KKR - Blackstone: 4 Reasons To Buy The Stock Right Now

2023-03-23 09:45:10 ET

Summary

- Blackstone is the largest player in the industry and has several catalysts that can provide outperformance in the coming years.

- The firm is strongly positioned and is likely to be the beneficiary of a growing private lending market.

- The headwinds faced by BREIT should not come as much of a surprise to sophisticated investors.

- During the recovery period, Blackstone will experience more tailwinds than competitors.

- The firm is trading cheaply relative to its historical levels. A solid dividend yield can support the share price in the event of worsening macro conditions.

Investment Thesis

The previous article " Three Reasons to Avoid Blackstone " received a lot of backlashes. However, as time has shown, the theses were correct. The alternative asset boom has turned to pessimism, and Blackstone ( BX ) stock posted one of the worst performances among alternative managers over the past year. The company lost about 32% of its market capitalization. By comparison, Apollo Global Management ( APO ) was down less than 6% and KKR ( KKR ) shed just over 13%. Only The Carlyle Group ( CG ) showed the worst result (for more information about the company, see here ).

Blackstone is the market mastodon, the industry leader with the largest amount of assets under management. There are several reasons why the company's shares may provide outperformance in the coming years. The firm is strongly positioned and is likely to be the beneficiary of a growing private lending market. In addition, Blackstone is trading below its historical levels, and the dividend yield can support the share price in case of worsening macro conditions.

BREIT Headwinds are Already Priced in

For about half a year, the attention of investors and financiers involved in the industry of alternative assets has been riveted to the non-traded Blackstone Real Estate Income Trust. BREIT manages $68.5 billion and specializes primarily in rental housing and industrial properties in the sun belt region of the southern and western United States.

Launched in 2017, BREIT has seen impressive growth over the years. At the moment, the value of the trust reached $116 billion and it became one of the largest buyers of real estate in the country. However, against the backdrop of changing market conditions, redemption requests from investors began to grow. In early December, Blackstone introduced buyback limits of 2% of NAV per month and 5% of NAV per quarter. Over the next four months, the company steadily extended the limit. In February, Blackstone received $3.9 billion in requests , of which it only bought back $1.4 billion, or 35%.

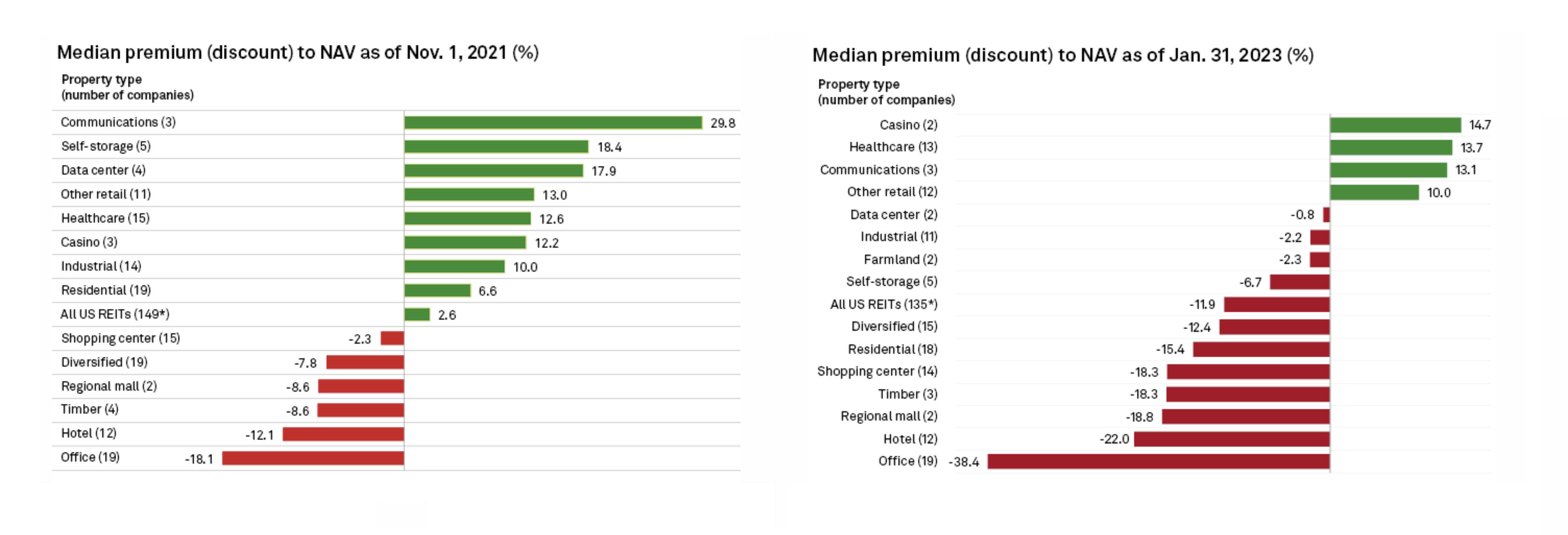

The headwinds faced by BREIT should not come as much of a surprise to sophisticated investors covering the real estate sector. The fundamental advantage of BREIT over publicly traded real estate investment trusts is the lack of volatility. Investors buy its shares at the par value of net assets, that is, with a P/NAV multiple of 1.0x. This can be a good deal during a period of falling interest rates when public REITs are trading at a premium to NAV and their capitalization rate is shrinking.

However, BREIT's advantage is its own Achilles heel. In November 2021 , when residential and industrial REITs were trading at a premium to NAV of 6.6% and 10.0%, respectively, buying BREIT at book value seemed like a great opportunity. However, the tightening of monetary policy has changed the balance of power in the market. In January 2023 residentials traded at a 15.4% discount on average and industrials traded 2.2% cheaper than NAV. Not surprisingly, savvy investors are trying to sell BREITs and shift their capital into cheaper REITs.

{kind=link}

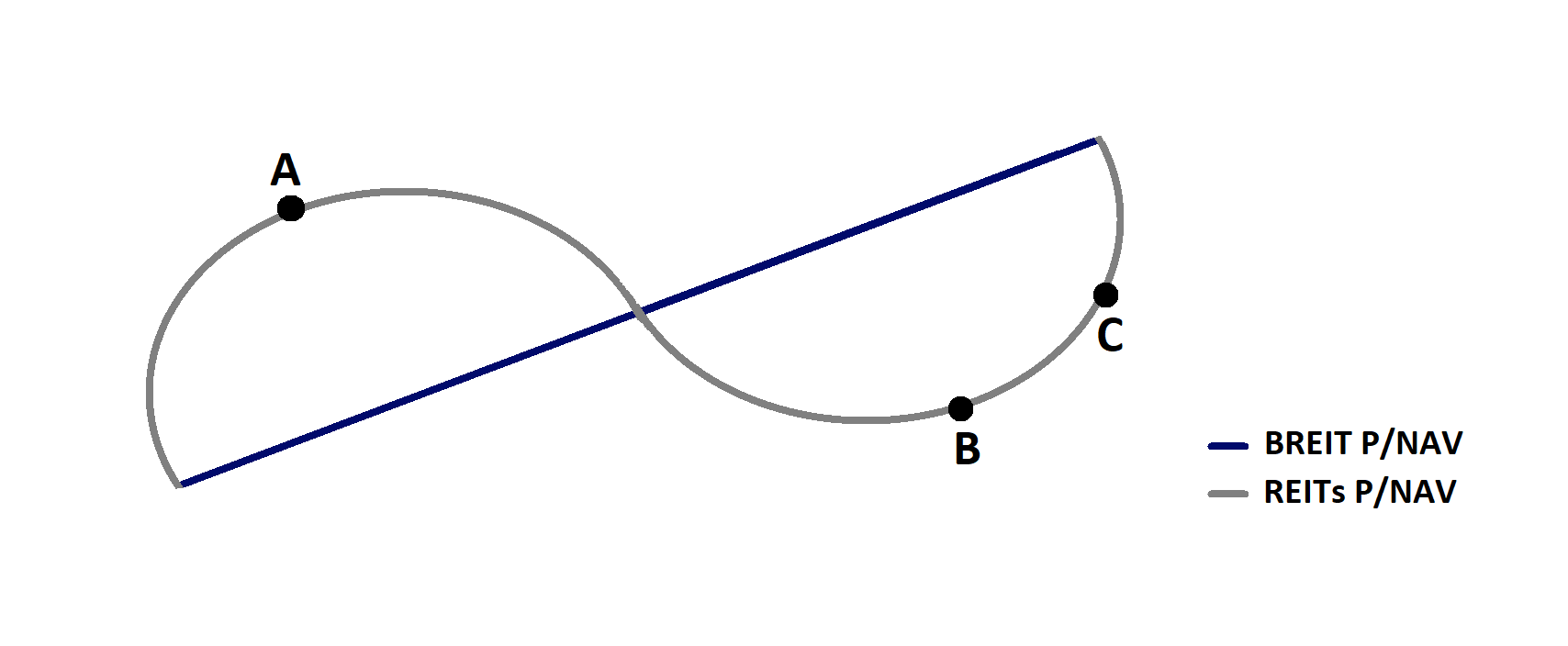

However, what makes BREIT today's underdog will provide it with outperformance as the gap between price and net asset value narrows again. Schematically, this can be represented as follows:

{kind=link}

The good news is that today we are at point C and the bottom of the market seems to be behind us. There are two main reasons for this conclusion:

- In December 2022 , REITs traded at the largest discount to NAV, reaching 20.8%. Since then, their value has recovered significantly.

- Few would argue that the main stage of monetary tightening is over. Inflation is showing clear signs of slowing down, and turbulence in the banking industry has made policy easing a matter of medium rather than long-term.

However, if we assume that this thesis is erroneous and that there are still several years of BREIT's underperformance ahead of us, the withdrawal limit gives the company a significant margin of safety. If BREIT continues to lose 5% of net asset value each quarter with zero inflows, then the company will lose approximately $23.1 billion by the end of 2024. For comparison, in the fourth quarter of 2022 alone, Blackstone increased total AUM by $23.8 billion.

Potential of the Private Lending Market

In recent years, private lending has been gaining momentum in the debt capital market. In the past, PE firms relied primarily on the largest banks and the debt markets to make leveraged buyouts. Today, alternative managers themselves are actively lending to LBO deals, and new players are entering the market.

Notable is the recent acquisition of a 50% stake in Cotiviti by Carlyle Group for $5.5 billion. The deal was fully funded by a syndicate of four private lenders: Apollo Global Management, HPS Investment Partners, Ares Management ( ARES ), and, of course, Blackstone.

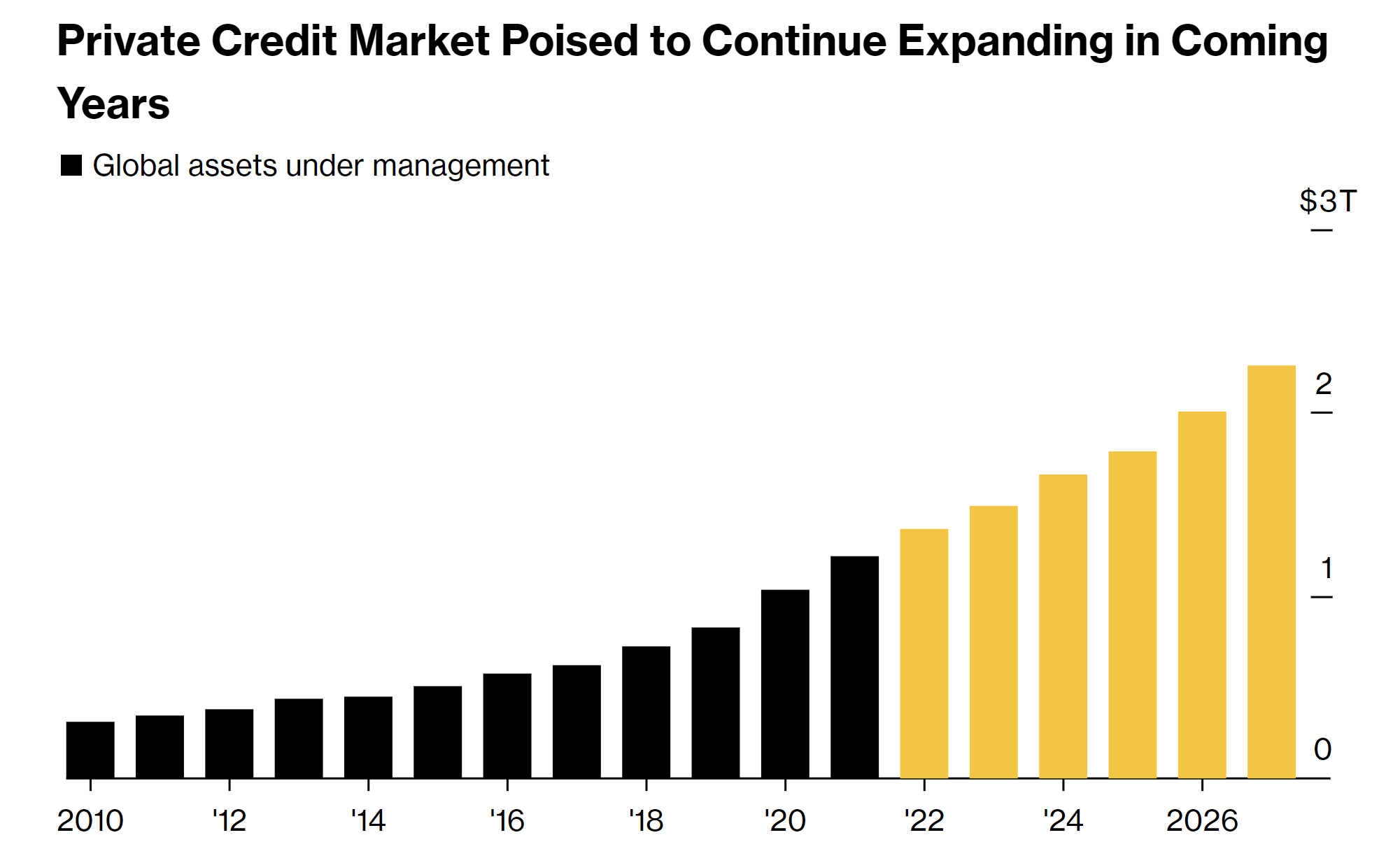

According to Bloomberg , the private lending market was valued at $1.2 trillion in 2021 and is expected to reach $2.3 trillion in 2027, projecting growth at a compound annual rate of 11.5% over the forecast period.

{kind=link}

Direct lenders can capture and hold a significant market share. HPS' partner Mike Patterson predicts that private lenders could take 10% to 25% of the LBOs financing market.

As one of the leaders in the alternative asset industry, Blackstone will be the beneficiary of this trend. Today, the Credit & Insurance segment is the third largest in AUM, accounting for $279.9 billion. However, it has also become the most growing in the past two years: since 2020, the segment has grown by 81.3%, while Real Estate has grown by 74.2%, and Private Equity - by 46.3%.

Strong Positioning for Future Outperformance

Blackstone shares posted one of the worst performances among alternative asset managers over the past year. The company lost about 30% of its market capitalization. By comparison, Apollo Global Management was down less than 3% and KKR shed just over 12%. Worse was only The Carlyle Group, whose stock fell by more than 30%. However, the latter company ran into difficulties during fundraising and also worked for a long time without a permanent CEO.

The performance of companies in the asset management industry has always been highly volatile, with revenue falling during periods of bearish sentiment but recovering quickly when the market is bullish. Alternative managers partially solve this problem due to the high share of fee-earnings AUM in the total structure of assets under management. FAUM brings firms stable management fees. However, Blackstone is inferior to its largest competitors in terms of FAUM's share in Total AUM, which is 73.7%. Only Carlyle has a smaller share - 71.5%.

| Total AUM |

| Fee-earnings AUM |

| FAUM as % of AUM |

| Blackstone ( BX ) |

| $975B |

| $718B |

| 73.7% |

| Apollo Global Management ( APO ) |

| $548B |

| $412B |

| 75.3% |

| KKR & Co. ( KKR ) |

| $504B |

| $412B |

| 81.8% |

| The Carlyle Group ( CG ) |

| $373B |

| $267B |

| 71.5% |

(Source: Companies' 10-K filings)

The smaller share of FAUM was a problem when the market activity decreased. However, it seems that the period of anomalous indicators is behind us. According to PwC , in the second half of the year, global market activity returned to pre-pandemic levels (it should be noted that activity in the US is still slightly higher).

{kind=link}

In other words, the potential for further decline is limited. At the same time, during the recovery period, Blackstone will experience more tailwinds than competitors, for the same reason - a greater dependence on performance fees.

Reasonable Price and Dividend Yield

Today Blackstone is trading at the lowest P/Cash flow multiple in years. The company was cheaper only in 2013-2015.

At the current share price and a payout ratio of 85%, the forward dividend yield is around 5%. Even if we don't see a market recovery in the short term, dividends will support stock prices.

Conclusion

Blackstone shares are one of the worst-performing alternative managers in a year. However, Blackstone is the largest player in the industry and has several catalysts that can provide outperformance in the coming years. The company has significant potential in the private lending market, and headwinds in the real estate segment seem to be priced in already. The firm is trading cheaply relative to its historical levels. In addition, a solid dividend yield can support the share price in the event of worsening macro conditions.

For further details see:

Blackstone: 4 Reasons To Buy The Stock Right Now