BX - Blackstone Missed Expectations Implications For Brookfield Asset Management

2023-10-22 22:13:14 ET

Summary

- Blackstone missed earnings expectations in Q3, primarily due to low fundraising and low performance fees.

- Brookfield Asset Management is yet to report its Q3 earnings, but implications from Blackstone's results suggest a potential slowdown in fundraising for BAM.

- BAM's earnings are not as dependent on investment performance as Blackstone's, making it a more stable investment option.

Dear readers,

I'm very fond of investing in alternative asset managers such as Blackstone ( BX ) or Brookfield Asset Management ( BAM ). They both run relatively similar asset-light businesses, but there are differences which I want to highlight in this article.

Blackstone has already reported their Q3 2023 earnings and missed expectations by a wide margin. Brookfield Asset Management is yet to report theirs on November 6th, but there are some major implications that we can draw from Blackstone's results. My hope is that this article will give you a better idea of what to expect from BAM.

Blackstone missed expectations

During the third quarter, BX has earned $0.94 per share in distributable earnings, which was 7% below expectations of $1.01 per share.

As a result, the share price has sold off by nearly 8% on the announcement and gave up most of the gains from the run-up that the stock had prior to being included in the S&P 500 ( SPX ) in mid-September. The stock now trades around $95 per share, which corresponds to about 25x distributable earnings.

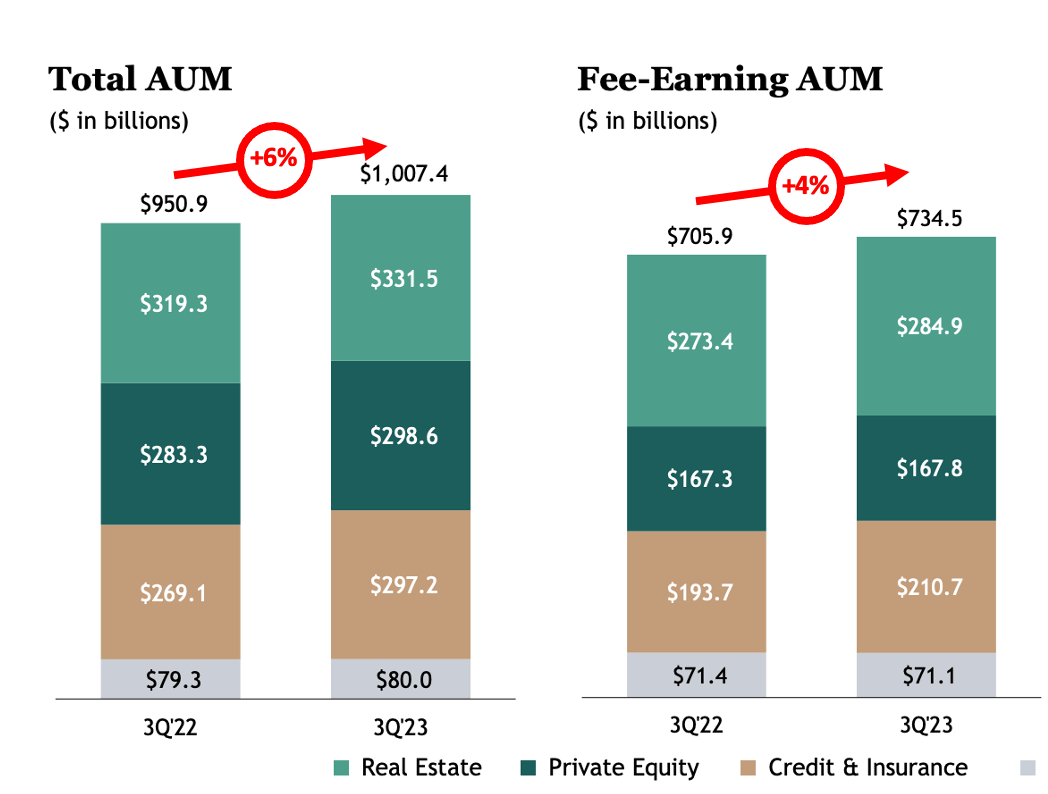

The earnings miss was primarily attributable to two things. Low fundraising and low performance fees. The significant slowdown in fundraising has resulted in subpar Total AUM growth of 6% YoY and only 4% YoY for Fee-Earning AUM. That's significantly below the target of 10-12%.

{kind=link}

BX Presentation

Frankly, a slowdown was expected and we could already see it in Q2 data, but the fact that there was zero growth in AUM over the third quarter suggests that the fundraising environment is getting worse than expected. Moreover, with the 2-year treasury yield at an all-time high once again and a hawkish Fed, I don't think things will improve anytime soon.

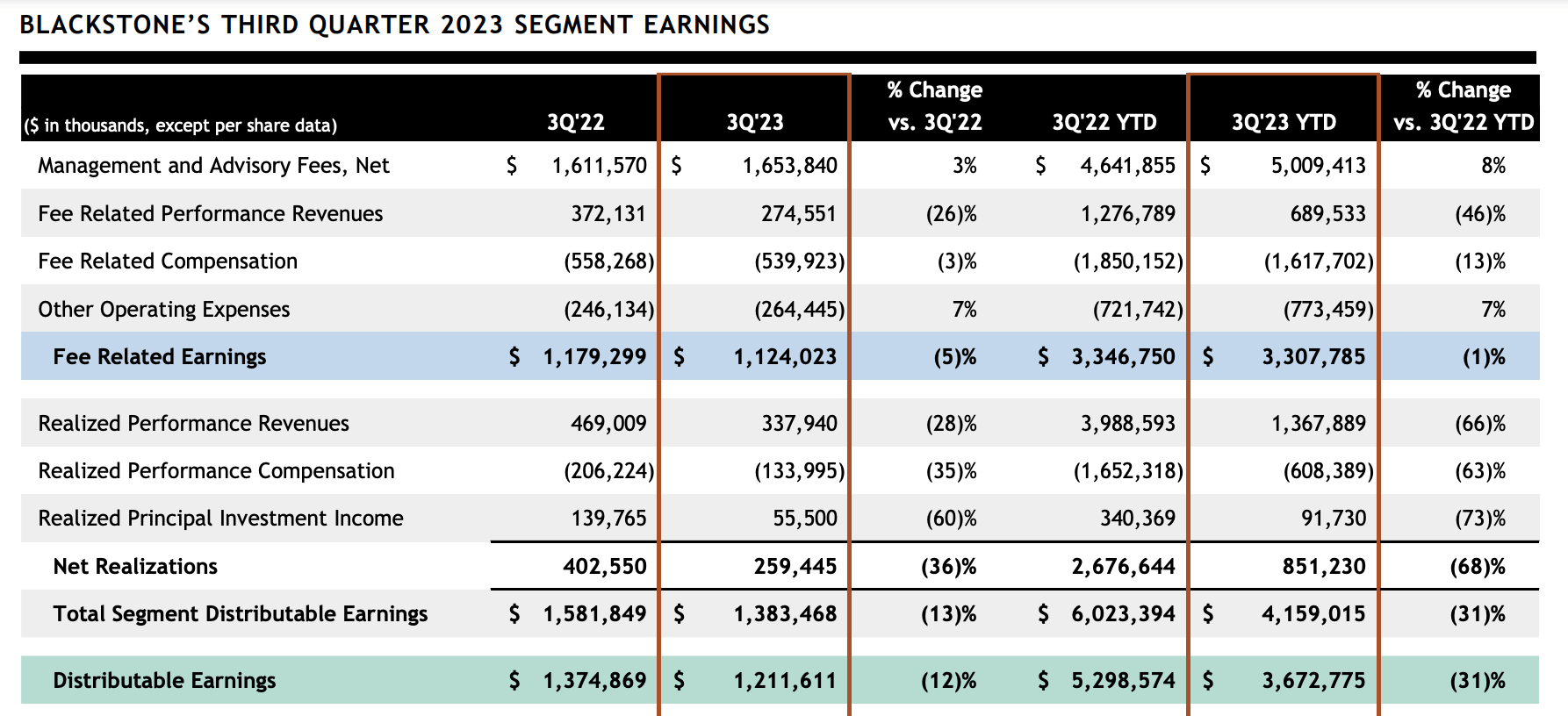

As a result of meager AUM growth, management fees, which account for most of Blackstone's earnings, have grown by only 3% YoY to $1.65 Billion. That's below expectations and below long-term growth targets for the company, but it's not what caused the company to miss expectations by such a wide margin.

The main problem lies in performance revenues (also known as the carry). This is extra revenue which Blackstone earns on top of its 1% management fees if its investment performs well. Performance fees are much less predictable and are the main reason why overall earnings are volatile and why Blackstone has adopted the variable dividend policy. Carry essentially magnifies good results in good times but hurts performance in bad times.

Over the most recent quarter, Fee-related performance revenues have declined by 26% YoY to just $274 Million. On a year-to-date basis, the decline was even more pronounced at -46% YoY. Consequently, total Distributable Earnings during the third quarter came in at $1.21 Billion, flat compared to Q2 2022 and down 12% YoY. This is why the stock missed expectations.

{kind=link}

BX Presentation

One positive takeaway from the third quarter is that outflows have slowed from $13 Billion in Q2 to $9 Billion in Q3 and remain quite low and below 1% of Total AUM. Moreover, the inflow-to-outflow ratio has improved slightly as Blackstone was able to raise $2.77 for every $1.00 of outflows (vs $2.50 last quarter). This shows that Blackstone's fee-related earnings are quite resilient and sticky.

So what is the main takeaway here?

Fundraising has come to a standstill during the third quarter, outflows remain low and performance fees are terrible as a result of tough market and economic conditions. Most importantly, future growth prospects over at least the next couple of quarters are poor, yet BX trades at 25x earnings (incl. performance-related earnings which are volatile and unpredictable). All things considered, I rate BX a HOLD and wouldn't add here.

Implications for BAM

Before diving into the specifics, there's one key difference between BX and BAM that you need to understand. BAM was created as a spinoff from Brookfield Corporation ( BN ) and as part of the deal, the corporations retained the carry for the first five years. In other words, BAM is a management-fee pure play and will not earn carry until the end of 2027.

We've just seen that the carry makes earnings very volatile and because it is very unpredictable Performance-related earnings are valued at a much lower multiple than Fee-related earnings ((FRE)). The fact that BAM only earns FRE can actually be an advantage because it will allow for very smooth growth in earnings and consequently dividends.

This means that the biggest reason why BX missed expectations is actually not an issue for BAM, simply because their earnings don't directly depend on the performance of their investments (yet).

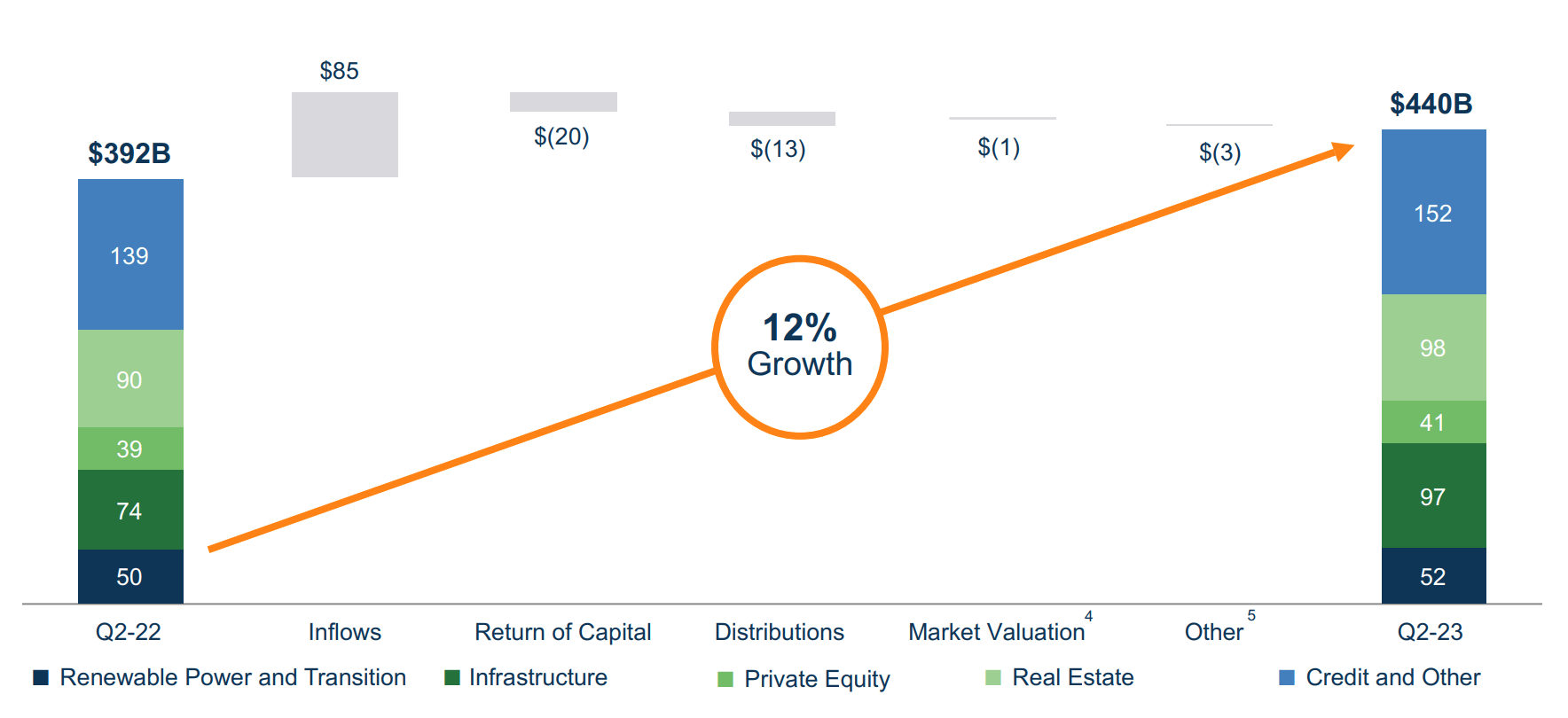

Unfortunately, the same cannot be said for fundraising which is just as essential for BAM as it is for BX. Over the last four (reported) quarters, BAM was able to raise $74 Billion which has increased Fee-bearing AUM by 12%. Broken down quarter by quarter, fundraising stood at $29 Billion, $15 Billion, $13 Billion, and most recently in Q2 2023 $17 Billion.

{kind=link}

BAM Presentation

So far, fundraising has been solid and if BAM can continue to average $15 Billion of new Fee-bearing capital per quarter, they will be on track to deliver 13% YoY AUM growth. That would be almost at their 15-20% long-term growth target. But having reviewed Blackstone's earnings, I expect that BAM will see a slowdown in Q3 as well with total fundraising around $10 Billion.

I don't know what the future holds, but it seems that a period of lower AUM (and therefore FRE) growth is likely ahead of us and BAM may not be able to hit their 15-20% target in the short to medium-term.

BAM currently trades at $30.4 per share which corresponds to 22.5x FRE. That's in the middle of the 20-25x FRE range that I normally consider as fair for asset-light alternative asset managers. Moreover, it's below BX's multiple of 25x, despite higher reported growth (so far).

But here's the thing.

If BAM's growth also slows, the stock could quite easily re-rate to 20x earnings, perhaps even lower if growth is really bad. That's why, although I prefer BAM to BX, I also rate it a HOLD and wouldn't add here, unless you expect BAM's Q3 fundraising to be significantly better than Blackstone's.

Bottom Line

BX's recent earnings reveal that the fundraising environment has become quite difficult, but also show that Fee-related earnings are very resilient. BX has taken a hit and now trades at 25x earnings. BAM which trades at just 22.5x earnings is yet to report its Q3 earnings. I expect BAM's fundraising to slow in Q3 and FRE growth to slow in the medium term. Between the two, I prefer BAM for its lower valuation and lower volatility thanks to the absence of carry, but I'm not buying either at this time.

For further details see:

Blackstone Missed Expectations, Implications For Brookfield Asset Management