STWD - Blackstone Mortgage Trust: A Higher-For-Longer Rate Bet With A 12.6% Yield

2023-10-28 08:20:29 ET

Summary

- Blackstone Mortgage Trust is a core portfolio holding for passive income investors seeking predictable dividend income from a leading commercial real estate investment trust.

- The trust's floating-rate positioning is a compelling reason to own it, as it should produce higher net interest income in a rising-rate environment.

- Despite a decline in portfolio value due to loan repayments, Blackstone Mortgage Trust has a well-performing loan portfolio and stable dividend coverage.

As far as I am concerned, Blackstone Mortgage Trust, Inc. ( BXMT ) is a core portfolio holding for passive income investors that want to invest in a leading commercial real estate investment trust and achieve predictable dividend income from the company’s stock.

Blackstone Mortgage Trust generated 126% dividend coverage in the third quarter and the business originated new loans, too. Rising loan loss reserves are set to prevent a fall-out from potentially increasing loan losses.

The most compelling reason why passive income investors should want to own Blackstone Mortgage Trust is the trust’s floating-rate positioning which should produce higher net interest income in a rising-rate environment.

My Rating History

My stock classification on Blackstone Mortgage Trust was Buy as I considered the CRE trust to be of high-quality in terms of dividend coverage.

The discount to book value was also a strong reason to consider buying the stock (the discount is now much larger, too). In 2023, fears have grown over the state of the U.S. office real estate sector and, in relation, the impact on portfolio quality for CRE trusts.

Taking into account that the trust’s portfolio remained well-performing in 3Q-23 and that it increased its CECL reserve for credit losses, I think passive income investors can sleep well with BXMT in their portfolios.

A Higher-For-Longer Rate Hike Bet

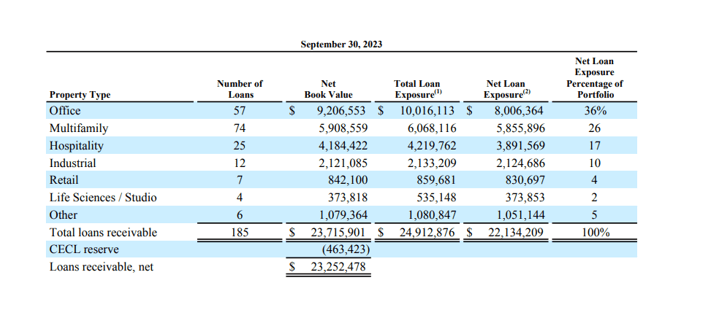

Blackstone Mortgage Trust’s investment portfolio was comprised of loans made to the office, multi-family, hospitality, industrial, retail and life science sectors. The office classification made up the majority of the trust’s investments with a representation of about 36%, up 1 percentage points QoQ.

Blackstone Mortgage Trust had a total portfolio value of $22.1 billion at the end of the third quarter compared to $23.1 billion in the prior quarter and the decline in portfolio value was due primarily due to loan repayments. As of September 30, 2023, 99% of the REIT’s loans by principal balance were floating-rate. Thus, BXMT remains a compelling rate-sensitive bet on a higher-for-longer rate environment.

{kind=link}

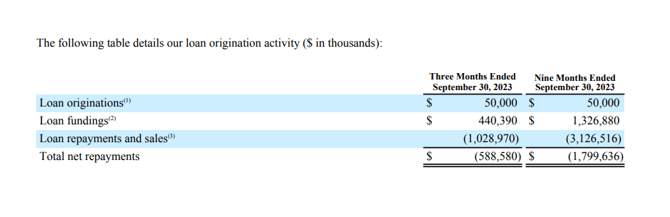

Blackstone Mortgage Trust, like I said, originated a small amount of new loans of about $50 million, in the third quarter. The REIT’s origination business pretty much ground to a halt in 2023 due to higher financing costs slowing demand for new investment capital.

Loan repayment and sales were $1.0 billion in BXMT’s third quarter which equals about the average of repayments throughout the year so far. Primarily due to loan repayments and suppressed loan activity, Blackstone Mortgage Trust’s portfolio value fell by about $1.0 billion in 3Q-23.

{kind=link}

Portfolio Quality

Blackstone Mortgage Trust still has a well-performing portfolio in the third quarter with 95% of loans performing according to expectations. A well-performing loan portfolio is a prerequisite for stable dividend coverage and Blackstone Mortgage Trust is not disappointing in this regard.

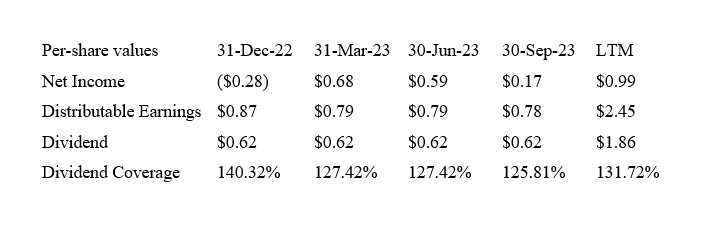

Stable Dividend Coverage (Blackstone Mortgage Trust)

Estimates for rising credit costs are reflected in Blackstone Mortgage Trust’s CECL (current expected credit losses) reserve which in the third quarter increased again.

The total CECL reserve totaled $477 million, reflecting an almost 39% increase since the end of 2022. By raising its CECL reserve, Blackstone Mortgage Trust guards against a future default of investment loans.

CECL Reserve (Blackstone Mortgage Trust)

Dividend Coverage

Blackstone Mortgage Trust earned $0.78 per share in distributable earnings in the third quarter, one cent less than it did in the previous quarter. With an LTM dividend coverage ratio of 132%, Blackstone Mortgage Trust is a solid passive income play for investors that are more concerned with income generation than stock appreciation.

The trust’s excess dividend coverage is driven by growth in distributable earnings, which were up 10% YoY (on a per share basis).

{kind=link}

High Margin Of Safety

Blackstone Mortgage Trust’s stock is selling at a larger discount to book value than in July, despite portfolio quality remaining robust and the trust guarding against an increase in loan defaults by increasing its loan reserves.

Furthermore, the stability of dividend coverage has not been affected in the third quarter at all and the mortgage REIT easily earned its dividend with distributable earnings.

All three major mortgage trusts, Blackstone Mortgage Trust, Starwood Property Trust, Inc. ( STWD ) and Ladder Capital Corp. ( LADR ) are value and income bargains, in my view.

The discount to BXMT today is 24% whereas STWD sells at a 13% discount and Ladder Capital at a 21%. I like all three mortgage trusts based on their large discounts to book value, stable dividend coverage and floating-rate exposure.

I will deliver updates for Ladder Capital and Starwood Property Trust, as usual, once the trusts have reported results for 3Q-23. Starwood Property Trust, based on diversification and stability of distributable earnings, is the safest CRE company to own , in my opinion.

Why Blackstone Mortgage Trust Could See A Higher/Lower Valuation

Passive income investors must pay close attention to the trust’s portfolio quality and dividend coverage, a deterioration in either of those two key metrics would likely signify trouble for the dividend moving forward.

What potentially could become a problem for Blackstone Mortgage Trust is that the trust has relatively high exposure (36%) to the office sector. A rise in defaults in this particular sector might result in higher loss reserves and lower distributable income moving forward.

My Conclusion

Blackstone Mortgage Trust’s 3Q-23 reminded passive income investors why the 12.6% yield is not as risky as it looks: The dividend remained robustly covered by distributable earnings in the third quarter.

Blackstone Mortgage Trust earned 126% of its dividend in 3Q-23 and even though this marked a slight decline from last quarter’s dividend pay-out ratio, the dividend itself is well-covered and passive income investors should continue to enjoy a $0.62 per share per quarter dividend moving forward.

The portfolio overall kept performing well and BXMT even saw a small increase in loan originations in 3Q-23. With its high floating-rate loan exposure of 99%, Blackstone Mortgage Trust remains a directional bet on higher interest rates as well. The stock is cheap based on book value and a buy.

For further details see:

Blackstone Mortgage Trust: A Higher-For-Longer Rate Bet With A 12.6% Yield