BKT - BKT: Sell Before The Distribution Is Cut

2023-11-08 03:26:13 ET

Summary

- BKT is a leveraged MBS CEF.

- The fund's distributions are mostly return of capital, with low net investment income and coverage ratios.

- BKT has few benefits or positives.

I last covered the BlackRock Income Trust ( BKT ), an actively-managed, leveraged CEF investing in high-quality agency MBS, over two years ago. In that article, I argued that BKT's distribution uncovered, unsustainable distribution would be cut sometime in the future, making the fund a sell.

Although the fund has managed to maintain its distribution since, doing so has led to significant decreases in NAV, income, and distribution coverage ratios. Performance has been incredibly weak too, with the fund seeing losses of almost 30%, significantly underperforming bond and MBS benchmarks. As the fund's distribution remains unsustainable, the fund remains a sell.

BKT - Overview and Analysis

Strategy and Holdings

BKT is an actively-managed, leveraged MBS CEF. The fund almost exclusively invests in agency MBS, basically residential mortgages backstopped by the U.S. government. Other similar securities account for a small portion of fund assets.

BKT

BKT is an actively-managed fund, which means that yields and returns could somewhat differ from those of bond / MBS indexes. Ideally yields and returns are higher, through savvy investments and alpha. Both could be lower, however, if management buys underperforming securities, or focuses on the wrong sectors. Nevertheless, most of the safer, higher-quality securities, including agency MBS, behave in very predictable ways, so significant outperformance or underperformance are unlikely.

Credit Risk

Agency MBS have very low credit risk, as homeowners almost always pay their mortgages , and as these specific mortgages are backstopped by the U.S. Federal Government, the strongest, most credit-worthy institution in the world. There is some risk, either due to a government default (unlikely and unprecedented) or from changes in regulation / government policy.

Due to the above, agency MBS tend to experience very few losses during downturns and recessions. As an example, BKT saw no net losses during 1Q2020, the onset of the coronavirus pandemic. Fund performance was quite similar to that of broad-based bond indexes, and weaker than that of treasuries, which benefit from a flight-to-quality effect during downturns. Ignore the large spikes in the graph below, those are almost certainly data collection issues.

Data by YCharts

Interest Rate Risk

Mortgages tend to have long maturities, with 30 years being standard. Securities with long maturities tend to have high duration and interest rate risk, as investors are stuck with these securities for a long time. Lots of mortgages were made with 2.5% - 3.0% rates in 2020 and 2021, and investors will have to wait decades before they can replace these with current mortgages yielding 7.0% and more.

Investors might not even get the chance to do so, if rates come back down in the interim. On a slightly more positive note, mortgages sometimes get pre-paid, and these have interim capital payments too, so rate risk is somewhat lower than expected for securities with such long maturities.

BKT itself sports a duration of 9.4 years, which is quite high on both an absolute and relative basis. Results are consistent with the above.

Fund Filings - Chart by Author

BKT's high, above-average duration results in high, above-average losses when interest rates rise, as has been the case since 2022.

In most cases, high duration means strong, above-average gains when rates decrease . Investors might bid up the price of current 10Y treasuries with yields of 4.6% if the Fed slashes rates to zero, for instance (securities with 4.6% yields would look attractive with Fed rates at zero). Homeowners, on the other hand, would refinance their mortgages as rates decrease, limiting investor gains. Not all homeowners would do so, but enough would to limit gains.

Due to the above, BKT does not necessarily outperform when rates decrease, the fund's high duration notwithstanding. Excluding the pandemic, last time rates went down was in 2019, during which BKT underperformed, broadly in-line with expectations.

Data by YCharts

BKT's high duration is a negative for the fund and its shareholders, and one with almost no silver linings. Pure downside, more or less no upside.

Distributions and Coverage Ratios

BKT currently sports a 10.3% distribution yield. It is strong yield on an absolute basis, and higher than that of most bonds and bond sub-asset classes. It is also almost thrice that of benchmark MBS index ETFs, a very wide spread.

Actively-managed funds can boost their income through focusing on securities with comparatively high yields and leverage. Nevertheless, generating thrice as much in income as your benchmark is self-evidently implausible: similar securities generally yield similar amounts, markets are rarely that inefficient.

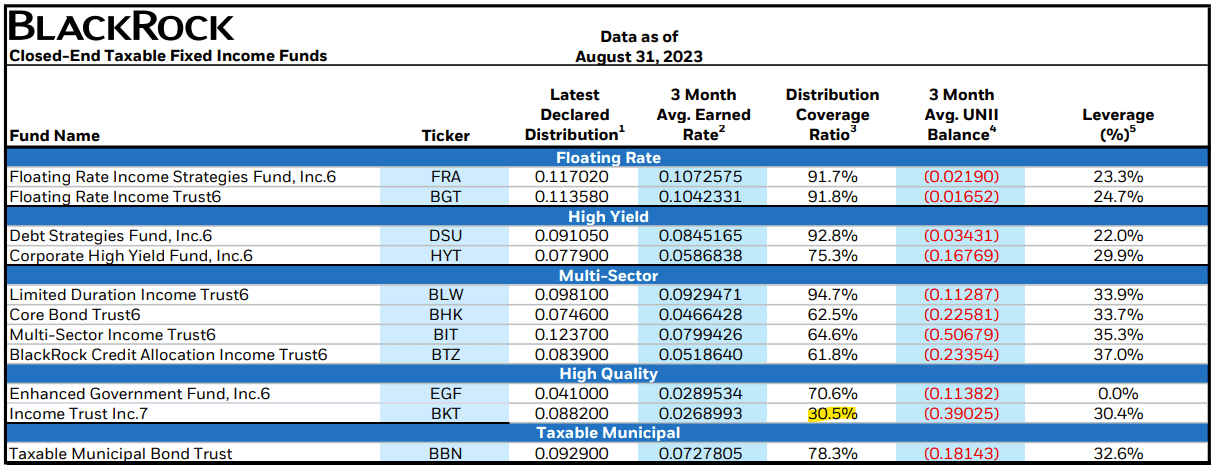

BKT does not, in fact, generate +10% in income, although exact figures vary. Management reports a coverage ratio of only 30.5%, implying income of only 3.0% - 3.5%.

{kind=link}

Said figures seem awfully low, as mortgage rates are currently at over 7.0%, and as (unleveraged) MBS ETFs yield +3.5%. BKT reports a yield to worst of 5.6%, which implies a distribution coverage ratio of 55% - 60%. Said figures seem more consistent with prevailing market conditions and rates, in my opinion at least.

BKT

In any case, BKT's distributions are quite clearly not covered by underlying generation of income. Capital gains could cover some of the gap, but almost certainly not all: MBS are income vehicles, and the fund's coverage ratio is simply too low for that.

Considering the above, BKT's distribution is almost certainly partly 'funded' through asset sales. Significant asset sales most likely. Due to this, fund NAVs should decline year after year, as has been the case since inception. Declines were much larger than those of MBS index ETFs too.

Funding a distribution through asset sales is unsustainable and self-defeating. As assets are sold, income and distribution coverage goes down, which means more assets need to be sold to cover the distribution, which means an even greater reduction in income and distribution coverage. The situation can't last for long, and rarely does.

One can see this process play out these past few years. From looking at prior coverage , the fund's distribution coverage ratio hovered around 70% in late 2021. A combination of losses and asset sales caused income to decline, with distribution coverage ratios hovering around 30% - 60% as of today. Lower coverage ratios means the fund will be forced to sell even more assets to fund its distributions, meaning quicker reductions in income.

As should be clear from the above, BKT's distributions are unsustainable, and will very likely be cut sometime in the future. In all honesty I would have guessed the fund would have cut by now, as the current situation seems untenable. Still, I do think the fund will be forced to cut, sooner or later.

Performance

BKT's performance track-record is below-average, at best. BKT consistently underperforms bond and MBS indexes on a NAV basis, but only very slightly so. Price performance is somewhat stronger, as discounts have tended to narrow. BKT currently trades with a 6.5% discount, not high enough to expect significant capital gains moving forward.

Seeking Alpha - Chart by Author

In my opinion, BKT's below-average performance track-record is a negative for the fund and its shareholders, although only a minor one at that. The unsustainable distributions and declining NAVs are very significant negatives, however.

Conclusion

BKT's unsustainable distribution make the fund a sell.

For further details see:

BKT: Sell Before The Distribution Is Cut