BB - BlackBerry Stock: From Bad To Worse

2023-03-31 14:54:08 ET

Summary

- BlackBerry Limited business hasn’t gained traction.

- The company has a multi-year downside trend and it doesn’t seem able to reverse that.

- The market valuation is too generous, a further steep correction for BB stock is in the cards.

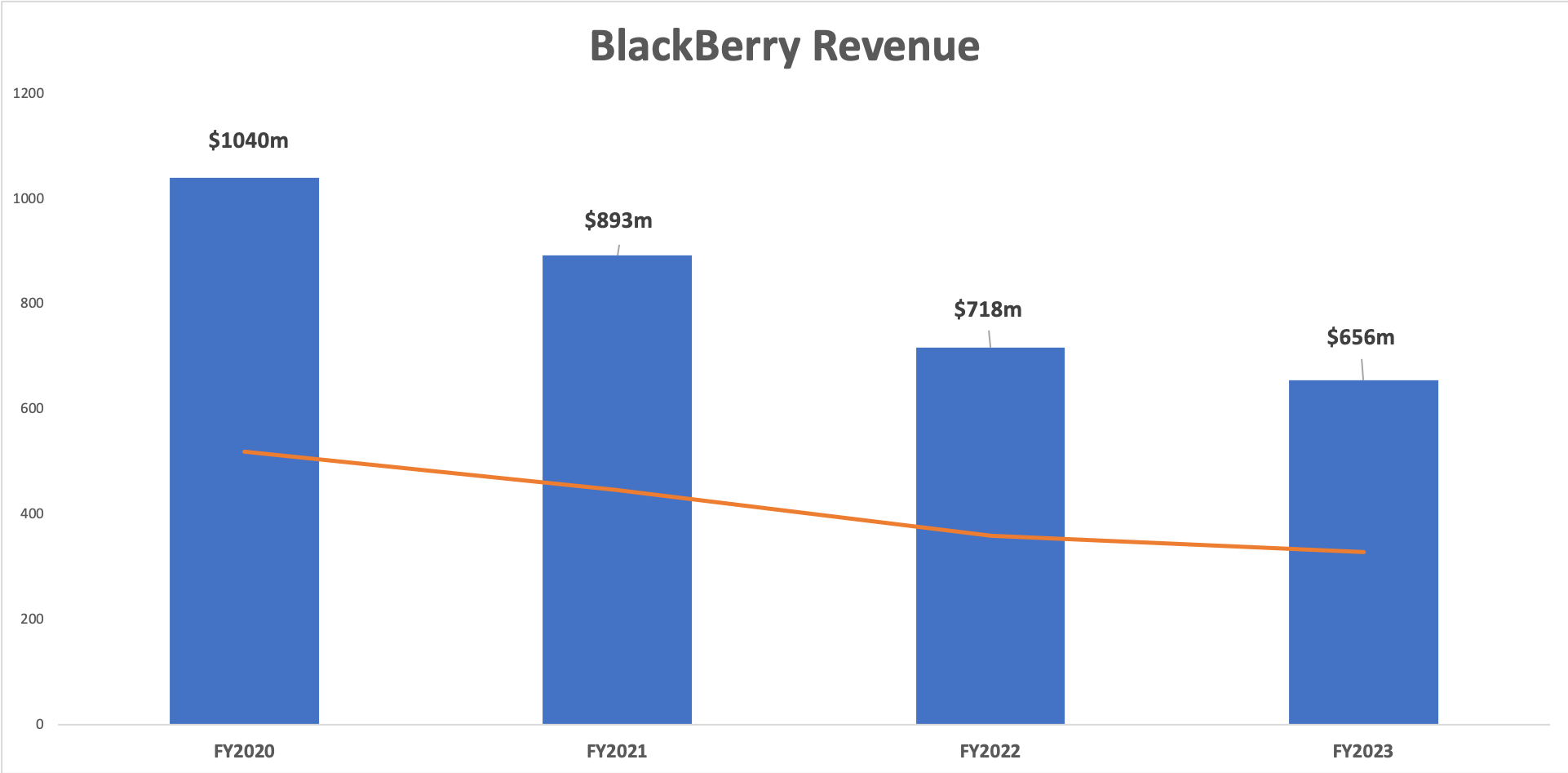

Unfortunately, the latest results for BlackBerry Limited (BB) paint a bleak picture for shareholders. The company's top-line revenue experienced a worrying high single-digit decline year-over-year. This decline is part of a larger trend, with BlackBerry's revenue decreasing at a compound annual growth rate of 17% over the last four years.

{kind=link}

BlackBerry's Turnaround Never Turns

BlackBerry Limited CEO John Chen has been at the helm of the company for a decade, but the promised results are still nowhere in sight. When he took over in 2013, BlackBerry was still generating billions in sales, and he made it his mission to refocus on the most profitable businesses. While he made some progress in this regard, the cybersecurity and IoT fields that BlackBerry is now operating in are highly competitive, and gaining traction has proven to be incredibly difficult. Although these areas are not as capital-intensive as producing phones or other equipment, they are also not particularly lucrative.

For a while, Chen was able to generate some cash flow by monetizing BlackBerry's patents, which he did quite successfully. However, once those patents began to age, that significant source of revenue disappeared.

It's worth noting that BlackBerry's management claims they stopped working on licensing their patents voluntarily because they were focused on selling them to an unknown consortium without a business history or funds. However, the likelihood of success was always low, as I have suggested before. Despite this, Chen's team continued down this path for over two years before giving up , and the licensing business essentially fell apart. I never seriously believed that they stopped monetizing their patents on purpose, as claimed. Still, if they did, it was undoubtedly a terrible mistake.

Now, BlackBerry is reportedly selling the same patents, which are two years older, to another entity for a token amount, not much more than $200 million. We will have to wait and see what comes of this sale.

BlackBerry’s Fair Value

BlackBerry’s stock price has been in a steady decline over the last few years. In March 2021, the shares were exchanged on NYSE at an average of $10. At the current prices, which are below $4 per share, can we confidently say that the bottom has finally been reached? Let’s look at some key numbers.

As BlackBerry has become essentially a cybersecurity play, it's useful to compare it to other cybersecurity companies, even though the results would be essentially the same for any software/tech company.

See the following table:

| Price to Earnings |

| EV/EBITDA |

| Price to Sales |

| BB |

| (Negative) |

| -29 |

| 3.4 |

| Fortinet, Inc. ( FTNT ) |

| 58 |

| 43.4 |

| 11.2 |

| Check Point Software ( CHKP ) |

| 21 |

| 16.1 |

| 7.1 |

Source: Author’s elaboration.

The price-to-sales ratio is significantly lower for BlackBerry, but this is mostly due to the fact that the Canadian company is not profitable (like the other two “peers”) and it’s not growing.

So perhaps it would be more appropriate to compare BlackBerry with some cybersecurity enterprises which are also currently not profitable, like Palo Alto Networks, Inc. (PANW), Okta, Inc. (OKTA), and CrowdStrike Holdings, Inc. (CRWD):

| Growth (2Y CAGR) |

| EV/EBITDA |

| Price to Sales |

| BB |

| -14% |

| -29 |

| 3.4 |

| Palo Alto |

| 27% |

| 151 |

| 10 |

| CrowdStrike |

| 60% |

| -694 |

| 13.4 |

| Okta |

| 49% |

| -19 |

| 7.2 |

Source: Author’s elaboration.

The issue here is that BlackBerry is not in the league of tech companies with high margins producing reliable profits, nor in that of companies that are unprofitable but fast-growing. Moreover, even those non-profitable/fast-growing firms can usually count on a positive Free Cash Flow stream (in the case of Palo Alto, a huge free cash flow stream), while BlackBerry ended the year with a negative free cash usage of $270M, with a very low single-digit Capital Expenditure, which is probably too low to be true.

So, the relative undervaluation of BlackBerry is just optical; it's probably more on the overvaluation side, indeed. In fact, how do you want to value a company in a steady downtrend that doesn’t make any money? Possibly just about the same level of its equity value (because we need to consider that BlackBerry’s balance sheet is not leveraged and the company is still in a net cash position).

On the positive side, it’s worth mentioning that BlackBerry has a reliable shareholder, Prem Watsa, who will definitely give his financial support if needed, as he did in the past. Eventually, he could even jump up and buy the remaining shares, so it's not naïve to assume that there is probably a floor to BlackBerry’s stock price that can’t be broken. However, if that floor is $4, $3, or $2, it’s hard to say!

It's also worth noting that John Chen, the CEO, will reportedly step down at the end of this calendar year. His turnaround efforts haven't yielded significant results, and his missteps outweigh his achievements in the last 10 years. He didn’t do a great job in increasing shareholders’ value, to say the least: therefore, shareholders should cheer his depart.

Bottom Line

BlackBerry Limited had another tough year, with its revenue declining by 9% YoY. What's even more concerning is that the company is now generating a large negative free cash flow, something that CEO John Chen had always managed to avoid in the past. With the abrupt halt of BB's patent licensing business, which had been a major source of cash inflow, the company's cash position is also under threat. While BB still has a net cash position, it's unlikely to last if the bleeding isn't stopped soon.

Overall, it's clear that BlackBerry is facing some serious challenges. Its current situation makes it hard to justify a high valuation, but it's worth noting that the company still has a net cash position and a reliable shareholder in Prem Watsa, who could provide financial support if needed.

BlackBerry Limited stock has already taken a significant hit in recent years, as mentioned earlier. But we're now looking at a company with declining sales and no profit to speak of, which is burning through cash. It's difficult to assign a fair value to BlackBerry Limited that's much higher than its current equity value (which is less than $1B). The problem is that BlackBerry Limited's market cap is currently 2.5 times higher than that.

For further details see:

BlackBerry Stock: From Bad To Worse