BB - BlackBerry Q4 Earnings: Still Not Looking Great

2023-03-08 10:54:20 ET

Summary

- BlackBerry preannounces its Q4 results and it's on target to miss its previous guidance. But that's not the only bad news.

- The real bad news is that BlackBerry's balance sheet has a land mine that investors are not fully appreciating.

- I lay out two options for BlackBerry's debentures with neither outcome being positive.

Investment Thesis

BlackBerry ( BB ) puts out its preliminary fiscal Q4 2023 results.

This is my contention, I don't think that anyone at this stage holds out much hope for BlackBerry.

No, let me rephrase. There are few investors left in this trade that believe that this is a growth company. There's always a hope that BlackBerry's share price is trading so cheaply relative to intrinsic value, that there's ''bound'' to be an opportunity to sell into strength as its share price appreciates on the back of some positive surprise.

However, over time even the shorts have decided to call it a day here.

{kind=link}

With few shorts left, this substantially reduces any potential for a short squeeze.

This is my thesis, even though BlackBerry's stock is down so significantly, its balance sheet holds a land mine that investors are not fully pricing in.

Therefore, I retain my sell rating on this stock.

One for the History Books?

Asides from the Covid crash of April 2020, BlackBerry has for the past 10 years continued to trade lower with time. When we look back to BlackBerry, I wonder if we'll read about BlackBerry in financial books in the same vein as either Blockbuster or Enron?

BlackBerry's history is one of consistently mismanaging shareholders' capital to buy up businesses, then restructure and write them off. The most recent write-off is Spark, for 20% of BlackBerry's market cap.

However, I don't believe that BlackBerry's intentions are nefarious. Indeed, that's not my contention at all. It's simply that capitalism is brutal. Simply put, in tech, you are either disrupting or getting disrupted.

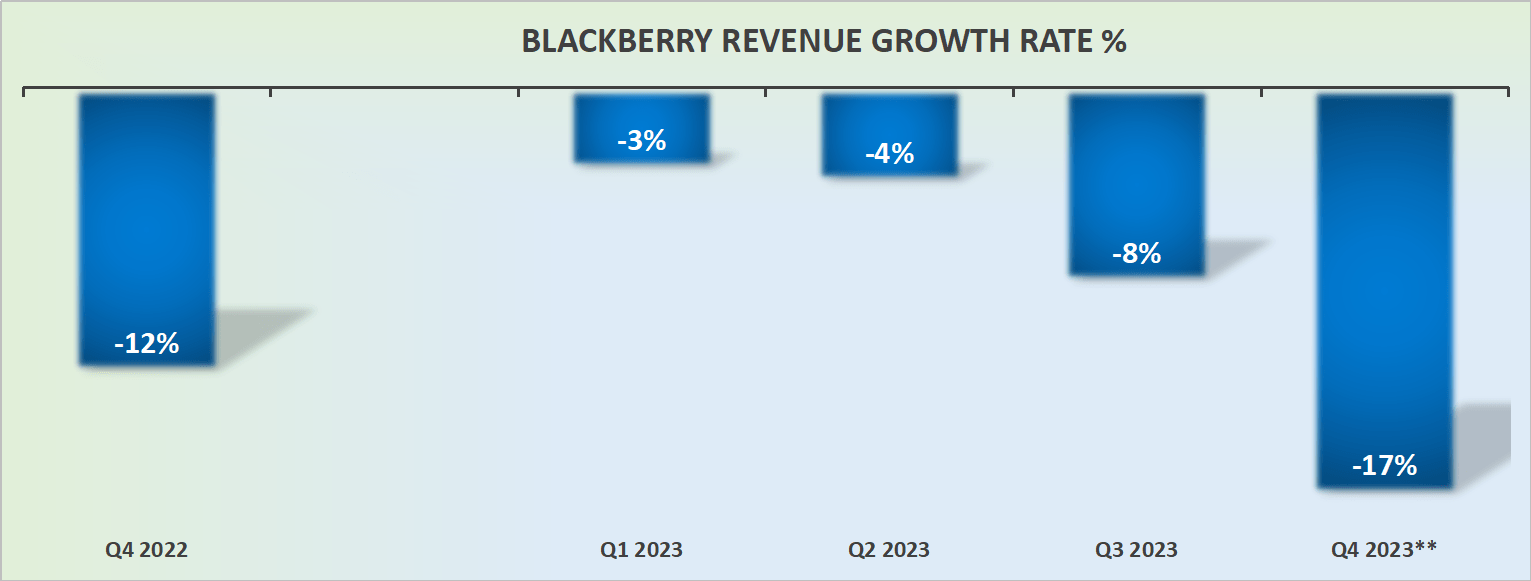

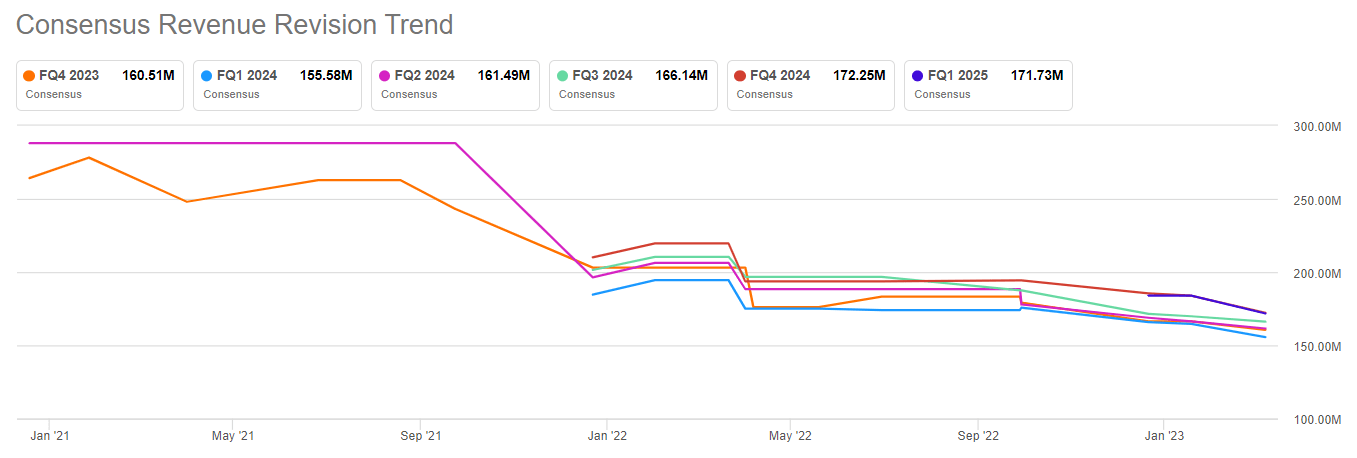

Revenue Growth Rates Don't Inspire Much Hope

{kind=link}

BlackBerry charges that the reason why its fiscal Q4 revenue estimates are expected to be so negative is that certain large government deals under negotiation didn't close in the quarter and that these large deals got pushed out into the next fiscal year.

But I believe that's only one part of the story. The other part is not about certain delays getting delayed. A more realistic appraisal focuses on the fact that for years BlackBerry's quarterly results have been reporting negative growth rates.

{kind=link}

What the graphic above shows is not only that analysts covering BlackBerry has been unanimously bearish on its prospects. But despite having bearish outlooks for the company, BlackBerry still manages to under deliver against those lower expectations.

Do BlackBerry's Patents Hold Tremendous Value?

For a long time, bulls have been making the case that BlackBerry's patents carry huge value. And that if management were to sell some of its patents, huge value would be unlocked from the business.

I have no intention to be glib, but I simply don't buy it. This is what I see, a business that holds $450 million of cash.

And against that cash, there are $500 million face value convertible debentures. What's more, these debentures mature this year, in November 2023.

So, BlackBerry faces two options.

- They can either refinance these convertibles. Presently, the convertibles have a 1.75% coupon. But with interest rates now at about 5%, I suspect that BlackBerry's interest payments will minimally be 9%-10%. That will delay the inevitable.

- Or BlackBerry can seek to convert its debentures into shares.

For their part, BlackBerry declares that there's a third option. BlackBerry was asked about its debentures in the prior earnings call, this is what CEO John Chen said,

Analyst

One of the debentures is due in about a year, any messaging on paying it down versus refinancing at this point?

John Chen

I think we're going to pay it down.

But I simply can't see how that's possible. If BlackBerry's cash burn rate is about $100 million per year, they only have about 3 years left of cash on the balance sheet. They simply can't pay down these debentures.

The Bottom Line

BlackBerry is a dead company walking. BlackBerry's balance sheet is meaningfully constrained. Investors should tune into BlackBerry's earnings call at end of March to find out what's the realistic plan for its convertibles debentures: shareholder dilution of approximately 25% of BlackBerry's market cap or to carry out that debt with 9%-10% coupon rates?

For further details see:

BlackBerry Q4 Earnings: Still Not Looking Great