HTFC - Blackstone Secured Lending: Delivering Results With An ~11% Yield

2023-11-22 14:04:26 ET

Summary

- Blackstone Secured Lending Fund announced decent quarterly results with rising net investment income and also saw NAV per share increase.

- The company's conservative approach and limited non-accruals reflect its strong position, with Blackstone being a top-tier manager in the alternative asset world.

- The BDC's dividend coverage remains strong, providing flexibility and helping to continue to fuel growth in NAV per share.

Written by Nick Ackerman.

Blackstone Secured Lending Fund ( BXSL ) announced its latest results , and the third quarter was not a blowout, but it was a decent one. There is absolutely nothing wrong with being slow and steady, either. This is a business development company ("BDC") managed externally by Blackstone ( BX ), one of the largest alternative asset managers in the world.

This was the first quarter that I've held a position in BXSL, after taking an initial position recently ahead of earnings. In taking a position in BXSL, I put some fresh capital to work, but it also came from selling out of Horizon Technology Finance ( HRZN ) after its recent pop from what felt like an overall mediocre quarter.

HRZN was starting to push toward the higher end of their premium range as well after bouncing higher. Though it is trading below the massive premiums we saw during 2021 and at the start of 2022, the premium is higher than most of the levels seen prior to these outlier years.

HRZN is working through several issues from a portfolio perspective, and being a venture-focused BDC is naturally going to be more volatile. I believe going up in quality to a more traditional BDC such as BXSL might be the better move over the short and medium term. This would likely be the right move if we get that inevitable recession that all economists predict. Of course, that has seemed to be the message going on for the last couple of years now. Only time will tell if it was the right move.

Valuation

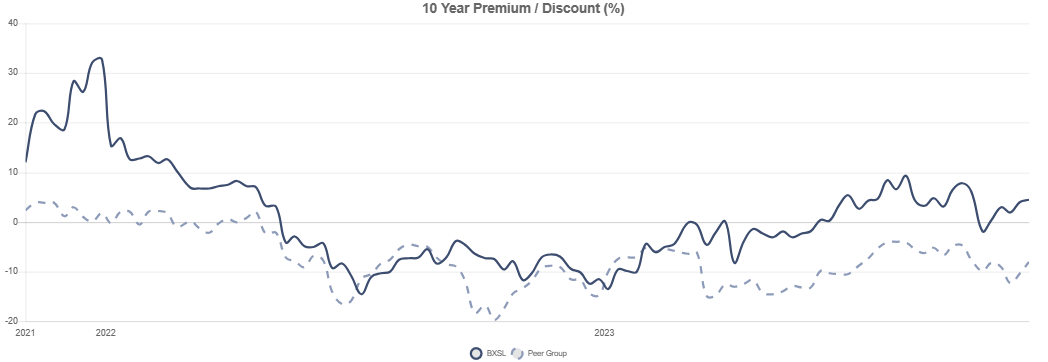

I would have taken a larger position in BXSL, but at near the higher end of their discount/premium range, even as net asset value per share rose a bit, I was more reserved. Ultimately, I'd be more interested in adding to this position over time when it sinks closer to a discount if that opportunity presents itself. Externally managed BDCs tend to trade at discounts, but perhaps the Blackstone name might be able to garner some premium.

Trying to define a discount/premium range for BXSL is also a bit more difficult as it is a relatively newer BDC, at least publicly. They were formed on March 26, 2018. Then was elected to be a BDC on October 26, 2018, with "loan origination and investment activities" beginning on November 20, 2018. Finally, the public didn't get access to BXSL until its IPO on the NYSE on October 28, 2021.

BXSL Discount/Premium History (CEFData)

{kind=link}

It initially popped to a massive premium, and that was probably really rewarding for those shareholders who held it while it was private and got in on the IPO. Capitalizing on that perfect opportunity for those investors to cash in, along with the sour market through 2022, led to BXSL beginning to trade at a discount for a fairly lengthy period of time relative to its public history. Only when the environment for investments started to look rosier - and perhaps those selling pressures from the initial pop toward the launch of the BDC - was it able to start to push toward a premium once again.

As mentioned above, I thought perhaps some of this premium was warranted due to the Blackstone name. Not only that, but it runs a solid portfolio with non-accruals at virtually zero (or less than 0.1%, to be more precise.) So far, we've seen that be the case as well, with CEFData showing that peers regularly trade at a lower valuation relative to BXSL. Even during 2021, the discount was closer to peers but didn't slip below where their peers traded for an overly extended period of time, nor was it at any sort of deep relative discount.

Latest Quarter

On the surface, net investment income and NAV per share rose, and that's basically what one wants to see from BDCs. Additionally, non-accruals remain extremely low. First-lien senior secured debt also encompasses nearly the entirety of their portfolio, which has led to the portfolio primarily being positioned in floating rate securities.

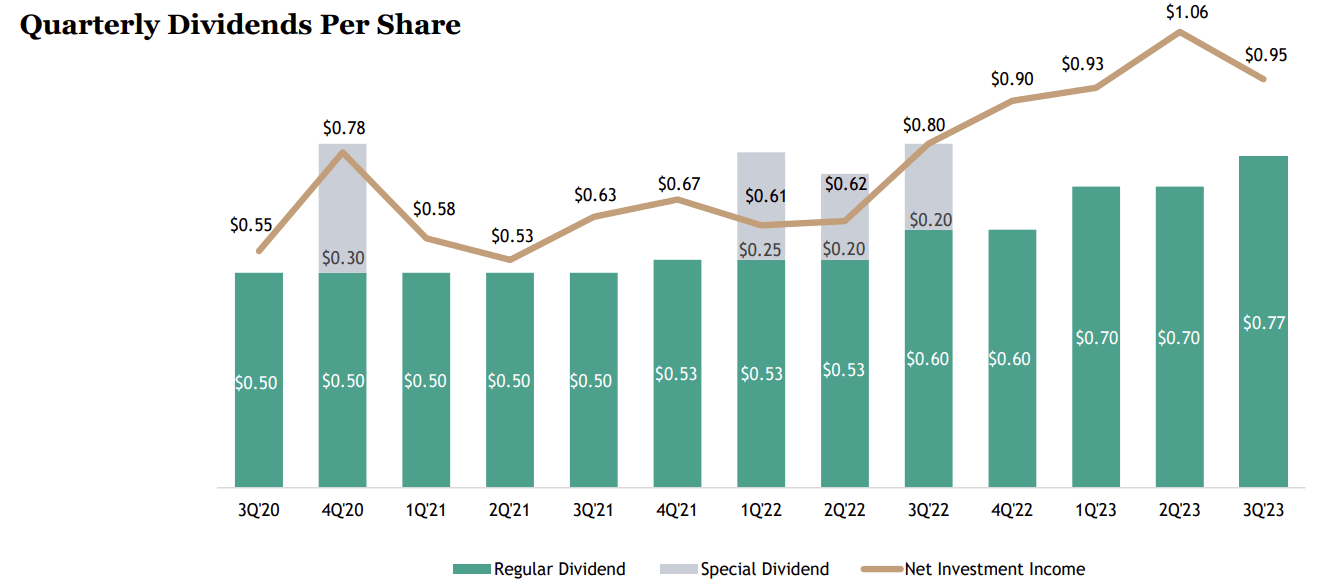

NII per share rose year-over-year from $0.80 to $0.95, representing a climb of nearly 19%. Given that they had only paid out $0.77 with their latest dividend, that helped provide a boost to the NAV per share. Dividend coverage given the Q3 NII came to 123%. That was down from last quarter as NII declined sequentially.

BXSL Dividend History Vs. NII (Blackstone)

{kind=link}

NAV per share moved from $26.30 to $26.54, good for an increase of $0.24 or nearly 1% from the prior quarter. $0.06 was chipped in to grow NAV as realized/unrealized gains. Year-over-year, NAV per share rose from the $25.76 level, representing an increase of $0.78 per share or an over 3% climb in NAV.

Given the latest dividend was also announced at $0.77, they are under-distributing, as they are required to pay out the majority of their earnings to investors, being a regulated investment company ("RIC"). That has started to lead to an excise tax in 2023, but at a tax of 4%, that's a fairly reasonable "cost" when they can earn 14%+ from their underlying loans.

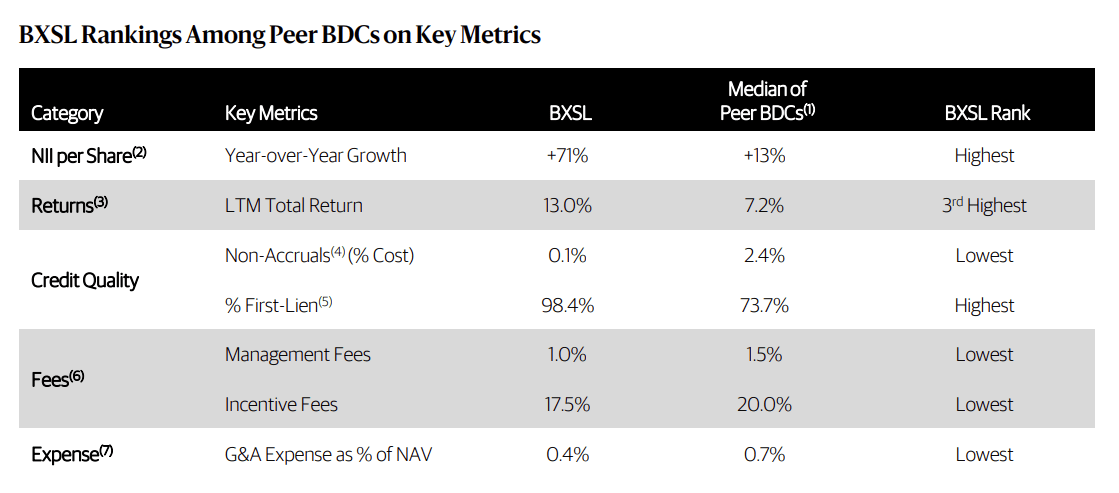

Of course, going into that 4% cost would also be the operating expenses of the fund. CEFData puts the non-leverage expense ratio at around 5%, meaning they'd still be earning a positive spread between the operating cost plus the excise tax. With their two-year IPO waiver period coming off, expenses are set to rise. The 0.75% management fee will go up to 1%. Their income-based incentive fee will also go from 15 to 17.5% now. These fees are below their peer BDCs, as noted in a prior presentation .

BXSL Ranking Vs. Peers (Blackstone)

{kind=link}

Keeping strong coverage of its distribution is something they are focused on doing as well, as it helps ensure the NAV per share will continue to grow or at least give it a much better chance to grow over time.

And as you can see, we’ve continued to focus on delivering high-quality yield to our shareholders building a level of confidence through continuing to raise our base dividends while also steadily building NAV per share. We believe that speaks to the funds ability to deliver for our shareholders despite macroeconomic headwinds.

That also means that if rates are cut, there is some cushion there as well when their floating rate exposure would start to see lower yields. 98.8% of their portfolio is in floating-rate debt, with 56% of their borrowings at fixed rates. The weighted average integrate they are paying is 2.88% on their unsecured debt, with the cost of debt at 4.94% in the latest quarter. So, in this case, their fixed-rate financing is lower than other BDCs that I follow, but it isn't detrimental to their operations. If the Fed starts cutting interest rates, it does mean they might be in a position where they are less impacted in terms of their own leverage.

Speaking of leverage, they've been continuing to work on deleveraging their portfolio. They made good progress on that front, with the latest quarter having leverage at 1.08x. That was down from 1.15x last quarter. As noted in their latest quarter, the overall target range is between 1 and 1.25x. That puts them on the lower end of their range, providing them with tons of flexibility going forward. They also noted debt maturities aren't too much of a concern in the near term.

Based on our pipeline activity, we would expect to remain within our target of 1x to 1.25x through the balance of the year. Additionally, we have low level of debt maturities over the next few years. The next maturity date for any of our outstanding debt facilities is 2025 with only 6% of debt maturing within the next 2 years and an overall weighted average maturity of 3.5 years. We continue to believe BXSL is well-positioned to maintain earnings in excess of our dividends as rates on 98.8% floating rate debt investments have continued to reset higher.

Conclusion

Blackstone Secured Lending Fund is in a strong position with the capacity to leverage up when they find the right deals. They are running a portfolio with very limited non-accruals currently, and that can be a reflection of their conservative approach and experience in the alternative asset world. The dividend coverage remains strong, and that gives them even more flexibility and helps grow NAV per share. The downside to that is they have to start paying excise tax, but as long as they continue to out-earn with higher yields than the associated costs, it can still be beneficial to shareholders in the long run.

For further details see:

Blackstone Secured Lending: Delivering Results With An ~11% Yield