TPG - Blackstone And KKR: My Top Alt Asset Manager Picks

Summary

- Listed alternative asset management firms have done well recently with a median average re-rating of 21.8% higher. But which one should you buy and which should you avoid?

- I share how I assess 10 key listed asset management firms using 5 simple criteria.

- I arrive at slightly contrary conclusions to dividend and asset management firm experts, but I am confident in my view and curious to see how it unfolds.

Introduction

In early January, I analyzed the private markets space via a deep dive on TPG Inc. ( TPG ). I would say my 'hold' assessment has been broadly in-line so far; the stock has generated 1.09% alpha vs. the S&P 500 ( SPY ) ( SPX ).

But what about other alternative asset managers? In this article, I share my current framework for selecting alpha picks in the alternative asset managers space and apply it to 10 of these listed funds:

- Blackstone ( BX )

- Ares Management ( ARES )

- Hamilton Lane ( HLNE )

- Carlyle Group ( CG )

- Blue Owl Capital ( OWL )

- Apollo Global Management ( APO )

- KKR ( KKR )

- StepStone Group ( STEP )

- TPG Inc. ( TPG )

- Brookfield Asset Management ( BAM )

My conclusion is that Blackstone and KKR are the best buys. Read on to find out why:

Selection Criteria

The following ranks various listed alternative asset management firms according to my selection criteria, which is listed in decreasing order of priority:

1. Large fee-paying AUM

Talk to any asset management CEO and their number one business goal is to increase AUM, particularly fee-paying AUM, which presents a highly sticky revenue stream. And it's not surprising to see why; asset management businesses benefit from tremendous amounts of operating leverage, incremental fee related margins well above 70%. For this reason, I too have a preference for large AUM asset managers.

Fee paying AUM comps (Company filings, Author's Analysis)

Blackstone stands out as the clear favorite here due to its $718bn fee-paying AUM, which corresponds to a peer-set market share of 26.8%. Brookfield Asset Management and KKR come in a close 2nd and 3rd place, although at a large margin of difference to Blackstone.

2. Moderate real assets AUM mix

I am bullish on real assets such as infrastructure, energy and real estate. I believe there is a sector rotation occurring from technology to hard assets, driven by inflationary effects, revamp to fiscal spending and the long-term drivers of a clean energy transition.

I have discussed these thematic ideas in depth in my previous articles: A global infrastructure ETF ( IGF ), a homebuilding ETF ( ITB ), a homebuilding stock ( MHO ) and a defense REIT ( OFC ). Cumulatively, these picks have generated a total alpha vs. the S&P 500 of 16.58%. I encourage you to read those pieces for elaboration on the fundamental drivers leading to my bias toward real assets.

Real Assets Mix of AUM (Company filings, Author's Analysis)

Note: The following are my estimates of real assets mix based on company filings. In some cases, the categorizations of real assets were mixed with other asset classes. I have taken a judgement call to categorize properly. Ultimately, the inference still holds without any ambiguity:

Brookfield Asset Management and Blackstone have the highest real assets mix in the peer-set, with KKR not far behind. I am inclined to slightly prefer Blackstone if I consider the next parameter:

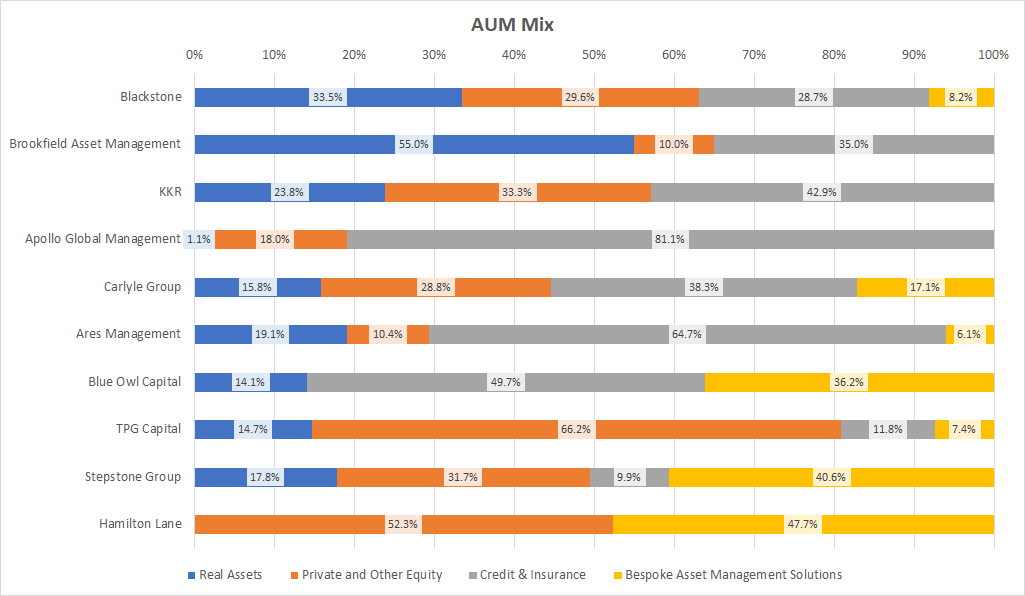

3. Well-balanced portfolio

Whilst I do want a higher proportion of real assets exposure, I am hesitant to have concentrated exposure to that asset class. This is not only due to risk mitigation reasons but also due to avoidance of excessive return erosions; infrastructure private equity tends to generate lower returns (8-15% annual return) in the long term compared to traditional private equity (upwards of 20% annual return).

Yes; it is true that an investor in the listed alternative asset should care less about the return profile compared to the AUM growth. However, my view here is that over a long enough period, traditional private equity will see a higher growth in fees across a market cycle as that would provide better returns.

AUM Mix of Alternative Asset Managers (Company Filings, Author's Analysis)

{kind=link}

Note: The following are my estimates of real assets mix based on company filings. In some cases, the categorizations of real assets were mixed with other asset classes. I have taken a judgement call to categorize properly. Ultimately, the inference still holds without any ambiguity:

On this parameter, Blackstone and KKR have the most diverse portfolios, with Blackstone at a slight advantage. Brookfield Asset Management's 55% real assets exposure sticks out as a clear outlier. Hence, for investors willing to accept concentrated real assets exposure, BAM may be an attractive option, especially since it scores well on the size parameter. For investors wanting more equity-like exposure, TPG is the clear favorite with a 66.2% exposure to equities.

4. Moderate amount of dry powder

US Monthly Recession Probabilities (Statista, Author's Analysis)

As the market is in a downturn currently with recession probabilities close to 50% by the end of 2023, I believe alternative asset managers with moderate amounts of dry powder (cash) would be relatively better positioned.

Dry Powder as % of AUM (Company Filings, Author's Analysis)

TPG Inc. has the largest dry powder mix, with KKR and Blackstone following in close 2nd and 3rd place. Until this criterion, Brookfield Asset Management was tracking well. However, it falls behind here with a dry powder as % of AUM of only 4.2% .

For those interested in TPG, in my previous analysis, I have identified Real Estate (Real Assets) and Impact Investing (Private and other equity) to be the incremental growth drivers for TPG. A key monitorable for those interested in TPG would be where this dry powder would get allocated. I believe given the already high equity exposure mix, it would be favorable to have much of the marginal allocation in the real assets category.

5. Attractive valuations

So far, the standout names have been Blackstone, Brookfield Asset Management and KKR.

NTM PE Valuations (Capital IQ, Author's Analysis)

Looking at the valuation comps, I am surprised Brookfield Asset Management is trading at a premium to larger, more diversified players such as Blackstone. I am even more surprised that Blackstone is merely trading at the median next-twelve-months [NTM] multiple of 20.0x. I believe given its much larger size, favorable AUM mix and moderate amounts of dry powder, it should be at a healthy premium to the peer-set median. KKR, which has closely followed Blackstone in the selection criteria, also seems attractively positioned at a 26% discount to the median NTM P/E multiple.

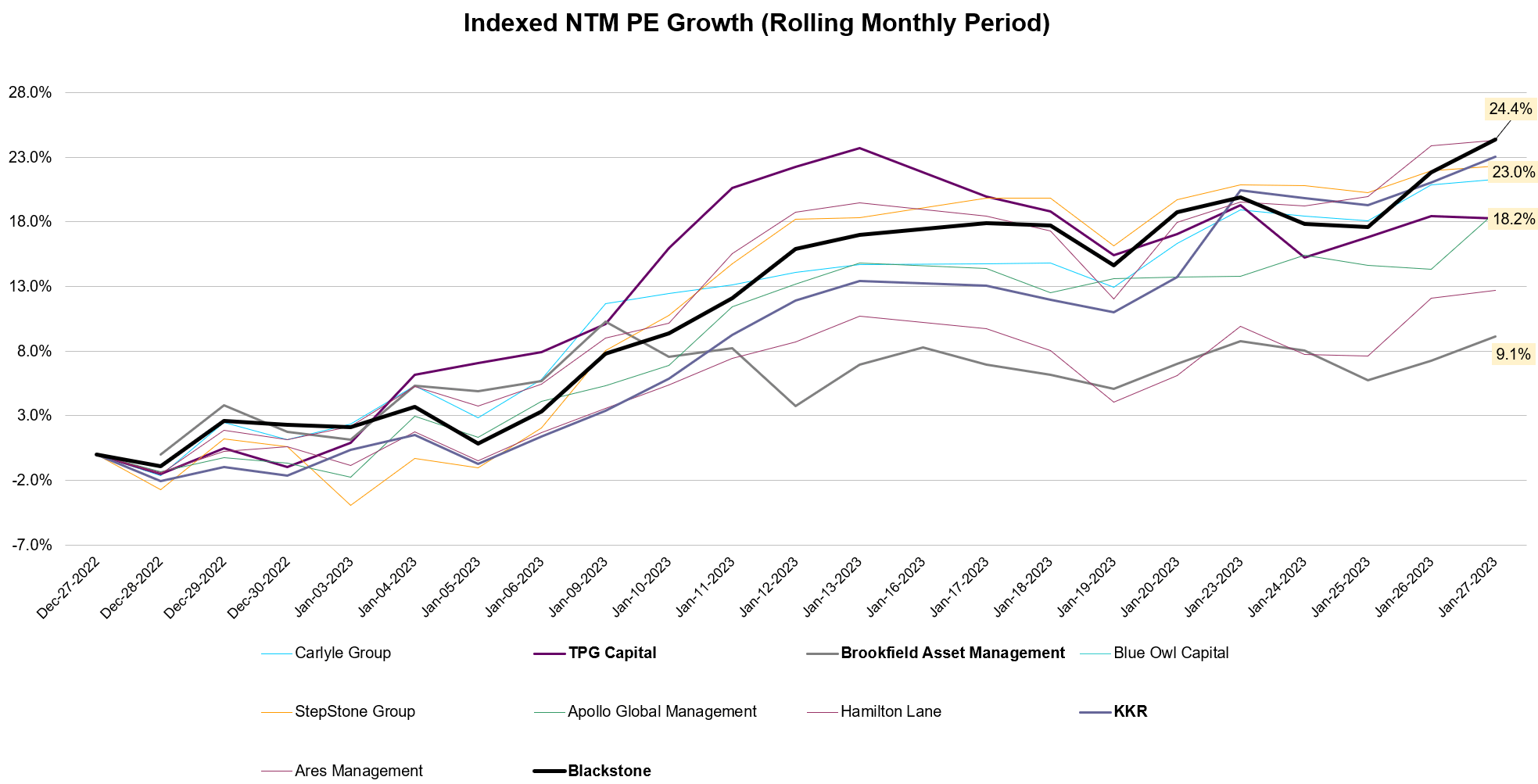

I love seeing positive momentum in my investment candidates since many academic studies have shown that momentum is a key, reliable driver of returns:

Indexed NTM PE Growth (Capital IQ, Author's Analysis)

{kind=link}

As a group, the listed asset management companies have re-rated by a median average of 21.8% over the last 30 days. Digging into the specifics, Blackstone has had the greatest positive momentum with a re-rating appreciation of its P/E multiple amounting to 24.4%. Brookfield Asset Management on the other hand has appreciated by only 9.1%. KKR is in the mid-range of the peer group with a re-rating of 18.2%, slightly below the median. And for investors who value high amounts of dry powder and high equity allocations, TPG has seen a solid re-rating of 23.0%.

Limitations of Selection Criteria

I contend that my selection criteria are hinged on logical and material value drivers of a company. Thinking about what ultimately drives consistent, growing cash flows for asset management businesses, one would arrive at very similar parameters. Indeed, they are considered industry-specific metrics to judge operational profiles and execution.

Yet, there are subjective elements involved, specifically in my assessment that real asset exposure is favorable due to my bullish view on it. If my thesis on that is wrong, then I would be caught wrong-sided. Additionally, the degree of portfolio diversification one prefers in the alternative asset manager is also a subjective call. The preferences and hence the outcomes according to my risk-reward utility function may be different than yours.

But this is where I hope my coverage of all key alternative asset management firms, uniformly across the critical value drivers helps you; you are able to compare and contrast and make your own assessments based on this comparables analysis of industry key metrics.

Decision Making

For what I'm looking for, Blackstone and KKR scored well on the key parameters. Brookfield Asset Management was attractive in some aspects, but I am deterred by its overly high portfolio concentration, relatively low amount of dry powder and likely overvaluation. TPG was a standout in the dry powder criterion, however it did not deserve much of a mention in other aspects.

All factors considered, my top picks would be Blackstone, followed by KKR, which I rate as 'buys'. I anticipate both of these to perform well and generate alpha. TPG and Brookfield Asset Management would be a 'hold' for me; I am less confident on their alpha potential.

A Contrarian Bias on Brookfield?

My bias on Brookfield Asset Management seems to be contrary to the prevailing Seeking Alpha authors' sentiments:

Bullish Sentiment on Brookfield Asset Management (Seeking Alpha)

{kind=link}

I notice my preference between Blackstone and Brookfield is the opposite to that of Dividend Sensei , who prefers Brookfield due to his judgement of faster and more stable dividends. This may be true if real assets grow much faster, however taking into account the higher valuation and preference for a balanced portfolio, I reiterate my view that Blackstone stands better. I do not pay much attention to dividends as I tend to focus more on total shareholder return, which more directly correlates to net worth accretion.

For further details see:

Blackstone And KKR: My Top Alt Asset Manager Picks