BKCC - BlackRock Capital Investment: The 11.7% Yield Has Always Been At Risk

2023-07-09 07:46:53 ET

Summary

- BlackRock Capital Investment's dividend history is unattractive, with a suspension during the pandemic and four cuts over the last ten years.

- The company's net asset value has not been well managed since its 2007 Nasdaq debut, contributing to a lack of market confidence in its future performance.

- Despite a high degree of safety in future quarters, the company's history of dividend cuts and unstable net asset value make it a risky investment option.

BlackRock Capital Investment's ( BKCC ) dividend history trendline is perhaps one of the most unappealing in the business development company space. BKCC suspended its dividend for three quarters during the pandemic, eventually reinstating it with an $0.04 cut with its common shares going on to lose 9% of their value over the last year. Income and net asset value per share growth form the most important metrics for investing in a BDC and BKCC is currently ranked D for its dividend safety by Seeking Alpha's scorecard and an F for consistency. The BDC last declared a quarterly cash dividend of $0.10 per share , in line with its prior payout and for an 11.7% forward annualized dividend yield.

BKCC is externally managed by BlackRock Advisors, an entity owned by the world's largest asset manager BlackRock ( BLK ). The BDC provides capital to middle-market US companies with investments typically ranging between $5 million and $20 million. It had a $587.8 million portfolio at fair value as of the end of its last reported fiscal 2023 first quarter. This was from investments spread across 121 portfolio companies and with a weighted-average portfolio yield of 12.4%, up 50 basis points sequentially from 11.9% in the prior fourth quarter. The increase was of course driven by the marked rise in the Fed funds rate which has pulled up LIBOR and SOFR.

Healthy Dividends Coverage Reduces The Risk Of Further Cuts

Critically, BKCC has not managed its net asset value, as defined by tangible book value, well since it started trading on the Nasdaq in the summer of 2007 as BlackRock Kelso Capital. NAV at $319.78 million for its first quarter did grow sequentially from $318.5 million in the fourth quarter, with NAV per share increasing by $0.03 to $4.41. Hence, the BDC is currently swapping hands at a roughly 22.5% discount to NAV, or 77.5 cents on the dollar. This would be a positive investable factor if NAV had a historically more investor-friendly trendline. However, it reflects a lack of market confidence in the ability of the BDC to protect NAV in future quarters. A turbulent dividend history is one thing, but this aggregated with a lack of NAV safety fully renders BKCC as a difficult ticker to recommend as a buy.

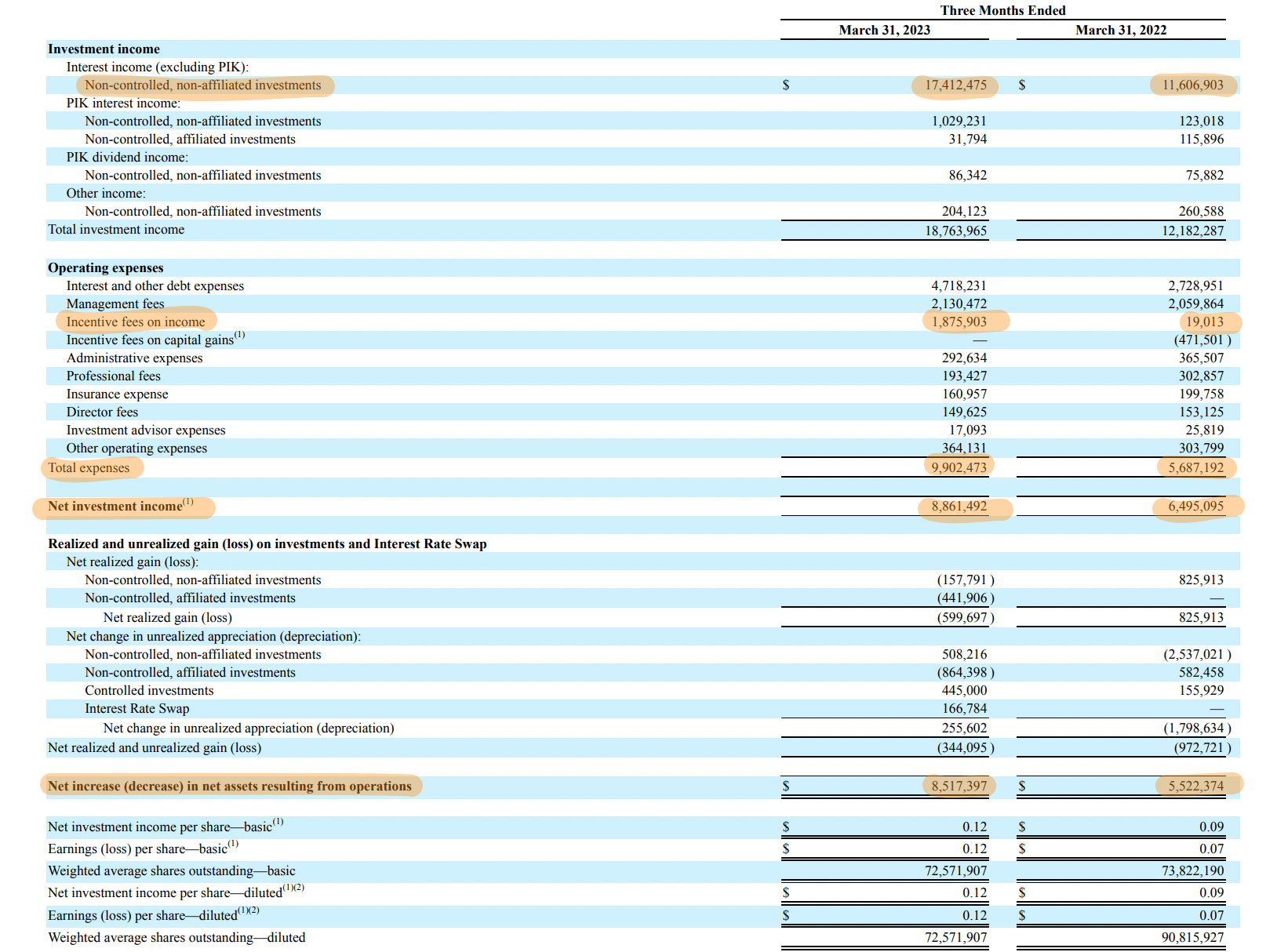

BKCC reported a first-quarter total investment income of $18.76 million, up 54% over its year-ago comp and a beat by $410,000 on consensus estimates. Growth was driven by interest income, excluding payment-in-kind, of $17.4 million. This was up from $11.6 million in the year-ago comp. Total operating expenses did increase by 74% year-over-year for net investment income of $8.86 million. Crucially, NII per share at $0.12 beat consensus estimates by $0.01 and was up sequentially from NII per share of $0.11 in the fourth quarter.

BlackRock Capital Investment Fiscal 2023 First Quarter Form 10-Q

{kind=link}

The current dividend is 120% covered against BKCC's first-quarter NII. This infers a high degree of safety in the future quarters against the backdrop of what's been four cuts in the last decade. The dividend is still a far way away from its per-quarter payout of $0.26 in 2013 with long-time investors likely having this in view as NII surges on the back of the current elevated Fed funds rate environment. The Fed funds rate has been hiked to its highest level since 2008 at 5% to 5.25%, a near-generational macroeconomic backdrop that has provided an opportunity for BKCC to ride up higher interest rates to further increase its dividend coverage and NAV.

The 11.7% Yield Has Always Been At Risk

Is BKCC a buy here against a coverage ratio that comes at marked odds with a history punctuated by cuts and perilous coverage ratios? No, but it's not a sell. The discount to NAV against a fast-rising NII from the current elevated Fed funds rate environment could feed through to NAV stability and possible growth. But NAV per share actually declined from its year-ago comp by $0.29. This came against NII which grew by 36% over the same time frame. To be clear here, BKCC's NAV still saw a year-over-year decline and barely grew quarter-over-year despite an NII that was in excess of the quarterly dividend by 20%.

BlackRock Capital Investment Fiscal 2023 First Quarter Presentation

{kind=link}

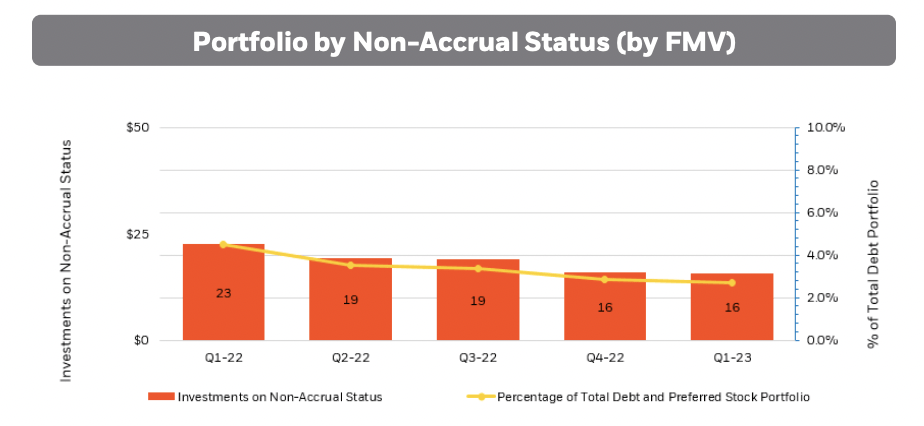

The likelihood of a near-term dividend cut is low, but compared to other BDCs guiding for strong dividend growth against the current macroeconomic context and with rising spillover income that has supported NAV and catalyzed supplemental payouts, BKCC is moving to simply not repeat the dividend cuts of the past as it reduces non-accrual loans as a percent of its investments. This was high at 2.7% of its portfolio at fair value during the first quarter.

For further details see:

BlackRock Capital Investment: The 11.7% Yield Has Always Been At Risk