BL - BlackLine: Insufficient Reward To Stay Invested

2023-05-30 14:00:00 ET

Summary

- BlackLine, a financial software company, has experienced a 25% decrease in its share price year-to-date due to high valuation and growth deceleration.

- The company faces competition from larger software powerhouses and carries net debt.

- With no valuation appeal at the moment, it's best to remain on the sidelines here.

After two years of nearly unstoppable growth, tech stocks are having somewhat of a crisis of identity this year as investors pummel the sector for high valuations and lack of profitability. With interest rates persistently high and the tough macro environment preventing corporate IT spending from fueling enterprise software growth, many investors are bracing for continued weakness in the sector.

Most tech stocks are up slightly on the year after being hit hard at the tail end of 2022; but for BlackLine (BL), the pain has only continued. This financial software company, specializing in the period-end close process, is down nearly 25% year-to-date. The diagnosis behind this crumble is a function of both BlackLine's high valuation experiencing a course-correction, as well as the inherent pessimism around the company's growth deceleration.

The question for investors now is: is BlackLine a rebound buy? There's no doubt about it: times are tough for BlackLine. To understand why, it's important to note that BlackLine's software is rooted on deep process automation for the department of the CFO, designed specifically to eliminate manual work and labor for accounting teams that deal with month-end/quarter-end close.

There are two ways of reading the tea leaves here. On one hand, we can say that similar to other software companies, the tough macro environment and sliced IT budgets are going to lead to de-prioritization of transformational software projects like BlackLine. This reality, in fact, is baked into BlackLine's results as its growth slows down to the mid-teens. On the other hand, however, we could also infer that the fact that companies are laying off staff across the board (especially in G&A, or general and administrative, departments like Finance that are not directly tied to either product development or revenue growth) means that companies will eventually seek permanent ways to slim down headcount and rely on technology instead of salaried number-crunchers.

The former is BlackLine's current reality; the future is the company's future opportunity set as corporate leaders are far more attuned to optimizing opex decisions. I see the company now as a mixed bag and am revising my opinion on BlackLine to neutral.

A balanced bull and bear thesis; valuation update

I see both bullish and bearish drivers for BlackLine. Here, in my view, are all the things going in the company's favor:

- Despite niche features, BlackLine is a true horizontal software product with big-hitting clients across industries. Finance departments are prevalent in every industry, and BlackLine's customer base includes heavy manufacturing giants like Boeing ( BA ), energy companies like Chevron ( CVX ), fellow tech companies like Salesforce ( CRM ), and hospitality names like Hyatt ( H ). The diversity of BlackLine's customer base, plus its name-brand recognition across industries, is a big plus for this company's expansion potential, especially into smaller middle-market companies where its next leg of growth opportunities lies.

- Large TAM- Despite its positioning as a niche company, BlackLine estimates its total addressable market ("TAM") at $28 billion, meaning the company's current ~$500 million revenue run rate is only a fraction penetrated into this market opportunity.

- Cost controls- In the face of slowing growth, BlackLine has done a good job at belt-tightening and not growing opex, which is leading to substantial profitability growth.

At the same time, however, I see the following two risks for the company:

- Fierce competition from larger names- SAP ( SAP ), Oracle ( ORCL ), and Workday ( WDAY ) are the powerweights in the financial software space. Companies may be itching to automate manual processes, but there is also a benefit to bringing tech solutions under one umbrella - and so companies already using one of these big platforms for their main finance functions may elect not to use another software provider for niche processes.

- Heavy debt- Unlike many other enterprise SaaS companies, BlackLine is in a relatively deep net debt position, which gives it far less financial flexibility.

Though BlackLine is not as expensive as it was pre-correction, the stock isn't exactly a value trade either. At current share prices near $51, BlackLine trades at a market cap of $3.1 billion. After we net off the $1.09 billion of cash and $1.39 billion of debt on the company's most recent balance sheet, BlackLine's resulting enterprise value is $3.4 billion.

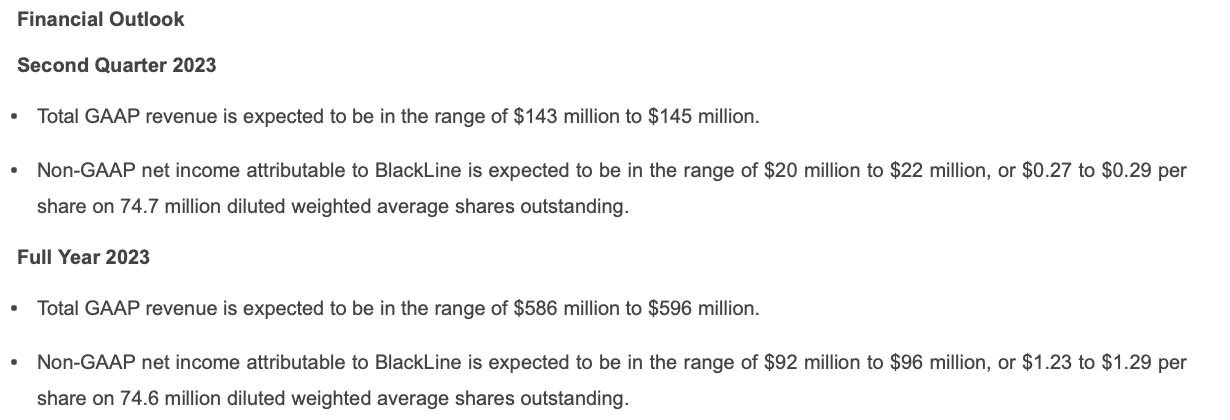

For the current fiscal year, meanwhile, BlackLine has guided to $586-$596 million in revenue, representing relatively meager 12-14% y/y growth. At the midpoint of this revenue range, BlackLine's valuation stands at 5.8x EV/FY23 revenue.

{kind=link}

Not cheap and not terribly expensive; but at the moment, I need a hefty valuation buffer to consider investing in SaaS names. I'm willing to buy back into BlackLine if the company keeps sinking to $39, a price target that represents 4.5x EV/FY23 revenue and ~25% downside from current levels.

Keep this stock around on your watch list - but don't be tempted to buy in just yet.

Q1 download

Let's now go through BlackLine's latest quarterly results in greater detail. The Q1 earnings summary is shown below:

{kind=link}

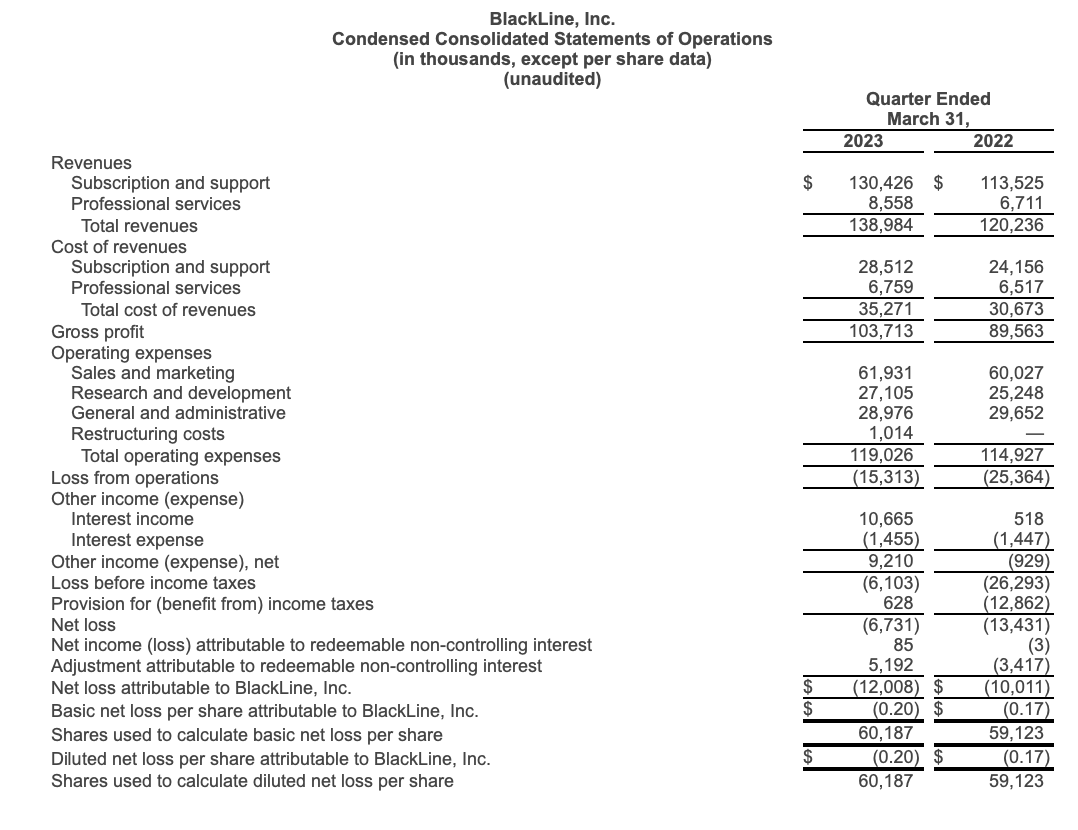

BlackLine's Q1 revenue grew just 16% y/y to $139.0 million, barely exceeding Wall Street's expectations of $138.2 million (+15% y/y). Even more notably, BlackLine's revenue decelerated sharply from 21% y/y growth in Q4 - a reflection of the hardships that the current macro environment has cast upon software companies, particularly large and complex integrations like BlackLine.

Customer growth has also been very slow. The company added just 48 net-new customers in the quarter to end at 4,236 total customers. Furthermore, net revenue retention rates fell to 106%, while billings growth of 14% y/y indicates that further deceleration is on the horizon (as seasoned software investors are aware, billings represents a better forward-looking indicator of growth as it captures deals signed in the quarter that will not be recognized as revenue until future quarters).

BlackLine noted that while it saw particular strength from its relatively nascent business in Japan, globally the company is experiencing sharp macro headwinds that is causing a delay in deal closings. Per co-CEO Owen Ryan's remarks on the Q1 earnings call:

I want to focus for a moment on what we delivered in the first quarter and the current market environment. What we are experiencing today is quite different than it was a year ago. I recognize that this is not a unique view and the impacts are not specific to BlackLine.

We are still seeing extended deal cycles as customers and prospects contended with the various challenges they presently face in their own businesses. Some of these are specific to the industries they operate in and others are influenced by the geographies they serve. For example, we have seen signs of strength in APAC particularly in Japan. Our enterprise business remains a steady performer, while middle market remains softer with relatively subdued deal activity."

The bright side here is profitability, which is a good silver lining in an otherwise tough quarter especially as investors focus more on the bottom line. Pro forma gross margins of 78.9% expanded 90bps y/y. In addition, BlackLine's cost controls have total pro forma operating expenses about flat at $94.1 million, up only 1% versus $93.3 million in the year-ago quarter - with cuts in G&A spending offsetting slight growth in sales and marketing and R&D costs. Pro forma operating income, meanwhile, soared to $15.6 million, representing an 11% margin - versus just 1% in the year-ago quarter.

Key takeaways

Amid slowing growth and a valuation that doesn't exactly necessitate immediate action, I'm content to move to the sidelines on BlackLine. It remains to be seen whether BlackLine can capitalize on its pockets of growth (such as its strong Japan trends) and whether this can counteract competitive pressures from larger software brands. At the moment, I'm leaning towards a risk-off approach here.

For further details see:

BlackLine: Insufficient Reward To Stay Invested