BSM - Black Stone Minerals: Distribution Cut Looks Likely In 2024

2023-08-18 17:12:49 ET

Summary

- While Black Stone Minerals kept its production guidance unchanged, a gassier outlook is a slight negative.

- The company's hedge book is currently a tailwind, but it is expected to become a headwind next year.

- Expect a distribution cut next year.

I've written about Black Stone Minerals ( BSM ) a couple of times, taking a bullish view in February , and turning more neutral on the name in May . Let's catch up on the name following its most recent earnings report.

Company Profile

As a quick refresher, BSM is a mineral interest holder that owns the commodities under tracts of land that it leases to producers in exchange for a royalty interest. As a mineral interest holder, BSM gets a percentage of the production or revenue from the production, typically 20-25%, and it doesn't have to pay for any operating transport or F&D costs. It also receives upfront lease bonus payments when it leases new land. BSM also has some non-operated working interests where it does have to pay its portion of the costs associated with drilling and operating these wells.

One of BSM's most important agreements is with Aethon in the Shelby Trough, where it has given the E&P exclusive access to its acreage and preferred royalty rates in exchange for increased drilling.

Q2 Earnings

For Q2 , BSM saw revenue fall -35% to $117.0 million, missing analyst estimates by about $10.6 million. The decline was largely due to lower commodity prices.

Earnings attributable to common unitholders came in at $73.1 million, or 35 cents per unit, down from $126.5 million, or 59 cents per unit. That missed the consensus estimate by -3 cents.

Adjusted EBITDA fell -3% to $109.2 million, with the number being helped by the difference in unrealized hedges in both periods. Distributable cash flow ((DCF)) dipped -3% to $103.6 million. On a per unit basis, DCF also slipped -3% to 49.3 cents from 50.9 cents.

BSM paid out a 47.5 cent distribution in the quarter. Its distribution coverage ratio was 1.04x.

Total production rose 8% to 36.2 MBoe/d, while working interest production fell -19% to 2.6 MBoe/d. Total volumes were down nearly -8% sequentially.

Mineral and royalty volumes rose nearly 11% to 33.6 MBoe/d year over year. These volumes declined nearly -9% sequentially from 39.3 MBoe/d in Q1.

Total natural gas production climbed nearly 14% to 14,670 MMcf, while oil & condensate volumes decline by -6% to 846 MBbls.

The company said overall rig counts in the U.S. declined -11%, while it saw an -8% decrease on its acreage, mainly in the Permian. Aethon had 5 rigs on its Shelby Trough acreage and is expected to be at its minimum pace of 27 wells at year-end.

BSM ended the quarter with zero debt and had $46.7 million in cash at the end of June.

This was a similar quarter to last quarter for BSM, with a tight coverage of its distribution and some decent year-over-year production growth. However, volumes have been declining quarter over quarter, showing the difficult environment for natural gas given current prices.

Hedge Book

BSM continues to currently benefit from the roll-off of low-priced hedges to more attractive hedges. In Q2, the company had a realized gain of $11.3 million from its hedge book.

{kind=link}

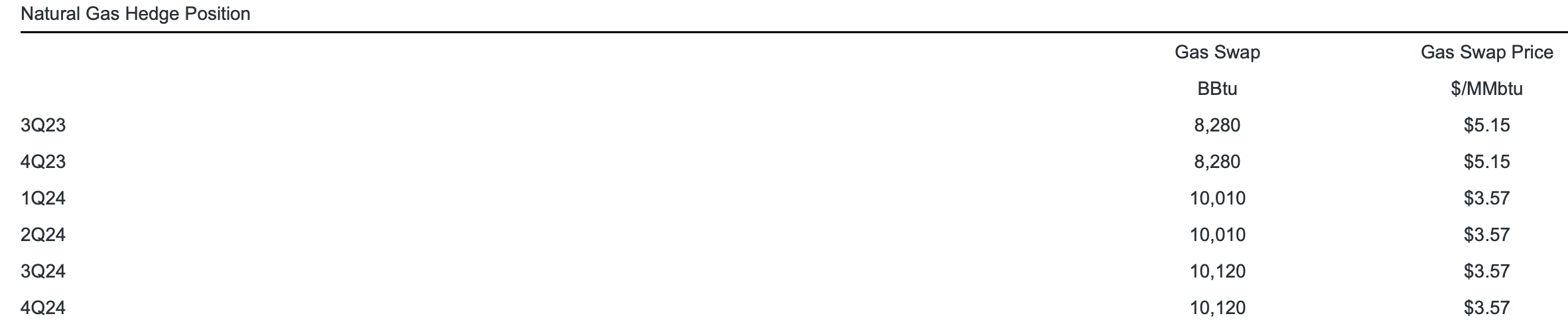

For the rest of 2023, its natural gas hedges have a weighted average price of $5.15. In 2022, its Q3-Q4 natural gas hedges had a weighted average price of $3.12. That's a 65% increase this year compared to last year.

For 2024, its weighted average price for natural gas hedges is $3.57. That's still about above 2022 levels, but a big decline versus 2023 levels.

For oil, weighted average oil hedges are $80.80 for the rest of 2023. The weighted average price Q3-Q4 in 2022 was $66.47. The company has oil hedges for 2024 at a weighted average price of $68.98.

While the hedge book is currently a tailwind, it will likely turn into a headwind next year.

Outlook

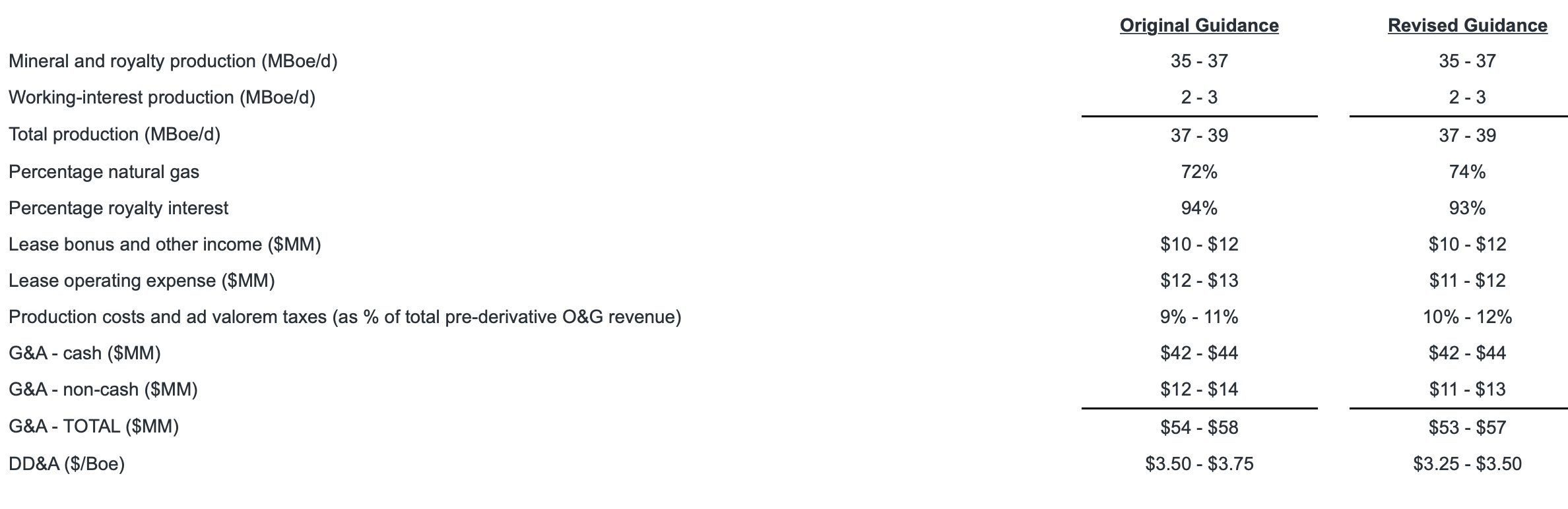

BSM slightly updated its outlook. It still expects production to be between 37-39 MBoe/d, although it is expecting that production to be slightly gassier. It's also expecting its overall G&A costs to be slightly lower at between $53-57 million versus an earlier outlook of $54-58 million.

DD&A is expected to come in lower. The company is now projecting it to be between $2.35-3.50 per BOE versus a prior forecast of $3.50-3.75.

{kind=link}

Commenting on the guidance mix being gassier, interim CFO Evan Kiefer said :

"We've seen several things going on this year that just shifted that focus towards the gassier mix. One, we did have a little bit of a pushback in the initial estimates on some wells in the Austin Chalk. We also saw a little bit of a shift from the Permian coming in a little lower than we originally forecasted at the beginning of the year, but also some increased benefit from the Haynesville side that has come in a little bit above estimates for the first half of the year. So really kind of a combination of those several things is what's driving the slightly increased gassier mix for the year compared to what we were looking at the beginning."

The company also noted that some of the wells in the Austin Chalk were in drilled in deeper area that are more gassy, while the core areas tend to have a higher percentage of liquids.

Overall, guidance was solid, with its production view unchanged and some slightly lower costs. The slightly gassier mix, however, is a bit of a negative, as liquid prices have been stronger than gas.

Distribution

One of the main reason many investors own BSM is for its distribution and nice 11% yield. BSM's coverage ratio has been pretty tight the last several quarters, with natural gas prices plummeting. However, it' hedge book has helped prop its distributable cash flow.

Ask about the distribution on its call, Kiefer responded by saying:

"And so one being the first and second quarter did come in fairly close with each other and almost within I think $0.5 million on a DCF basis. And so, one, we saw the coverage and felt comfortable with where the balance sheet was today to maintain that higher payout ratio. And as you mentioned, even going through kind of the remainder of the year, just looking at natural gas, where third quarter were up to on the strip today, call it, $2.50, which is really just under a 20% increase from what we saw in first quarter. So we do like maintaining that distribution as best we can. I think right now, there's some momentum at least on pricing that does help that through the third quarter and even above that into the fourth quarter with gas prices being closer to $3. And so yes, we like the ability to maintain that, I think, with the balance sheet strength and the forecast that we're currently looking at for the second half of the year allows that."

With its current hedge book and better winter natural gas pricing, BSM should be able to maintain its distribution the rest of this year. However, it becomes much trickier next year when it has much lower-priced hedges in place. At that point, the distribution likely will need to be cut unless natural gas prices rally. While I'm bullish on natural gas prices a bit further out, investors will need to root for a cold winter to help spur a natural gas prices in the more immediate future.

Conclusion

Until I see a natural gas price rally, I can't get on board with BSM at this point given the roll-off of its hedges next year. And barring that rally, the distribution will have to be cut next year at the latest. Meanwhile, I don't think investors have priced that into the stock at this point.

As such, I plan to remain on the sidelines. Lower realized commodity prices, declining sequential volumes, and favorable hedges rolling off next year is not at great combination.

For further details see:

Black Stone Minerals: Distribution Cut Looks Likely In 2024