MBB - BKT: Risks Remain Elevated (Rating Downgrade)

2023-10-01 10:01:47 ET

Summary

- The article evaluates BlackRock Income Trust (BKT) as an investment option at its current market price.

- BKT has not performed well since the last review in 2022, leading to a less-than-bullish rating.

- The fund's extensive use of leverage and lack of diversification pose a heightened risk environment, making it advisable to avoid.

Main Thesis & Background

The purpose of this article is to evaluate the BlackRock Income Trust ( BKT ) as an investment option at its current market price. This fund is one I have written about many times, and is managed by BlackRock ( BLK ), with an objective to "manage a portfolio of high-quality securities to achieve both preservation of capital and high monthly income", primarily through exposure to agency mortgage-backed securities.

This is a fund I have owned in the past but turned sour on when I shifted away from fixed-income funds for the most part. This occurred back in 2022, when I last covered BKT. Over the past year and a half from that review, BKT has indeed vindicated a less-than-bullish rating:

Fund Performance (Seeking Alpha)

Given the time that has passed since that article and the recent volatility in the markets, it seemed like a good time to take another look at BKT. As a fund that investors in agency MBS - one of the safest asset classes in the market in terms of credit quality - this could seem like a reasonable play for those worried about more turmoil. While tempting, I actually see a heightened risk environment for BKT given its extensive use of leverage and lack of diversification. As a result, I believe this fund should continue to be an "avoid", and I will explain why below.

2023 Has Not Been Kind To Agency MBS

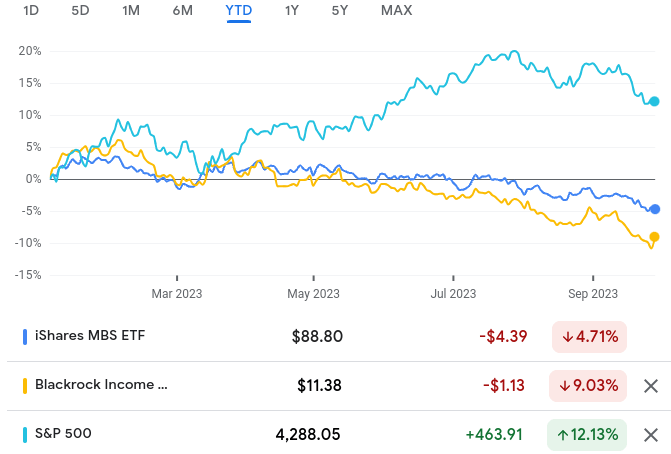

To start, let us take a moment to reflect on how the macro-environment has been treating agency MBS this calendar year. In a nutshell - it hasn't been pretty. To illustrate, let us compare BKT (which invests almost exclusively in agency MBS) and a benchmark fund for this sector - the iShares MBS ETF ( MBB ):

YTD Performance (Google Finance)

{kind=link}

As you can see, agency MBS have been a losing play this year. In fairness, fixed-income as a whole has struggled, but this has limited their usefulness given how strongly equities have rallied.

Of note, BKT has been hit harder than the benchmark ETF. This is due to a sustained inflationary environment and inverted yield curve. On the one hand, inflation readings have kept the Fed keeping short-term rates elevated:

{kind=link}

Simultaneously, concerns about longer-term economic health are keeping long-term rates from rising as quickly. This is pressuring borrowing costs for leveraged CEFs (such as BKT), while limiting income opportunities at the longer end of the yield curve. This is central to why BKT has under-performed MBB.

The concern here is that the macro-environment is not going to change much in the next few months to shift this dynamic. While further out agency MBS may have a brighter future and BKT could rally, in the near term these headwinds remain in place. Inflation is still too high and the Fed is still committed to a "higher for longer" rate environment. This means that leveraged CEFs that focus on fixed-income securities will keep on feeling pressure. For this reason, BKT's weakness in 2023 has a reasonable chance of continuing.

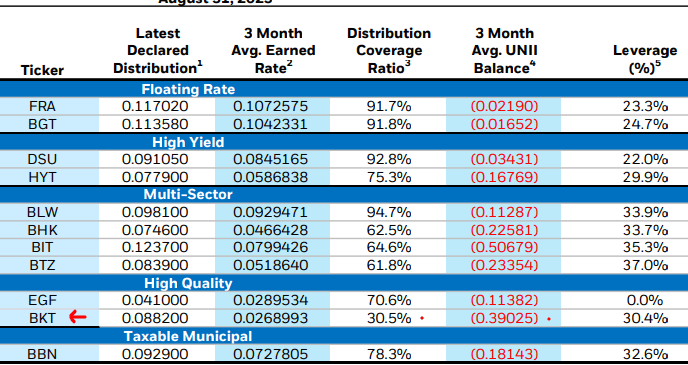

Problems With BKT? Income Metrics Are Weak

The biggest problem I have with BKT at this moment is more of a micro-concern. This is income production which, unfortunately, is looking very shaky. During my last article, I highlighted this as a problem, yet BKT has continued to pump on a consistent (and high) yield in the interim. That's the good news.

The bad news is that the fund's income metrics have deteriorated quite substantially since then. This has occurred to the point where I cannot see how the fund can maintain its current level going forward. A cut seems extremely likely given how low the coverage ratio is and how many months in arrears the negative UNII balance is registering:

{kind=link}

One would probably have to wonder how BKT is maintaining this income stream with such lousy income metrics - especially since those metrics have been consistently weakening with time!

The answer lies in how the fund is offering this payout. Those words "return of capital" (which I generally don't like to see for monthly payouts) are the underlying solution - as noted in BlackRock's most recent notice:

Return of Capital Illustration (BlackRock)

{kind=link}

My point here is a simple one. BKT is at high risk of a dividend cut and that cut is likely to pressure the share price when it occurs. While the fund's discount to NAV (more on that below) and its ability to still pay a "high" yield even after a cut will help buffer the downside, it is generally advisable to buy after a cut and not before it. That is why I will only be considering this fund until that headwind has cleared - which I expect to happen in the short-term.

Valuation Not An Automatic Catalyst

I am now going to shift and examine what some may consider a positive of the fund. This is the valuation, which rests at a discount in excess of 4% at time of writing:

BKT's Current Price (BlackRock)

{kind=link}

As my followers know, I tend to prefer CEFs at a discount. So this could make BKT an ideal candidate. And, to be fair, it does suggest it is at least worthy of consideration. But there are a few key points for why I am not bullish on this fund despite the valuation at the moment.

One, BKT's discount valuation is not unique. It often sits at a discount so hoping it will move to par (or at a premium) after one purchases it is not the most realistic scenario on a short time horizon. Two, BKT actually had a wider discount when I last covered it last year! That means, despite losing 8% in total return since that time, the discount has widened. That has occurred because the NAV has been in a constant downtrend over the past few years, as illustrated below:

1,3, & 5-Year NAV Performance (BlackRock)

{kind=link}

This is not a good sign and reflects how detrimental the fund's "return of capital" strategy has been. I'd rather see the distribution cut and the NAV stop hemorrhaging losses, but clearly the management team has other ideas.

The overall takeaway here for me is not that the discount to NAV is "bad", but simply I don't see it as much of a tailwind for the rest of 2023. The fund has sat at a discount for a while without it helping much, and to think that is going to change right away is not that realistic. So while BKT checks the box on an attribute I generally like to see, it isn't enough to make me a buyer for now.

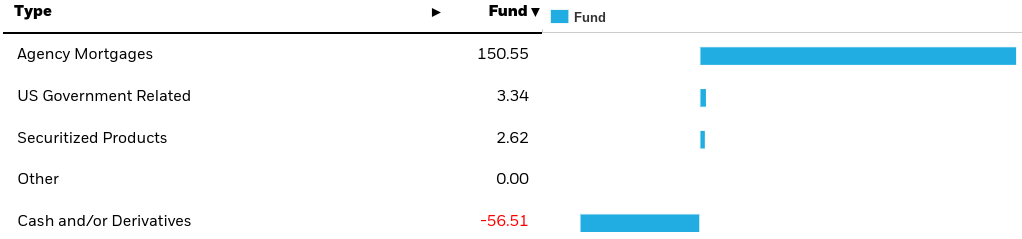

Agency MBS Have An Interesting Dynamic

I will now take a moment to consider the broader agency MBS space. As mentioned, this is pretty much all BKT owns - and it does so in a leveraged capacity:

{kind=link}

So it stands to reason one would want to be very bullish on this sector before diving in to this particular fund.

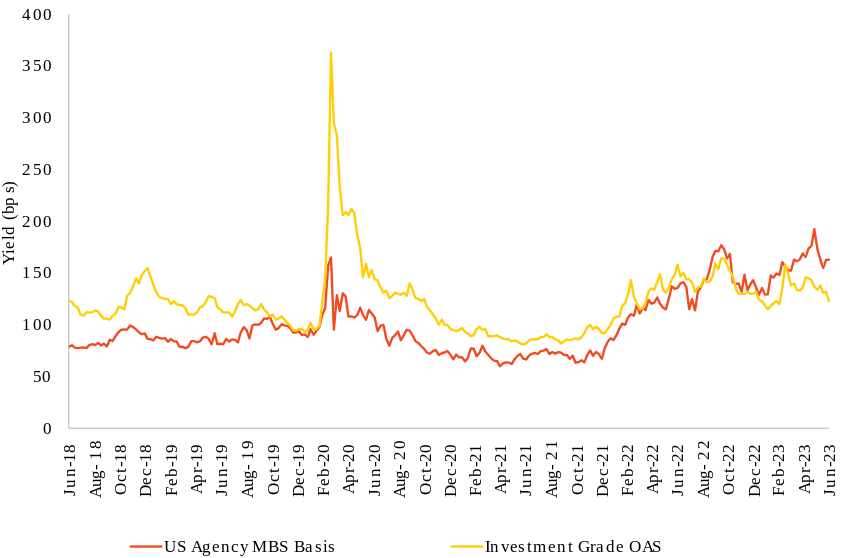

On the surface, there are fundamental reasons to consider agency MBS in this environment. It is generally a very stable asset class given the agency backing and/or protection, so these securities can be useful in a down or turbulent market. Further, agency MBS have seen their attractiveness relative to treasuries grow over the course of 2023. These are often seen as substitutes for each other given they are backed by the US government (albeit in different ways). So investors in these generally low-risk securities often compare the two. Currently, agency MBS have a very apparent spread advantage:

MBS and IG-rated Corporate Bonds' Spread Over Treasuries (Yahoo Finance)

{kind=link}

As you can see, agency MBS are offering a spread to treasuries that is both higher than IG-rated corporate bonds and one that is also above-average for the sector based on the last five years. This suggests there is some inherent value in this idea - contradicting some of the other points I have made in this article.

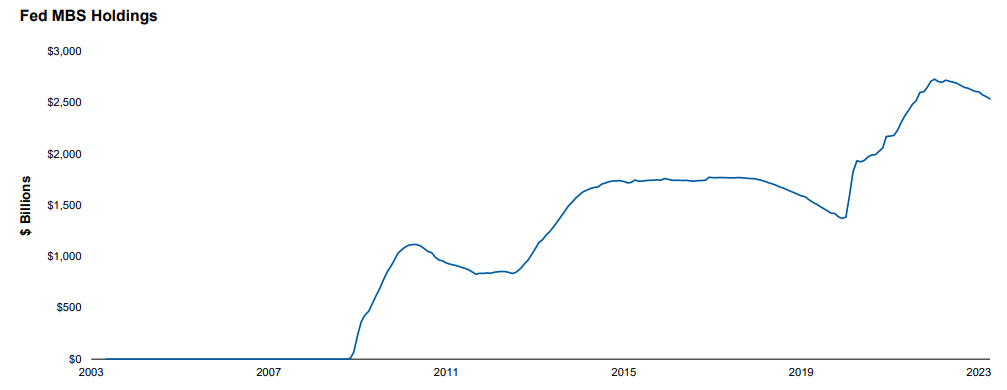

The problem is that this spread exists for a few reasons and one is that the Federal Reserve has been allowing MBS to roll-off its portfolio. Without this price agnostic (and large) buyer, banks and private investors are going to have to make up the windfall. Given the size of the Fed's position in MBS, this is going to prove a challenge going forward:

Fed's MBS Holdings (Federal Reserve)

{kind=link}

Realistically the Fed is going to continue its taper and higher benchmark rate program in Q4. There is going to have to be a major shift in the economy and/or inflation metrics for this to change their course before the new year. With the Fed being a large buyer of MBS in the past, this tailwind is mitigated for the next quarter - and probably in 2024 as well.

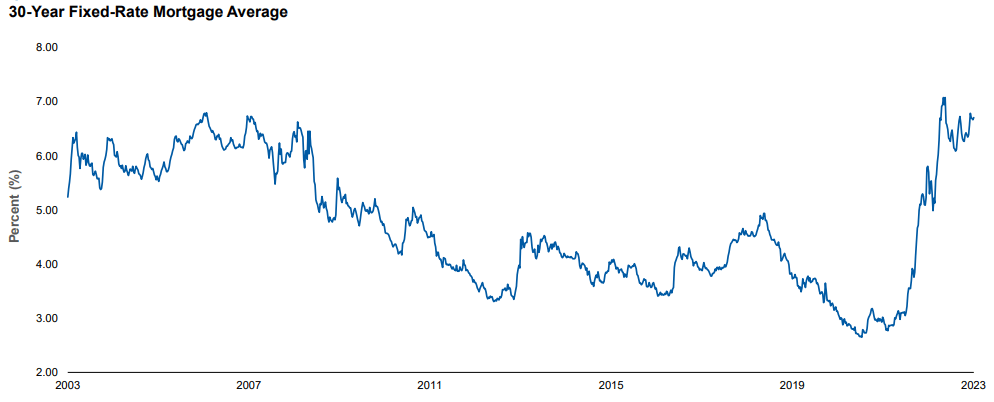

Can new buyers step in? Absolutely - and that very well could happen. This is just a risk - and risks do not always materialize into actuality. Given that new issues are yielding in the 6-7% range, finding new buyers may not be as hard as it sounds:

Current Rates (30 yr. MBS) (Bloomberg)

{kind=link}

With this in mind, readers must be asking - isn't this good news for both investor demand for BKT and for BKT's income stream?

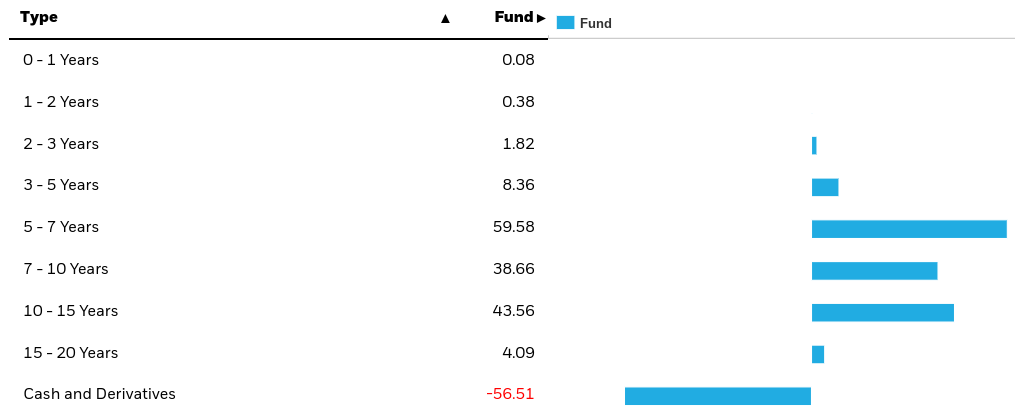

The answer is yes, but only marginally. The problem is that BKT cannot take immediate advantage of higher yields unless it is able to amplify its leverage. And I wouldn't be thrilled to see that in this environment. The reason is that BKT owns all MBS and by nature those are long-dated assets:

BKT's Holdings by Maturity (BlackRock)

{kind=link}

This means that BKT is stuck with securities yielding less than the prevailing rate. They can either sell them (probably at a loss) or increase leverage (which also increases expenses) to build a larger allotment of current MBS.

This is not the easiest of scenarios to navigate but has come about because prepayments of mortgages are on a sharp decline. As current rates rise, homeowners have little incentive to refinance. With the Fed showing no signs of cutting rates, BKT will continue to hold quite a large percentage of MBS that are not yielding what current offerings are. This presents an income headwind in addition to the one discussed previously.

Bottom Line

BKT has not been a strong performer of late and I'm not sure that will change. While agency MBS have some fine points going forward, this is not the way I would play the space. Leverage is getting punished this year as the yield curve remains inverted, BKT's discount is not enough to attract buyers, and the Fed continues to let its holdings roll-off (removing what was once a fundamental source of buyer demand).

This all adds up to an "avoid" for me. I will be hesitant to own or recommend this fund until the macro-picture changes. When it does, I will be happy to give BKT another look but at this time I can't find a compelling reason to not move on to greener pastures.

For further details see:

BKT: Risks Remain Elevated (Rating Downgrade)