BLKB - Blackbaud: With Trends Accelerating Risks Have Waned (Rating Upgrade)

2023-12-12 11:28:19 ET

Summary

- Blackbaud has seen a +40% jump in its stock year to date, accompanied by stronger growth trends and a richer bottom line.

- The key themes that have moved in Blackbaud's favor include an increase in organic revenue trends and continued cost rationalization, leading to expected margin accretion next year.

- However, Blackbaud's valuation does not compensate for its lagging growth, and the company faces fundamental risks such as competition and reliance on transactional revenue.

Blackbaud ( BLKB ), a vertical software company that is dedicated to the needs of charities and non-profit organizations, is proving an old adage to be true: that everything that is old can be made new and exciting again, at least for a little bit.

This legacy software provider has seen its stock jump over 40% year to date, a rally that has been accompanied by both stronger growth trends and a richer bottom line:

I'll concede that I made an earlier, overly pessimistic call on Blackbaud (though part of the stock's rally this year has been driven by general market enthusiasm for lower interest rates). I last wrote a bearish opinion on Blackbaud in July, when the stock was trading closer to $75 per share. Since then, Blackbaud has released Q3 earnings - and that's what makes me more sanguine on the company's prospects.

We'll dive into more detail in the next section, but the key themes that have moved in Blackbaud's favor are an increase in organic revenue trends, continued cost rationalization that have bolstered its bottom line, and management's bullish expectations for further improvements in FY24.

At the same time, however, I'm not ready to fully back Blackbaud and add it to my portfolio just yet. One core reason here is that, despite being a slower-growing legacy tech stock, Blackbaud's valuation does not compensate for its lagging growth. We'll look at this one on an earnings basis, since Blackbaud's revenue growth rates don't exactly inspire a premium valuation based on revenue multiples.

At current share prices near $86, Blackbaud trades at a 19.0x P/E ratio based on Wall Street's consensus FY24 pro forma EPS expectation of $4.57, representing 17% y/y earnings growth on the back of 7% y/y revenue growth to $1.19 billion (note that Blackbaud's top-line growth rates have been choppy: they were at the low single digits for most of last year before recently spiking back to mid/high single digit growth in the most recent Q3). Even when fully factoring a 17% earnings growth expectation (which may be aggressive) and looking at Blackbaud's PEG ratio of 1.1x, there doesn't seem to be an immediate valuation draw - which is what I'd expect in order to invest into a slower-growing, decades-old tech firm.

Let's also not forget the fundamental risks that this company possesses:

- Blackbaud competes with far larger and more generalized CRM platforms like Salesforce ( CRM ). From a buyer perspective, the very real possibility that Blackbaud faces financial difficulty and can't support/provide software updates a large upfront IT investment may be a compelling reason to choose a sturdier competitor

- Reliance on transactional revenue creates ebbs and flows in the business. Unlike many other SaaS companies that generate primarily subscription-based revenue, Blackbaud depends on transactional revenue which declines when charitable giving is down (as it did during the pandemic).

- Heavy debt load- As of its most recent balance sheet, Blackbaud carries ~$740 million of debt on its books, which is more than 2x the company's adjusted EBITDA of ~$340 million.

The bottom line here: I'm not ignoring the slightly stronger top-line trends in Blackbaud, but neither do I see a meaningful path to stock price appreciation when it's already sitting at a ~19x P/E ratio. I am neutral on this stock: watching and waiting here is still the best approach.

Q3 download

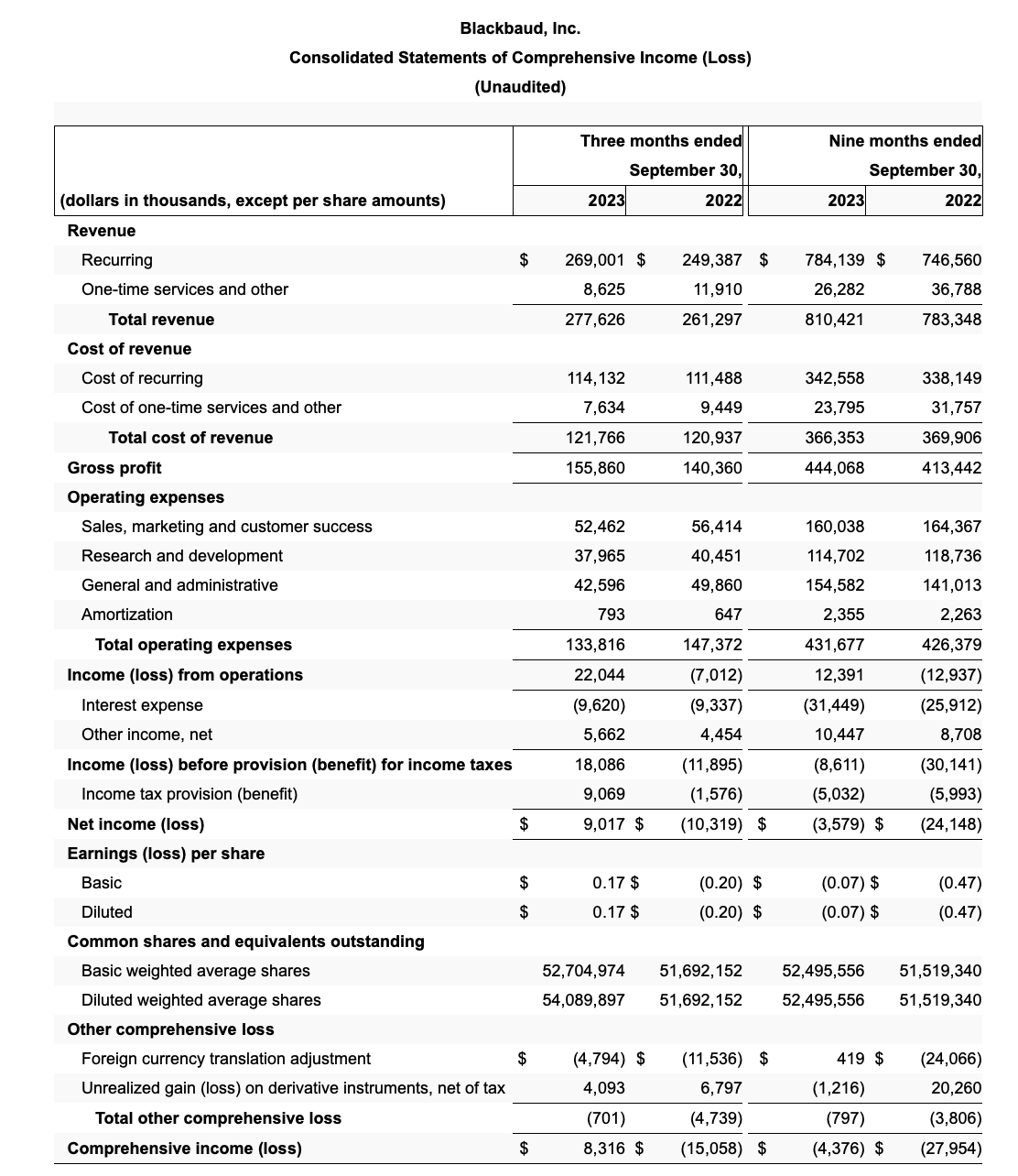

Let's now go through Blackbaud's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

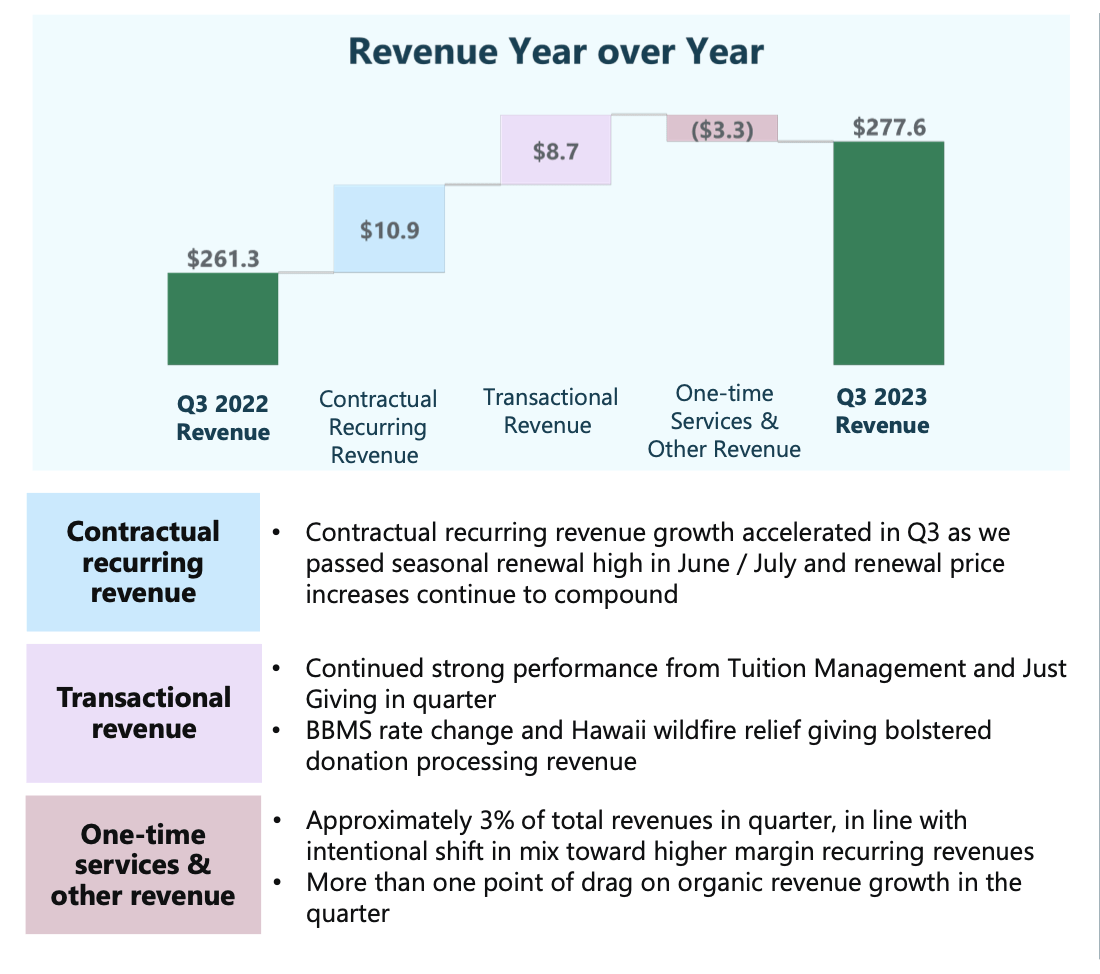

Blackbaud's revenue grew 6% y/y in the quarter to $277.6 million, ahead of Wall Street's expectations of $275.9 million by a relatively small ~40bps margin. Importantly, organic revenue growth - which strips out the impact of Blackbaud's frequent acquisitions and divestments - grew 8.3% y/y. This, in turn, represented nearly a doubling of growth rates from 4.4% y/y in Q2 (and just 3.4% y/y in Q1).

The chart below lays out some of the drivers for better-than-expected revenue growth.

{kind=link}

Importantly, note that the company successfully renewed a lot of contracts in June and July, while also pushing price increases onto its customer base. Meanwhile, transactional revenue saw improvement from higher giving rates, where the company specifically called out Hawaii wildfire efforts as a driver for increased giving.

Here's some further context from CFO Anthony Boor's prepared remarks on the Q3 earnings call , specifically calling out the benefits of recent pricing actions:

For the quarter we continued to see excellent results from modernizing our pricing model in the social sector. We also continued to extend contract terms. Last year the majority of contract renewals were for a one-year term, this year the vast majority have been for a three-year term and recall that there are embedded mid to high single-digit price escalations in years two and three of multi-year contracts.

The power of this transformation is remarkable and is just now being felt in the business. There are three additional benefits of this modernization program. First, it provides a higher degree of revenue security. Second, it dramatically increases revenue visibility and predictability, which aids planning. And third, it reduces the volume of internal work effort involved in the renewal process. And given that our retention metrics have held up or are slightly improved, we're quite happy with the impact this program is generating. The remaining third of our revenues are transactional in nature and are composed of donation processing, consumer giving, and tuition processing for our K-12 school clients. These revenue streams are connected to and result from our software subscriptions. They have good value for our customers, eliminate their busy work, and create greater customer stickiness. All three saw good volume growth this quarter and like contractual recurring, we've had good success implementing price increases in this area of the business as well, although at more modest rates."

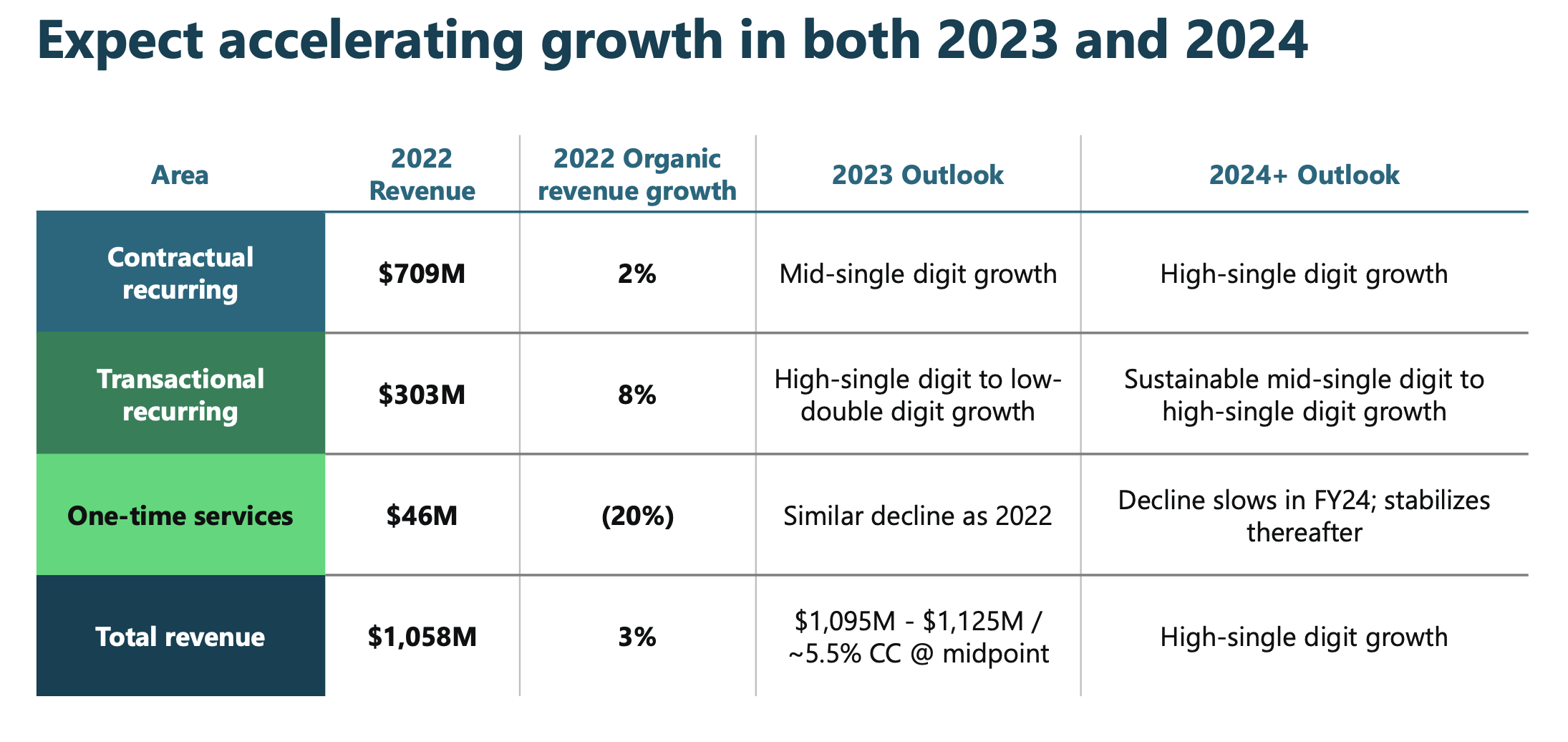

The company is expecting stronger growth trends to continue into FY24:

Blackbaud high level FY24 expectations (Blackbaud Q3 earnings deck)

{kind=link}

As shown in the chart above, the company expects contractual recurring revenue to accelerate to high single digit growth next year (versus mid single digit growth this year), and for transactional revenue to slightly edge up to "mid single digit to high single digit" growth. Overall, total revenue is expected in the high single digits, versus 5.5% y/y this year.

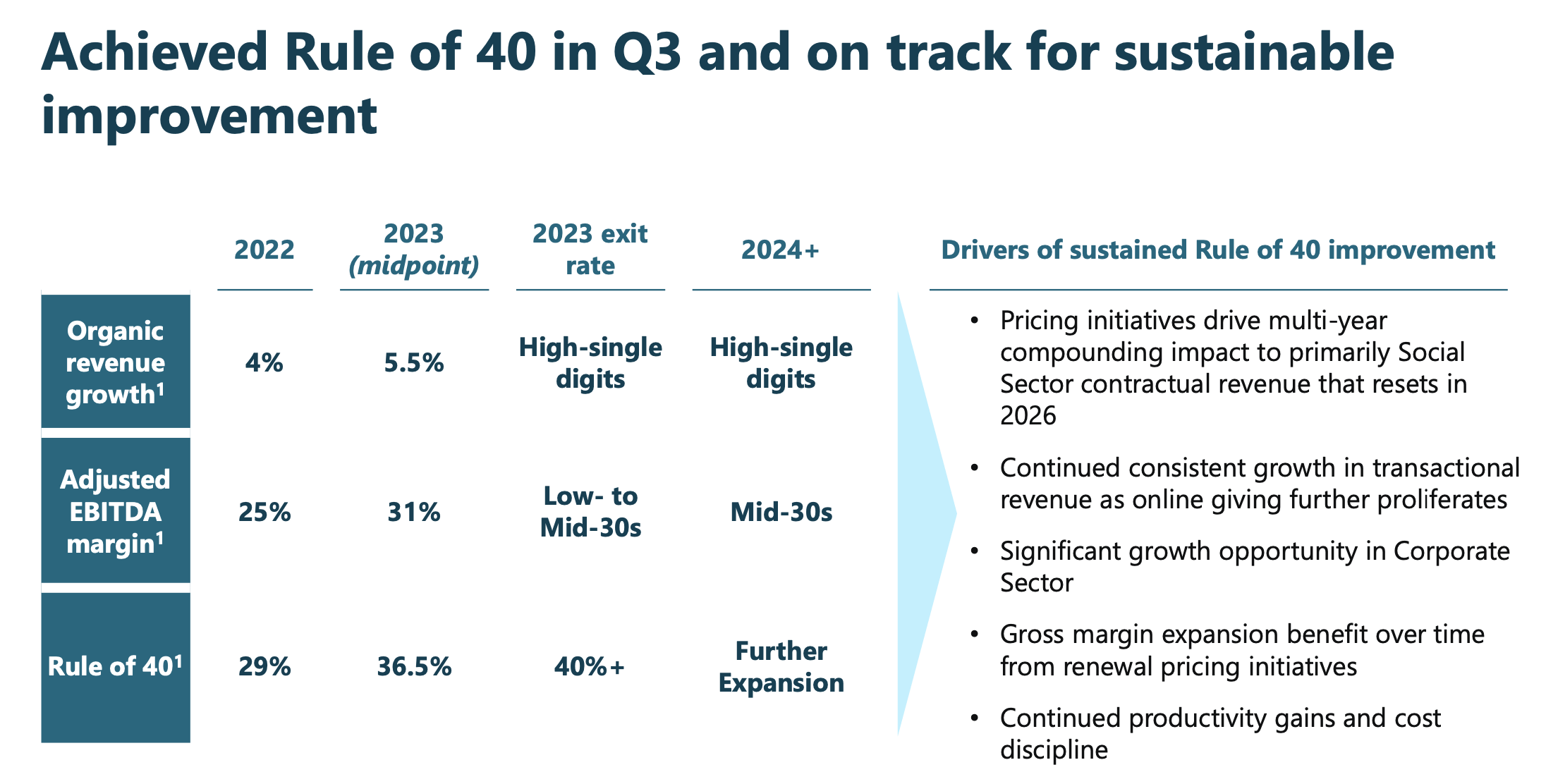

The company is also banking on continued adjusted EBITDA expansion, with this year's expected 31% adjusted EBITDA margins improving to a margin in the mid-30s next year:

{kind=link}

Key takeaways

It's true that at face value, Blackbaud seems to be enjoying improved trends: but that's against relatively poor comparisons over the past few years. I still have trouble digesting a low-growth software company investment at a ~19x forward P/E ratio. With recent sequential improvements, I no longer believe there's substantial downside in this stock, but neither do I think this is a major winner either.

I'd continue to navigate away from this name and invest elsewhere.

For further details see:

Blackbaud: With Trends Accelerating, Risks Have Waned (Rating Upgrade)