OCSL - BlackRock Or PennantPark For Solid 12% Yield?

2023-07-05 12:33:13 ET

Summary

- We compare dividend coverage for two BDCs currently yielding around 12% before including any supplemental or special dividends (discussed below).

- We suggest one of these companies with a list of positives that investors should consider.

- However, this company also has a higher amount of watchlist investments which is why I am not purchasing at this point.

- Please see the chart at the end of this article comparing the potential impact on NAV per share, assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery.

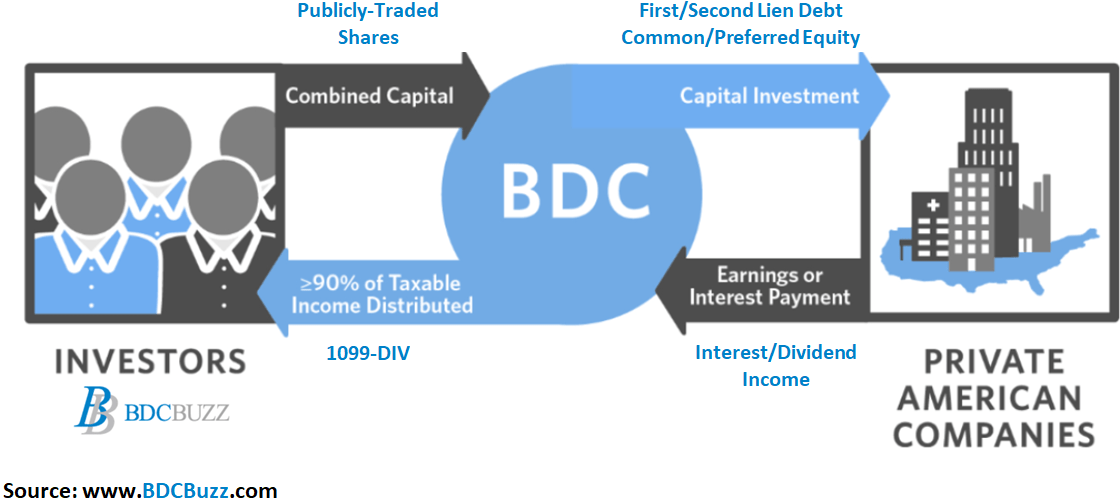

Quick Introduction To Business Development Companies

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds. Anyone can invest in BDCs as they're public companies traded on major stock exchanges. Also, many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings).

{kind=link}

The two biggest mistakes that I see new BDC investors make are:

- Not understanding why BDCs trade at different prices and thinking that price-to-NAV is the only measure to find a "good deal."

- Focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality.

Please see the end of this article for a quick discussion of how BDCs are valued. This article discusses dividend coverage for BlackRock TCP Capital ( TCPC ) and PennantPark Floating Rate Capital ( PFLT ) which currently have dividend yields of around 12% before including any supplemental or special dividends (discussed below). At the end of the article, I pick one of these BDCs and compare the potential impact on net asset value ("NAV") per share assuming that 100% of its watch list investments (including non-accruals) defaulted with 0% recovery.

Last month, we focused on portfolio credit quality (not dividend coverage) for FS KKR Capital ( FSK ), PennantPark Investment ( PNNT ), TriplePoint Venture Growth ( TPVG ), Goldman Sachs BDC ( GSBD ), Hercules Capital ( HTGC ), Monroe Capital ( MRCC ), and Prospect Capital ( PSEC ) in the following articles:

- Better High-Yield Buy: FSK or PSEC?

- PennantPark: Big Win From Dominion/Fox Settlement

- Venture Debt Opportunity Yielding 13% To 14%: HTGC or TPVG?

- Safer 12% Yield: Goldman Sachs BDC or Monroe Capital

BDC Buzz

Comparing Dividend Coverage

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with financial projections including base, best, and worst-case scenarios to test the sustainability and/or changes to the current dividends for TCPC and PFLT .

TCPC

BlackRock TCP Capital ( TCPC )

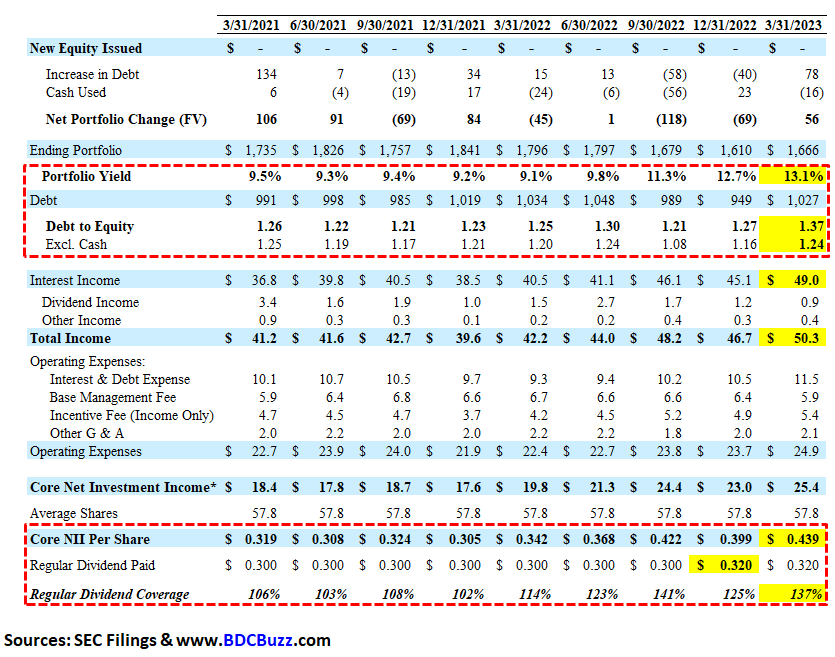

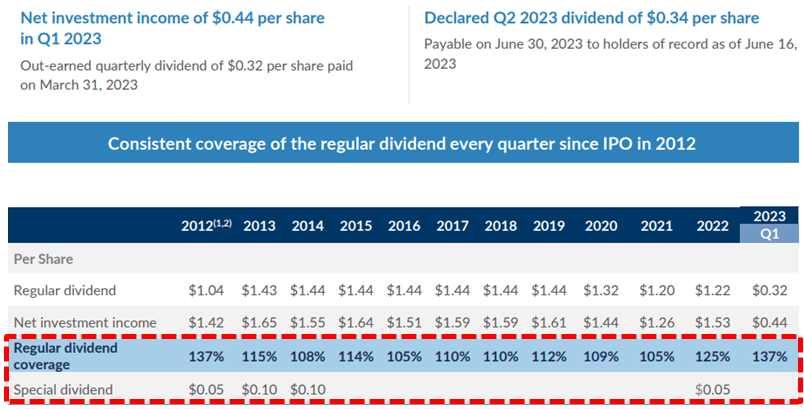

For Q1 2023, TCPC hit my best-case projections mostly due to portfolio growth coupled with higher investment yields and $0.01 per share from prepayment premiums and related accelerated original issue discount ("OID") and exit fee amortization. TCPC has covered its regular dividends by around 131% over the last four quarters.

We delivered strong net investment income of $0.44 per share in the first quarter. Given the floating rate nature of our portfolio, our net investment income continues to benefit from higher base rates as well as wider spreads on new investments, resulting in a run rate NII that is among the highest in TCPC's history as a public company."

{kind=link}

On April 25, 2023, the board re-approved its stock repurchase plan to acquire up to $50 million of common stock at prices at certain thresholds below NAV per share. During Q1 2023, there were no shares were repurchased. Fitch reaffirmed its investment-grade rating with a stable outlook during Q1 2023.

In May 2023, TCPC increased its quarterly regular dividend by 6% from $0.32 to $0.34 per share for Q2 2023, as projected in the previous best-case projections.

In recognition of the higher ongoing earnings power of TCPC, primarily to provide the rate environment, our Board of Directors today announced an increase of $0.02 per share to the quarterly dividend distribution. The second quarter dividend of $0.34 per share. Our board has always taken a disciplined approach with regard to the dividend given our emphasis on stability and strong coverage through our recurring net investment income. Throughout TCPC's history, we have consistently covered our dividends with recurring net investment income. This commitment remains important to us and even accounting for the dividend increase declared for the second quarter, our first quarter dividend coverage ratio would've been approximately 129% ."

Previous reports correctly predicted the reduction of TCPC's regular dividend from $0.36 to $0.30, which was at the top of my estimated range of $0.28 to $0.30. At the time, the company had a spillover/UTI of around $0.78 per share. However, this is typically used for temporary dividend coverage issues. Please do not rely on UTI as an indicator of a "safe" regular dividend .

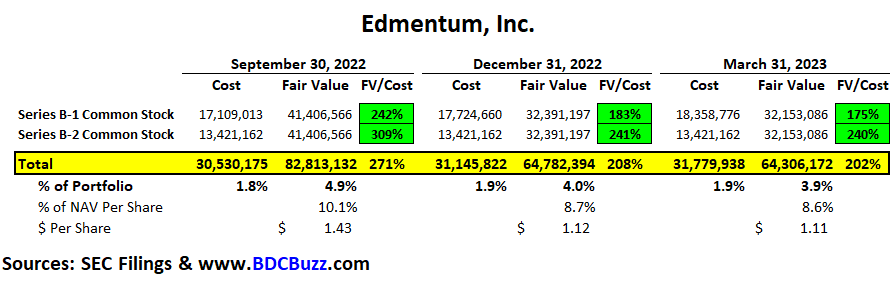

As discussed in previous articles, Edmentum, Inc. is a provider of online learning programs that was acquired by Vistria Group . Similar to NMFC, TCPC chose to re-invest a meaningful portion of the proceeds and "remain a significant shareholder of Edmentum , due to strong conviction in the continued growth." As shown in the following table, TCPC's investment in Edmentum declined but remains around $64 million and still accounts for around 4% of the portfolio.

{kind=link}

Management discussed Edmentum on the recent call:

I can give you some perspective because we've talked about it, and then time will tell, but I think if you think about what Edmentum has successfully done in moving its business forward over time it's made a big push from going from analog to digital. Obviously, that's where the market is going for ed-tech, and they've done a very good job, I think, proactively of going from broader-based assessment and targeted content to much more personalized assessment and targeted content to move students forward from a baseline - from a - where they are to a baseline or ahead of it. A big part of that value proposition going forward is the ability to do that very proactively in a very targeted manner. And not surprisingly, some AI type of technology is actually additive to that it gets - it makes it a more robust function. So, the product set will certainly incorporate that and Edmentum as a company should let the CEO who's exceptional in his field speak to it directly, but has even before AI became kind of the topic the other day, we're exploring incorporating that into their product set because that is where the market ultimately will go and will benefit from . But I think that makes it a better product, not a less relevant product. And that's one that I think will only enhance what they're doing on a personalized basis with students. How that ultimately rolls forward? I think time will tell, but from a point of view of the thinking at the company level they've been thinking about AI and incorporating it for quite some time now . And I haven't tracked the other online education performance. I don't think they're necessarily comparative businesses. But at least from my perspective, it's something that would be additive to what they do and they certainly seem that way as well."

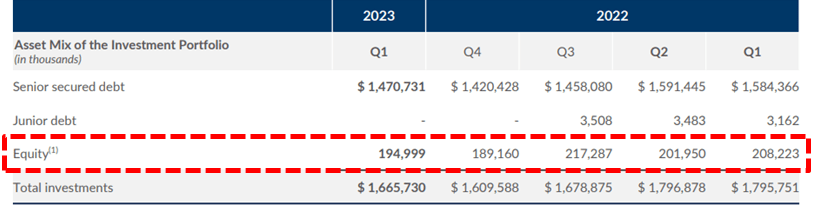

As shown below, equity investments decreased from $217 million in Q3 2022 to $195 million in Q1 2023 ( 12% of the total portfolio ), mostly due to marking down Edmentum . There's a good chance that management will continue to monetize additional equity positions, driving increased recurring interest income taken into account with the "best case" financial projections.

{kind=link}

BDCs should continue to benefit from tightened lending policies and potentially increased banking regulations, which will likely include stronger capital and liquidity standards for certain banks. BDCs have a distinct advantage over banks in that they have "permanent equity capital" and are not subject to "runs on the bank," which could lead to the forced liquidation of undervalued assets.

The broader social and economic implications, weakness and even turmoil in the banking sector is hardly a new dynamic to establish private market participants. Rather, it is a dynamic we have benefited from for most of our nearly 23 years lending to middle market companies who continue to look in ever greater numbers for alternatives to traditional forms of financing. We believe the reaction to recent events in the banking sector will likely make it even l ess efficient and less economical for banks to lend to the middle market, and therefore further support, if not accelerate the opportunity for well-positioned private credit lenders such as ourselves . In addition, the swift collapse of several banks and ongoing concern with the sector has been a reminder to borrowers of the benefits of working with a direct lender like BlackRock. Direct lenders can act quickly when needed and have permanent capital that facilitates stable long-term financing solutions to borrowers that remain available during periods of market dislocation . We have seen this firsthand many times, including during the early days of COVID, and again, more recently this past quarter with the few portfolio companies we have that had cash deposits with Silicon Valley Bank. When the news about the challenges that the bank started to spread and these companies had difficulty accessing their liquidity, our team was in position to provide short-term liquidity had it been required. Fortunately, the Fed stepped in to backstop their deposits and ultimately our capital was not needed, but our ability to work directly with these borrowers and to act quickly or further reminders of the value that private credit managers can provide."

The recent instability in the banking sector is likely to have a considerable effect on BDCs, resulting in continued improvement in yields on new investments and a wider range of investment opportunities. As a result, BDCs can continue to be very selective in their new investment choices. Earlier this month, TCPC management mentioned the more lender-friendly environment with better terms, including stronger covenants (safer investments) and higher overall yields taken into account with the best-case projections:

Given further pullback and bank's ability to lend in this environment exacerbated by the regional bank turmoil in the first quarter, we are continuing to benefit from a more lender-friendly investment environment with improvements in both pricing and terms relative to just 12 months ago. Post quarter end, we have seen a modest pickup in activity and have been investing selectively, maintaining our underwriting discipline, while being mindful of the inflationary environment. We emphasize companies that have significant pricing power to pass on higher input costs, including increases in their cost of capital. We are being disciplined and deploying new capital in this uncertain environment, while also selectively taking advantage of the more lender friendly investment environment. We've reviewed a substantial number of transactions during the quarter and deployed capital in a small percentage of those opportunities."

The amount of recurring/stable earnings could continue to increase, driven by higher interest rates, new investments at higher yields, and the rotation out of equity positions into income-producing debt. Also, there's a chance for additional special dividends in 2023 paid out of spillover/UTI (undistributed taxable income) which was around $1.20 per share as of December 31, 2022, even after paying a special dividend of $0.05 per share in Q4 2022.

{kind=link}

PFLT

PennantPark Floating Rate Capital ( PFLT )

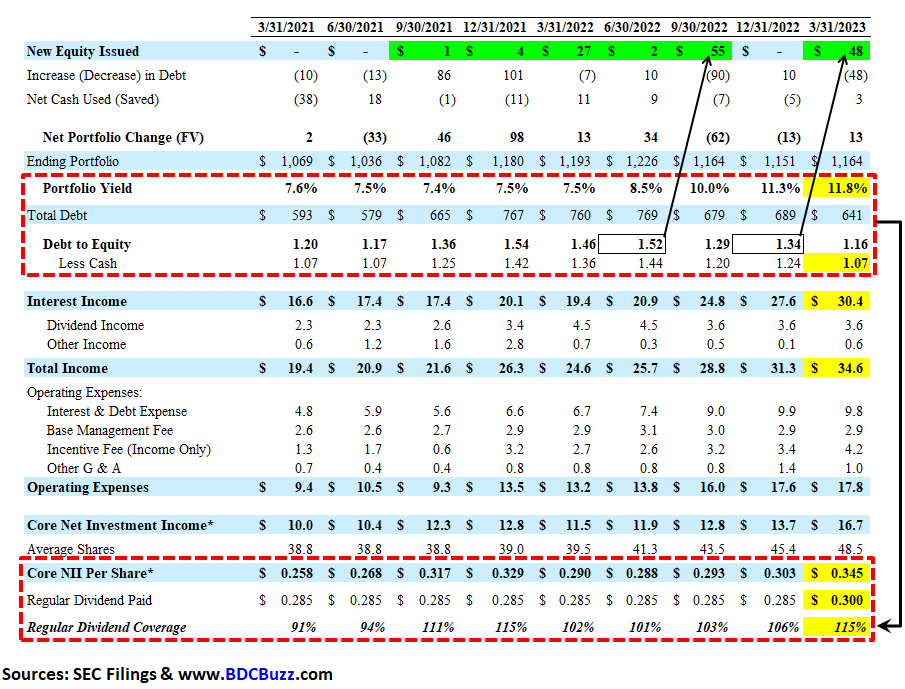

For calendar Q1 2023, PFLT reported slightly above my best-case projections with another meaningful increase in its portfolio yield (from 10.0% to 11.8% over the last two quarters) partially offset by lower-than-expected portfolio growth and dividend income from its PennantPark Senior Secured Loan Fund ("PSSL").

{kind=link}

In May 2023, PFLT increased its monthly dividend of $0.1000 to $0.1025 per share (an increase of 2.5%) starting in July 2023 which was between the previous base and best-case projections.

Art Penn, Chairman/CEO: "We are pleased to announce an increase in our monthly dividend based on the continued strong underlying credit performance of our portfolio in this environment. With our primary focus on lower-risk senior secured floating rate loans to U.S. companies, we are positioned to preserve capital and protect against rising interest rates and inflation. We have a visible pathway to continue to optimize the balance sheets at both PFLT and PennantPark Senior Secured Loan Fund I LLC over the coming quarters, which we believe will increase net investment income ."

In April 2023, Dominion Voting Systems and Fox News Network agreed to settle the defamation lawsuit. As part of the settlement, Fox News agreed to pay Dominion $787.5 million. PFLT has a minority equity interest in the company resulting in around $4 million ($0.08 per share) of net proceeds . The timing and amount of any distribution is uncertain and subject to change. After incentive fees, this would be around $0.064 per share of additional earnings .

PFLT has an equity ownership in Dominion Voting, which subsequent to quarter end settled their lawsuit with Fox News for $787 million. Dominion has communicated their intention to distribute the net settlement proceeds and PFLT share is estimated to be approximately $4 million."

However, there's a good chance that management will not be paying a special dividend and retain the excess earnings as "spillover that can potentially go into protecting that dividend over time."

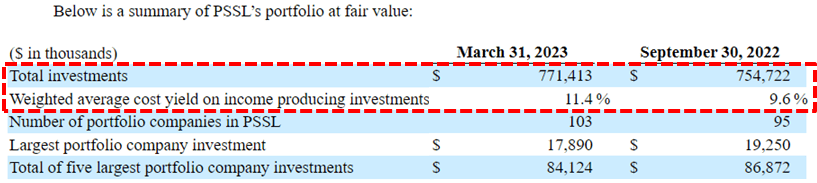

PFLT continues to improve returns from its PennantPark Senior Secured Loan Fund ("PSSL") through refinancing the borrowing facilities and growing the portfolio. Total investments in its PSSL portfolio have increased from $565 million to $771 million over the last six quarters and the weighted average yield on investments increased from 7.1% to 11.4%.

As of March 31, the JV portfolio equaled $771 million. And together with our JV partner, we continue to execute on the plan to grow the JV portfolio to $1 billion of assets. Subsequent to quarter end, the JV closed its second CLO financing and the sixth CLO for the PennantPark platform. This new financing will allow the JV to further diversify and increase its balance sheet. We believe that the increase in scale and the JV's attractive ROE will enhance PFLT's earnings momentum."

{kind=link}

PFLT will probably continue to rotate out of non-income-producing assets and reinvesting into higher-yielding assets over the coming quarters, which does not require higher use of leverage.

We typically participate in the upside by making an equity co-investment. Our returns on these equity co-investments have been excellent over time. Overall, for our platform from inception through March 31, we've invested over $394 million in equity co-investments and have generated an IRR of 26% and a multiple on invested capital of 2.2x."

Similar to TPCP, I'm expecting continued improvement in PFLT's earnings (for the base and best-case projections) partially supported by higher portfolio yield due to better pricing and previous rate increases, higher returns from its PSSL, maintaining higher leverage, and portfolio rotation (out of non-income-producing assets) taken into account with updated the projections:

We believe NII can continue to grow as we optimize the balance sheets of both PFLT and our JV. With leverage at PFLT at 1.17x debt-to-equity and target leverage of 1.4 to 1.6x , we plan on thoughtfully moving towards our target. The combination of excellent credit quality and higher yields on our portfolio matched with a visible pathway to more optimized balance sheets at PFLT and the JV positions us for stable and growing NII over the coming quarters. So we've got two levers, we think, to grow NII. Even if you take a stance that risk-free rates are coming down, SOFR is going to come down, we don't think so. But even if it is, we still feel very good about our income generation capacity, which helped drive our decision about the dividend increase ."

BDC Valuations

Author's Note: The following information was provided to subscribers of Sustainable Dividends along with updated target prices and suggested limit orders (for making purchases) for TCPC and PFLT .

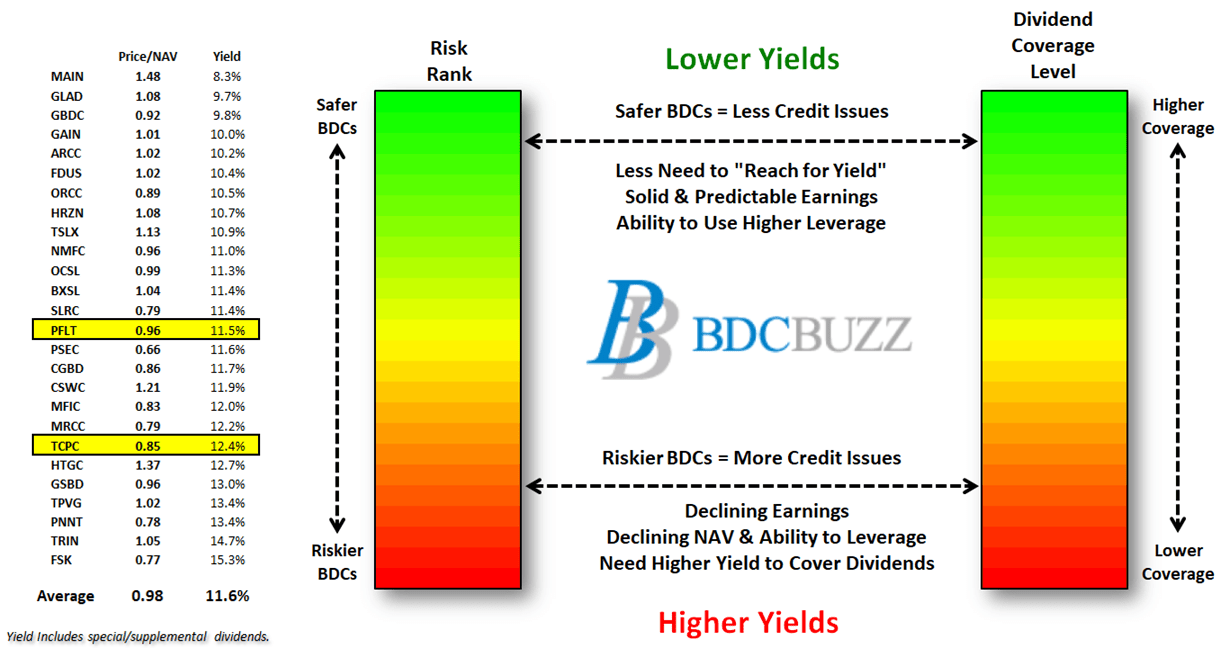

There are very specific reasons for the prices that BDCs trade driving higher and lower yields mostly related to portfolio credit quality and dividend coverage potential (not necessarily historical coverage).

{kind=link}

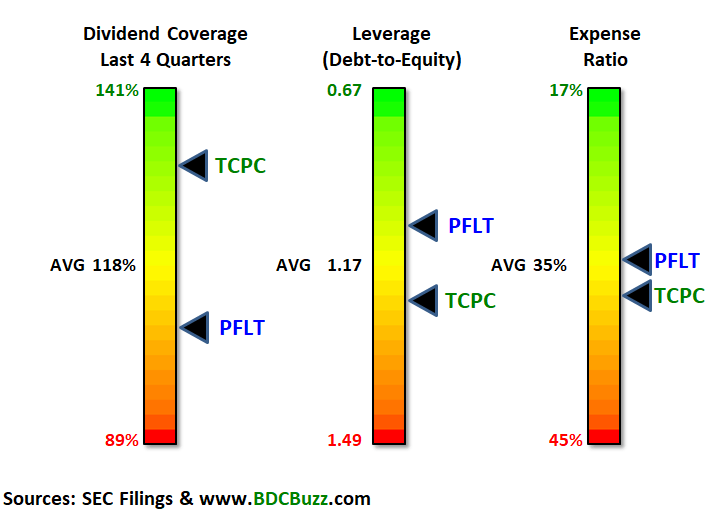

The charts below compare the various metrics for TCPC and PFLT including dividend coverage over the last four quarters, leverage or debt-to-equity, and expense ratios.

{kind=link}

{kind=link}

Clearly, TCPC is the winner from a historical dividend coverage standpoint but PFLT has relatively lower leverage implying the potential for more portfolio growth (for increased earnings). Also, PFLT has a slightly lower expense ratio which measures operating, management, and incentive fees compared to available income. Later this month I will have a full article discussing and comparing BDC expense ratios. BDCs with lower operating expenses can pay higher amounts to shareholders without investing in riskier assets.

Gun to my head, I would choose TCPC over PFLT for the following reasons:

- Excellent historical and projected dividend coverage.

- Regular dividend increase and special dividend in Q2 2023.

- Paid a special dividend of $0.05 per share in Q4 2022.

- Its investment in AutoAlert was restructured (back on accrual status) and will contribute to dividend coverage during Q2 2023.

- Relatively low amounts of PIK income, currently around 3% of total income.

- Cumulative "total return" hurdle or "look back" provision when calculating income incentive fees to protect shareholders from capital losses.

- Base management fee of 1.00% for assets in excess of 1.00 debt-to-equity.

- Previously waived incentive fees.

- First-lien investments account for 76% of the portfolio's fair value.

- Highly diversified portfolio with only four portfolio companies contributing 3% or more to dividend coverage.

- Fitch reaffirmed its investment-grade rating with stable outlook.

- 94% of portfolio debt investments bore interest at variable rates and only 29% of borrowings are at variable rates.

- SBIC license provides an incremental source of long-term (10 years), low-cost capital (average rate of 2.5%).

- Potential rotation out of equity positions into income-producing debt positions.

- Conservative dividend and accounting practices (recognizing fee income over the life of the investment).

- Clear/transparent management when discussing portfolio credit quality (see notes in this report) and measured approach when raising and deploying capital.

- Potential upgrade and increased target prices due to improved portfolio credit quality.

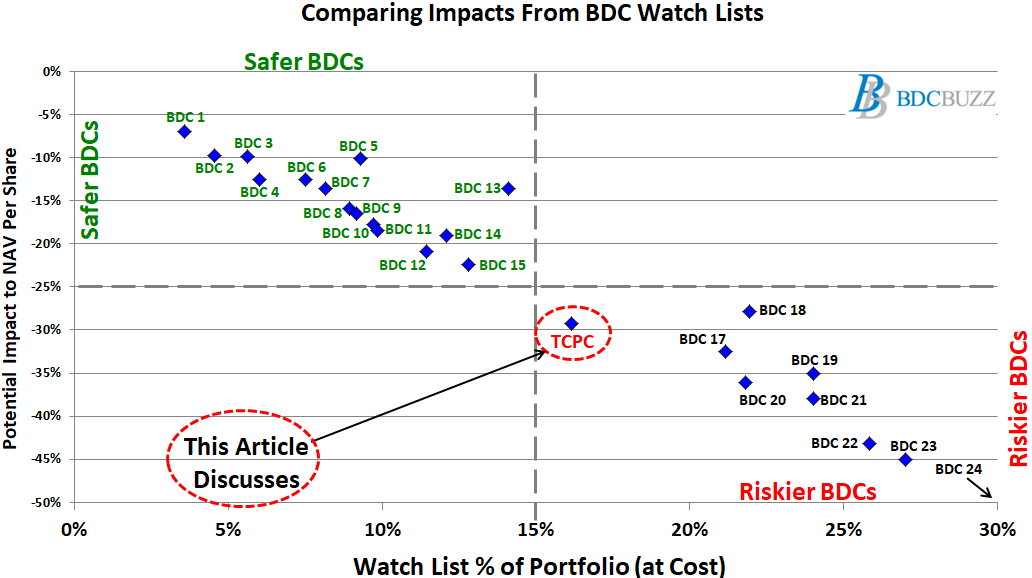

However, I will not be adding to my TCPC position mostly related to the amount of investments considered "watch list" currently around 16% of the portfolio cost compared with the average BDC closer to 13% and will discuss this in an upcoming article. The following chart shows the potential impact on NAV per share for each BDC, assuming that 100% of watch list investments (including non-accruals) defaulted with 0% recovery. This is the worst-case scenario for this group of investments. The largest NAV declines over the last four quarters were mostly BDCs with larger amounts of watch list investments. Subscribers who believe the economy is headed for a "hard landing" with a deep, broad, and/or extended recession should focus on the BDCs closer to the top left corner.

{kind=link}

As mentioned in previous articles, I sold around ~20% of my TCPC position in March 2020 at an average price of $14.40. I was overweight in the stock as it was previously around 8.5% of the portfolio, which is larger than a "full position." The "Annualized" return shown below does not use a simple average but shows the actual compounding of annual returns. This is the true return each year.

For further details see:

BlackRock Or PennantPark For Solid 12% Yield?