BL - BlackLine: Multiple Growth Drivers (Rating Upgrade)

2023-08-07 13:12:27 ET

Summary

- BlackLine's key growth drivers include its partnership with SAP, the new Accounting Studio product, and expansion opportunities in Asia-Pacific.

- BL's current valuations are below historical averages and what its key peers are trading at now.

- I raise my rating for BlackLine to a Buy, taking into account both the company's growth potential and the stock's valuation metrics.

Elevator Pitch

My rating for BlackLine, Inc. ( BL ) stock is a Buy. I reviewed BL's financial performance for the final quarter of 2022 in my February 28, 2023 initiation article .

With this latest update, I upgrade BL's rating from a Hold to a Buy. BlackLine has multiple growth drivers such as geographic expansion in Asia, a new product, and a key partnership. I am of the view that BL deserves to trade at a higher valuation multiple in consideration of its long-term growth prospects, which explains my Buy rating for BlackLine.

Key Partnership

In the company's fiscal 2022 10-K filing , BL highlighted the company's key partners like "technology vendors such as SAP ( SAP ) and Microsoft ( MSFT ) Dynamics, professional services firms such as Deloitte and Ernst & Young and business process outsourcers such as Cognizant ( CTSH ), Genpact ( G ) and IBM ( IBM )."

BlackLine's partnerships are a key driver of its future growth, and it is worth paying attention to BL's collaboration with SAP in particular. On its corporate website , BlackLine refers to itself as "an SAP platinum partner with a global reseller agreement under which BlackLine's cloud-based solutions are offered as SAP Solution Extensions" otherwise known as SolEx.

The company's partnership with SAP contributed approximately a quarter of its Q1 2023 top line as indicated at its first quarter earnings briefing . But BL revealed at JPMorgan's ( JPM ) 51st Annual Global Technology, Media and Communications Conference on May 23, 2023 that it is estimated to have achieved a mere 10% penetration rate with SAP's clients.

As disclosed in its Q1 2023 results presentation slides , BlackLine boasted a 4,200-strong customer base as of the end of March this year. However, only about 1% of BL's clients generate in excess of $1 million in yearly revenue for the company. As such, there are substantial upselling opportunities associated with the SAP partnership.

The SAP partnership also played a key role in BL's geographic expansion plans as detailed in the next section.

Geographic Expansion

BlackLine derived 71% and 29% of the company's FY 2022 sales from the US and foreign markets, respectively as per its 10-K filing. It is noteworthy that no single geographic market, apart from the US, accounted for over 10% of BL's top line last year.

At the company's Q1 2023 results call, BL mentioned that its SAP or SolEx partnership witnessed "a number of new global customers beginning their transformation journeys with BlackLine", particularly new clients coming from Japan.

Earlier, Seeking Alpha News reported that BlackLine strengthened "its APAC region presence by opening a new office and plans to launch a new data center within a Google Cloud facility in Sydney, Australia." With its Asia-Pacific business accounting for close to 10% of its clients, it is easy to understand why BL has recently expanded in Sydney, which is where the company's Asia-Pacific headquarters sits.

As highlighted above, it is clear that BL's current revenue is too concentrated in its home market, the US, and there is a compelling need for the company to seek new growth drivers in international markets. Therefore, it is encouraging to see BlackLine trying to grow its business operations in foreign markets outside the US through various means such as partnerships and new facilities.

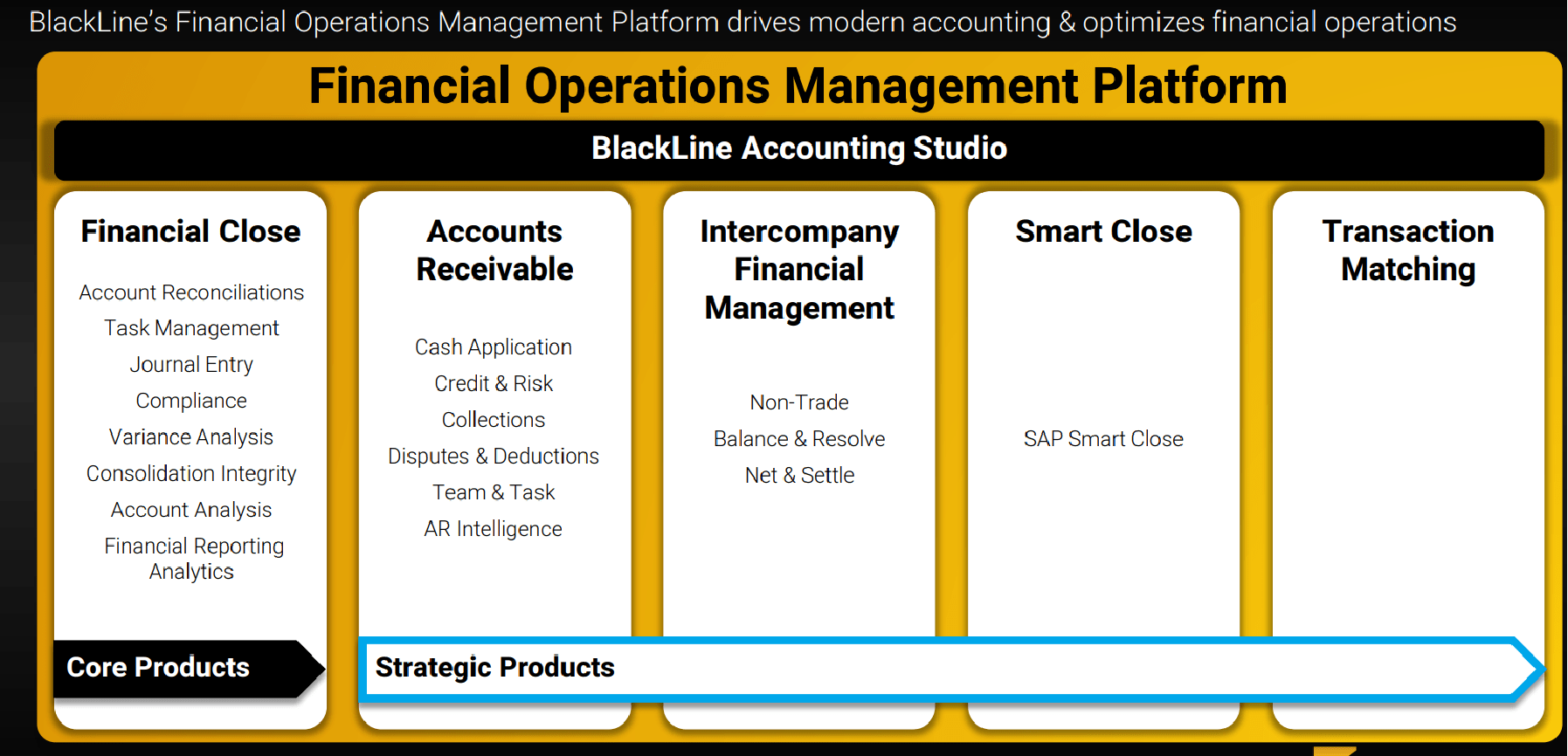

New Product

In November last year, Blackline announced that it will be introducing a new product known as Accounting Studio in the second quarter of 2023. In its announcement, BL described Accounting Studio as a platform to "unify BlackLine's existing solutions" and "configure standardized process workflows with end-to-end automation."

BlackLine's Key New Product, Accounting Studio

{kind=link}

BL's new product, Accounting Studio, appears to be gaining good traction with the company's customers in the initial stage of its launch. BlackLine disclosed at its Q1 earnings call that it has witnessed "more and more early adopter customers sign up" for Accounting Studio.

More importantly, there is the potential for BL's revenue mix to become more favorable with sales contribution from the Accounting Studio product. At the JPM Global Technology, Media and Communications Conference in late May, BlackLine emphasized that Accounting Studio will be priced in a manner such that the company is "getting paid back a (share of the) value of what you bring to the customer." In other words, BL is hinting that its pricing model for Accounting Studio will allow it to maximize the profitability generated from the new product's sales, and the new Accounting Studio is likely to be a higher-margin offering as compared to the company's other solutions.

Long-Term Growth Targets And Valuations

BlackLine is now valued by the market at 5.9 times consensus forward next twelve months' Enterprise Value-to-Revenue as per S&P Capital IQ's valuation data. BL's peers, Paylocity Holding Corporation ( PCTY ) and Five9 ( FIVN ) are currently trading at relatively higher consensus forward next twelve months' Enterprise Value-to-Revenue multiples of 8.0 times and 6.2 times, respectively. BlackLine's five-year mean consensus forward Enterprise Value-to-Revenue valuation metric is also higher at 10.4 times (source: S&P Capital IQ) .

In my opinion, BL's valuations are most likely going to get closer to peer and historical averages when the company meets its growth targets for the long run. BL specifically noted at the May 2023 JPMorgan Global Technology, Media and Communications Conference that it has the confidence to "achieve a 20% to 25% (top line) growth" (versus +13% FY 2023 consensus revenue growth estimate) by virtue of being "a leader in the market with our growth levers." I have touched on BlackLine's major growth drivers in the earlier sections of this article, which I view as supportive of the company's long-term financial goals.

Closing Thoughts

BL's current valuations are below that of its peers, and also lower than what the stock was valued on average historically. But there are multiple growth drivers that could drive a re-rating of BlackLine's valuations in time to come, which supports my Buy rating for BL.

For further details see:

BlackLine: Multiple Growth Drivers (Rating Upgrade)