BKCC - BlackRock Capital: Could Be Another Yield Trap

2023-10-18 16:24:23 ET

Summary

- BlackRock Capital Investment Corporation offers a high dividend yield of 12%, but it is likely a poor investment for most investors.

- BKCC invests in highly speculative debt securities and loans from troubled middle-market companies.

- The company has a history of poor performance, with a 77% decline in share price since inception and declining dividend distributions.

BlackRock Capital Investment Corporation ( BKCC ) is a business development company with a mouth-watering dividend yield of 12% but it also has every indication of being a poor investment for the majority of investors in my view.

The company invests into secured and non-secured debt securities and loans from middle-market companies (market values ranging from $100 million and $1.5 billion) utilizing BlackRock (BLK) as its main advisor and most of its investments are highly speculative in nature. A great majority of companies that borrow from BKCC have trouble borrowing from elsewhere due to either having bad credit ratings, no credit rating or being in trouble. Large banks and regional banks generally both see these companies as too risky for investment and this can make it very difficult for these types of companies to borrow. This is why they come to business development companies and agree to pay very sizeable interest rates.

Many of the company's loans are "secured" by assets of the borrowing company but I wouldn't put too much faith in this since those assets can usually go for a fraction of their reported value if the company were to go bankrupt. A factory being valued at $20 million pre-bankruptcy might have trouble finding buyers for $5 million as an example, making secured loans not so secured after all.

Typically when the economy is strong business development companies perform very well because they make a leveraged bet in favor of the overall economy. One could also say that these companies bet on the status of capital availability or ease of reaching liquidity since that's the bread and butter of troubled companies. Troubled companies can stay alive for a long time as long as they can access capital and keep rolling their debt but as soon as liquidity starts drying up and capital becomes tight, they often find themselves in deep trouble. The issue with BKCC is that it was performing poorly even during the best of times in terms of access to capital and liquidity. When the Fed was literally printing money and interest rates were kept near zero from 2009 to 2021, this company still had trouble turning this favorable situation into high performance.

The company has been around for almost 17 years and its share price is down -77% since inception and its total return is only 53%, corresponding to an average annual return of 2.6% which barely keeps up with the inflation.

Not only that but the company's dividend distributions have also been on a sharp decline during this time. In the last 17 years, the fund's dividend payments dropped from 42 cents per share to 10 cents per share which is a drop of 77%. After accounting for inflation, the real drop is higher than 90% during this time. Many times people who invest their money into high-yield stocks and bonds say that they plan on keeping their investments forever and don't care about share price fluctuations as long as dividends keep coming in, but this kind of thinking could result in shrinking income over time.

Since its IPO in 2007, the company's net income is down by as much as -92%. This also explains why dividends kept shrinking. As the company's NAV and assets keep shrinking, its income will also keep shrinking because it has less assets to earn income from. I believe this will result in even smaller dividends and a shrinking share price. This kind of business is not sustainable in the long term in my view.

The company currently trades at a price-to-book-value ratio of 0.79 indicating that it's selling for a 21% discount against its book value. Some could say this amount of discount provides some level of safety but I don't agree that there is any amount of discount that can provide safety when a company's book value keeps shrinking at a rapid rate.

If the company was having so much trouble when the economy was growing nicely, the Fed was extremely accommodative and capital markets were flush with liquidity, how will it perform well when things get tough?

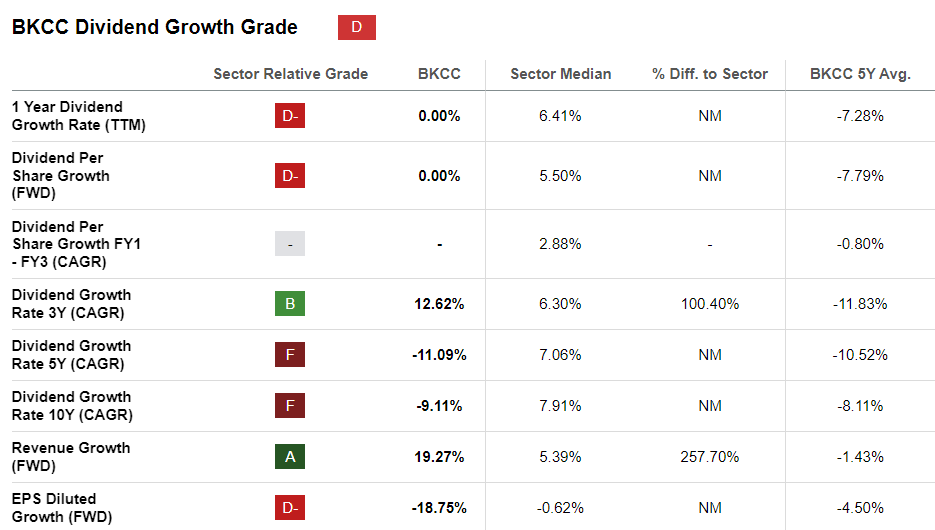

The company's dividend history looks pretty poor no matter how you cut it. It's 1-year dividend growth of 0% falls well below the sector median of 6.41%. The company's expected forward dividend growth of 0% is also well below sector average of 5.5%. The company's 5-year and 10-year dividend average annual growth rate are -11% and -9% respectively.

{kind=link}

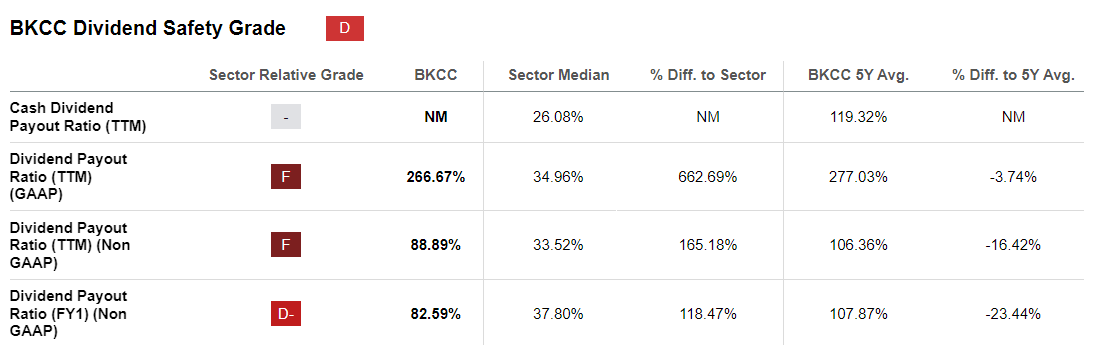

Things also look rather poorly from a dividend-sustainability perspective for BKCC. The company's payout ratio is 266% on a GAAP basis and 89% on a non-GAAP basis, both significantly above the sector median in the 30-35% range. This shows that the company's current earnings might not be able to cover its dividends and there might be further dividend cuts in the future. Since this company is designated as an "investment firm" for tax purposes it has to distribute virtually all of its earnings in dividends in order to avoid getting taxed, which explains why its payout ratio is so high but it also makes it incredibly difficult to sustain its current dividend in the long run as the company's earnings keep shrinking along with its book value.

{kind=link}

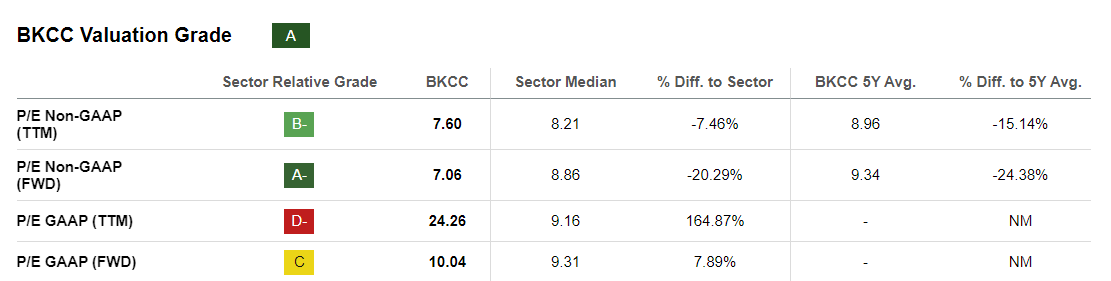

As much as valuations go, it depends on which metrics you look at. If you look at the company's P/E based on its adjusted non-GAAP earnings, it looks cheaper than the sector average with a P/E of 7 versus 8. On the other hand, if you look at GAAP figures, the company's trailing P/E of 24 and forward P/E of 10 both look higher than the sector average of 9. In general I would say that BKCC is fundamentally cheap but it's cheap for a good reason. This is an ever-shrinking asset that I believe will keep shrinking unless something dramatically changes.

{kind=link}

In conclusion, although this company's high yield and relatively low valuation (along with 21% discount against its book value) look tempting, this doesn't look like a good investment that will result in good returns for investors. In the past investors lost so much money trying to chase yield because they were desperate for income and there was no alternative but now that risk-free bonds are yielding 5.5%, investors have more options to pick from to generate income. If you absolutely must invest into business development companies, there are much better options out there such as Main Street Capital ( MAIN ) and Capital Southwest ( CSWC ) both of which have proven track records of outperforming for investors.

For further details see:

BlackRock Capital: Could Be Another Yield Trap