BDTX - Black Diamond Therapeutics: MasterKey Approach Validated With Lung Cancer Update

2023-08-03 08:53:34 ET

Summary

- Shares have risen by 94% so far in 2023 but have lost over three-quarters of their value since IPO at $19 in 2020.

- There is a clear unmet need in 2L NSCLC space post osimertinib, with a $500M+ opportunity contrasting favorably to the $75M enterprise value.

- BDTX-1535 data update showed RECIST responses in heavily pretreated patients coupled with ctDNA reductions in relevant driver mutations.

- Bear thesis is that future updates will disappoint (particularly durability), the competitive landscape is rapidly evolving and the FDA might not allow for an accelerated approval pathway.

- BDTX is a Buy. I see a pathway to value creation via 2024 expansion cohort updates in focused patient populations for BDTX-1535 as well as initial data for the RAF program.

Shares of precision cancer medicine developer Black Diamond Therapeutics ( BDTX ) have lost over three-quarters of their value since IPO was priced at $19 in 2020. However, they are up 94% so far in 2023 after the company posted a positive data update in June for lead drug candidate BDTX-1535 in advanced non-small cell lunger cancer patients.

When the news came out, I thought that a continuation move higher was likely but the stock seemed more appropriate for swing traders with risk tolerance for such speculative names. After all, the company was competing in a heavily crowded space (EGFRm lung cancer) where I doubted a smaller player would be able to carve out a niche (much less bring a better solution to the table than its larger peers).

Surprisingly, after listening to the interim results webcast , I came away with the conclusion that BDTX-1535 presents a unique solution to a complex problem for cancer patients who've failed treatment with standard of care osimertinib (Tagrisso). Additionally, there's a potential line-agnostic path to market in patients with intrinsic drivers and Black Diamond's MasterKey approach is replicable in other targets with high unmet need.

Given the above, I chose to purchase a pilot position (currently down 25% in the interest of transparency) and bring this story to readers' attention.

Chart

{kind=link}

Figure 1: BDTX weekly chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, we can see an ugly gap down in May 2021 after data update for then lead candidate BDTX-189 failed to impress. High rates of diarrhea, vomiting and nausea (predominantly Grade 1 or 2) along with ALT increase (can indicate damage to liver) made for an uncompetitive profile. One of 3 patients with EGFR exon 20 mutation had a RECIST response, 3 HER2 exon 20 patients had stable disease and 1 of 6 patients with HER2 amplification responded. Unsurprisingly, this program was discontinued in April 2022 ("due to evolution of EGFR HER2 exon 20 landscape") which left the stock in the penalty box for much of the past year.

Conversely, in the daily chart below we can see share price spike to $7 on recent data update for BDTX-1535. From there, the stock has pulled back to mid $3s (think it's bearish that the secondary offering price point of $5 did not hold, though to be fair it could in part be related to the doldrums the biotech sector is currently experiencing).

{kind=link}

Figure 2: BDTX daily chart

On the whole, my take is that for investors interested in this name, gaining initial exposure in the current range is a logical action ahead of Q4 2023 phase 1 data update and progress in 2024 for expansion cohorts.

Overview

Founded in 2017 with headquarters in Cambridge (65 employees), Black Diamond Therapeutics currently sports enterprise value of ~$75M and pro forma cash position of $175M providing them operational runway into 2025.

There are ~54M shares outstanding out of 500M authorized. Accumulated deficit to date is $355M.

The company's strategy centers on the precision oncology space via discovery and development of novel MasterKey therapies (targeting families of oncogenic mutations in patients with genetically defined cancers, per 10-K filing ). Black Diamond's "special sauce" if you will is its Mutation-Allostery-Pharmacology (MAP) discovery engine which allows them to analyze genetic sequencing data to discover the oncogenic mutations they can in turn inhibit with MasterKey therapies. The bottom line in terms of clinical differentiation with this approach is it supposedly enables them to target a greater number of patients across these genetically defined tumors (broaden the market opportunity).

The company seeks to do this across several programs (EGFR, BRAF, FGFR3) as seen below, but for the purposes of our thesis I will be focusing on EGFR given validation provided by recent phase 1 data.

{kind=link}

Figure 3: Pipeline

BDTX-1535 is a brain penetrant, mutant selective, irreversible EGFR MasterKey inhibitor in clinical studies for lung cancer (NSCLC) and brain cancer ((GBM)). For those unfamiliar with the EGFR landscape, inhibitors of this target provide substantial patient benefit and are first line-standard of care (osimertinib which does $6B in sales annually). Unfortunately, most patients eventually acquire resistance and relapse (hence the unmet need). Also, up to half of them develop CNS metastases either at diagnosis or while on treatment (contributes to increased resistance and poor prognosis, see 10-K filing ). To be fair, current standard of care osimertinib does have some CNS penetration but is still far from ideal.

Moving on to GBM, as I understand it this is one of the most dreaded diagnosis for a clinician to give, where prognosis remains poor despite surgical resection followed by radiation and chemo (current standard of care). Only a quarter of newly diagnosed patients survive 2 years or longer and up to 50% of GBM tumors express one or more EGFR oncogenic alterations. So far, EGFR therapies have been unsuccessful in this space due to varied alterations and low levels of brain penetration, among other factors. At least theoretically, one would think that given its differentiated drug profile BDTX-1535 would have a shot here (expectations remain low).

Building on this theme of targeting a wide variety of mutations with MasterKey inhibitors to broaden the market opportunity, the company aims to repeat this blueprint in RAF with BDTX-4933 targeting oncogenic BRAF Class I, II, III and activated RAF dimers in the setting of RAS mutations. Here as well, the company will build on the success of predecessors (current drugs target V600E Class I mutations in melanoma and other solid tumors) by pursuing Class II and III mutations for which there are no approved therapies. Also, much like in EGFR, all classes of BRAF mutations commonly occur in patients with CNS tumors or brain metastasis and current drugs have poor CNS penetration (also unwanted paradoxical activation leads to poor efficacy, secondary malignancies and undesired adverse events, see 10-K filing ).

Corporate Slides

Figure 4: Unmet need in RAF space

Lastly, to round out the pipeline the company has preclinical programs in FGFR and an undisclosed target (for competitive reasons I assume) that could enter the clinic in the 2024 to 2025 timeframe.

Focusing on the EGFR Data

I hope readers will forgive my rather brief overview above, as I felt that the majority of questions surrounding Black Diamond's platform, technology and value proposition are better addressed by the actual clinical data along with management and KOL commentary ( see webcast on interim results here) :

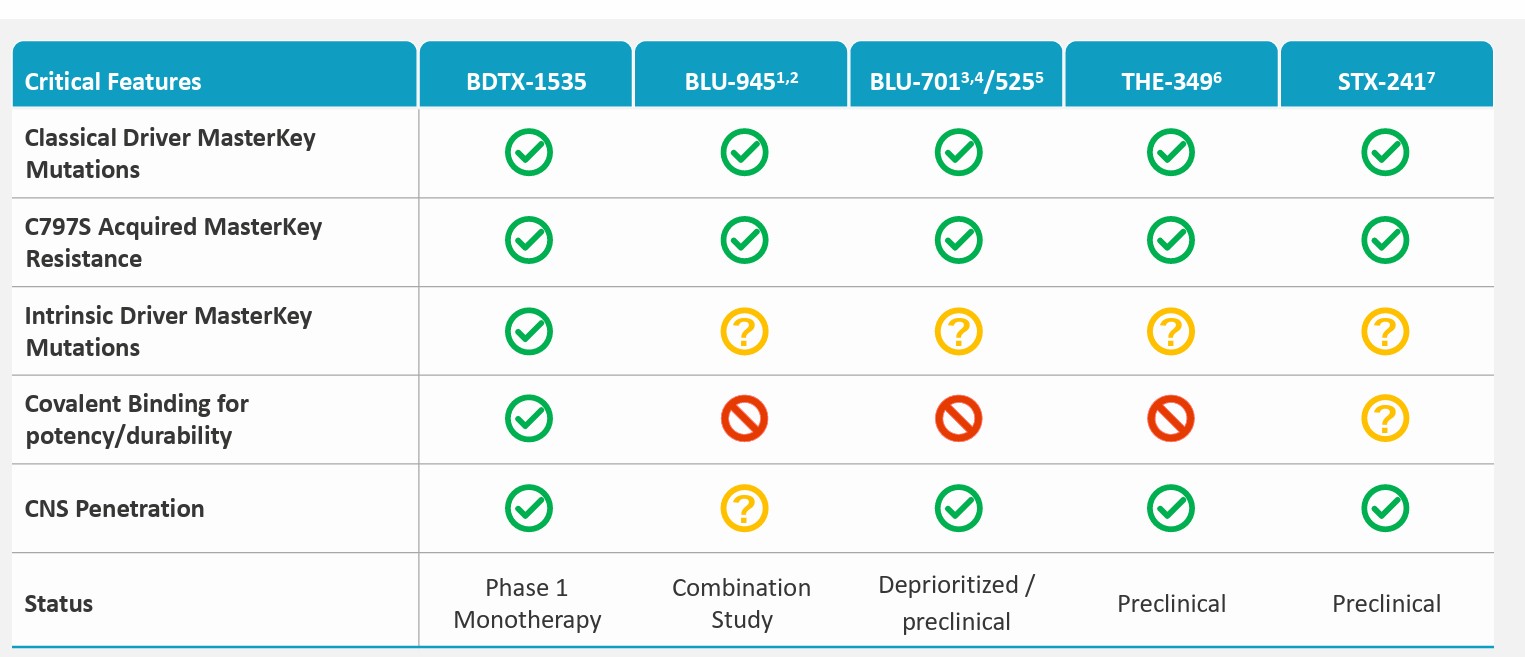

- CEO notes that the 2nd line post-osimertinib space is a key unmet need in the lung cancer space. There are no targeted therapies for the C797S resistance mutation. There are no targeted therapies for these other complex EGFR mutations, so BDTX-1535 could become the first 4th generation EGFR TKI to enter this space.

{kind=link}

Figure 5: Competitive landscape in next-gen EGFR space

- From a patient perspective (not to mention their physicians), we can see how an oral therapy uniquely tailored for their tumor would be an appealing alternative (delay use of chemo and other alternatives with significant side effects). Also, many patients have brain metastases and BDTX-1535 has high brain penetration which may provide benefit for them as well. There is also an unmet need in newly diagnosed patients with intrinsic driver mutations (BDTX-1535 could be a first-line option for them based on their tumor mutation profile).

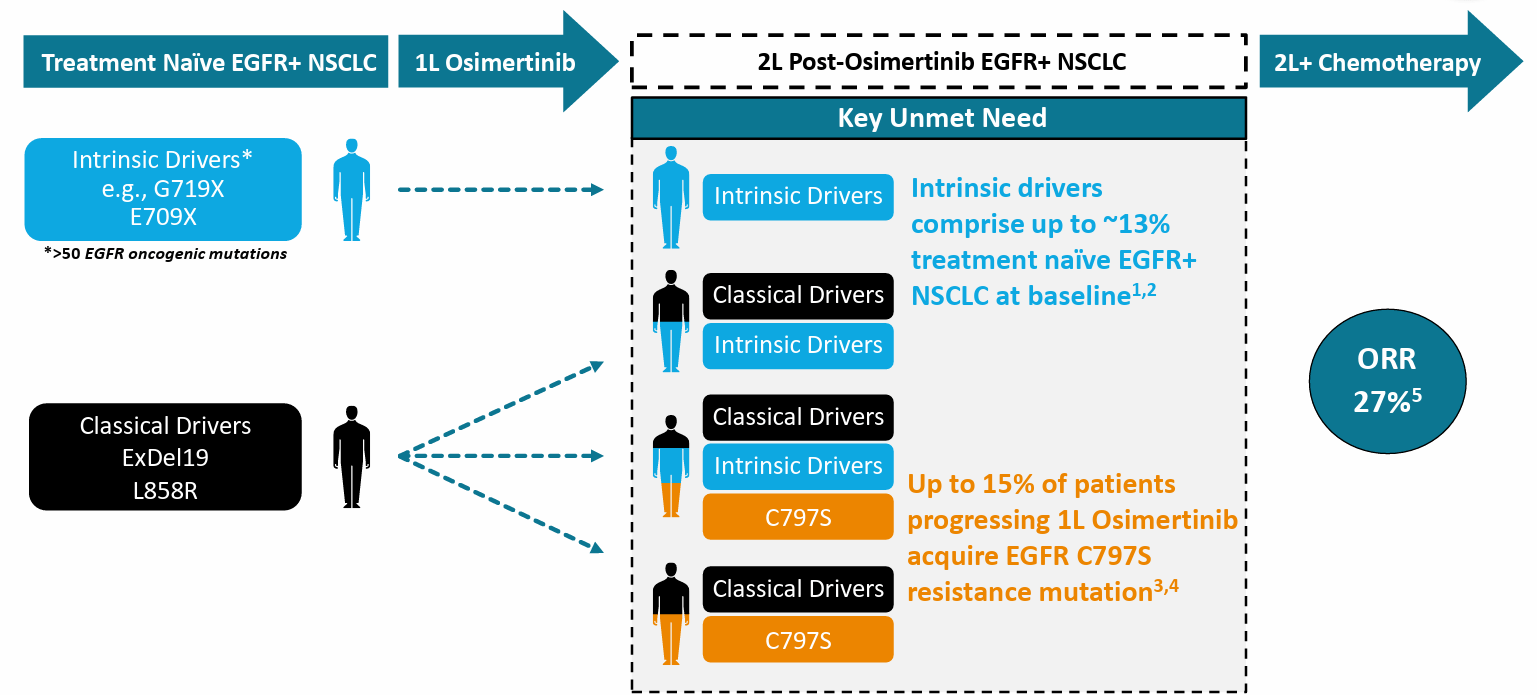

- June's data update clearly demonstrated clinical POC (proof-of-concept) with confirmed anti-tumor activity in all EGFR mutant MasterKey families. Again, the intended objective is to pursue the 2nd line NSCLC market by targeting the landscape of mutations that occur after treatment with approved 3rd generation TKIs such as osimertinib.

{kind=link}

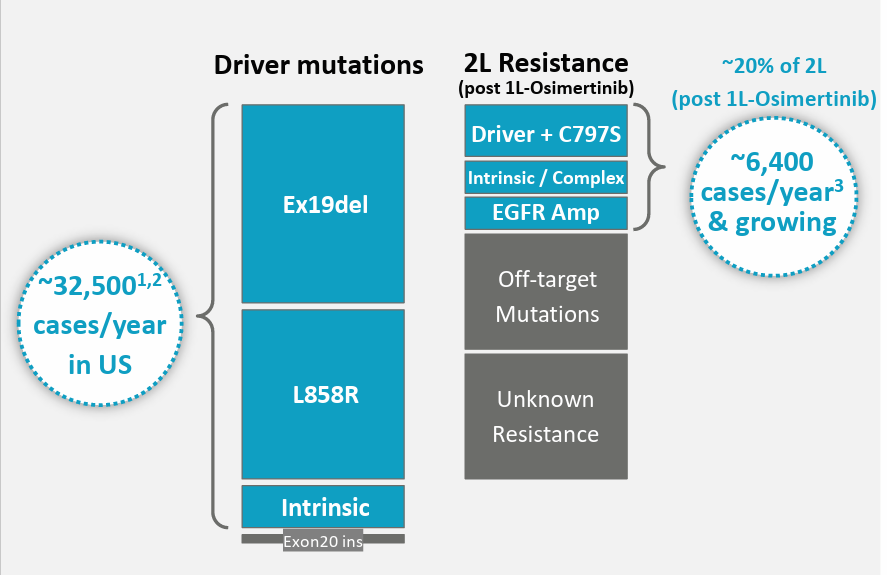

Figure 6: Key unmet need in 2L NSCLC space

- Other important readthroughs from the data (including genetic sequencing) confirm that these MasterKey mutation families do in fact arise after treatment with osimertinib as predicted in real world data. Patients who responded to BDTX-1535 harbored a wide variety of EGFR mutations. Data also indicates that 2L lung cancer is comprised of a very large group of EGFR mutant patients and is a much larger addressable patient population than would be predicted for the group harboring C797S mutation alone.

- The company provided PK data from all 51 GBM (glioblastoma) and lung cancer patients that were treated. Focusing on the 24 patients comprising NSCLC cohort, dose linear PK and confirmed target coverage was confirmed at the once daily dose with "manageable safety profile" (color me skeptical every time I hear that phrase). Radiographic responses were observed in lung and also in patients with CNS metastasis, supported by ctDNA results which confirmed loss of driver and resistance alleles at therapeutically active doses. Again, key part of thesis is the larger market opportunity than originally thought as clinical activity was observed across both acquired and intrinsic mutation families (has the effect of increasing the addressable population for BDTX-1535). For patients treated with Gen3 EGFR drugs like osimertinib, there's a 25% chance of developing one of 50 acquired or intrinsic resistance EGFR mutations (from there they make the decision to try various rounds of checkpoint inhibitor or chemotherapy).

- KOL notes that the profile of BDTX-1535 is ideal for such opportunities, as it potently targets these mutations while sparing on target inhibition of wild type EGFR to deliver a favorable safety profile. Covalent mode of binding achieves durable target engagement.

- A mini crash course in the treatment landscape for EGFRm NSCLC was helpful, with a fun fact being that the founders of Black Diamond Therapeutics (and other members of leadership) participated in the approval of first generation of reversible EGFR inhibitors with Tarceva 20 years ago. The presence of T790M mutation (acquired resistance to those therapies) led to the development of osimertinib as the frontline agent of choice. Molecular landscape continues to evolve in EGFR as thanks to osimertinib the T790M mutation has all but disappeared. Now, we are seeing the emergence of a whole new group of drug resistance mutations including C797S (landscape is maturing through use of next generation sequencing which in turn revealed additional mutations known as intrinsic drivers). BDTX-1535 targets multiple groups of mutations including classical (Ex19del, L858R) but also intrinsic oncogenic driver mutations not well covered by osimertinib as well as groups of mutations that mediate acquired resistance to osimertinib therapy (including C797S). Management believes 1535 has all the attributes one would want for a best-in-class 4th gen EGFR TKI (see Figure 4 above) and key competitors are behind in preclinical (Thesus Pharmaceuticals and Scorpion Therapeutics).

- The other key aspect of data's relevance to our thesis is that it validates the company's MasterKey approach to targeting multiple families of mutations with one drug (can now repeat this success with other high value targets).

- As for today's landscape, KOL notes that the majority of EGFR NSCLC patients have classical driver mutations for which osimertinib is approved. Up to 13% of them have intrinsic drivers that osimertinib does not address, and as patients progress on therapy the landscape becomes even more complicated (up to 15% of patients with C797S resistance mutations, others have complex mix of mutations). BDTX-1535 could make things more simple given it has the potential to treat a broad spectrum of these mutations appearing after osimertinib.

- Chemo is the go-to option for patients progressing on osimertinib, with 27% ORR (why high unmet need remains as there are currently NO targeted therapies for this diverse spectrum of EGFR mutations). Afatinib is also used off label (covers 3 such mutations) but has severe tolerability issues.

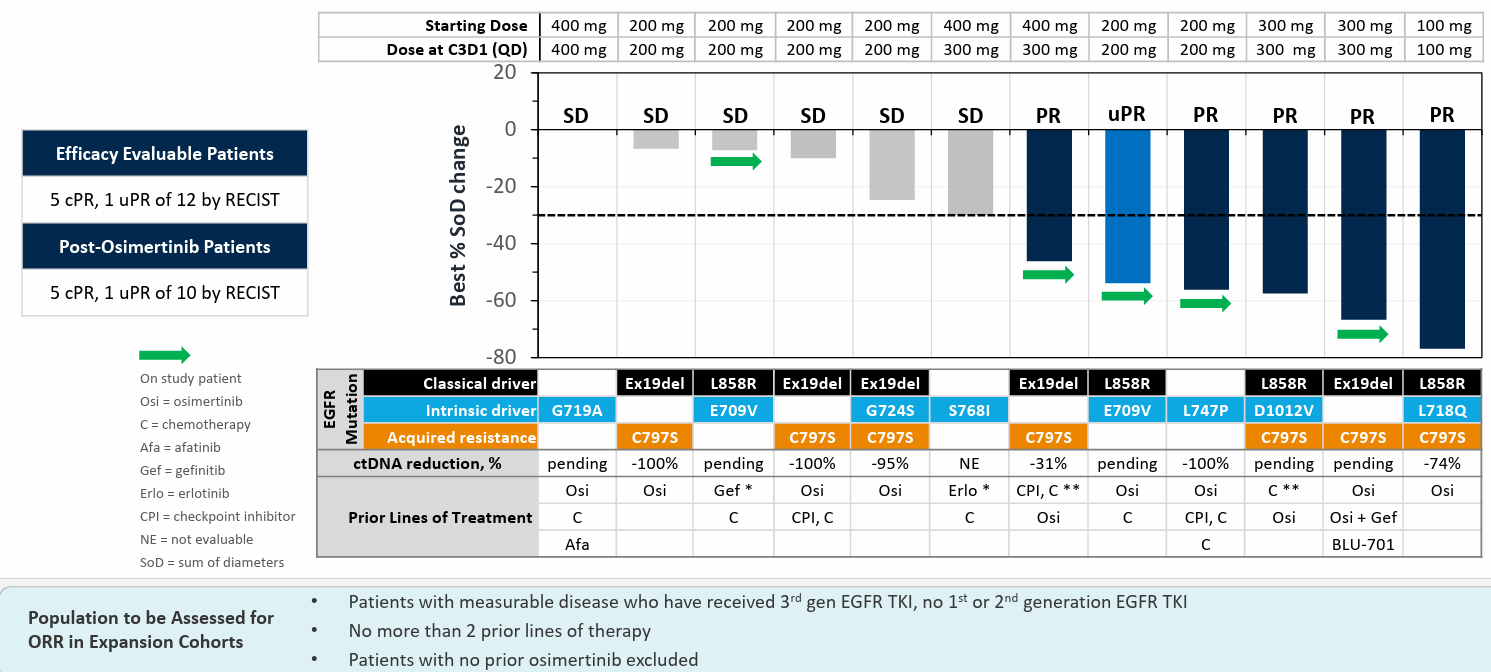

- Moving on to the actual data, one devil's advocate point is that there's no mention of durability at first. Also, while 24 lung cancer patients were treated, the company focused on the subgroup of 12 patients most resembling their target population to be enrolled in expansion cohorts. Here, 5 of 12 responded (41% ORR) and a 6th could potentially be confirmed (6 remaining had stable disease). Company is transitioning from capsule to tablet formulation and moving swiftly into expansion cohorts (seems like accelerated approval is a distinct possibility, though I remain skeptical). Again, the 41% ORR gives is an idea of what ORR could look like in future cohorts (could even improve as these were later line patients whereas target population is 2nd line after osimertinib). NSCLC patients were heavily pretreated with median 2 prior therapies (ranging from 1 to 9) and two-thirds received prior chemo. ALL 24 NSCLC patients received prior EGFR TKI treatment with osimertinib used in 19 of them. Dose limiting toxicities were observed at 400mg dose driven by EGFR WT effect (clinical activity seen at 100mg to 300mg doses). They will discuss phase 2 strategy with FDA later this year (keep in mind that Project Optimus has them shifting away from MTD or maximum tolerated dose strategy).

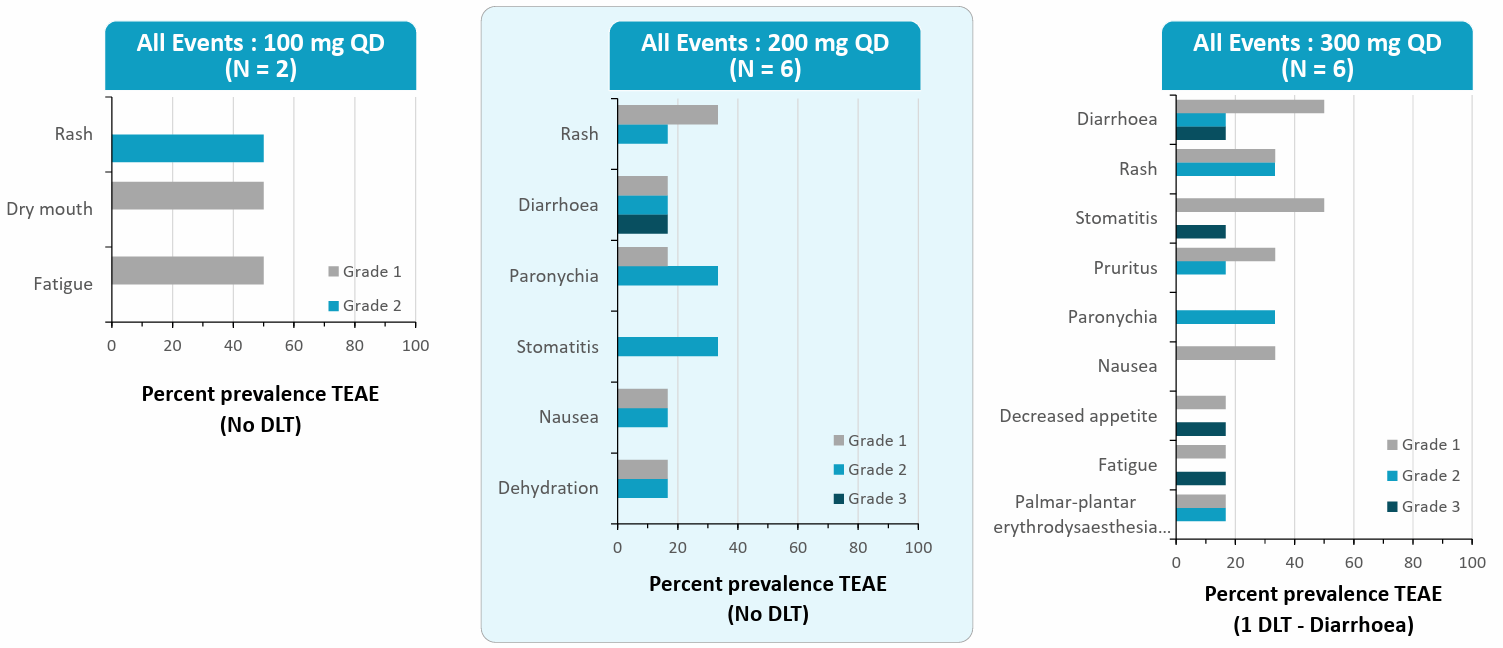

- As for the key issue of safety, the most common adverse event was rash (60% to 80%), diarrhea (20% to 50%), stomatitis (0% to 40%) across the 100mg to 300mg dose range with majority of cases being mild to moderate (similar across GBM and NSCLC). 2 DLTs occurred at 400mg dose. While I don't like these instances of rash or diarrhea, management contends that they are similar to osimertinib which sports 58% rate of rash and diarrhea in the FLAURA study.

{kind=link}

Figure 7: Adverse event profile for BDTX-1535

- 200mg dose seems like it could be the sweet spot and was suggested by trial investigators to be evaluated in upcoming expansion cohorts (ORR as primary endpoint). Again, despite the above rates of rash, diarrhea and other events, it's telling that there were no discontinuations due to adverse events (there was just 1 grade 3 case of diarrhea, managed with standard measures). Again, profile was similar to osimertinib data in frontline FLAURA trial.

- For the 12 efficacy evaluable patients they focused on, these were started at 100mg to 400mg and allowed to dose reduce to adverse events or escalate if well tolerated. 6 patients had target lesion reductions exceeding 30% with 5 of 6 confirmed (4 of these still on treatment). ctDNA reductions were predictive of clinical radiographic benefit. 10 of 12 patients received prior osimertinib and the majority received 2 to 2 lines of chemo. Durability remains a key devil's advocate point as management states it's too early to comment and they kick the can down the road (accurate look at durability will come from expansion cohorts in more focused, earlier line patient population). Also, the "slice and dice" approach to presenting optimal patient responses leaves burden of proof on future updates and especially full expansion cohort data.

{kind=link}

Figure 8: RECIST responses in evaluable patients with a variety of driver and resistance mutations

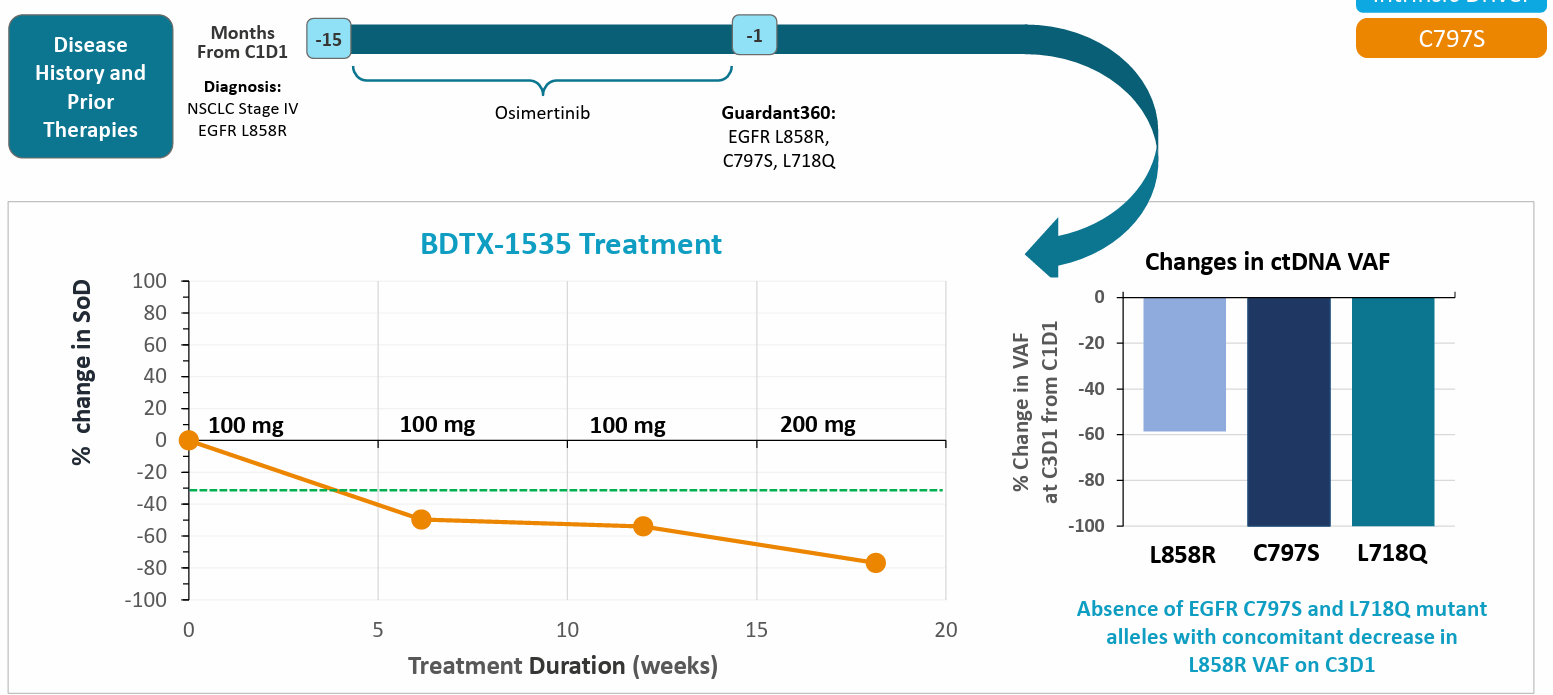

- I take case studies with a big grain of skepticism, but the totality of evidence seemed quite convincing. For one patient with C797S mutation, ctDNA analysis showed complete elimination of this and L718Q mutation along with significant reduction in L858R (confirmed partial response in complex mutation case, neurological symptoms improved, reduction in CNS mets & groin metastasis indicative of systemic and brain activity). Another patient's ctDNA showed complete eradication of L747P mutation (intrinsic driver), another showed complete eradication of both C797S and Exon19del driver which had persisted. Another very heavily pretreated patient was on BLU-701 for 2 months, partial response on BDTX-1535 let him get off oxygen and out of the wheelchair and go on vacation in France. One last patient was not included in the waterfall plot due to absence of measurable disease in lung, but was quite beat up (past chemo, checkpoint, afatinib, radiation, osimertinib, HER3 ADC discontinued due to AEs) and had complex mutations (EGFR G719A and L861Q). 2 areas in brain and lung were growing, 50mg was tolerated well, escalated to 100mg and now on therapy for over 9 months with recent scans showing absence of tumor in brain and lung (complete response was quite striking).

{kind=link}

Figure 9: Supportive case study taking special note of ctDNA reductions in classical, intrinsic & resistance drivers

- From here, the goal is to open expansion cohorts in 2H 23 with primary objective of ORR (well established surrogate endpoint for accelerated approval in lung cancer). Only patients with measurable disease and no more than 2 prior therapies including 3rd gen EGFR TKI would be enrolled. One cohort would include patients with C797S resistance mutation while another would focus on those with intrinsic driver mutations. They will also discuss with the FDA the opportunity to open an expansion cohort in newly diagnosed patients with intrinsic driver mutations (could support line agnostic approval).

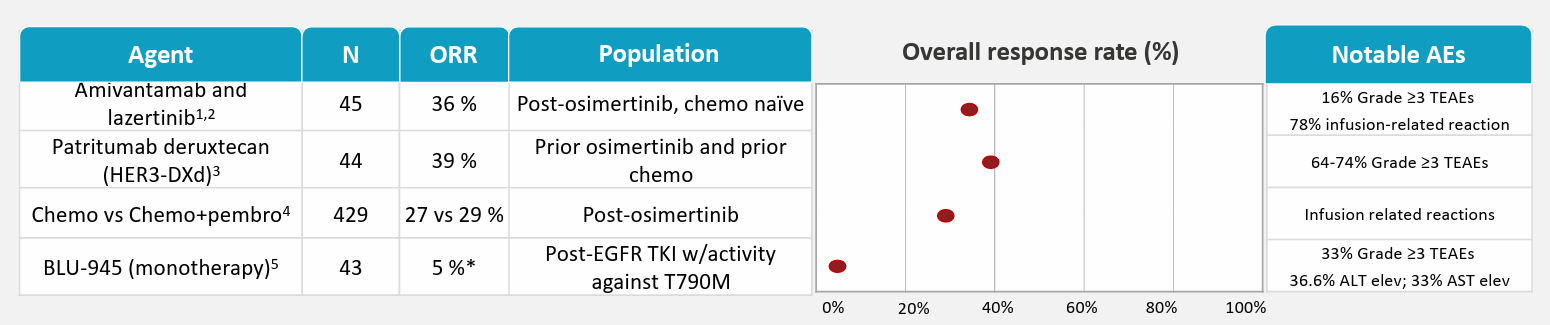

- As for competitor data (see table below), management highlights 27% ORR for chemo and 39% ORR for HER3 ADC (at the expense of over 60% Grade 3 or above adverse events). Amivantamab + lazertinib combo showed 36% ORR but 3/4 of patients have infusion reactions and BLU-945 showed less than 10% ORR. It would seem that IF the 41% ORR for BDTX-1535 holds up in expansion cohorts, it would be a highly competitive drug.

{kind=link}

Figure 10: Competitor data in patients with prior 3rd gen EGFR TKI

- KOL notes that post osimertinib setting is a wide open space and one of the highest areas of unmet need with the exception of lung cancer patients post IO (immunotherapy). Most patients get carboplatin or pemetrexed with response rates of 20% to 30% and PFS of 3 to 5 months (they do okay on chemo but would prefer another pill like osimertinib that works just as well and is tailored to their specific mutation). KOL notes that afatinib is more potent, but he often can't give it at the recommended phase 2 dose of 40mg and has to dose reduce due to bad rash or diarrhea.

- As for next steps, they will align with the FDA on expansion cohorts and go-forward dose. Additional data from end of phase 1 will be submitted to scientific conference later this year. Update on GBM cohort will be given in Q4 (since they mention it so little, I assume expectations are very low here).

- Moving on to Q&A, we are reminded that ctDNA markers are a well validated measure in the lung cancer space (correlate very well with clinical benefit). ctDNA reductions give management confidence that they are affecting the target mutation and validates the consistency of activity observed so far across various types of mutations including complex cases. Green flag is that data is internally consistent (so far). On the competitive landscape, an analyst notes that HER3 ADC and amivantamab are doing head-to-head trials against platinum chemo (so his take is that single arm studies are not likely to receive accelerated approval from the FDA). One comparison that helped me on the data is that for third-line patients, 10% to 12% ORR is historically observed for docetaxel and so in that light the 41% ORR for BDTX-1535 is even more promising in these late-stage patients. Up to half of these NSCLC patients have brain metastasis, making 1535's CNS penetration even more important in that light.

- On market opportunity, osimertinib is now the dominant EGFR inhibitor selling $6B annually. 1535 addresses the 13% of intrinsic mutations not covered, also the C797S mutation in up to 15% of that post osimertinib population. Real world evidence shows that ever since osimertinib was approved in 1st line, the number of patients with this resistance mutation have been increasing (from 7% of population to 11% to 15% in latest data cut in 2022, so I expect this to continue to increase). In the US alone, real world evidence points to 4,000 patients annually with intrinsic driver mutations and 6,000 with acquired resistance mutations C797S and other complex mutations.

- The company's MasterKey hypothesis (targeting families of similar mutations) appears to have been validated here with BDTX-1535 targeting up to 50 different mutations across acquired and intrinsic resistance. This greatly increases the overall addressable patient population and demonstrates the utility of broadening out the target product profile to cover as many mutations as possible.

Other Information

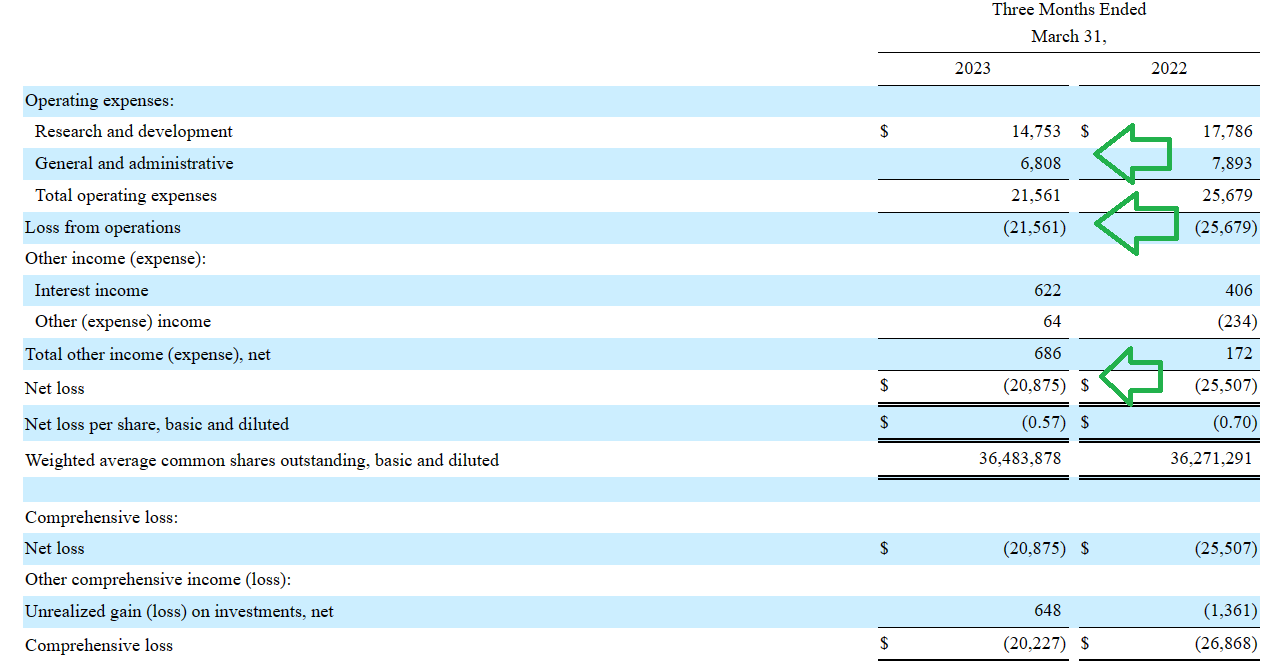

For the first quarter of 2023 , the company reported cash and equivalents of $103M (does not include proceeds of $75M from recent offering). This contrasts favorably to net loss of $21M, comprised of R&D expenses of $14.8M and G&A of $6.8M. At the time, management guided for operational runway into Q3 2024, so with the recent financing I imagine that's been extended to at least mid-2025. Conversely, let's not forget the ramp up in expenditures that will be required for expansion cohorts of BDTX-1535 not to mention RAF program moving forward into phase 1.

{kind=link}

Figure 11: Favorable trends in expenditures year over year

As for market opportunity being targeted, I believe we touched on that above in the call notes but it still bears reiterating (especially as contrasted to current $150M enterprise value). Not even looking at the rest of the world or GBM (I conservatively assume that indication is a zero until otherwise proven), for NSCLC in the US across intrinsic & complex drivers, EGFR amplification and resistance mutations (C797S) we are looking at over 6,000 cases per year (expected to grow significantly in coming years).

{kind=link}

Figure 12: Addressable NSCLC opportunity in US alone

Putting a price tag on that which is similar to osimertinib (~$16,000 for a month's supply) and we are conservatively looking at a market opportunity in excess of $500M (even when I assume limited duration of therapy or cut that price tag in half). Again, when contrasted to current $75M EV that offers an asymmetric risk/reward profile for my investment, the reason for which I brought this name to readers' attention.

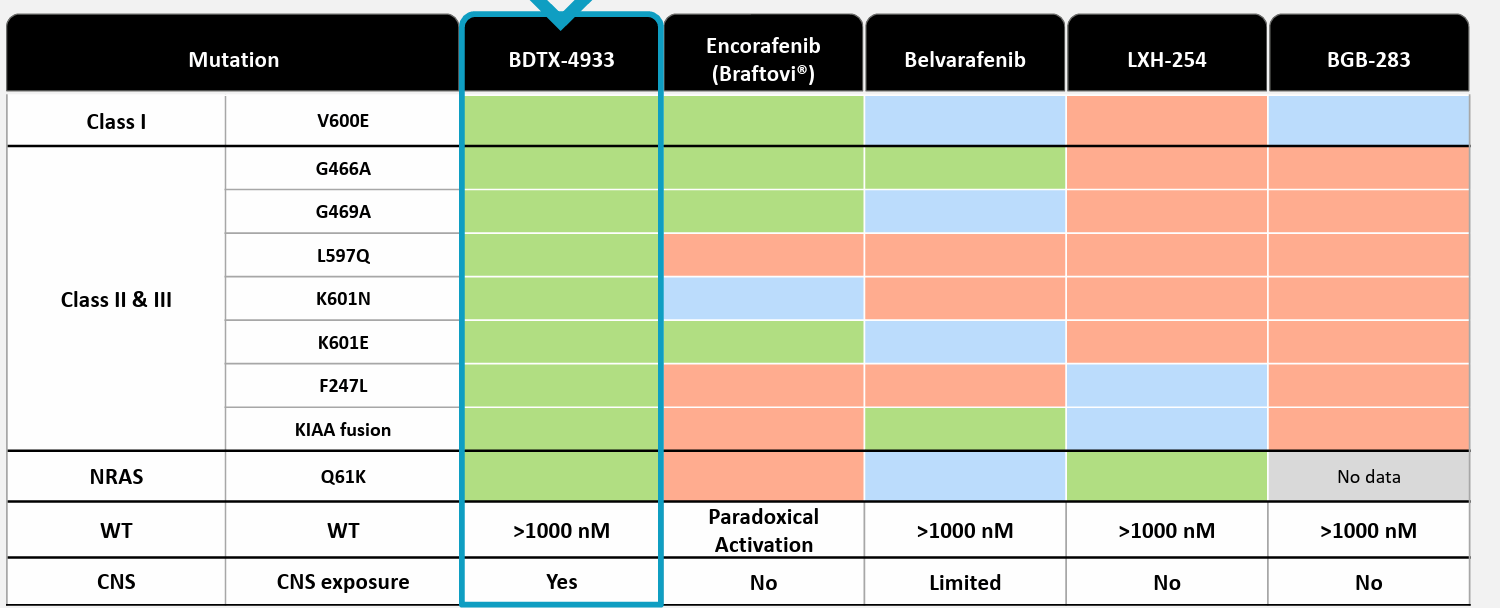

On top of that, we receive a call option in the form of the company repeating this blueprint with other drug targets such as RAF. Speaking of this one, in 2019 Pfizer ( PFE ) paid $11.4B to acquire Array Biopharma to get its hands on Braftovi (encorafenib) among other interesting drugs in the smaller company's pipeline. Much like BDTX-1535 in EGFR, the idea for BDTX-4933 would be to address a broader patient population given more complete coverage of known mutations along with CNS penetration and potentially improved safety profile.

{kind=link}

Figure 13: BDTX-4933 versus competition in RAF landscape

As for institutional investors of note, RA Capital scooped up $4.68M of shares in the recent secondary offering bringing its total holdings up to 3.21M shares (~6% of the company). BB Biotech has been steadily adding to its outsized stake now at over 8.1M shares (nearing 15% stake). Behbahani Ali (New Enterprise Associated, also on the Board of Directors) added 1M shares on the secondary to total 4.448M shares. As for other insiders, CEO and Director David Epstein owns over 670,000 shares (nice to see he has skin in the game, though that is down from 936,000 previously).

Moving on to leadership , President & CEO (and Co-Founder) David Epstein served prior as Chief Scientific Officer of OSI Pharmaceuticals (acquired by Astellas for over $4 billion in 2010). Co-Founder and Chief Scientific Officer Elizabeth Buck served prior as Assistant Director of Advanced Preclinical Pharmacology at OSI Pharmaceuticals as well. Chief Business Officer and Chief Financial Officer Fang Ni served prior as Principal of Versant Ventures (nice readthrough given Versant backed the company since inception). Chief Medical Officer Sergey Yurasov served prior as Chief Medical Officer at Immune Design Corp (acquired by Merck in 2019). Board of Directors seems quite stacked including Ali Behbahani (General Partner at NEA), Wendy Dixon (former Global Marketing Head at Bristol Myers Squibb), Sam Julkarni (CEO of CRISPR Therapeutics), Alec Mayweg (Managing Director Versant Ventures) and Rajeev Shah (Managing Director RA Capital) to name a few.

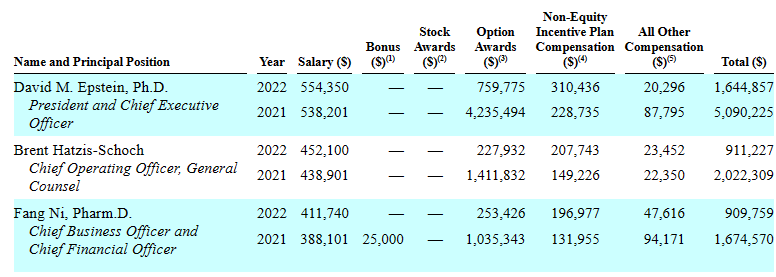

Moving on to executive compensation, cash portion of salary for CEO & team seems reasonable (for a company this size) at $554k and under. Level of option awards is quite low for 2022, but in 2021 was on the high side for CEO at over $4.2M.

{kind=link}

Figure 14: Executive compensation table

Moving onto useful nuggets from members of our investing group, MikeCriv notes that side effects for BDTX-1535 were usual (what's expected for EGFR inhibitors) but cited concern on dose limiting diarrhea. Still, he points out that the drug gives hope to patients after Tagrisso.

As for patent protection, per 10-K filing the company owns 7 provisional US patent applications, 4 pending US patent applications and one issued US patent. They also own 10 Patent Cooperation Treaty patent applications and 28 foreign patent applications. Expirations would be in the range of 2039 to 2043 (excluding term extensions). For BDTX-1535, patent applications cover NSCLC and GBM programs including composition of matter, polymorphs as well as methods of use (expirations in 2040 to 2042 range).

As for other useful nuggets from the 10-K filing (you should always scan these because investors may not get the complete picture from press releases), it's worth highlighting that in December 2022 the company announced spinout by the MAP drug discovery engine into Launchpad (new venture formed to exploit MAP for discovery of large molecule therapeutics). I'm not sure how to value such an early-stage enterprise, but at the least it's an interesting aspect of the story that remains under the radar. Also, Black Diamond Therapeutics does not own any facility that could be used for clinical-scale manufacturing and relies on third party manufacturers (lack of internal control could result in supply bottlenecks or related risks).

Final Thoughts

To conclude, with enterprise value of ~$75M, Black Diamond Therapeutics makes for an interesting (& unexpected) addition to our clinical stage portfolio. While it's true that oncology is an increasingly crowded space relative to certain other therapeutic areas we've chosen to prioritize such as rare disease and RNAi, to my eyes there is a clear opportunity ("white space") in 2nd line NSCLC in the post-Tagrisso setting for the company to pursue with lead candidate BDTX-1535.

I was initially very skeptical for a number of reasons, including competition, but the promising (though very early) monotherapy activity observed contrasts well to combination trials being run by competitors and potentially harsher tolerability profiles as seen with HER3 ADCs or amivantamab lazertinib combination. I am still concerned about the "slice and dice" nature of the initial data set and need to see further data updates including expansion cohort to become more comfortable with the drug's overall profile.

To be clear, this is not a position I am suggesting readers "max out" as we still need to see durability data in Q4 and FDA feedback on regulatory pathway (company thinks accelerated approval pathway is a possibility, while analysts are of the opinion that head-to-head trials will be required). Also, safety profile of BDTX-1535 needs to further be fleshed out so I can get a better gauge of rates of diarrhea, rash & other adverse events of note and how well patients truly tolerate the drug.

With the above caveats, the exciting aspect of thesis for me is clinical validation of the MasterKey approach to targeting multiple families of mutations with a single drug (and how they could repeat this blueprint with other high value oncology targets such as RAF or FGFR3). IF (big if) data continues to look promising for BDTX-1535, becoming the 4th gen EGFR TKI of choice and first mover in this space would be a great step in the right direction.

For readers who are interested in the story and have done their due diligence, BDTX is a Buy and I suggest accumulating dips in the current range. A prudent plan could be to acquire a partial position, then wait for Q4 data update before taking further action (letting the derisking event guide your decision).

From a near term perspective (next 12 months), I see pathway to value creation via Q4 update and more importantly expansion cohort data in 2024 coupled with initial phase 1 results for their RAF program.

As for risk rating (1=low, 5= high), I will err on the side of caution and call this one a 4 given the early-stage nature of the story (including key concerns of durability and evolving competitive landscape in EGFR). Dilution in the near term is less of a risk given recent financing, but the stock could take a hit in Q4 if in the worst case scenario the GBM update is a zero causing this program to be discontinued. Likewise, if durability disappoints for NSCLC data update in Q4, burden of proof would be on 2024 expansion cohort data and such "show me" stories often remain weak in the meantime. As for competition, in 10-K filing BDTX cites Gilotrif and Tagrisso, Rybrevant lazertinib combination from Janssen, patritumab deruxtecan from Daiichi Sankyo, Blueprint Medicines' stable of EGFR candidates, BBT-176 from Bridge Biotherapeutics, Taiho Oncology's TAS 2940 and ERAS-801 (among others, too many to name). Erasca's ( ERAS ) initial GBM data for its EGFR program is expected 2H 23 and details in its slides that the addressable patient population in US + EU is 37,000 patients.

For further details see:

Black Diamond Therapeutics: MasterKey Approach Validated With Lung Cancer Update