MBB - BKT: Vulnerable To A Correction And Distribution Cut (Rating Downgrade)

2024-01-22 06:31:46 ET

Summary

- The BlackRock Income Trust offers a high yield of 8.80%, making it an attractive option for income-seeking investors.

- The fund invests in AA-rated mortgage-backed securities, providing a reasonable yield for investors looking for guaranteed government-backed securities.

- While the fund has seen recent gains, there is a risk of share price declines due to the powerful run-up in bonds, and investors may want to take some gains and reduce their risks.

- The Federal Reserve is unlikely to cut interest rates to the degree that the market expects during 2024. That suggests that the fund will decline over the next month or two.

- The fund is consistently failing to cover its distribution and might be forced to cut, applying further downward pressure on the current share price.

The BlackRock Income Trust ( BKT ) is a closed-end fund that income-seeking investors can employ as a method of achieving their goals. The fund’s current 8.80% yield certainly appears to render it quite competent in this area, as this is a higher yield than many bond funds possess today. This is especially true because this is not a junk bond fund, but rather one that focuses on AAA-rated mortgage-backed securities. The iShares MBS ETF ( MBB ), which invests in similar assets, only yields 3.42% as of the time of writing. That would appear to make this fund one of the only ways to invest in mortgage-backed securities that are guaranteed by the U.S. government and still receive a reasonable yield. Retirees and other risk-averse investors in need of income to pay their bills might appreciate this.

As regular readers may recall, we last discussed the BlackRock Income Trust back in the middle of August. Obviously, a great many things have changed since that time, especially in the market environment. In August, market participants were slowly beginning to accept that the Federal Reserve might actually be serious about its “higher for longer” statements, which were reinforced by the federal funds rate hike the previous month. As such, bonds and bond funds were being sold off and yields were rising. This reversed in October, as optimism surrounding near-term rate cuts started to push bond prices up and yields down. This rally was sufficiently large to more than offset the mid-year decline and shares of the BlackRock Income Trust are up 1.78% since the date that the previous article was published:

{kind=link}

This may not seem like much, but it is a bit better than the 1.69% gain that the iShares MBS ETF delivered over the same period. In addition, the share price performance is not really a good indicator of how well a fund’s investors actually did. This is because closed-end funds like the BlackRock Income Trust tend to pay the overwhelming majority of their investment profits out to their shareholders in the form of distributions. This is different from index exchange-traded funds, as such entities rarely pay out their capital gains. As such, we should always include the distributions paid in any analysis of a closed-end fund’s returns. When we do that, we see that investors in the BlackRock Income Trust received a 6.49% total return since the date that my previous article on this fund was published. That is far better than the total returns provided by either the iShares MBS ETF or the Bloomberg U.S. Aggregate Bond Index ( AGG ):

{kind=link}

This is certainly going to make this fund appeal to those investors who are interested in receiving income while preserving their income. Unfortunately, this fund’s risks are higher than they were several months ago because of the powerful run-up in bonds over the past few months. It seems unlikely that this fund will be able to hold on to all of its recent gains and it may experience share price declines for a little while. We have already seen this in the fact that the fund’s share price is down over the past few days. As such, investors may wish to take some gains and thus reduce their risks. I am not recommending completely dumping the fund, but selling off some of your position should allow you to keep some of your recent gains and buy back in at a lower price following the correction. This process would actually result in higher income going forward, as you would have more shares after you buy it back at a lower price than you do now.

About The Fund

According to the fund’s website , the BlackRock Income Trust has the primary objective of providing its investors with a high level of monthly income while still preserving the value of its capital. This is a fairly common objective for a bond fund, and it does make sense since bonds are one of the only investments that guarantee a profit over their lifetime as long as the issuer does not default. There is little risk of default in this case though due to the nature of the bonds in which the fund invests. The website explains its basic strategy:

BlackRock Income Trust, Inc.’s investment objective is to manage a portfolio of high-quality securities to achieve both preservation of capital and high monthly income. The Trust seeks to achieve its investment objective by investing at least 65% of its assets in mortgage-backed securities. The Trust invests at least 80% of its assets in securities that are (i) issued or guaranteed by the US government or one of its agencies or instrumentalities or (ii) rated at the time of investment either AAA by S&P or Aaa by Moody’s. The Trust may invest directly in such securities or synthetically through the use of derivatives.

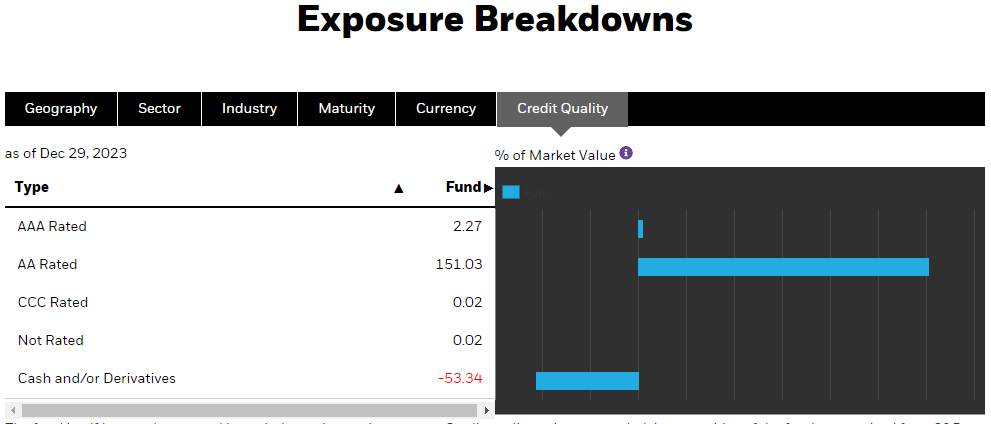

The United States government is generally considered to be free of default-related risk, at least in nominal terms. While it is true that an investor who purchases long-dated agency mortgage-backed securities and holds them until maturity may lose purchasing power due to inflation, most people do not actually consider that to be a default. For the most part, we can conclude that the securities in the fund are generally going to be free of default risk, at least if the fund is actually following its own guidelines regarding the composition of its portfolio. The webpage is not exactly clear on this, as nearly everything held by the fund is AA-rated, not AAA:

{kind=link}

The guidelines above seem to imply that this fund will only invest in AAA-rated securities but nearly all of its assets are invested in AA-rated securities. That would, on the surface, suggest that the fund is not following its own investment guidelines and is riskier than it claims to be. However, it is important to note that the United States government is not a AAA-rated entity. S&P and Fitch both have AA ratings on the Federal Government – only Moody’s still has an Aaa rating on the United States government. The fund’s website is not clear as to whether these are S&P or Moody’s ratings, but if they are S&P ratings then the fund could still primarily consist of U.S. government-backed mortgages.

The website suggests that this is indeed the case:

{kind=link}

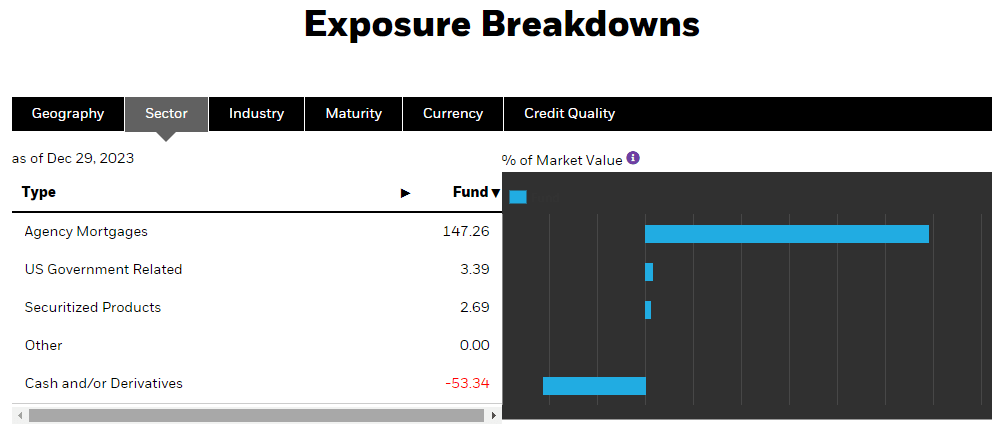

We can see that nearly all of the fund is currently invested in agency mortgages, which are mortgages that are guaranteed by Fannie Mae, Freddie Mac, Ginnie Mae, or something similar (such as the USDA). It is important to note though that mortgages backed by Fannie Mae or Freddie Mac are not explicitly guaranteed by the United States government. As such, they theoretically do have some default risk. However, due to the fact that both of these agencies are still in receivership and were basically taken over by the Federal Government during the sub-prime mortgage crisis back in 2008, these securities are almost certainly going to be about as close to default-free as bonds that have a stated guarantee. As such, we can see that the fund does appear to be satisfying its stated guidelines as to the securities that it holds in the portfolios. For the most part then, investors who are worried about losing money because of a default should feel relatively comfortable with this fund.

As some readers will almost certainly note, the above tables show that the fund actually has a negative weighting to cash and derivatives. This is because this fund is employing leverage as a method of boosting the effective yield of its portfolio. That makes sense since this fund has a yield that is competitive with most junk bond funds, yet it is investing in U.S. government-backed mortgages that most certainly do not have junk bond ratings. We will discuss this in more detail later in this article, but the leverage does increase the risk that this fund will suffer losses due to interest rate changes. As such, the fund is not completely risk-free by any stretch of the imagination.

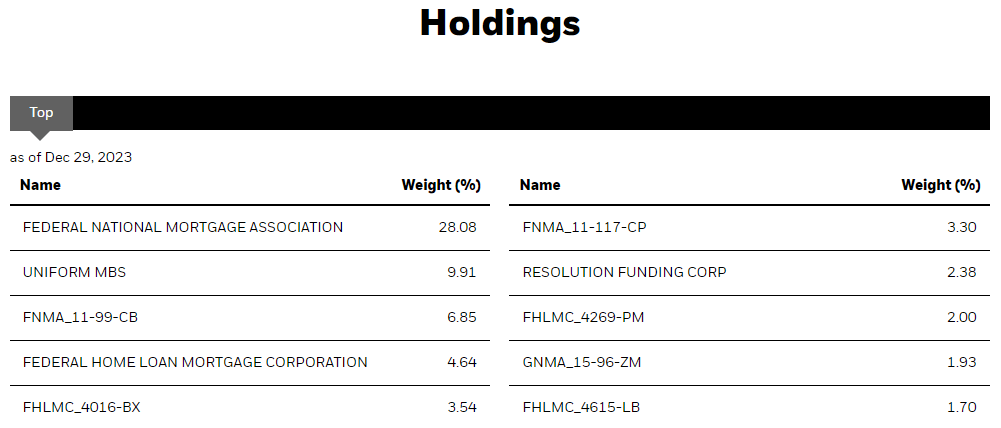

Here are the largest holdings in the BlackRock Income Trust as of the time of writing:

{kind=link}

As we can see, the largest position is a 28.08% weighting to securities issued by the Federal National Mortgage Association (Fannie Mae). However, we can also see some other Fannie Mae-backed securities in this portfolio, as both the FNMA_11-99-CB and FNMA_11-117-CP are the same thing. We can also see large allocations to securities issued by Freddie Mac:

| Freddie Mac Security |

| Weighting |

| Uniform MBS |

| 9.91% |

| Federal Home Loan Mortgage Association |

| 4.64% |

| FHLMC_4016-BX |

| 3.54% |

| FHLMC_4269-PM |

| 2.00% |

| FHLMC_4615-LB |

| 1.70% |

Finally, we see a 1.93% allocation to Ginnie Mae-issued mortgage-backed securities in the form of the GNMA_15-96-ZM issuance. The Resolution Funding Corporation, which is the only thing on the fund’s largest positions list that is not issued by one of the three government-sponsored mortgage securitization companies, is an entity that issued bonds to finance the government bailouts of various savings and loan associations during the 1980s. As is the case with the Ginnie Mae-backed securities, these bonds are explicitly guaranteed by the United States Treasury. As such, they should have relatively similar characteristics to U.S. Treasury securities and be free of default risk.

As regular readers are no doubt well aware, I do not typically like to see any individual issuer account for an outsized proportion of a bond fund. This is due to the fact that a large weighting removes many of the benefits of diversification and makes the fund’s shareholders vulnerable to the risks of that asset individually. In the case of this fund though, I am willing to make an exception. The reason for this is that everything in this fund has an explicit or implicit link to the United States government. Realistically, problems with any individual issuer whose securities represent a large position in this fund’s portfolio will reverberate throughout the entire U.S. (and possibly the global) economy. In short, it will not matter what any individual investor has in their portfolio, they will be affected by such an event. Therefore, diversification would not help at all and even investors who do not own shares of this fund will be affected by any problems with the assets in the portfolio. Thus, the fact that this fund is very concentrated in bonds issued by only a few entities is fine, even for those investors who want to limit their own risks.

Risks And Reasons For The Sell Rating

As we have already established, the BlackRock Income Trust appears to be about as free from default risks as is reasonably possible to achieve. That does not mean that this fund is completely free from risks, however. The biggest risk surrounding the fund’s assets and share price is the interest-rate risk.

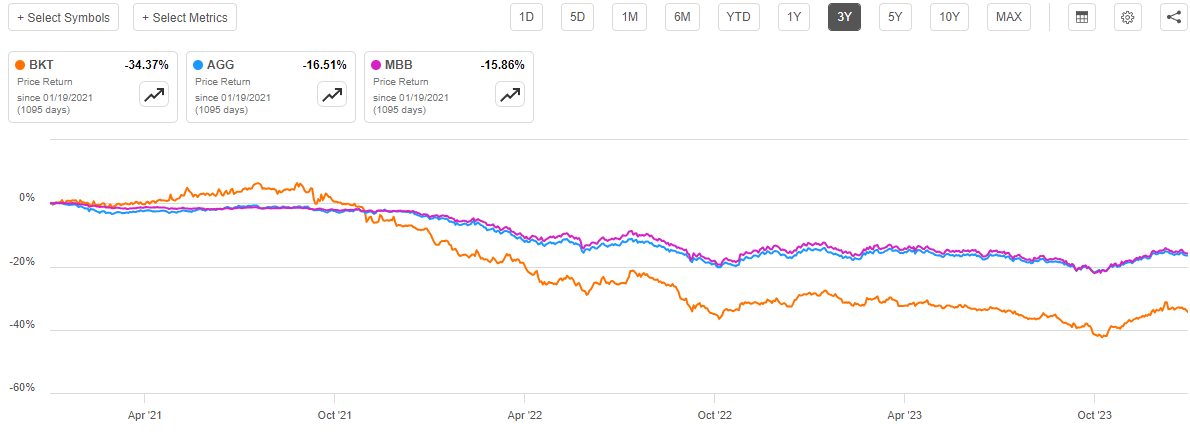

As everyone reading this is likely well aware, bond prices move inversely to interest rates. When interest rates go up, bond prices go down and vice versa. The fund’s share price will typically move with bond prices because the share price performance of closed-end funds usually bears some correlation to the value of the assets in the fund’s portfolio. This is the reason why the price performance of this fund has been so dismal over the past few years. As we can see here, the fund’s shares are down 34.37% over the past three years. This is substantially worse than the 16.51% decline of the Bloomberg U.S. Aggregate Bond Index and the 15.86% decline of the iShares MBS ETF:

{kind=link}

The reason why this fund has underperformed to such a degree is because of its use of leverage. The important thing to see right now is that the fund’s share price declined over the trailing three-year period. That is due to the fact that interest rates rose over the period as the Federal Reserve tried to scale back on monetary expansion and combat the high inflation rates that we have seen in the post-pandemic period.

The fund’s performance over the past few months has been much better, though. Long-term interest rates in the current cycle peaked in mid-October 2023 and then started to decline. Naturally, bond prices have been rising since that peak and have pulled up the fund’s shares with them. The shares of the BlackRock Income Trust are up 12.54% since October 20, 2023. That is much more than either of the indices:

{kind=link}

The fact that the fund’s share price outperformed both indices is not surprising for the same reason that it underperformed during times of falling bond prices. The fund’s use of leverage amplifies its movements in either direction. This is important when we consider the reason why interest rates have been declining.

Long-term interest rates are set by the market, not the Federal Reserve. The federal funds rate, which is the only interest rate that is officially determined by the central bank, has not changed since July 2023. As we can see here, the effective federal funds rate was rising until mid-year and has remained flat since then:

{kind=link}

The market expects that the Federal Reserve will shortly pivot its monetary policy and begin rapidly cutting rates. It currently believes that the Federal Reserve will reduce the federal funds rate six times in 2024 beginning with the March meeting of the Federal Open Market Committee. In accordance with this belief, market participants have been buying up long-dated bonds, which causes the price to rise and yield to decline.

However, there is a very real chance that the market is wrong about the probability of rate cuts by the Federal Reserve this year. For example, last week, Federal Reserve Governor Chris Waller stated that the central bank may cut rates three times in 2024, not six times like the market has priced into bonds. That alone suggests that the bonds held by the BlackRock Income Trust are probably overpriced.

Mr. Waller also strongly implied that the first rate cut will not be in March:

When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully.

With economic activity and labor markets in good shape and inflation coming down gradually to 2%, I see no reason to move as quickly or cut as rapidly as in the past.

In other words, Mr. Waller’s comments suggest that recent economic data has been too strong to support the idea of an interest rate cut in March. The Federal Open Market Committee only has six meetings in 2024 after the March meeting, so if there is no cut in March it becomes exceedingly difficult to make a case for six interest rate cuts in 2024.

This is especially true when we consider that the most recent inflation report came in hotter than the economists expected, and it showed that inflation is still a long way from the Federal Reserve’s target level. As such, a March rate cut could cause inflation to take off again and force the Federal Reserve to pivot once again and raise rates in 2024. It would make much more sense for the central bank to simply hold rates where they are for a while and see what happens.

This all strongly suggests that shares of the BlackRock Income Trust are likely to decline over the next few months. We have started to see that, as shares are down over the past five days, but they still look likely to continue to decline as the market still has more rate cuts priced in than we are actually likely to see. As such, it makes sense to sell some of your position in this fund today and then wait to buy back in later in the year after the shares have corrected.

Leverage

As mentioned earlier in this article, the BlackRock Income Trust employs leverage as a method of boosting its yield beyond that possessed by any of the assets in the fund’s portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase agency-backed residential mortgage-backed securities. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case. Unfortunately, this strategy is less effective today with borrowing rates at 6% than it was a few years ago when borrowing rates were close to 0%. This is because the difference between the interest rate that the fund has to pay and the yield on the purchased securities is much narrower than it once was.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for that reason.

As of the time of writing, the BlackRock Income Trust has leveraged assets comprising 31.29% of its total assets. This is quite a bit higher than the 30.11% leverage that the fund had the last time that we discussed it, which is concerning. The fund’s net asset value is up 0.16% since the date that the previous article was published (far less than the share price gain), so the fund must have borrowed more money. That suggests that it has actually increased its vulnerability to a market correction over the past few months, which is exactly what we do not want to see.

With that said, the fund’s leverage is still not unreasonable, and it does compare fairly well to other fixed-income funds. We should not need to worry about its leverage too much, but we still need to watch it closely as we do not want further increases in leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BlackRock Income Trust is to provide its investors with a very high level of current income. In order to achieve this objective, the fund invests in a portfolio of mortgage-backed securities issued by government-sponsored enterprises that should have no risk of default. This is a very interesting choice because these bonds are going to have lower yields than junk bonds or similar securities that do have an inherent risk of default-related losses. The fund employs leverage to collect payments from more securities than it could otherwise control, boosting the effective yield of the portfolio, but we would still expect this fund to have a somewhat lower yield than most other fixed-income funds.

However, this is not the case. The BlackRock Income Trust currently pays a monthly distribution of $0.0882 per share ($1.0584 per share annually), which gives the fund an 8.80% yield at the current price. This is a comparable yield to that possessed by the highest-yielding junk bond funds, which is very surprising. The fund has unfortunately not been especially consistent with its distribution though, as it has both raised it and cut it many times over its history:

{kind=link}

The fact that this fund’s distribution has varied quite a bit over time might prove to be a turn-off for those investors who are seeking to earn a safe and secure income from the assets in their portfolios. However, it is very common for a fixed-income fund to vary its distributions over time because the returns that these funds are able to obtain from the market are highly dependent on interest rates as well as the willingness of investors to take risks. These factors are both entirely out of the fund’s control. The fact that the distribution has varied over time is still disappointing though because the recent high levels of inflation have resulted in everybody needing more income to sustain the same standard of living that they had prior to the pandemic. Unless the fund constantly increases its distribution, it does not really provide a rising income unless investors reinvest some of the distributions that the fund pays out. This might not always be possible, depending on how much income a given individual requires.

As I have pointed out numerous times in the past though, the fund’s past history is not always the most important thing for us to consider. After all, anyone who purchases the fund’s shares today will receive the current distribution and the current yield and will be completely unaffected by actions that the fund has taken in the past. Therefore, the most important thing for our purposes today is how well the fund can sustain its current distribution. Let us investigate this.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. As such, this report will not include any information about the fund’s performance over the past seven months. That is certainly disappointing, as we have seen two wildly disparate markets in the intervening period, as bonds were generally experiencing a bear market over the summer but a bull market during the last three months of 2023. However, this is still a more recent report than the one that we had available to us the last time that we discussed the fund so the updated information will be useful for our analysis of the fund’s sustainability. After all, this fund has not cut its distribution since 2022 so an updated analysis of how well it is covering the current payout is always welcome.

During the six-month period, the BlackRock Income Trust received $141,813 in dividends along with $7,799,514 in interest from the assets in its portfolio. This gives the fund a total investment income of $7,941,327 over the period. The fund paid its expenses out of this amount, which left it with $3,705,331 available for shareholders. As might be expected, that was nowhere near enough to cover the fund’s distributions during the period. The BlackRock Income Trust paid a total of $11,275,720 to its shareholders over the six-month period. At first glance, this is likely to be very concerning since we would usually prefer a fixed-income closed-end fund to fully cover its distributions with its net investment income. This fund obviously failed to accomplish that during the period.

Fortunately, there are other methods through which the fund can obtain the money that it needs to cover the distributions. For example, it might be able to exploit the fact that the price of bonds changes with interest rates to earn some trading profits. These are realized capital gains, which are not considered to be investment income for tax or accounting purposes, but they still clearly represent money coming into the fund that can be distributed to its investors.

Unfortunately, the fund had mixed success at this task during the period in question. The fund reported net realized losses of $14,526,815 but was able to offset this with $14,579,268 in net unrealized gains. Overall, the fund’s net assets declined by $7,472,490 after accounting for all gains and losses during the six-month period. Thus, this fund clearly failed to completely cover its distributions during the period. This is certainly concerning, particularly the fund also failed to cover its distributions during the full-year 2022 period. The fund’s net asset value has declined 2.51% since June 30, 2023, as well, so even the year-end rally in the bond market was not sufficient to ensure that this fund was able to cover its distribution during the second half of the year. Investors who are concerned about risks will undoubtedly be worried here as the fund may be forced to cut its distributions in the near future simply to avoid destroying its own asset base.

Valuation

As of January 18, 2024 (the most recent date for which data is available as of the time of writing), the BlackRock Income Trust has a net asset value of $12.43 per share but the shares only trade for $12.03 each. This gives the fund’s shares a 3.22% discount on net asset value at the current price. That is a bit more expensive than the 4.40% discount that the shares have had on average over the past month, but it could work reasonably well as a price to pare back your positions.

Conclusion

In conclusion, the BlackRock Income Trust is one of the most conservative ways to earn a very high yield today as the fund’s portfolio is invested mostly in U.S. government-related mortgage-backed securities. These are about as safe as we can get without buying Treasuries. Unfortunately, the fund does still have interest-rate risk, and this could be a problem right now as the market is probably too optimistic about the near-term trajectory for interest rates. As such, the shares might be overpriced and vulnerable to a correction. In addition, the fund is consistently failing to cover its distribution and might have to cut the payout in the near future. For these two reasons, investors might want to consider paring back their positions and reducing some risk by taking money off of the table.

For further details see:

BKT: Vulnerable To A Correction And Distribution Cut (Rating Downgrade)