BRCC - Black Rifle Coffee Company Needs To Drastically Expand Its Client Base

Summary

- Massive drop in EBITDA from positive numbers in 2019 and 2020.

- Negative free cash flow.

- High liabilities to asset ratio in absolute and relative terms.

Black Rifle Coffee Company ( BRCC ) stock has had a poor performance over the past year, losing 38.8%, and more tragically it's down 82% from its high in April 2022. The company started quoting on the NYSE in February 2022, at $10. And did exceptionally well as often happens, over the next 3 months.

BRCC combined with a SPAC to bring the stock to float. The valuation of the company at the time stood at $1.7 billion . However, after the rally was short-lived and as profits began to shrink so too did the share price.

They sell premium coffee online and through a large number of coffee shops that they call outposts. The company also has a wide range of merchandise items that cater to the tastes of military and security personnel as well as patriots in general.

However, BRCC's stock price keeps faltering. And I don't see this company managing a drastic turnaround anytime soon. From my analysis of their fundamentals and technicals, I would say the company's stock price is headed lower.

My price target for BRCC stock is at $1.30, I base this level on my model using the trend in EBITDA, liabilities to asset ratio, and free cash flow. Let's look at some of the numbers for Black Rifle Coffee Co. although not exhaustive, these are the ones I look at for long-term fundamental analysis.

Basic Fundamentals

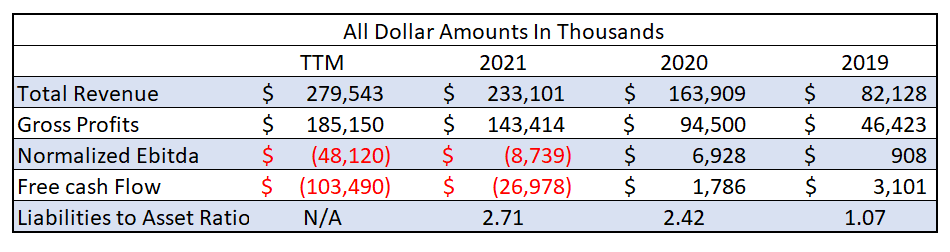

BRCC has seen its revenues increase considerably since 2019, and along with it so have gross profits. Revenue has increased an average of 53.90% per year since 2019. Which is great, but the rate of increase has been declining.

In 2020, total revenue increased by 99.58% over the previous year, while in 2022, using TTM data revenue increased by 19.92%. Gross profits show a similar story. In 2020, gross profits jumped by 253.08% in 2019. However, the TTM for 2022 shows an increase of 19.92% over 2021.

{kind=link}

EBITDA

Looking at EBITDA, we see that something has gone terribly wrong with this company's profits. Despite increasing revenue and gross profits, from 2020, the firm has managed to enter into negative earnings in 2021 and is about to multiply that loss by 5.5 for 2022.

Black Rifle Coffee Co. managed to see two years of positive earnings in 2019 and 2020. Where the company managed to multiply EBITDA by 7.7 in 2020 over 2019. I'm assuming that was thanks to their large online sales readiness during the pandemic lockdowns.

So, the lockdowns ended but revenues and profits didn't stop increasing, as we can see from the table above. Yet in 2021, the company takes a major loss and posts a negative EBITDA of $8.7 million. The TTM EBITDA is exceptionally worse at negative $48.12 million.

These numbers, in my opinion, are worrying, and I would be led to expect further losses for 2023. A major turnaround in profitability is needed, and if it comes mainly from cutting costs or increasing sales, then both would need to be dramatic.

Free Cash Flow

This number is the one that tells you how long a runway a company has. And at the moment the runway for BRCC is really short. The drop into negative numbers for free cash flow has coincided with negative EBITDA. So, it may be that the problem is due to that.

However, many companies have negative profits but still have positive free cash flow. What is concerning is the exponential drop in the TTM free cash flow compared to the number in 2021. With the year coming to an end, we can expect a very similar number for 2022 to the TTM.

So, BRCC is currently experiencing a negative cash flow for 2022 that is nearly 4 times the amount for 2021.

Liabilities to Assets Ratio

The liabilities to assets ratio is another number that has worsened greatly since 2019. In the first year I have data, the liabilities to assets ratio stood at 1.07 as of 2019. The problem I see is that BRCC now has a liabilities-to-assets ratio of 2.71 for 2021, making me seriously question its capabilities to pay back expenses and debt going forward.

That seems high compared to other companies in most industries. And looking at an industry peer and direct competitor, Starbucks has a liability-to-asset ratio of 1.31 in 2021. This indicates BRCC may be way beyond the industry average

However, its debt-to-assets ratio is more in line with its peers and more within a manageable range. Its current debt-to-assets ratio is at 0.41. Starbucks has a debt-to-assets ratio of 0.85 as of September 2022.

Quant Performance Score

Looking at our Quant Performance for BRCC, we see this coffee company gets a strong sell recommendation. The rankings for the following factors are all in danger territory, in particular Growth, which gets a flat F.

I have to add that SA authors and Wall Street analysts both give BRCC stock a Buy evaluation. Yet I struggle to see where their confidence comes from.

Technical Analysis

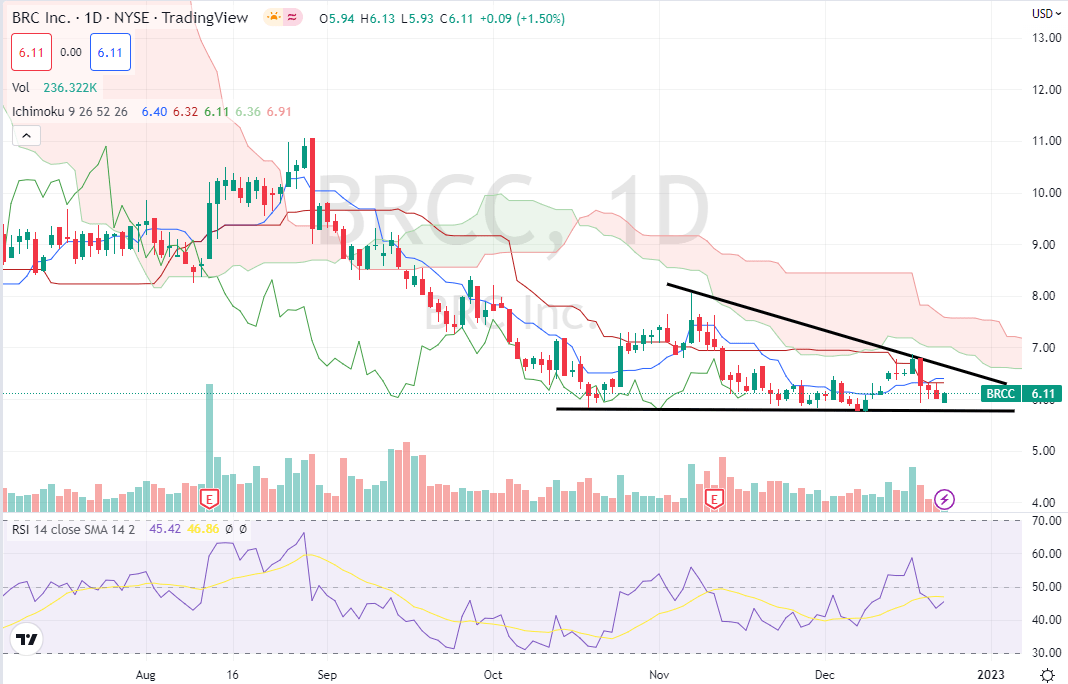

Looking at the technical analysis of BRCC stock, I see a lot of bearish indications. Looking at the day chart, we can see that price action is below the cloud, with all components of the Ichimoku Kinko Hyo system indicating a bearish trend.

{kind=link}

Price action attempted a rally in August 2022 and a break above the cloud on the back of higher-than-expected earnings. However, that flurry didn't last, and the bear trend was reassumed at the end of that month.

More recently, the BRCC stock price has been trading sideways with lower highs. This activity has given rise to a triangle, outlined by the two black lines. From experience, the third touch on one of the triangle's sides is when the chart pattern gets broken. And it currently looks like the stock's price is heading south.

It may bounce off the horizontal support line, but I would say it most likely breaks it to the downside.

What BRCC Stock Does Have

- The company has a few factors that could increase its sales and revenue. How well they can implement them and how much they would impact its balance sheet remains to be seen.

- Scale for brand awareness: The company has achieved a notable level of brand awareness among its target customers, but there is still plenty of room for growth.

- Large media presence: Black Rifle Coffee Co. has a very large social media presence, which demonstrates the commitment and loyalty of its customers. Leveraging this medium to expand sales through brand awareness could provide increased sales.

- Growing gross profits: The company reports an estimated 57% CAGR in revenue from 2019 to 2022.

- Premium quality brand with a loyal customer base: This factor could push earnings higher if they can reduce debt and increase sales by acquiring a wider client base.

Conclusion

Black Rifle Coffee Co. really needs to turn things around and increase revenue and consequentially profits in a big way. To do that, they need to raise brand awareness to much higher levels. Given that it has a large social media presence when compared to some of its direct peers, it could be possible.

Overall, with their current fundamentals and the technical analysis for BRCC stock. It doesn't seem likely to me that this stock's price will be turning around anytime soon. I remain extremely bearish on the price of BRCC stock for the first half of 2023.

For further details see:

Black Rifle Coffee Company Needs To Drastically Expand Its Client Base