BL - BlackLine: Margin Gains Offset By Weaker Growth

2023-11-14 01:22:08 ET

Summary

- BlackLine, an accounting and finance software company, has seen a 20% decline in its stock price this year due to weak growth and lower renewal rates.

- The company faces fierce competition from larger players like SAP, Oracle, and Workday, and relies heavily on reseller partners for sales.

- BL's heavy debt and unappealing valuation make it a risky investment, and it may struggle to achieve its revenue targets for next year.

With markets roaring back to year-to-date highs, I continue to advocate for extremely selective stock-picking all the way through next year. It's a great time to review underperforming names and make sure they're not sitting in our portfolios when the opportunity cost is a 5% risk-free interest rate.

BlackLine ( BL ), in my view, will have further downside. This accounting and finance software company has slid more than 20% year to date, almost a complete reversal from many of its mid-cap software peers that are up by roughly the same amount since the start of January. Weak growth is the culprit, and even profitability gains earned via layoffs were not enough to get investors excited about this name again.

Risks for BlackLine are mounting with each passing quarter

I last wrote a bearish opinion on BlackLine in August, when the stock was trading at similar levels. Since then, the company has released Q3 results that gave me even more conviction in my bearish outlook: we'll discuss details in the next section, but on top of growth deceleration, the company is reporting weaker renewal rates.

I see a number of red flags with this company, including:

- Fierce competition from larger names. SAP ( SAP ), Oracle ( ORCL ), and Workday ( WDAY ) are the powerweights in the financial software space. Companies may be itching to automate manual processes, but there is also a benefit to bringing tech solutions under one umbrella - and so companies already using one of these big platforms for their main finance functions may elect not to use another software provider for niche processes.

- More and more sales share is going to reseller partners. More than three-quarters of BlackLine's large deals have partners involved. While this may help the company in the short term to chase growth without investing in opex, in the long run this may cede too much revenue share away.

- SAP concentration. More to the point above, the company noted that in Q3, 25% of its revenue came from its partnership with SAP, which is also a competitor to BlackLine in the end-to-end financial accounting software stack.

- Heavy debt. Unlike many other enterprise SaaS companies, BlackLine is in a relatively deep net debt position, which gives it far less financial flexibility.

Valuation update

It makes perfect sense, then, that BlackLine isn't exactly a premium growth stock - but at the same time, BlackLine's valuation isn't exactly appealing enough to invest in either.

At current share prices near $51, BlackLine trades at a market cap of $3.13 billion, and after netting off the $1.16 billion of cash and $1.39 billion of convertible debt on BlackLine's balance sheet, the company's resulting enterprise value is $3.36 billion.

Meanwhile, for next year FY24, Wall Street analysts are expecting the company to generate $1.81 in pro forma EPS (+19% versus this year's $1.52 consensus) on $667.3 million in revenue, representing 13% y/y growth. The underlying revenue target may be difficult to achieve, given growth has already decelerated below those levels - but nevertheless, taking consensus estimates at face value, BlackLine trades at:

- 5.0x EV/FY24 revenue

- 28x FY24 P/E

Neither of these multiples screams value. And so what do we have here? A mid-cap software company that has already reached a saturated, mature phase of its lifecycle with slowing growth and few upside catalysts - in my view, it's best to stay on the sidelines and invest elsewhere, as I think a risk-free 5% return on cash will solidly outperform this name throughout next year.

Q3 download

Let's now go through BlackLine's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

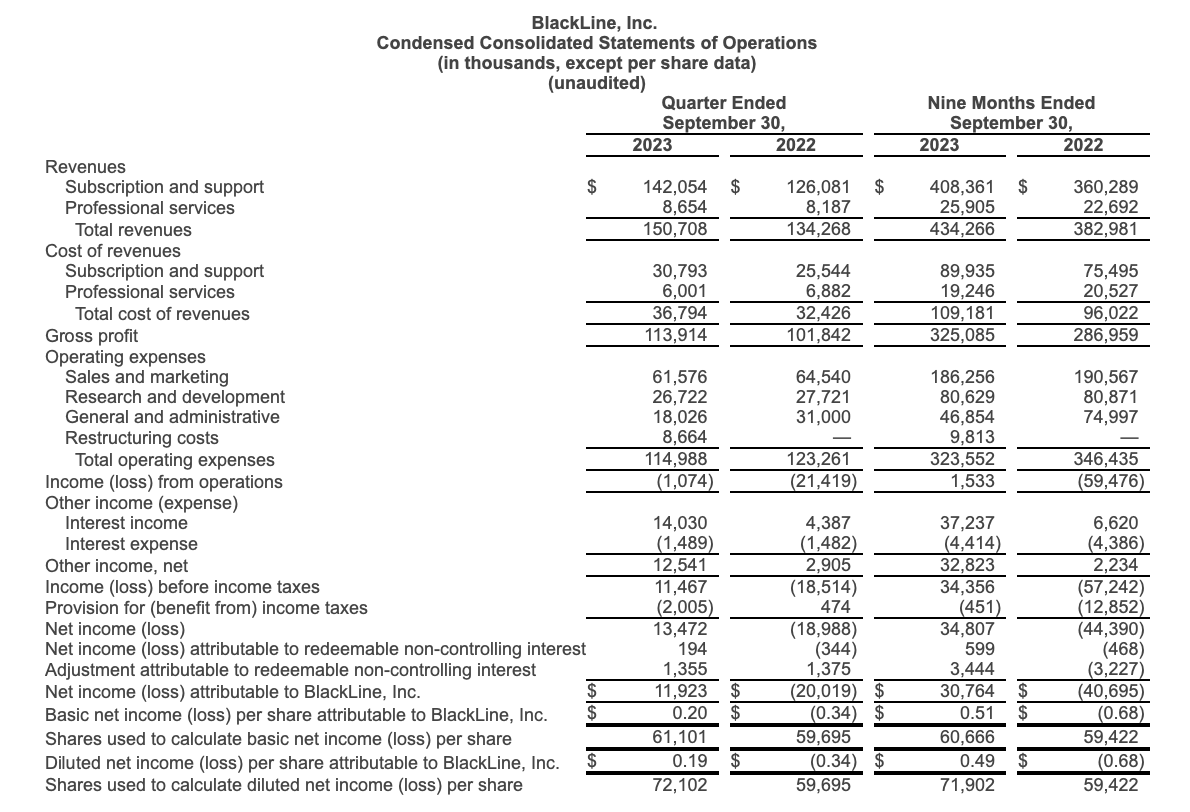

Revenue grew only 12% y/y to $150.7 million, effectively in line with Wall Street's slightly more modest expectations of $149.9 million. Growth also decelerated from 13% y/y in Q2, which in turn was much weaker sequentially than 16% y/y growth in Q1. It's a far cry from the pandemic era when BlackLine stock was rallying (at one point hitting above $120 in early 2021) when the company was still growing at a mid-20s clip.

But as with most situations, there are both risks and opportunities here, and I would be remiss not to mention the largest one for the company: mid market. Unsurprisingly, most of BlackLine's revenue to date has been from larger enterprise clients that have sophisticated accounting departments looking to improve their close process. But a large opportunity exists in mid-market, where these less-sophisticated finance departments use a combination of software tools and Microsoft Excel ( MSFT ) to close their quarters.

Mid-market strength is the reason that BlackLine added 89 net-new customers this quarter (to end with a total of ~4.4k customers), sequentially much stronger than 40-50 net adds over the past few quarters. (It should be noted as well that BlackLine hosted its annual customer conference in Q3, which may also have provided a bump to new deal signings).

Per founder and co-CEO Therese Tucker's remarks on the Q3 earnings call surrounding the mid-market opportunity for BlackLine:

When we segmented the market opportunity, we saw that mid-market customers often lack a modern end-to-end consolidation solution and customers typically use a combination of manual processes and excel. Sounds familiar? While not required when customers combine FRA with our existing financial close solutions, BlackLine can provide a complete end-to-end platform for close and consolidation, which is a very powerful value proposition and offers a real competitive advantage.

Looking up market, we've already seen adoption by several large enterprise companies using BlackLine as a tool to assist with consolidation efforts. However, to be successful across both the enterprise and mid-market requires more than just a market-leading product. We need domain expertise, customer feedback and collaboration from our partners to succeed. So that's where we've spent considerable time and effort running these efforts in parallel with our product development teams. Through existing customer advisory boards, many who purchased FRA and are now using it for consolidation, along with partner groups, we are aligning our road map to evolving industry trends while ensuring that customer experience is top of mind. The enthusiastic reception from our customers as we extend further into the record-to-report process is validation of our efforts and our strategy."

Unfortunately, this mid-market opportunity is offset by other go-to-market weaknesses. Renewal rates in the quarter fell to 94%, as the company cited many of its customers are opting not to renew or to shrink seat counts in an attempt to conserve on budgets and consolidate the number of software vendors they use.

Net revenue retention rates also softened to 105%, versus 106% in the past two quarters, driven not only by weaker renewal but by tempered expansion activity within the current install base.

Meanwhile, profitability did rise, driven by the company's decision to lay off just under 10% of its workforce earlier this year.

{kind=link}

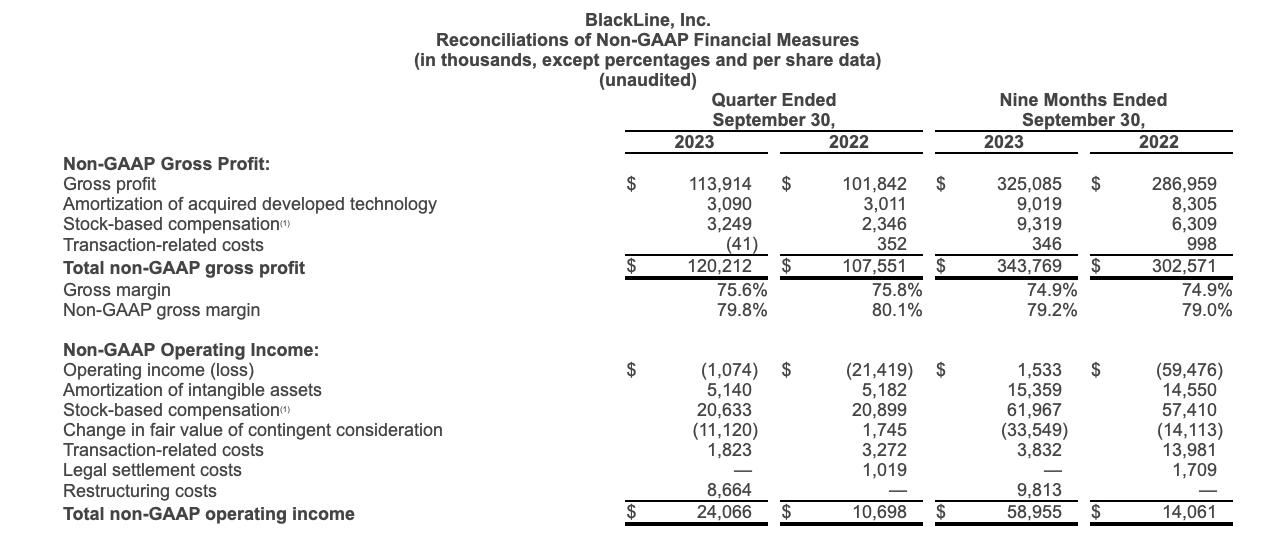

Building on a high gross margin (which remained flat y/y on a pro forma basis at ~80%), pro forma operating income more than doubled to $24.1 million, representing a 16% pro forma operating margin - versus just 8% in the year-ago quarter. Unfortunately, however, there is only so much that layoffs and cost-cutting can do to spark profit growth - and without meaningful top-line growth going forward, BlackLine's ability to justify its ~28x P/E will be limited.

Key takeaways

I continue to see limited incentives to invest in BlackLine as the company struggles with muted growth rates. In my view, the recent downtrend in this stock has further room to go (BlackLine could fall to a ~4x revenue multiple). Buying mid-2024 puts on this stock is a great way to capitalize on weakness here.

For further details see:

BlackLine: Margin Gains Offset By Weaker Growth