BB - BlackBerry Stock: Valuation Vs. Reality Patent Sales And Profitability Woes

2023-06-20 14:07:30 ET

Summary

- I argue that BlackBerry Limited stock is overvalued and hold doubts about its future prospects.

- Despite the recent sale of patents, BlackBerry's balance sheet continues to hold back the company.

- Historical revenue growth rates have been negative, and future growth projections appear optimistic, making me skeptical about its underlying prospects.

Investment Thesis

I argue that BlackBerry Limited ( BB ) is overvalued for what it offers. The business has put together a grand forecast where it will reignite its revenue growth rates from a larger base next fiscal year, fiscal 2025. However, I remain highly skeptical.

Furthermore, at its core, is the question of BlackBerry's balance sheet . Yes, after the sale of its patents, BlackBerry now has enough cash to pay off its debt matures this year, but what's left is a business that needs to rapidly improve its profitability to support its current valuation.

I remain bearish on BB stock. Even though I recognize that the share price is clearly climbing higher since my previous bearish analysis .

Rapid Recap

BlackBerry provides software and security solutions.

In my previous analysis, I stated:

For a long time, bulls have been making the case that BlackBerry's patents carry huge value. And that if management were to sell some of its patents, huge value would be unlocked from the business.

Lo and behold, less than 20 days after I wrote those comments, BlackBerry's management would unlock the ''huge value'' locked up in its patent.

How much did BlackBerry fetch from the sale of its 32,000 patents? BlackBerry will make about $170 million in cash upfront, with possibly a further $50 million or thereabouts over the next several years.

Note, there are further sums expected, if those patents ultimately do end up delivering tremendous value, but for all intents and purposes, we should not consider anything more than $200 million in the next few years. Although, more could come over the next 5-plus years.

So how should we appraise BlackBerry now?

BlackBerry holds about $660 million of cash and equivalents (including the patent cash). But against this cash, BlackBerry has about $360 million worth of debentures (debt instruments) that are amortized on the balance sheet, but actually hold $500 million at face value. Simply put, this is an unprofitable business, that holds slightly more cash than the claims against that cash.

And to further complicate matters, this debt matures this year. Meaning that once the debt is paid off, BlackBerry will hold about $150 million of cash on its balance sheet. For my part, I still remember not too long ago, when BlackBerry held more than $1 billion of cash.

Revenue Growth Rates Guided to Move Higher

{kind=link}

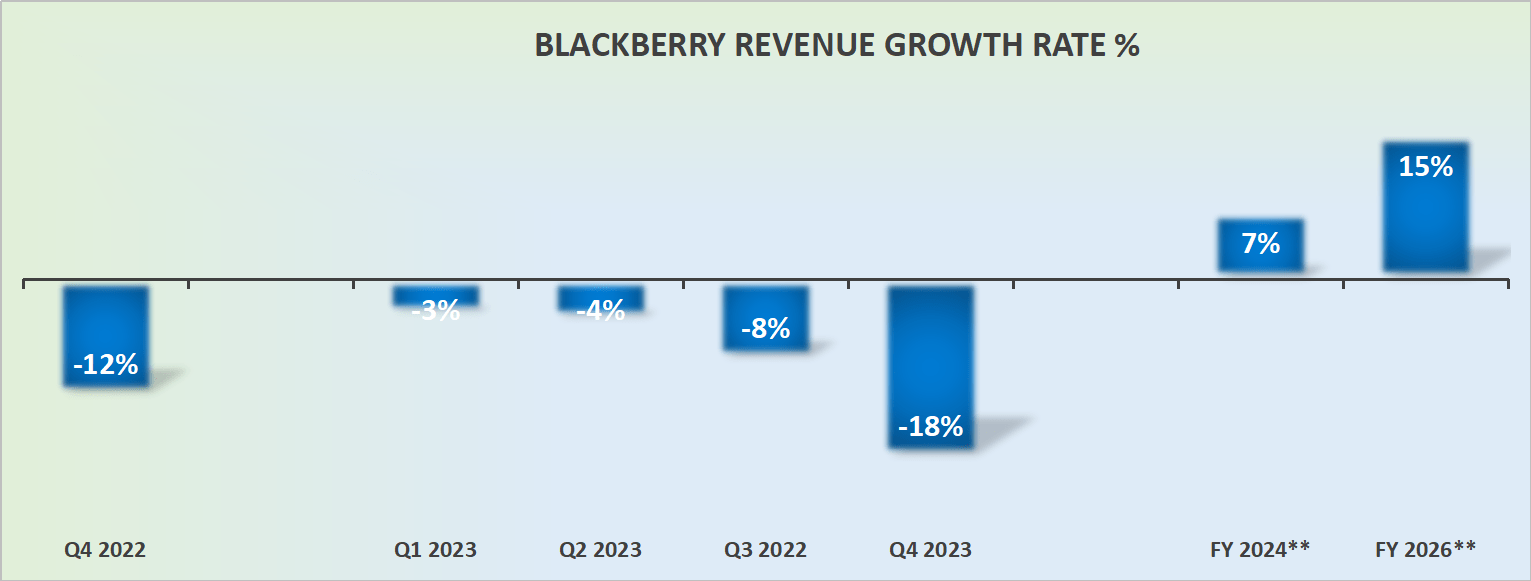

For the most part, over the past several years, BlackBerry has reported negative y/y revenue growth rates.

BlackBerry has had the occasional good quarter where it reports positive revenue growth rates, for instance, when it acquired Cylance in 2019, although Cylance has mostly been written off since.

Accordingly, here's a company that has a history of delivering negative revenue growth rates. And yet, looking ahead to fiscal 2024 , the fiscal year that BlackBerry is in right now, BlackBerry is guiding for approximately 7% growth.

Given inflation and other opportunities to raise prices, this growth rate is a possibility. Even though, I would rapidly respond that BlackBerry has had numerous back-to-back quarters of easy comparables, and yet delivered disappointing negative revenue growth rates.

And yet, looking ahead beyond fiscal 2025, out to next year, BlackBerry is intimating that it's going to grow by around the mid-teens CAGR? I simply fail to buy into this allusion.

The Bull Case in Focus

{kind=link}

BlackBerry has for many years disappointed its shareholders. Now, BlackBerry guides that it expects to reach non-GAAP profitability in Q4 of this fiscal year, and then proceed to remain non-GAAP EPS positive and cash flow positive.

Now consider this, neither of these metrics takes into account the substantial amount that BlackBerry capitalizes for intangibles each year (about $30 million) plus its stock-based compensation expense (a further $30 million). Hence, meaning that BlackBerry isn't actually guiding to be actually ''clean GAAP'' profitable anytime soon. It will be profitable only as a heavily adjusted figure.

I'm not inclined to pay even 4x forward sales for BlackBerry. There are significantly better businesses, in better shape, trading just as cheaply as BlackBerry. This one is not for me.

The Bottom Line

I believe BlackBerry Limited stock is overvalued, and I have my doubts about its prospects.

While the company predicts a revenue growth rebound next year, I remain skeptical. Moreover, BlackBerry's balance sheet raises concerns.

This is despite the fact they sold some patents for around $170 million. Further, their historical revenue growth rates have been negative, and their projections for future growth seem optimistic. Even if they reach non-GAAP profitability, it excludes significant expenses. Personally, I wouldn't pay 4x forward sales for BlackBerry when there are better businesses trading at similar valuations.

For further details see:

BlackBerry Stock: Valuation Vs. Reality, Patent Sales, And Profitability Woes