BKCC - BlackRock Capital Investment: 10.2% Yield And A Merger Catalyst

2023-12-12 05:10:44 ET

Summary

- BlackRock Capital's portfolio has improved in quality since I last covered the BDC in 2023, with a shift towards first lien positions and a decrease in nonaccrual loans.

- The merger between BlackRock Capital and BlackRock TCP Capital is expected to result in a better diversified portfolio and operational benefits.

- Currently, BlackRock Capital trades at a discount to net asset value, but the merger and improving portfolio quality could close this gap.

BlackRock Capital Investment ( BKCC ) is a small BDC following a first lien strategy and the company’s portfolio has fundamentally improved in quality in the last several years. In September, the BDC announced the merger between BlackRock TCP Capital ( TCPC ) and BlackRock Capital which is set to a larger, better diversified portfolio that will follow a first lien strategy as well. I believe the gap between share price and net asset value could close if the merger is successful. Currently, BKCC trades at an 11% discount from its net asset value and shares supply a solid 10% yield!

Previous rating

I recommended BlackRock Capital in April 2021 -- 10.6% Yield And 12% Discount To Net Asset Value -- because the BDC moved away from junior capital positions and chose to accentuate a first lien strategy. I believe the shift towards senior capital positions and the merger between TCPC and BKCC will leads to a more cost-efficient, diversified portfolio which may result in a share price revaluation and the closing of the gap between share price and net asset value.

Transformation of BlackRock Capital's portfolio and improved asset quality

BlackRock Capital has historically had credit issues which stemmed from its low-quality investment portfolio that included a lot of junior capital positions. In recent years, however, the BDC has moved away from junior capital positions and focused more on originating higher quality debt, chiefly first liens, which has helped improve the BDC’s portfolio quality. As of September 30, 2023, 85% of BlackRock Capital’s investments were first liens.

BlackRock Capital

Other assets, besides first liens, include second liens, unsecured debt, preferred equity and common equity, the total dollar values of which are displayed in the chart below. With a market value of $283M and a total portfolio value of $595M, BlackRock Capital is a very small BDC, however.

{kind=link}

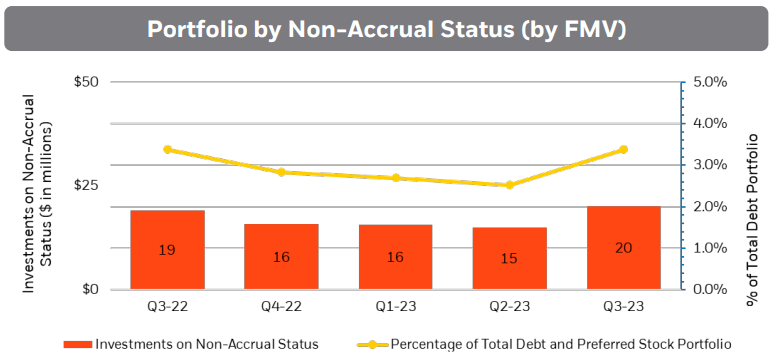

The transition away from junior capital positions to higher quality debt, first liens especially, has paid off for Blackrock Capital as its portfolio quality has improved over time. Since I last covered BlackRock Capital in 2021, the nonaccrual percentage has declined from about 5% to 2% meaning the company's credit quality has overall improved. Nonaccrual loans represent those loans in a BDC's portfolio that may not get fully repaid and may have to be written off completely. Now, Black Rock Capital’s credit issues are not fully resolved, but the portfolio looks a lot healthier than it did in 2021.

{kind=link}

The portfolio trend shows a dip in fair market value during the early stages of the pandemic, with the portfolio value bottoming out at $458M in Q1'21. The portfolio has consistently grown since Q1'21, however, and the FMV of BlackRock Capital's total investments has since risen 30% to $595M.

{kind=link}

Turning to BlackRock Capital's coverage trend.

The non-weighted quarterly dividend coverage ratio in the last five quarters was 119% implying that the BDC generates more than enough interest income from its debt investments that it can afford to pay its quarterly $0.10 per-share with ease. The trend in BlackRock Capital's dividend coverage is also favorable as the degree of coverage improved in every single quarter last year.

{kind=link}

Merger transaction may be a catalyst for share price revaluation

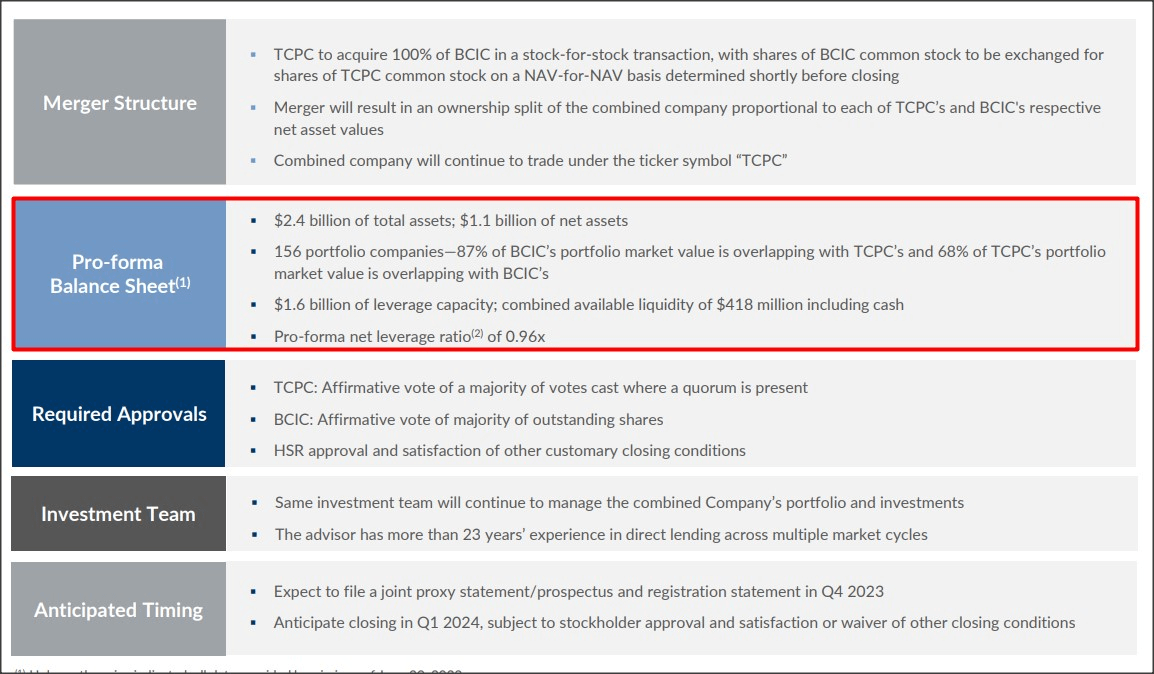

In the third-quarter, another BlackRock BDC, BlackRock TCP Capital, announced that it will acquire BlackRock Capital in a 100% stock transaction. The deal is meant to improve the company’s portfolio diversification and cost structure. The adviser, as an example, proposed to lower the management fee from 1.50% to 1.25% and cover 50% of the merger expenses (capped at $6M) related to the merger between BlackRock TCP Capital and BlackRock Capital.

The merger is expected to yield a BDC with $1.1B in net assets and an asset mix that is set to include 90% senior secured loans. First lien investments are expected to drop slightly to 78%, but the newly merged BDC will clearly be oriented towards senior secured loans.

{kind=link}

BlackRock Capital’s valuation

BlackRock Capital and BlackRock TCP Capital are both priced at a discount from their respective net asset value. BlackRock Capital is currently trading at a price-to-NAV ratio of 0.89X while BlackRock TCP Capital has a price-to-NAV ratio of 0.95X. In the last three years, BKCC has had an average P/NAV ratio of 0.83X... implying that shares are trading at an 8% premium to the average. I believe that BKCC could ultimately trade at net asset value, if it continues to sort out its remaining credit problems, and the merger may just be the catalyst that BlackRock Capital needs.

Risks with BlackRock Capital

BlackRock Capital has seen an improving nonaccrual trend in the last three years, but the current credit profile is far from perfect. The biggest risk that I see with BlackRock Capital affects other BDCs as well: the interest rate trend. It is more likely than not, in my opinion, that the Federal Reserve will lower interest rates next year which may result in weaker net interest income growth. What would change my mind about BlackRock Capital is if the implied merger benefits could not be realized and the net asset value, post-merger, would widen again.

Final thoughts

BlackRock Capital’s asset quality and nonaccrual trends have improved since I last worked on the BDC. The BDC is now driving a solid first lien strategy and even the merger with TCPC is not going to change this materially. BlackRock Capital’s dividend coverage also indicates that the dividend is very well supported by the BDC’s net investment income. I believe the merger between BKCC and TCPC offers operational benefits (reduced management fees) that the BDC would otherwise not be able to achieve. Since shares of BKCC and TCPC trade at discounts to net asset value and the merger is expected to result in cost and portfolio synergies, I believe the discount to net asset value could ultimately fully disappear... if the merger is completed successfully!

For further details see:

BlackRock Capital Investment: 10.2% Yield And A Merger Catalyst