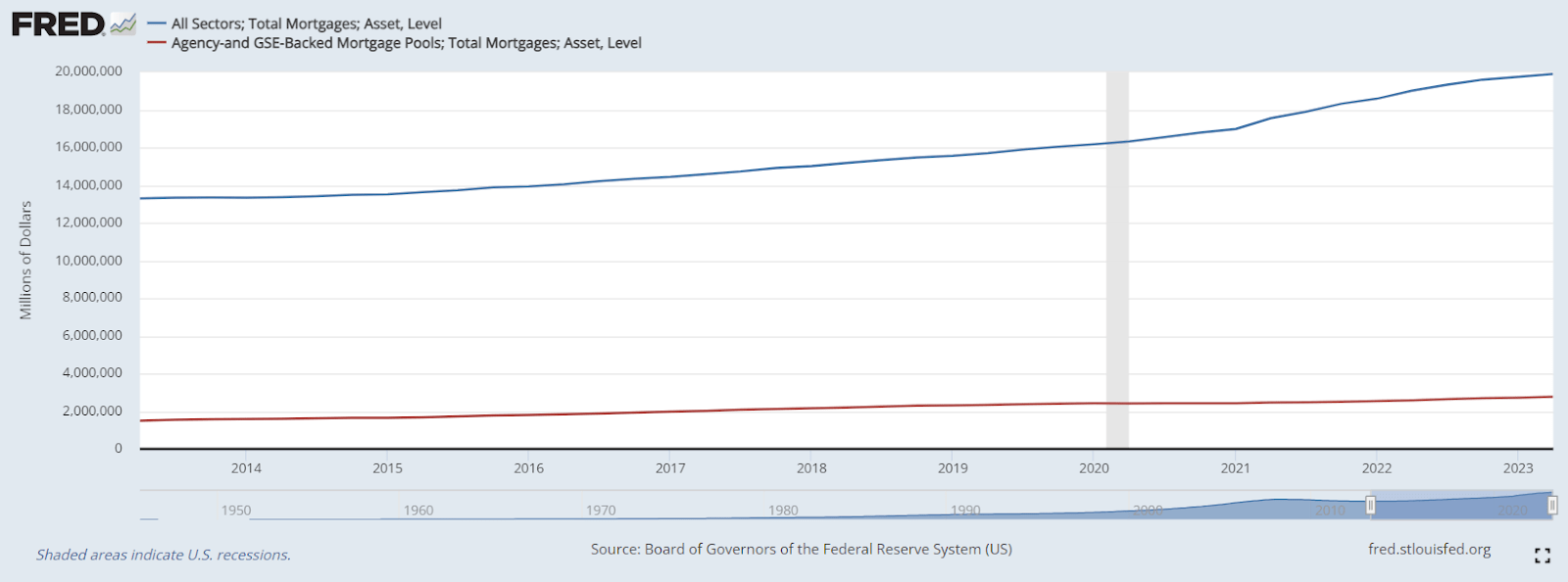

We have already seen a rise in ABS issuance in the last ten years. Looking back, we can see that while GSE-insured mortgages make up only a small percentage of total mortgages, their share of the market is rising. They have almost double the growth rate than total mortgages, showing us that there is increasing demand for less risky mortgages that shows no signs of slowing.

All Mortgages & ABS (Federal Reserve Bank of St. Louis)

{kind=link}

Total Mortgage issuance growth rate: 4.97% p.a.

Total ABS issuance growth rate: 8.40% p.a.

In order to keep attractive yields, funds like BKT require newly issued mortgages and MBS to add to their books. This increase in issuance means that BKT's management will have a greater pool of investments to pick from as they rebalance the fund's holdings; added diversity allows for a greater execution of the fund's edge: active management. Since the fund is not constrained to any set level of leverage, hedging, or asset allocation (aside from the rule about assets needing to be GSE-backed), the managers can react to shifting macroeconomic conditions.

Macroeconomic Opportunity

Recently, I wrote an article on a bank loan CEF , where I discussed increased credit card delinquencies , among other macroeconomic factors that have led me to believe that consumers are feeling a lot of pain from inflation and raised rates. Since ABS are guaranteed by GSEs, investors won't need to fear this pain hitting BKT.

Instead, opportunity lies in how long rates will need to be extended for, as it allows for the purchase of more fixed-rate mortgages at the higher rates. With the "higher for longer" narrative still the Fed's go-to, we can expect BKT to have ample time to add these new issued to its books.

Counterpoints

It is important to highlight the downsides to any fund that I do positive analysis for. Here are several of the potential issues investors may have with BKT.

-

CEF market prices have no guarantee of returning to NAV, and there is no guarantee that any discount, currently discounted by 4.77%, will not widen after the purchase of shares.

-

The management fee comes out to 1.17% of net assets, requiring BKT to outperform the passive index by that amount just to break even. This is a risk as well and can potentially drag returns.

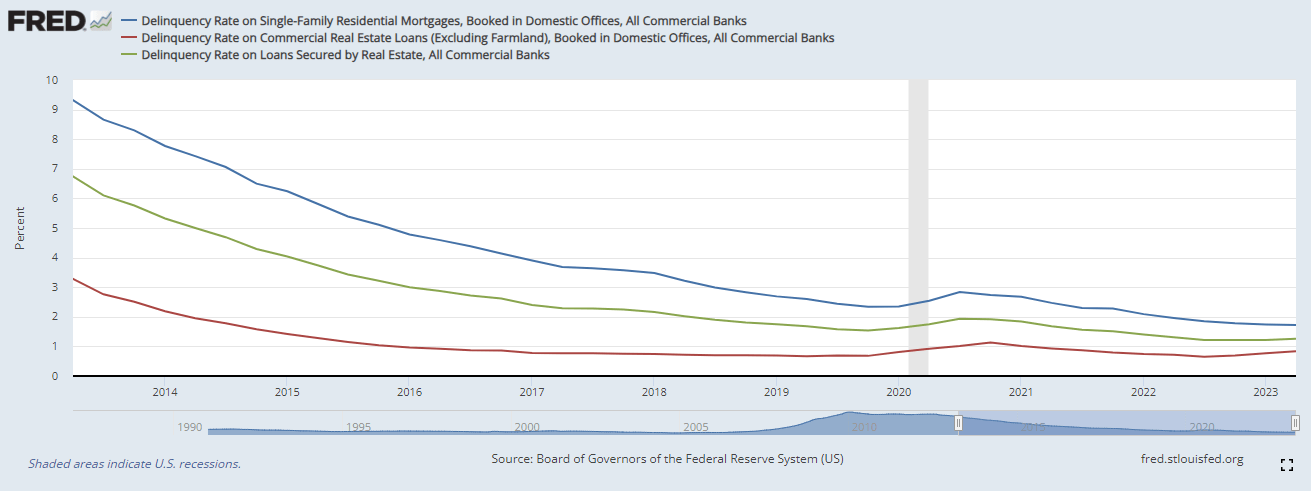

- Fears of mass mortgage defaults might be overblown, which could cause investors to seek safety in ABS and limit their risk short-sightedly. In the last ten years, we've only seen a decrease in defaults across the board in real estate. The delinquency rate for mortgages held by commercial banks in Q3 2020, the peak of pandemic-related defaults, was still lower than Q3 2018 and half the rate from Q2 2015. Overall, we see less risk in the markets, meaning that agency protection might reduce yields for little extra value.

Delinquency Rates on Mortgages (Federal Reserve Bank of St. Louis)

{kind=link}

Conclusion

For investors seeking refuge from the volatility of mortgage REITs, agency-backed mortgages present a compelling option. The BlackRock Income Trust ((BKT)) stands out as a notable player in this space, offering active management, strategic leverage, and a diversified portfolio that aims to deliver consistent returns in excess of 8-10%.

While the fund's expense ratio and the potential widening of its discount to NAV are points of consideration, its ability to navigate rate changes, capitalize on new mortgage issuances, and its resilience against macroeconomic challenges underscore its appeal. Rising demand for less risky mortgages and the growth of ABS issuance indicates a promising future for BKT.

For further details see:

BKT: Harnessing The Power Of Agency-Backed Mortgages For Reliable Returns