BL - BlackLine: Losing Firepower (Rating Downgrade)

2023-08-13 20:56:43 ET

Summary

- BlackLine, a financial software company, has seen sharp declines in its share price corresponding to decelerating revenue growth.

- Macro challenges are gating customer upgrades and slowing down new wins.

- BlackLine is resorting to more reseller partners to drive higher win rates.

- On the flip side, profitability is improving, but BlackLine's valuation is still not cheap enough to consider investing in.

Suddenly all at once, investors' confidence in the recent rally seems shaken. Earnings season is in full swing, and even though most results are coming in well above expectations, small beats to guidance aren't enough to offset investors' fears that valuations have hit highs again and that the risk premium to holding equities is sufficient enough to convince investors to shift away from high-yielding cash and bonds.

BlackLine ( BL ), a financial software company that specializes specifically on the period-end close process, is one of the few software companies to see sharp y/y declines in its share price. Down more than 25% year to date, losses have accelerated for BlackLine in the month of August as the company posted lackluster quarterly results.

While I commonly advocate for buying fallen-angel tech stocks on dips, I don't think BlackLine has quite reached the value threshold yet. In my opinion, I'm not confident enough in the company's growth drivers to bank on a fundamental-related rally, and especially as current macro conditions push more and more companies to cut back on G&A related functions like finance, implementation-heavy projects like BlackLine will continue to get pushed.

Earlier this year, I was neutral on BlackLine. At the time, I had posited that the company's positive profitability progress was offset by slowing top-line growth, but ultimately that its valuation sat at multiples that were neither opportunistic nor risky. Now, however, with growth slowing down more substantially to the low teens, I am now fully bearish on this stock. To me, here are the key risks that BlackLine faces:

- Fierce competition from larger names. SAP ( SAP ), Oracle ( ORCL ), and Workday ( WDAY ) are the powerweights in the financial software space. Companies may be itching to automate manual processes, but there is also a benefit to bringing tech solutions under one umbrella - and so companies already using one of these big platforms for their main finance functions may elect not to use another software provider for niche processes.

- Slow customer growth. BlackLine barely manages to add ~50 customers every quarter. This is a signal that BlackLine is a complex, heavy implementation project that requires long sales cycles that are incredibly difficult to close in a tough macro environment.

- Heavy debt. Unlike many other enterprise SaaS companies, BlackLine is in a relatively deep net debt position, which gives it far less financial flexibility.

Valuation isn't much of a draw for BlackLine either. At current share prices near $50, BlackLine trades at a market cap of $3.04 billion. After we net off the $1.13 billion of cash and $1.39 billion of convertible debt on BlackLine's most recent balance sheet, the company's resulting enterprise value is $3.30 billion.

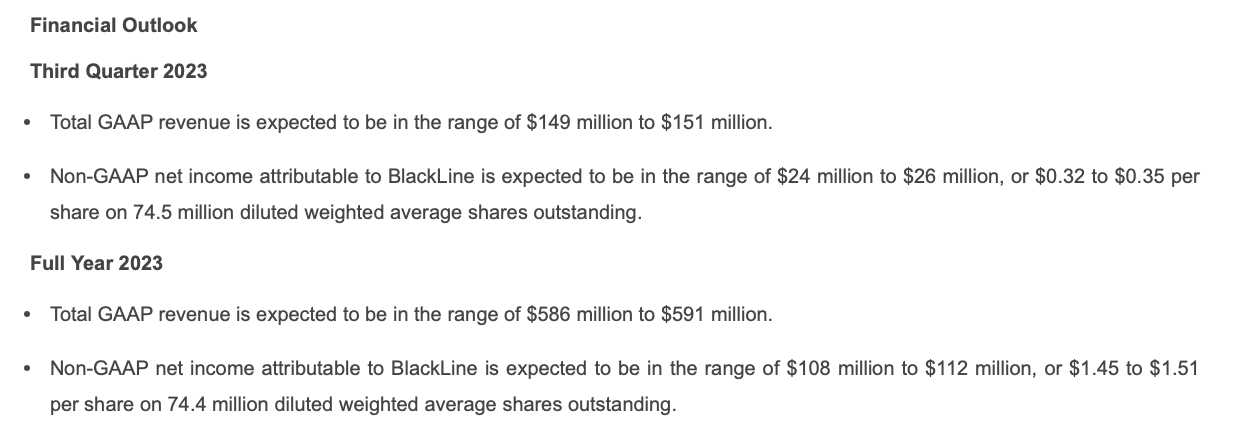

Meanwhile, for the current fiscal year, BlackLine has updated its guidance to $586-$591 million in revenue, or 12-13% y/y growth. It cut $5 million from the high end of its guidance range, citing deeper macro headwinds and its expectations for a flatter back-half recovery across Q3 and Q4.

BlackLine outlook (BlackLine Q2 earnings release)

{kind=link}

This puts BlackLine's valuation at 5.6x EV/FY23 revenue - not expensive, of course, but not cheap enough to warrant any near-term rebound without specific fundamental catalysts to drive growth.

All in all, I find very few reasons to stay invested in BlackLine. Sell the stock here and reinvest elsewhere.

Q2 download

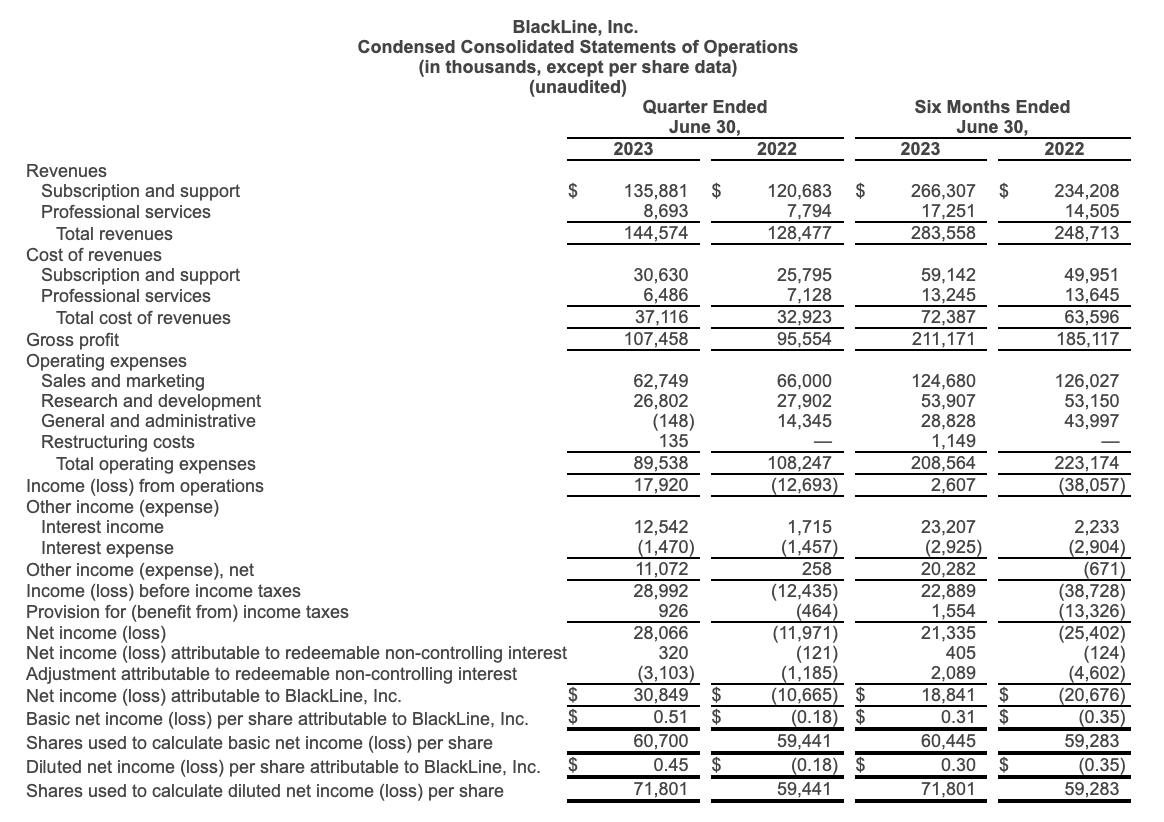

Let's now go through BlackLine's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

BlackLine Q2 results (BlackLine Q2 earnings release)

{kind=link}

BlackLine's revenue grew 13% y/y to $144.6 million, only slightly ahead of Wall Street's expectations of $144.0 million (+12% y/y). Of note is the fact that revenue decelerated quite sharply from 16% y/y in Q1, and 21% y/y in Q4 - so in light of this decay in growth rates, it's no big wonder why BlackLine's valuation multiples have compressed and the stock has lost momentum since the start of the year.

To its credit, BlackLine is aware of its revenue underperformance and taking actions to try to resuscitate recent trends. Internally, the company is combining its business development and sales teams under the same leadership, in an attempt to unify and improve end-customer outcomes. Externally, the company is relying more and more on its partner network to drive new deals and work on implementations. BlackLine noted that it entered into a reseller agreement with a "blue chip global consulting firm" to broaden BlackLine's presence in the field. The company noted that partners were involved in 80% of large deals in Q2 alone.

Here is commentary from CFO Mark Partin's prepared remarks on the Q2 earnings call, detailing the macro environment and the reason behind the full-year guidance cut:

Net revenue retention remained stable at 106% as we continue to experience a lower velocity of customer expansion activity due to persistent macro uncertainty. Strategic product performance represented 20% of sales. Partners were involved in 80% of large deals this quarter driving both net new and expansion deals globally as we continue to enable, train and drive higher levels of partner activity [...]

As we enter 2023, we expected to see a slight improvement in market demand in the back half of the year. However, as we closed out the second quarter and based on current trends, we now see a slightly flatter demand profile for the back half of the year. As such, we are taking the high end of our previous range off the table and adjusting our full year revenue expectations to reflect this."

We'll call out, however, that in the face of weaker demand BlackLine has succeeded at growing its bottom line and focusing on expenses. Year over year on a pro forma basis adjusting for stock comp, the company managed to reduce sales and marketing expenses by ~2% and general and administrative expenses by ~14%. Combined with strong pro forma gross margins at 78.8% (+10bps y/y), BlackLine grew pro forma operating income to $19.3 million, or a 13.3% margin versus just a 2.1% in the year-ago Q2.

Key takeaways

BlackLine's improvements to profitability are admirable, but the company is nowhere near profitable enough to justify its $3+ billion market cap - and as such, its decelerating revenue growth is going to take center stage as the year goes on. Unfortunately, I don't see material drivers for BlackLine to get its growth rate back up to the 20s, and as such its >5x forward revenue multiple is difficult to defend. Continue to exercise caution here.

For further details see:

BlackLine: Losing Firepower (Rating Downgrade)