BKT - BKT: It Is Time To Buy Agency MBS Bonds

2023-05-28 06:06:46 ET

Summary

- BlackRock Income Trust is a fixed income closed end fund.

- BKT focuses on buying AAA Agency MBS bonds and leverages them up to enhance profits.

- The CEF does not have a fixed leverage cost structure and has not seen its distribution coverage balloon as rates have moved up.

- We feel lower prepayment rates on mortgages are now priced in, and we are going to see peak rates this summer.

- This CEF is the leveraged structure of the very similar vanilla ETF MBB.

Thesis

BlackRock Income Trust ( BKT ) is a fixed income closed end fund. The vehicle buys AAA Agency MBS securities and leverages them up to enhance the yield paid to investors. We have covered this name before, with the fund down over -4.5% on a total return basis since we highlighted that the asset class will continue to be under pressure:

Performance (Seeking Alpha)

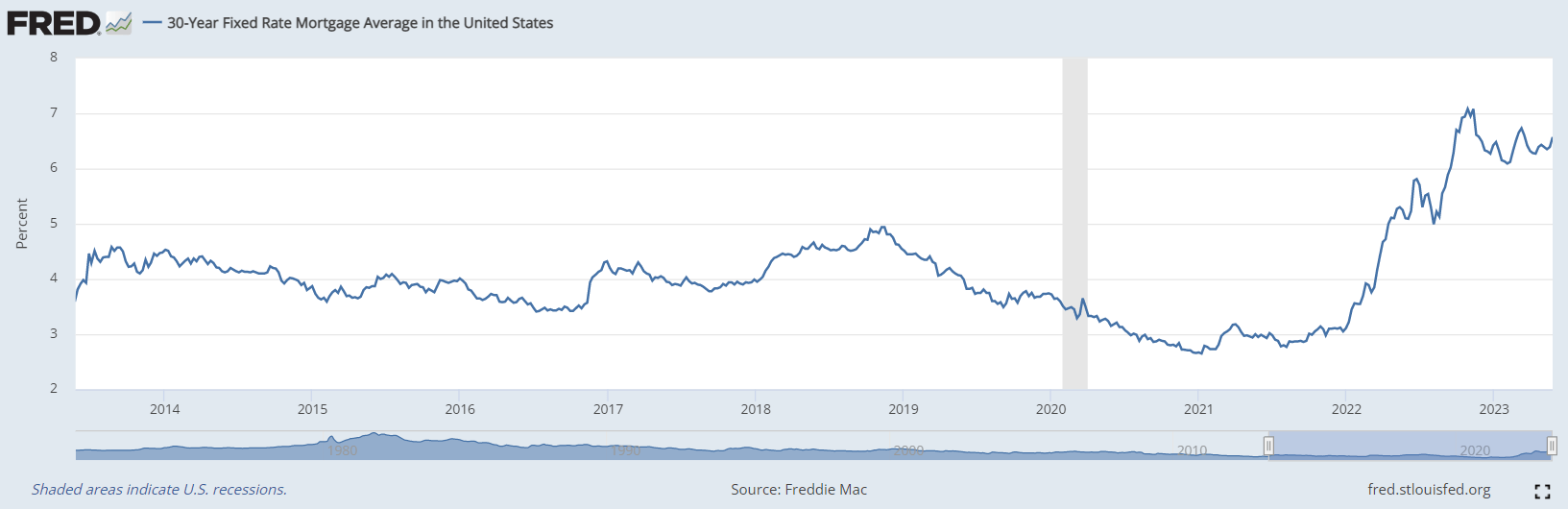

At the time of our last article covering this name (September 2022) the Fed was not even close to being done hiking rates, and the quantitative tightening program was just starting. Almost ten months later, we are in a completely different spot in the economic cycle. We are of the opinion that we might have seen the last hike by the Fed, and although we do not expect a pivot this year, we see this summer as peak rates for the cycle. Mortgage rates have also been on a long journey that has seen 7% being breached:

{kind=link}

Market timing is impossible, but an informed reader should have a look at how long-term rates have done in the past decade. Is today's level the top? We are unsure. We are quite confident though that 2024 will bring lower rates, and investors will look back on 2023 as the 'year of the bond', when fixed income purchases should have been made.

BKT is by no means an immaculate CEF (we are going to discuss this further in the article), but it is a nice clean way to express a view on Agency MBS bonds. The famous mREITs (NLY, AGNC, CIM, etc.) do a similar business but in a more complex and leveraged fashion. BKT just buys Agency mortgages, leverages them up and passes the return to you. There are no other hedges or complexities in this business model. The fund has been hurt by its high financing costs (many repos that adjust to market pricing), but will benefit from an increasing NAV during a lower rates environment.

In essence BKT is a leveraged way of purchasing Agency MBS bonds. If an investor thinks we are close to a peak for this asset class from a rates perspective, then BKT is a good vehicle to express that view. Its ETF cousin is the iShares MBS ETF ( MBB ), but since the ETF does not have any leverage that fund will not have the same return profile during a decreasing rates environment.

Holdings

The fund holds exclusively Agency mortgages:

Holdings (Fund Fact Sheet)

All underlying assets are AAA rated, and the vehicle is subject to rates and pre-payment risk only. We feel the underlying asset class has now embedded the slower prepayment risk in the underlying cash-flows, and this is reflected in the fund's duration profile:

Duration (Fund Fact Sheet)

Premium/Discount to NAV

The CEF is now trading at a discount to net asset value, but is back in its usual historic range:

Outside the zero rates environment witnessed in 2020/2021, the CEF was trading at slight discounts to net asset value. It reverted to a significant premium as there was a general push for yield by the investor community. It is back to a 'normal' discount at the moment.

Distributions

We mentioned in the 'Thesis' section of the article that this CEF is not 'immaculate'. What we meant there is that the structure did not lock in funding via preferred shares or a cheap long term Repo structure, and as a result is paying a high funding amount:

{kind=link}

A high cost of funds translates into an unsupported dividend yield. However, even if the fund fails to generate a current carry profile, it will benefit from the sudden capital gains associated with the underlying securities when the time comes. And those gains will be reflected in a higher NAV for the entire fund as assets get valued daily.

Conclusion

BKT is a fixed income CEF that focuses on Agency MBS bonds with a 30% leverage ratio. BKT is the CEF expression of the unleveraged ETF ( MBB ), and an informed reader can see their close correlation throughout time. Agency MBS bonds have a basis to Treasuries of the same maturity profile, being priced wider from a yield perspective. We believe we are about to have peak rates this summer, hence peak Agency yields as well. BKT's structure does not have a fixed rate funding rate, hence the fund was not able to fully profit from rising rates. From that angle we can see that the CEF is using a high amount of ROC to cover its dividend (if its funding would have been fixed the CEF would have had improved coverage as rates rose). We view this structure as a play on lower yields in Agency MBS bonds next year. There will be a significant NAV accretion when rates go down and bond prices go up. When we look at BKT we feel it is time to start Buying this name.

For further details see:

BKT: It Is Time To Buy Agency MBS Bonds