BXMT - Blackstone Mortgage Trust: Office Doom Hangs Like The Sword Of Damocles

2023-03-22 10:43:50 ET

Summary

- Blackstone's commercial mREIT BXMT has seen it's stock price drive off a cliff recently.

- Concerns regarding the company's office exposure (~40%) have many selling the stock.

- Morningstar has BXMT's five-year average P/B at 1.13x versus the 0.70x it trades at currently.

- What about that 13% dividend yield?

- Keep reading for a review of the REIT, a comparison to peers BRSP and TRTX, and where I think things stand.

Over the last year I’ve found a number of commercial mortgage REITs during my screening process. The first one I really dug into was ACRES Commercial Realty Corp. ( ACR ) where I wrote up their Series C preferred shares in July 2022. I followed up my review with an article in January 2023 comparing ACR’s two different preferred shares , ACR-C and ACR-D.

Next I researched BrightSpire Capital ( BRSP ) back in September 2022 when they were trading at a P/B of 0.62x with peers trading at an average of 0.88x. The company is amidst a potential turnaround effort which included internalizing management of the REIT. I still believe in the long term story and wrote an update about them earlier this month .

My most recent research centered on another potential turnaround with TPG RE Finance Trust ( TRTX ) trading at a P/B of 0.60x. The REIT tapped Doug Bouquard, former head of U.S. commercial real estate at Goldman Sachs, to lead the firm last year and since then they’ve worked to preempt the downcycle.

I’ve run into Blackstone Mortgage Trust a lot in my research. Typically I encountered it as trading near the top of the peer group in terms of P/B multiple. Here are two examples of BXMT trading at P/B of 0.95x in September and 0.82x just recently at the end of February.

Author's SA Article: P/B comparison chart of commercial mREITs.

{kind=link}

Author's SA Article: P/B comparison chart of commercial mREITs.

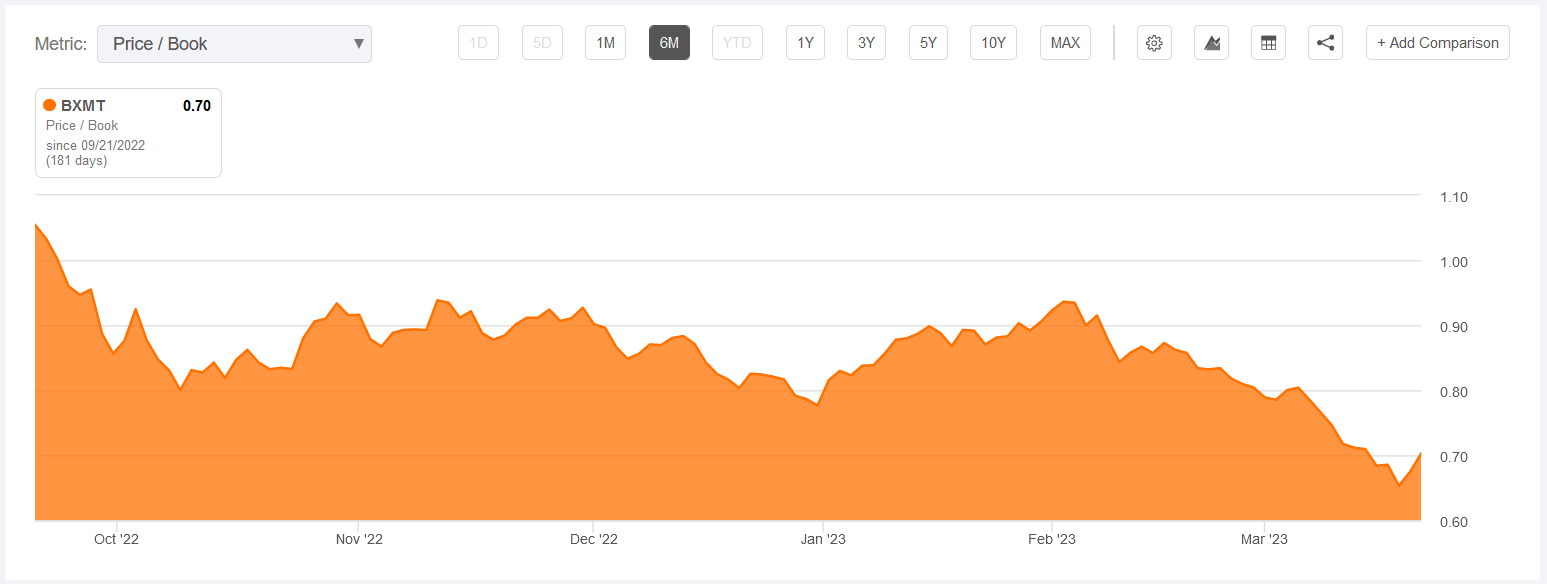

What a difference a few weeks makes. Today Seeking Alpha pegs their P/B at 0.70x at a price of $18.50 per share.

{kind=link}

Seeking Alpha: 6-month P/B BXMT Chart.

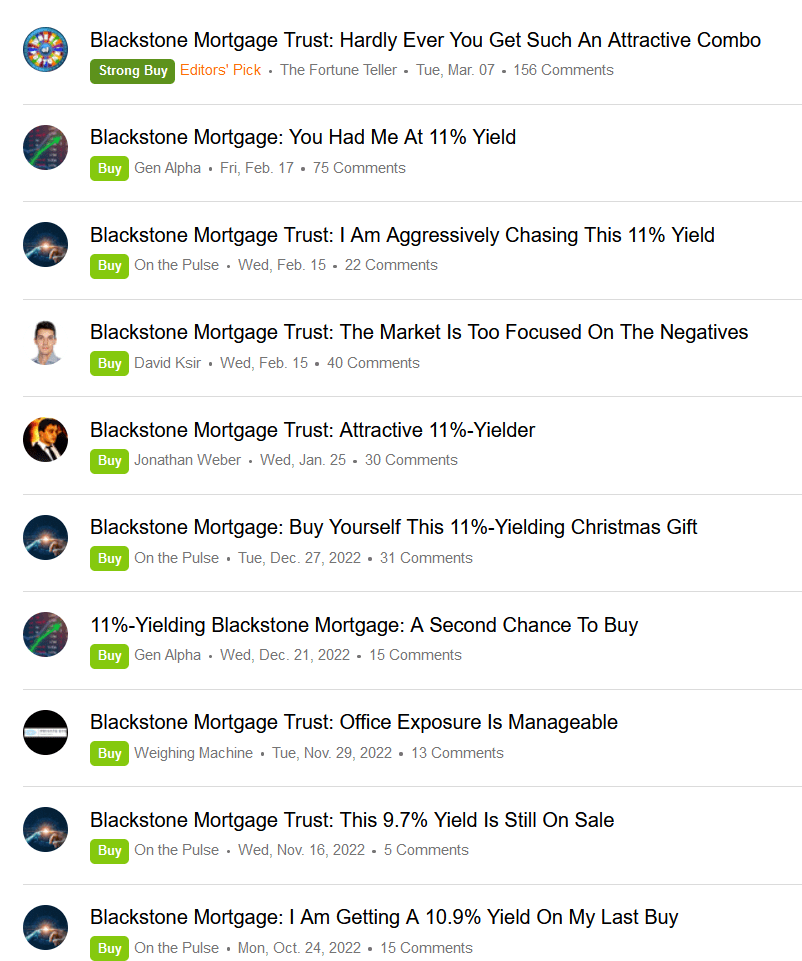

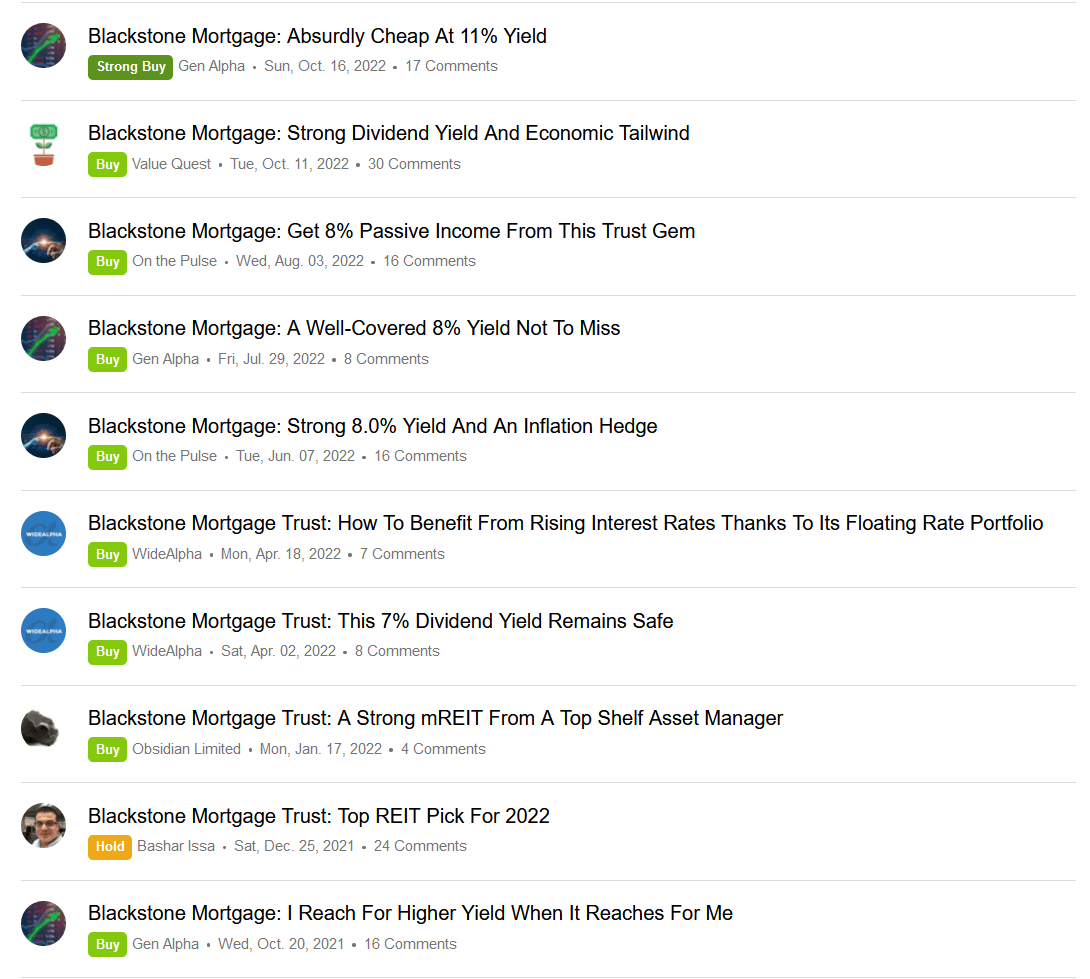

Before everyone on Seeking Alpha became bank experts this REIT was a favorite. You would have to go back to December 2021 before you find any article without a BUY or STRONG BUY rating, and even this article wasn’t bearish and simply offered a HOLD rating. As far as Seeking Alpha contributors go, Blackstone Mortgage Trust has not held a SELL rating since February 2020 . The author who gave the sell recommendation in February 2020 gave it a buy rating in March 2020 after it collapsed 50% in value along with other mortgage REITs in the COVID crash.

{kind=link}

Seeking Alpha: BXMT Articles.

{kind=link}

Seeking Alpha: BXMT Articles.

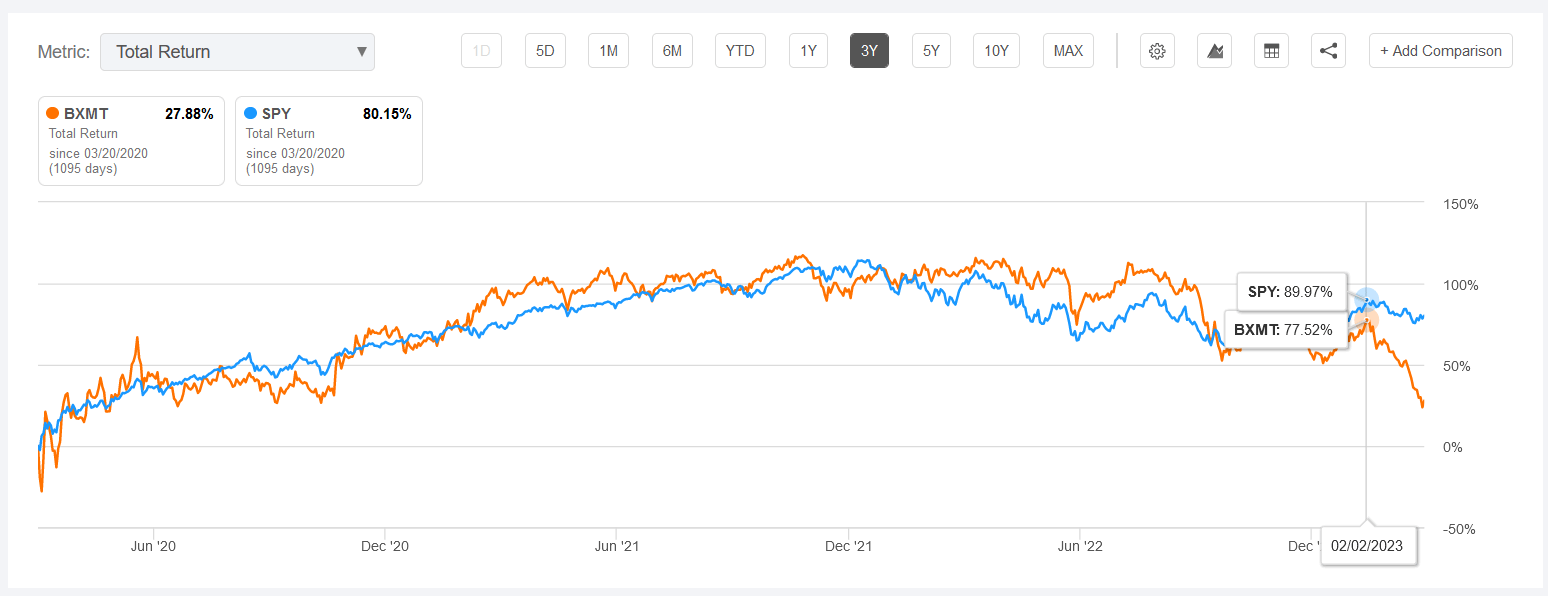

With the stock trading at historically low P/B multiples, performance could be at a trough right now, so keep that in mind as we look at this three-year performance chart. We’re looking at total return results for BXMT and SPY for comparison.

{kind=link}

Seeking Alpha: 3-year total return chart of BXMT and SPY.

The first thing I note is that broadly speaking, across this time frame the variance between the two’s results has been fairly minimal. That makes the cliff BXMT has flown off since the beginning of February all the more noticeable. That’s not to say that one should expect the two to converge somehow moving forward.

So what’s beneath the performance here? Let’s take a look before we take a bite of this 14% annual dividend high yielder.

What is BXMT’s Current Financial Health?

Let’s start by getting a baseline of the company’s financial position. We’re going to do this in comparison with the two mREITs mentioned earlier: BrightSpire Capital and TPG RE Finance Trust. Here’s the data.

| (millions except per share data) |

| Price as of March 21st, 2023 |

| $18.50 |

| $6.09 |

| $7.16 |

| Number of common shares |

| 172.284 |

| 128.872 |

| 77.41 |

| Market value of common shares |

| $3,187 |

| $784.83 |

| $554.26 |

| Debt |

| $20,158 |

| $1,824 |

| $4,160 |

| Total Capitalization |

| $23,345 |

| $2,609 |

| $4,714 |

| Total Equity |

| $4,544 |

| $1,389 |

| $1,121 |

| Book Value per Share |

| $26.38 |

| $10.78 |

| $14.48 |

| Revenue |

| $1,339 |

| $364 |

| $306 |

| Distributable earnings |

| $494 |

| $126 |

| $84 |

| Distributable earnings per share 2022 |

| $2.87 |

| $0.98 |

| $1.08 |

| Distributable earnings per share 2021 |

| $2.62 |

| $0.87 |

| $1.09 |

| Distributable earnings per share 2020 |

| $2.48 |

| $1.01 |

| -- |

| Distributable earnings per share three-year average |

| $2.66 |

| $0.95 |

| $1.09 |

| Current dividend per share |

| $2.48 |

| $0.80 |

| $0.96 |

| Ratios |

| Dividend yield |

| 13.41% |

| 13.14% |

| 13.41% |

| Dividend yield on book value |

| 9.40% |

| 7.42% |

| 6.63% |

| Distributable Earnings / Dividend |

| 1.16 |

| 1.23 |

| 1.13 |

| Price / Book |

| 0.70 |

| 0.57 |

| 0.49 |

| Price / 3-year distributable earnings |

| 6.96 |

| 6.39 |

| 6.60 |

| Distributable Earnings / Revenue |

| 36.93% |

| 34.70% |

| 27.32% |

| Return on Equity |

| 10.88% |

| 9.09% |

| 7.46% |

| Current Assets / Current Liabilities |

| 1.32 |

| 1.87 |

| 4.99 |

| Debt / Equity |

| 4.44 |

| 1.31 |

| 3.71 |

*Distributable earnings for TRTX were negative in 2020 as part of their historical issues. I excluded it as an outlier for our comparisons.

Commercial mREITs are typically levered vehicles so it’s no surprise to see Blackstone at a pretty high 4.44x Debt/Equity ratio. Managing liquidity here will be important as their current assets near current liabilities. From a debt perspective, Blackstone is the most levered with the least liquidity compared to these peers.

The perspective is a bit better when we look at things from a profitability standpoint given Blackstone’s highest return on equity and net-profit margin at 36.93%. This above average profitability coupled with Blackstone’s outsized reputation globally likely explains why the REIT is typically at the top of the pack in terms of P/B valuation. And as I mentioned, BRSP and TRTX are both amidst turnarounds due to poor performance in the past.

Dividend coverage for each of these issues is in the same range, as well as their current dividend yield. What’s notable is that Blackstone is actually paying out a higher yield on their equity when compared to the other two. That could be a potential indicator of stress if there continues to be adverse conditions in the market.

All three of these companies are battling credit risk issues as rising interest rates have pressured their predominantly floating rate loan portfolios. On the one hand, this has helped to drive earnings higher for Blackstone and peers, but it’s also increased the credit risk of their borrowers who are seeing much higher interest payments than perhaps expected.

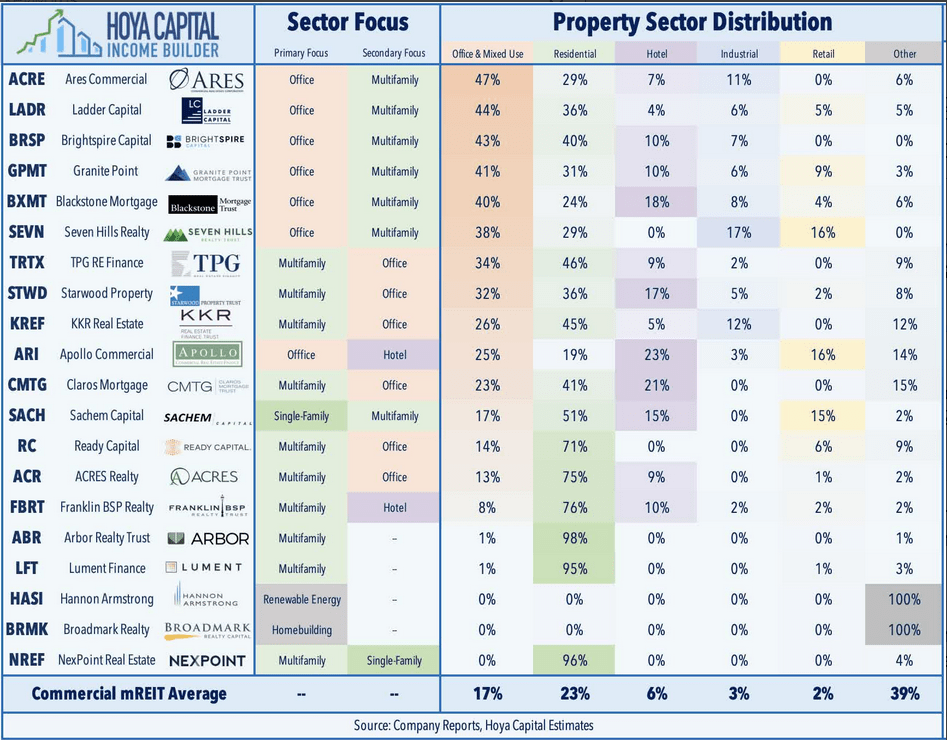

Commercial property has been dealing with the fallout of retail values for years. Then came the pandemic and the flight from the office. Office properties have been in the crosshairs as a result as owners look to make use of these spaces. Some of the downward pressure on Blackstone is related to their historical primary focus in the office sector. Take a look at this graphic produced by fellow SA contributor Hoya Capital in their recent real estate outlook .

{kind=link}

Hoya Capital: Commercial mREIT Sector Exposure

From this we can see that BXMT and BRSP both are in the top-five commercial mREITs by concentration in office & mixed use properties at 40% and 43% respectively. Clearly this is well above the average of 17% and has pressured Blackstone this past year as evidenced by their increase of $201.5 million (+62%) in their current expected credit loss or CECL reserve bringing it to $326.1 million at the end of 2022.

Currently they have five office loans that are rated at a risk rating of 4 or 5. These are loans that are at risk of principal loss which the CECL reserve is attempting to account for. Management noted that their high risk office loans represent only 5% of the overall portfolio in their most recent earnings call . That means they have 35% of their office loans which have not been at risk to date.

Depending on one’s perspective moving forward, these office properties could be a problem. For comparison we can consider that this detail management provided regarding the loans they already have reserved against. “ On average, our reserves are 20% of our loan balance and imply asset value reductions of nearly 50%. ”

Those are steep asset value reductions but in the next turn management assures listeners that this is not “ typical ”. They go on to share these details about their office exposure.

“54% of our office loans are backed by assets that are newly built or recently substantially renovated, with an average vintage of 2021 and an average origination LTV of 60%. 34% of the office portfolio, most of the remainder, carries one or more significant credit enhancing qualities, such as particularly low leverage, high debt yield, location in high growth Sunbelt markets or material additional sponsor equity commitment in the last year.”

Whatever one’s opinion might be regarding the future of office, we can see that Blackstone does not seem concerned too much about their exposure. With 97% of the loan portfolio performing currently, things would need to take a sharp turn for there to be an impact. If we take their word for it, management believes that it would take “ lasting declines of 30% to 40% in real estate values for us to experience a loss at our position in the capital structure. ”

Historically Low Valuation, But Office Doom Lingers

If one is comfortable with the exposure to office here, this REIT may offer opportunity. Morningstar has BXMT’s five-year average P/B rating at 1.13x – well above the 0.70x it’s near today. A reversion to the mean here would imply 61% upside.

Investors must keep in mind the B component of this equation. If there’s an acceleration of defaults in the office sector, book value will take a hit – so even if it gets back to 1.13x P/B in that case investors may lose money. Take a look at the string of office defaults reported by the Commercial Observer earlier this month.

“Aside from Brookfield’s default in Downtown Los Angeles the other dominos include RXR, which is negotiating with lenders to convert two New York City office buildings to residential. In Washington, D.C., a $38.1 million commercial mortgage-backed securities ((CMBS)) loan on an office building that houses the U.S. Department of Treasury is headed to special servicing . And, in perhaps the most substantial sign of distress, Columbia Property Trust, which owns in San Francisco, New York and Washington, defaulted in February on $1.7 billion in debt backed by seven of its office buildings.”

The Brookfield default referenced was related to two office properties worth $784 million. Blackstone (not BXMT, but the head honcho BX ) themselves defaulted on a $562 million note backed by 3.6 million square feet of office and retail properties in Finland. Adding all of these up we are seeing over $3 billion in office defaults here.

Blackstone defaulted after seeking an extension from the holders to liquidate – but talks must have fallen through and they chose to strategically default instead. If BXMT’s manager is choosing to strategically default on office properties they own, who’s to say that this trend won’t continue? I’ll acknowledge that there may be some geopolitical risk involved here as well given the location of the properties.

Investors here must make themselves comfortable with the ramifications and outlook on the office sector before they make an investment. In a worst case scenario for BXMT, issues with their office properties could lead them to debt covenant issues. These covenants are as follow:

-

Our ratio of EBITDA to fixed charges, as defined in the agreements, shall be not less than 1.4 to 1.0;

-

Our tangible net worth, as defined in the agreements, shall not be less than $3.6 billion as of each measurement date plus 75% to 85% of the net cash proceeds of future equity issuances subsequent to December 31, 2022

-

Cash liquidity shall not be less than the greater of (i) $10.0 million or (ii) no more than 5% of our recourse indebtedness.

-

Our indebtedness shall not exceed 83.33% of our total assets.

The major one I could see tripping them up is the fourth. If we look at total assets at the end of last year we see $25.4 billion compared to their $20.2 billion in debt. This puts their Debt / Total Assets at 79.5%.

If asset values decline by $1.2 billion (-4%) to $24.2 billion then they would be right at the 83.33% limit. Of course this assumes that their debt amount remains level at $20.2 billion. Net book value of their office portfolio is $9.5 billion. Assuming that 5% of this amount is related to already impaired loans that leaves us with roughly $9 billion which has not been specifically reserved against. So it would take a 13% haircut to the rest of these office properties to cause a $1.2 billion decline.

These are considerations and estimations that one looking to invest here needs to keep in mind. It’s not one limited to BXMT though as its peers with office allocations are dealing with the same challenges. Yet investors here would be wise to balance the risks as a liquidity crunch could be a real issue in today’s environment.

I’m not suggesting that the REIT is in any immediate danger – moreso just attempting to give readers a sense of the risk profile involved. And how one might make attempts at stress testing the portfolio to see where it might cause issues.

Reputation or not, no business is immune to issues.

Blackstone Mortgage Trust Investment Analysis Takeaways

There are reasons why I own BRSP and TRTX, but not BXMT. Historically it was simply because Blackstone’s REIT was trading at higher P/B multiples and in the case of commercial mREITs I think that’s one of the better valuation methods. My attraction to the sector started with depressed multiples below 0.70x P/B and I wouldn’t have expected to see BXMT hit those levels.

The reason I look for companies trading at a discount to book value is for the simple reason Benjamin Graham discussed in The Intelligent Investor back in 1949: Margin of Safety . Graham devotes the entire final chapter of this book to this idea as “ the Central Concept of Investment ”.

Here’s a reflection of his about the concept:

“The margin-of-safety idea becomes much more evident when we apply it to the field of undervalued or bargain securities. We have here, by definition, a favorable difference between price on the one hand and indicated or appraised value on the other. That difference is the safety margin. It is available for absorbing the effect of miscalculations or worse than average luck. The buyer of bargain issues places particular emphasis on the ability of the investment to withstand adverse developments.”

[pg. 281-282; The Intelligent Investor, 4th edition; Benjamin Graham.]

Blackstone Mortgage Trust trades at a discount to its book value currently which may provide a margin of safety. Risks are mainly related to credit issues in their portfolio which could trickle upward and impact their debt covenants and cash flows. A deeper than expected recession could stress the portfolio further in a time of tightening liquidity.

For my own purposes, BXMT still doesn’t look as appealing to me as BRSP and TRTX. The reason being is different for each.

BrightSpire not only manages a loan portfolio but also directly owns a selection of real estate in Europe. I like the diversification of owning hard assets internationally and their recent shift to internalization (rather than being externally managed like Blackstone) means that management interests are likely to be more aligned moving forward. Cost reductions are already being realized as a result of this internalization as well. All of these things coupled with BRSP’s lower debt profile, higher liquidity, and lower valuation give me confidence.

TRTX is a bit of a different story. What I like there is the high liquidity they have which has been built intentionally. Management has been proactive in engaging with their borrowers, conservative with their CECL reserves, and have aggressively reduced their exposure to the office sector. And they trade at an even steeper discount to book value. I don't think the market has fully appreciated the strategic changes made here.

That said, I don't think BXMT is a bad investment. They may have some challenges balancing their liquidity moving forward, as with all of these commercial mREITs, but investors have the expertise and resources of Blackstone at work to preserve the portfolio. With the stock trading at an above-average discount to book value this may represent a rare opportunity. But it could also represent a risk.

For those that are interested here, a deeper dive into their loan portfolio and office exposure specifically would be instructive.

For further details see:

Blackstone Mortgage Trust: Office Doom Hangs Like The Sword Of Damocles