KKR - Blackstone Vs. Apollo: The Winner Might Shock You

2023-11-17 07:20:00 ET

Summary

- Asset management is a cash-minting machine of an industry with infinite growth capabilities. But, there's a catch.

- BlackRock and Vanguard have destroyed the traditional mutual fund industry, and now there is only one place left with fat fees.

- Alternative asset management is a $20 trillion industry, growing at 35% and charging about 5X higher fees than BlackRock or Vanguard.

- Management teams consistently earn $60 to $600 million per year and are worth it, generating Buffett-like 20% returns for investors over the last decade.

- Blackstone Inc. is the king of alternative assets with $1 trillion in assets, and Apollo Global Management, Inc. is #3 and the king of private credit. One of these is currently a good buy and capable of 4X the short-term returns of the other.

Imagine the perfect business. A business with infinite scalability, mints money, and is guaranteed to increase in value over the long term.

Asset management is such a business. Think about it. Investing money for people and getting paid a percentage of the assets as fees is a glorious business.

A business model that will never die unless the world ends, which Goldman Sachs thinks is usually a 2.5% risk.

- The current risk of nuclear war is 10% due to the proxy war in Ukraine.

But there is a problem for asset managers: index funds!

{kind=link}

About $10 trillion in assets are now invested in exchange-traded funds, or ETFs, worldwide. That's 15% of the $60 trillion asset management industry, which manages part of the $454 trillion that Credit Suisse thinks existed in global wealth at the end of 2022.

Wait a second? If $454 trillion in wealth exists and only $60 trillion is run by managers, then doesn't that mean just 13% market penetration?

87% of the potential addressable market is untapped, meaning asset management has a long growth runway.

And the addressable market, all the wealth in the world, will keep growing exponentially for as long as human innovation exists.

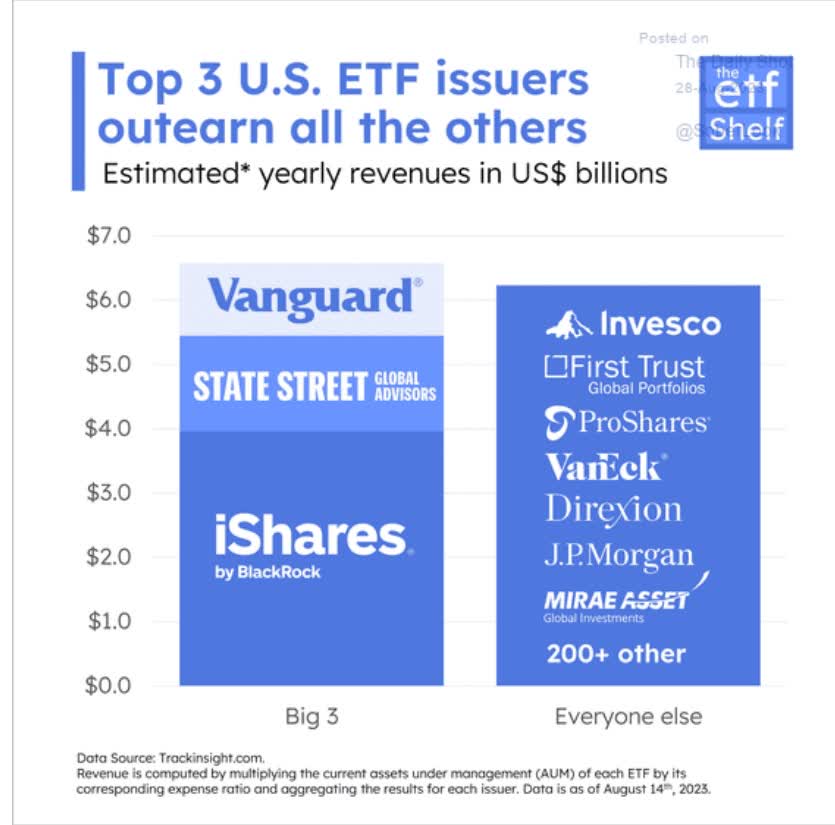

The only tricky thing is fees. Vanguard and BlackRock (BLK) have led a race to the bottom on fees.

So much so that they now charge 0.03% expense ratios for their S&P 500 funds, and BlackRock's corporate expense ratio (for all its funds) is 0.15%.

The days of 2% and 20% are gone for mutual funds...but not necessarily alternative asset managers.

Average Expense Ratio For Alternative Asset Managers (Including Performance Fees)

| Alternative Asset Manager |

| Ticker |

| Fee Bearing Assets Under Management ($ Billions) |

| Annual Fees $ Billions |

| Average Expense Ratio |

| Blackstone |

| ( BX ) |

| 749.6 |

| 6.822 |

| 0.91% |

| Brookfield Asset Management |

| BAM |

| 711.3 |

| 5.954 |

| 0.84% |

| Apollo Global Management |

| ( APO ) |

| 488.5 |

| 2.489 |

| 0.51% |

| Kohlberg Kravis Roberts & Co |

| KKR |

| 443.1 |

| 3.02 |

| 0.68% |

| Ares Capital |

| ARES |

| 259.9 |

| 2.682 |

| 1.03% |

| Total |

| 2652.4 |

| 20.967 |

| 0.79% |

(Source: FactSet Research Terminal.)

Some analysts estimate that the $20 trillion alternative asset management industry will grow at 35% annually for the next decade.

So, let's summarize:

- $454 trillion in global net worth

- $60 trillion asset management industry

- $20 trillion (33%) is alternative assets

- the five largest alternative asset managers command about 10% market share

- and are averaging 0.8% fees compared to BlackRock's 0.15%

- mutual funds average 0.47%, and that's why ETFs are slowly replacing them.

Massive growth potential in an infinitely scalable market, with fees that are 5X higher than what BlackRock, king of asset managers, gets away with.

Can you see why I love this industry?

Can you see why I plan to invest $2.6 million of my retirement funds into Brookfield Asset Management?

Do you see why I'm such a fan of Blackstone Inc., the king (so far) of alternative asset managers?

But what about the others? Recently, I've gotten many requests from members in our chat room about comparing and contrasting articles between Blackstone and Brookfield and their smaller but potentially faster-growing peers.

The most requested comparison is Blackstone vs. Apollo Global Management, Inc., so let's look at how the 3rd biggest alt asset manager in the world stacks up to the industry's heavyweight.

Business Model: Winner Blackstone

Blackstone is tough to beat as the king of asset managers. It has $1 trillion in assets under management, or AUM, $731 billion of which is fee-bearing.

Blackstone was founded in 1985 and operates in all 4 major parts of alternative assets.

- real estate: 44% of base-management fees

- private equity: 27%

- credit & insurance: 21%

- hedge funds: 8%.

Blackstone has almost 5,000 employees, including some of the industry's best executives, consultants, and advisors.

Just 5% of money managers can beat their benchmarks, but those skills can be bought for the right price.

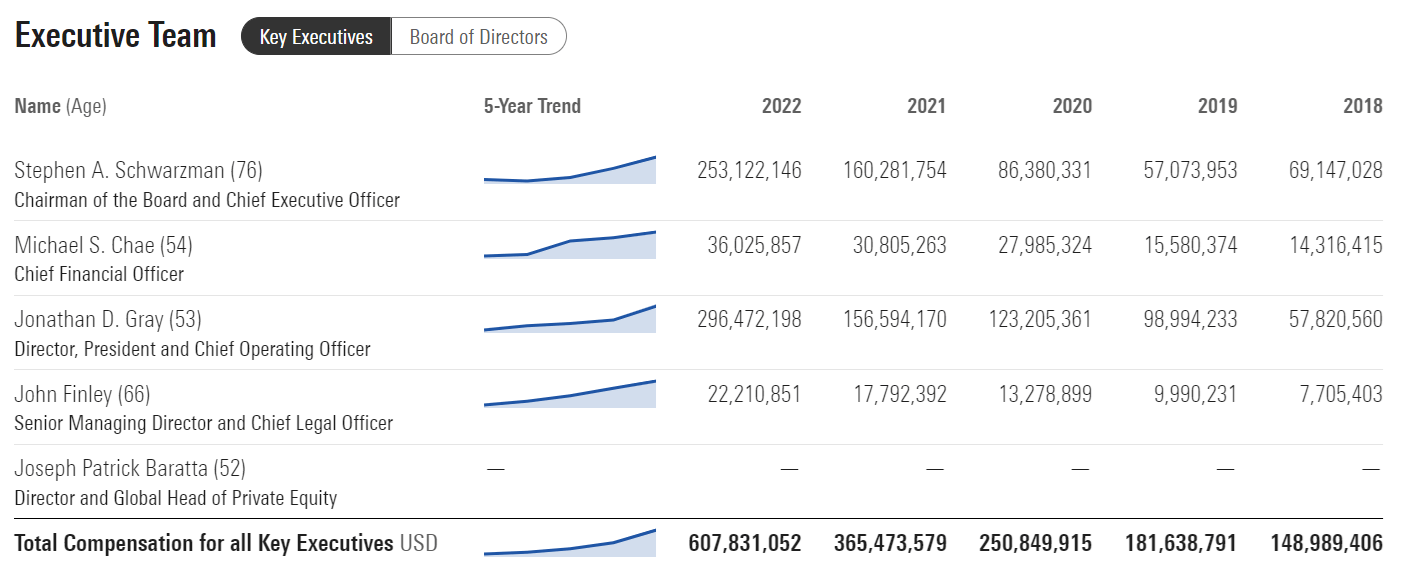

In the case of Blackstone, here is how much it pays its executives.

{kind=link}

Blackstone's industry-leading executives earned $608 million last year, including its founder, Stephen Schwarzman (worth $31.3 billion), earning over a quarter of a billion. And he wasn't even the highest-paid executive; that would be the COO, who made almost $300 million.

- almost $1 million per day

Morningstar

Most likely, the vast majority of that $241 million in "other comp" is restricted stock units sheltered from taxes.

{kind=link}

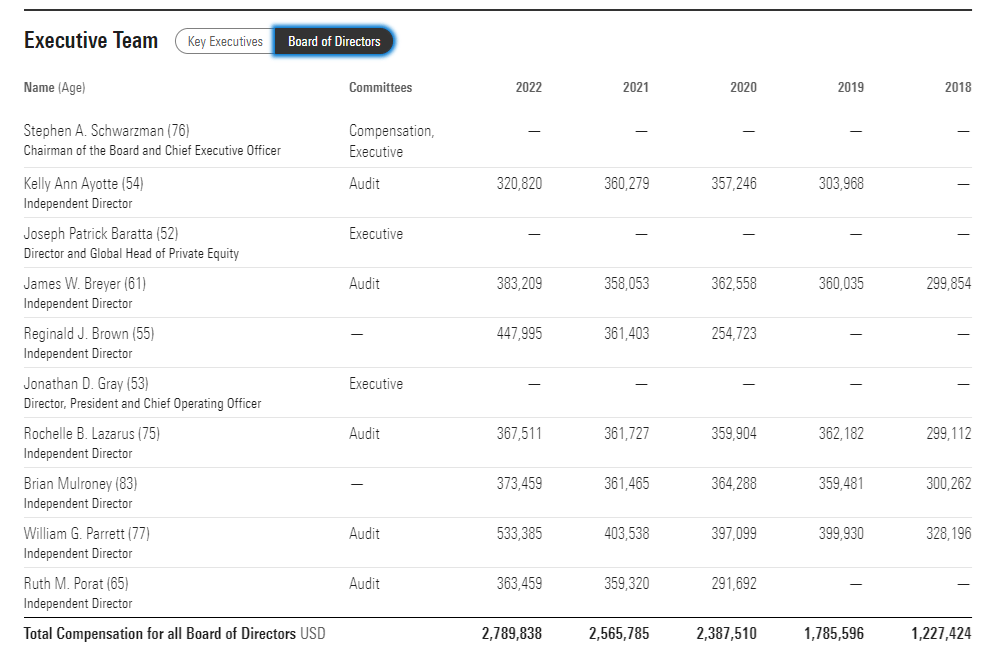

The average board member at Blackstone makes $280,000 per year, and the typical board will meet six times per year, and the average board meeting lasts 3 hours.

- $15,600 per hour working on average, 18 hours per year.

The compensation for BX's board has been growing by 24% since 2018, and the comp for the executives has been growing their pay 42% per year.

Why are Blackstone's executives paid so much? Before 2019, it was a partnership 45% owned by the founders, with Schwarzman owning about 19% of the company.

Blackstone has done a great job in navigating the complex world of private markets since the Great Recession, and there is one big upside of having executives that own 45% of the stock...dividends!

In the last decade, Blackstone has repurchased $3.6 billion in stock and paid $31 billion in dividends. The reason is precisely because the founders and partners want to get paid.

- in the last year, Blackstone paid out $2.6 billion in dividends

- $1.2 billion went to the founders and partners

- about $500 million to Schwarzman

- whose total compensation, including dividends, was almost $750 million.

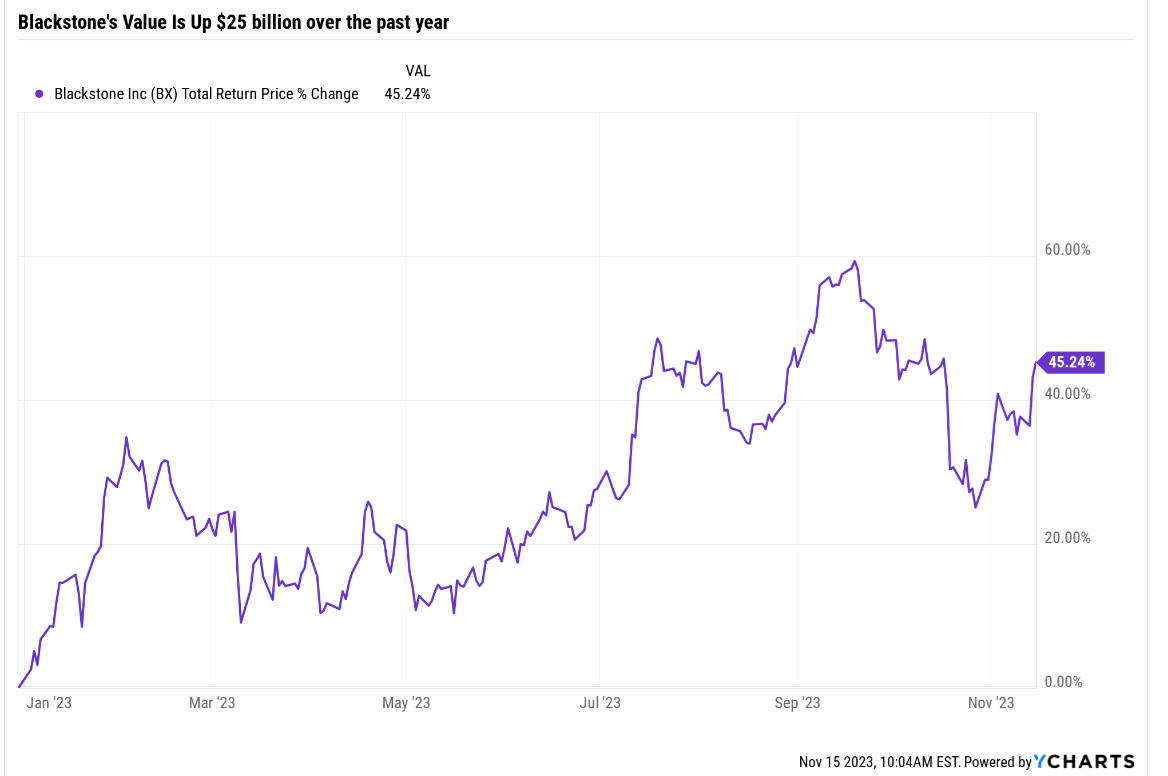

{kind=link}

The founders and executives received about $1.8 billion in total compensation and dividends to increase the company's value by $25 billion.

- They were paid 7% of the value they created (on paper, at least).

For context, Apple (AAPL) CEO Tim Cook earned $99 million in 2022 and got $800,000 in dividends from his 837,000 shares.

Apple and Blackstone are both up 45% in the last year. Apple's value is up $900 billion, and Tim Cook was paid 1/9th of 1%.

The Apple executive team made $208 million in 2022 and received $17 million in dividends for a total comp of $225 million, or 0.025% of the company's value increase.

So Blackstone's executives made 288X more than Apple's executives, adjusting for their relative value increases.

Can you see why alternative asset management is so attractive? Not only is it a money-minting machine, but the reward for success is so great it makes Apple's executive comp look like paupers in comparison.

Of course, that's because Blackstone is the world leader in one of the most lucrative fields on earth.

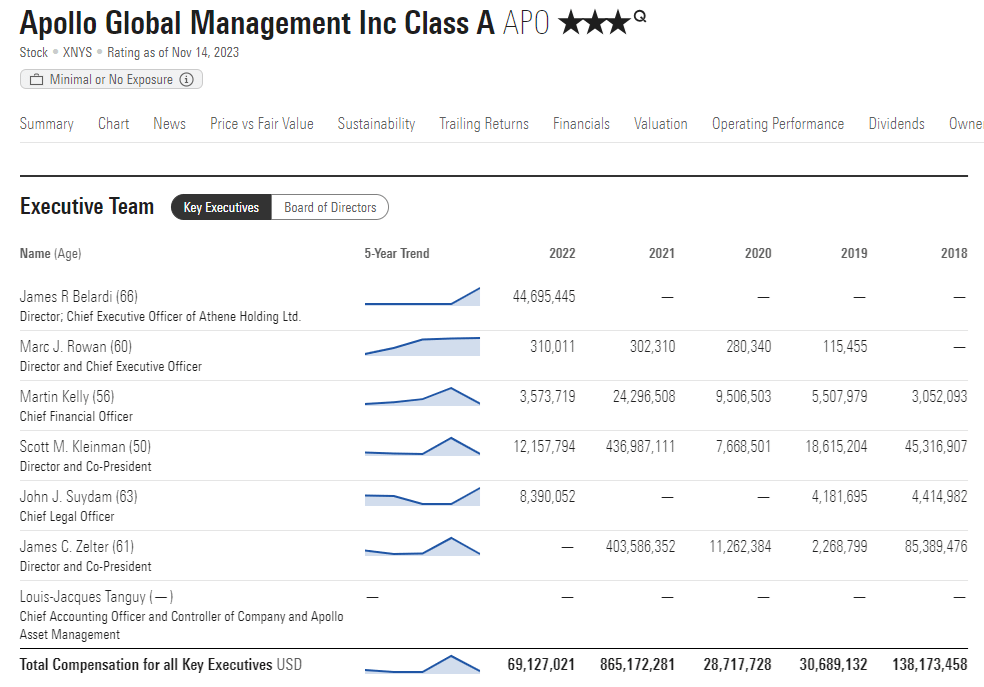

How about Apollo? The #3 player?

{kind=link}

That's the benefit that BX has in being #1. It can afford to pay its executives almost 10X more than Apollo, the 3rd largest alt manager on earth.

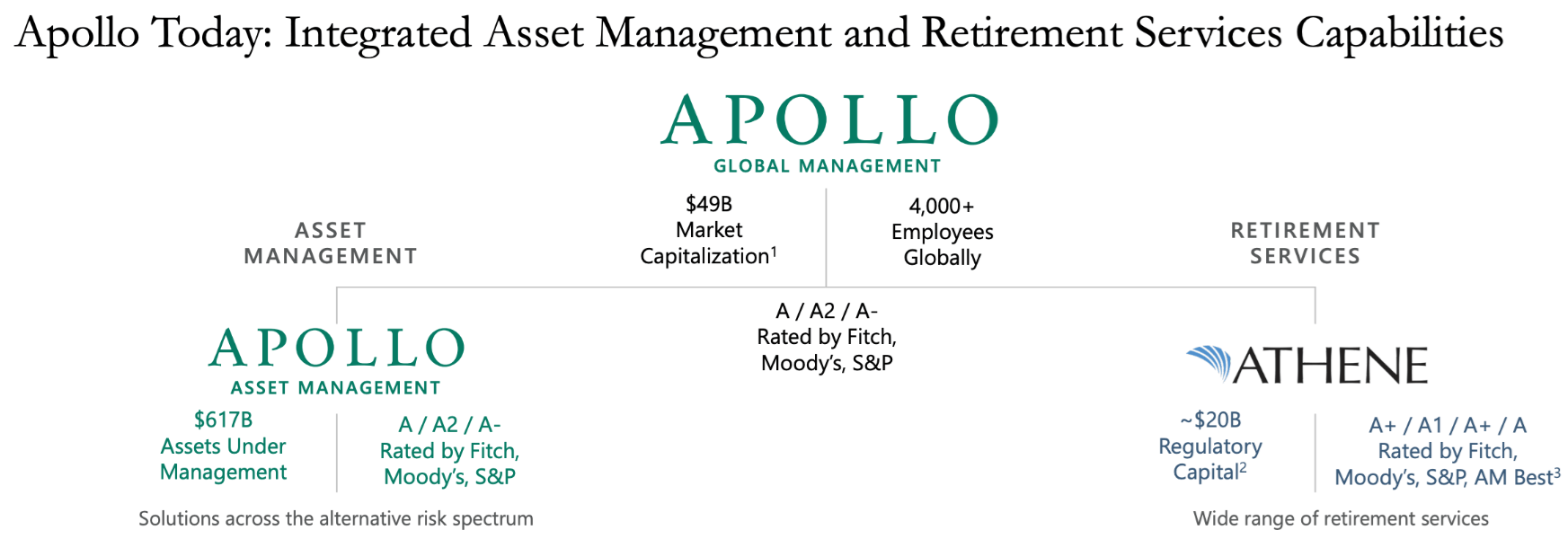

{kind=link}

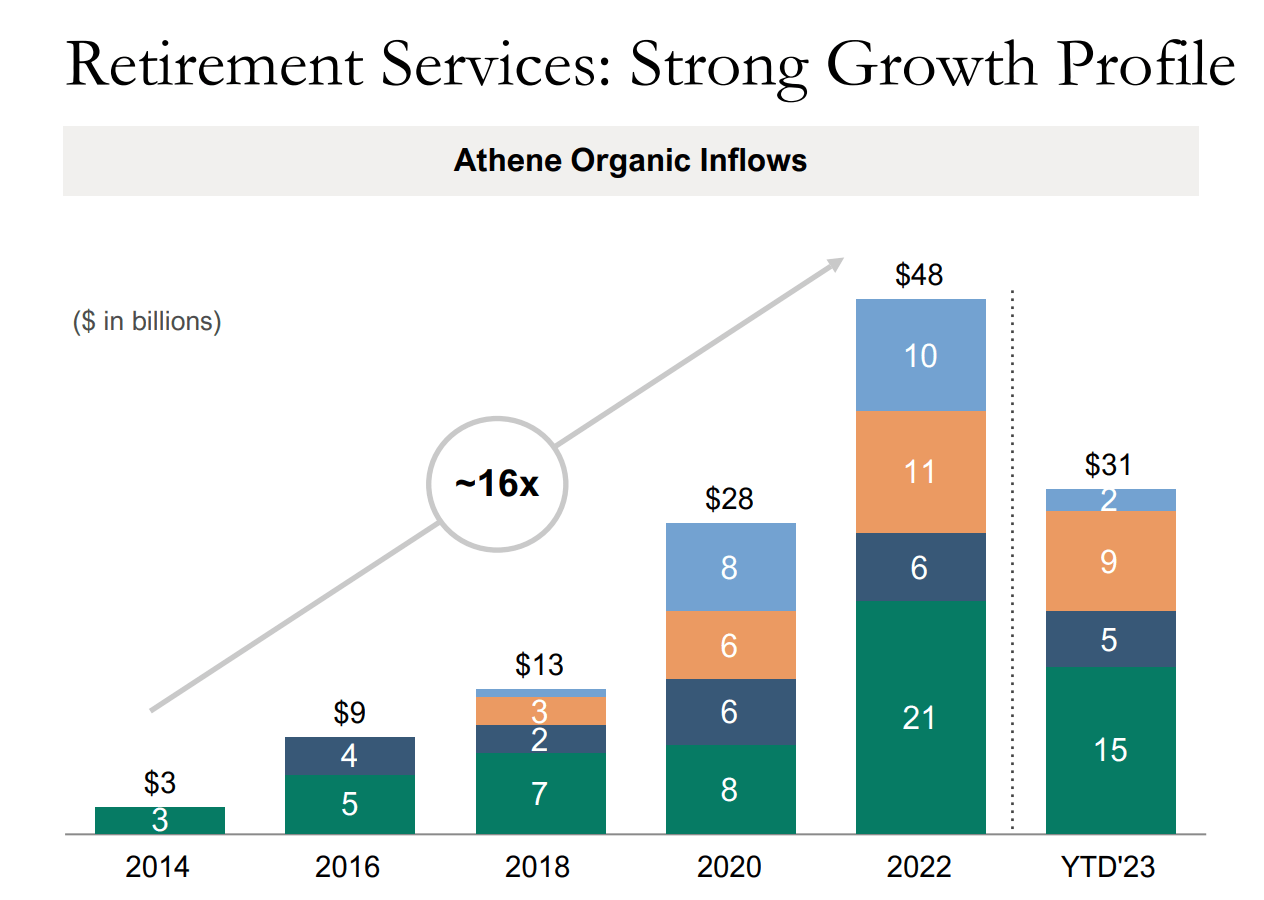

Apollo has an asset-light business just like Blackstone, but also has a retirement service business called Athene.

- Asset light = company doesn't invest its own money into physical assets but manages assets owned by others

- It is fee focused and has higher leverage and, thus, higher returns on equity.

The big difference between Blackstone and Apollo is that 80% of Apollo's fee-bearing assets under management are in private credit.

Blackstone (and Brookfield) are pretty diversified and roughly equally invested across its various businesses.

Private credit is extremely flexible and scalable at the right times, such as during the Pandemic credit boom.

The downside is that the fees aren't as high as infrastructure managers like BX and BAM can charge.

- APO average expense ratio: 0.51%

- BX: 0.91%

- BAM: 0.84%.

Given that Blackstone has a larger potential growth market, by having its finger in every part of the industry pie, in every industry on earth, I have to give this round to BX.

Profitability: Winner Blackstone

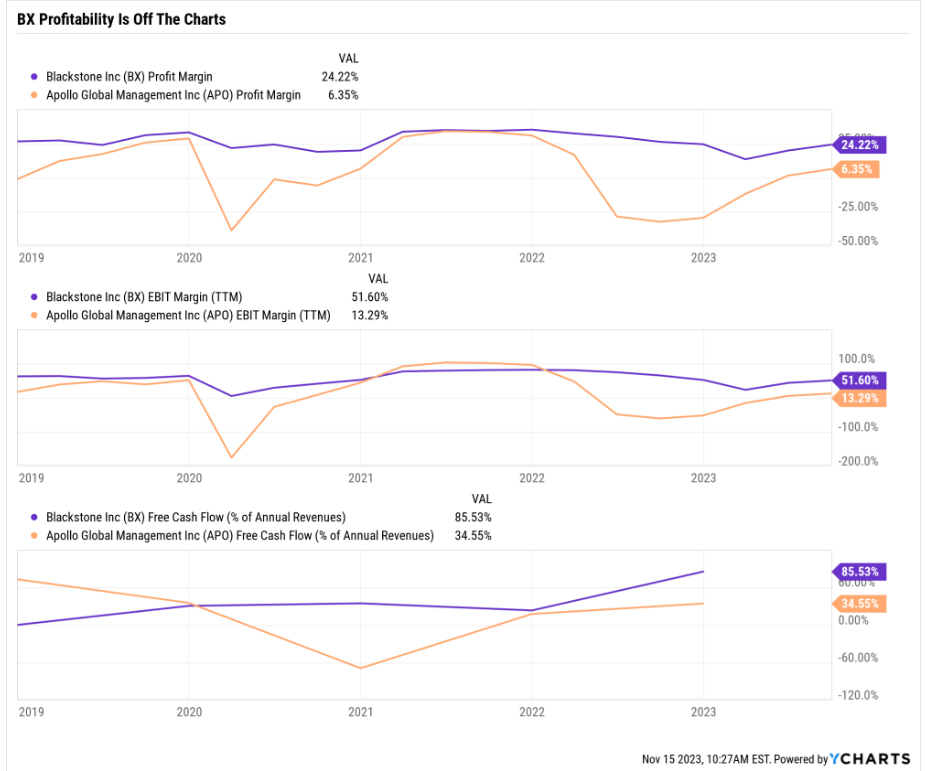

We just saw how BX is charging its clients almost twice the fees of Apollo, and when you combine it with twice the scale, here's what falls to the bottom line.

{kind=link}

35% free cash flow margins for any business are in the top 10% of all companies. And that's what APO is delivering. But Blackstone is currently enjoying 85% free cash flow margins.

That means even after paying its executives insane amounts of compensation and running the business, including paying taxes and investing in future growth, 85% of every dollar is dropping straight to the bottom line.

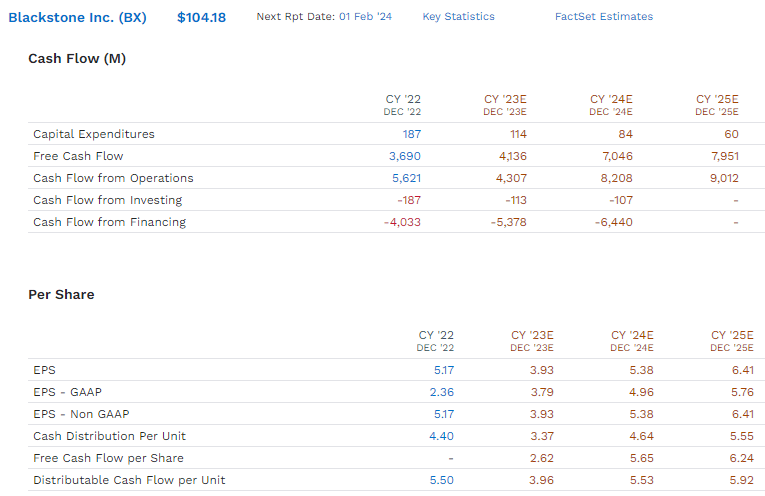

{kind=link}

Blackstone's free cash flow is exploding and is expected to almost triple in three years.

While free cash flow margins can be highly volatile, here is what analysts expect from the global king of alt management's free cash flow margin.

- 2022: 29%

- 2023: 41%

- 2024: 57%

- 2025: 50%.

Analysts expect BX to be able to maintain approximately 50% free cash flow margins in the coming years.

Those are mind-blowing numbers.

BX pays out 85% of that cash flow as dividends since 45% of shares are owned by the partners and founders who want to get paid cash.

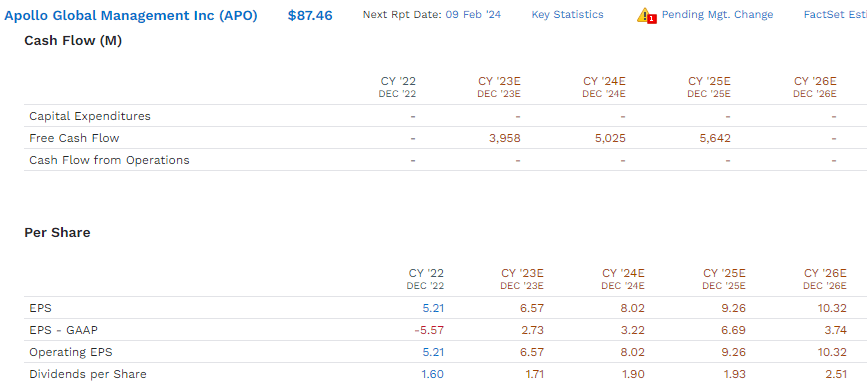

How about Apollo?

{kind=link}

APO's free cash flow is an impressive $4 billion this year, growing 18% annually through 2025.

But BX's free cash flow is growing at 39%, more than twice as fast as Apollo's.

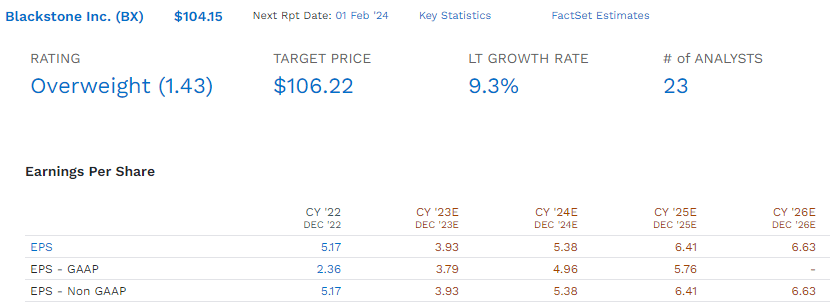

Growth Rates: Winner Apollo

OK, Blackstone blows away Apollo for fees, and its profitability is just outrageous.

Through 2025, it's expected to grow twice as fast as Apollo. But what about the long term? What about 2026 and beyond?

{kind=link}

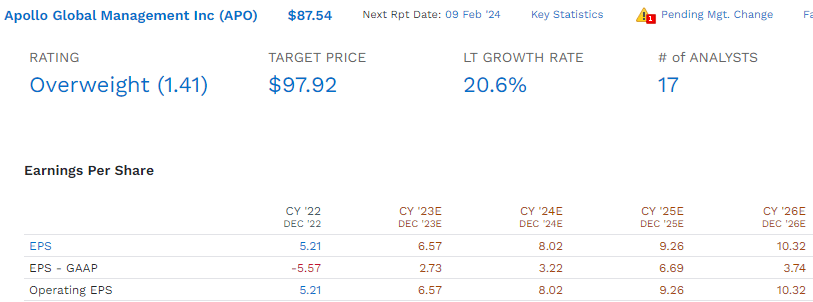

Apollo is expected to grow at a Buffett-like 21% per year for the foreseeable future.

That includes EPS growth of 18.6% through 2026.

Darn impressive, and not likely something BX can keep up with.

{kind=link}

So does that mean APO is the hands-down better investment?

Total Return Potential: Winner Apollo

Total return is yield + growth + change in valuation.

{kind=link}

So, let's take a look at the long-term consensus return potential for BX and APO.

How can we estimate the yield for alternative asset managers with variable payout policies and volatile dividends?

How about the 5-year average yield? We'll call that a proxy for the typical yield in both companies.

| Investment Strategy |

| Yield |

| LT Consensus Growth |

| LT Consensus Total Return Potential |

| Apollo Global Management |

| 3.4% |

| 20.60% |

| 24.0% |

| Brookfield Asset Management |

| 4% |

| 12.70% |

| 16.6% |

| Schwab US Dividend Equity ETF |

| 3.9% |

| 9.70% |

| 13.6% |

| Blackstone |

| 3.7% |

| 9.30% |

| 13.0% |

| Nasdaq |

| 0.8% |

| 11.2% |

| 12.0% |

| REITs |

| 4.6% |

| 7.0% |

| 11.6% |

| Dividend Aristocrats |

| 2.3% |

| 8.5% |

| 10.8% |

| S&P 500 |

| 1.7% |

| 8.5% |

| 10.2% |

| 60/40 Retirement Portfolio |

| 2.1% |

| 5.1% |

| 7.2% |

(Source: FAST Graphs, FactSet.)

Both Blackstone and Apollo appear to be amazing long-term opportunities, but Apollo's smaller size and the Athene annuity business give it an edge and make it worth considering for income growth investors.

{kind=link}

Apollo has achieved incredible growth thanks to annuities invested more aggressively than most annuity providers.

In a low-rate world, its expertise in private credit allowed it to earn superior returns and, thus, very strong earnings growth from this business.

Will a world of higher rates destroy that edge? That is not likely, given that Apollo has been around since 1990.

But Athene was founded in 2009 out of the financial crisis carnage. So, while management at Athene and Apollo knows how to navigate a regular rate world just fine, the actual business model hasn't been tested.

Financial Strength: Winner Apollo

Let's use S&P credit ratings as our proxy for fundamental risk.

S&P

Blackstone is rated A+ stable, meaning a 0.6% fundamental risk of your investment going to zero within three decades.

Apollo has an A stable credit rating and a 0.66% fundamental risk.

Apollo has $62 billion in liquidity vs $7.2 billion in liquidity for Blackstone.

Why is APO's liquidity so much larger? Athene is an annuity company, so it is like APO and has its own float-generating cash printing machine.

Valuation: Winner Apollo

{kind=link}

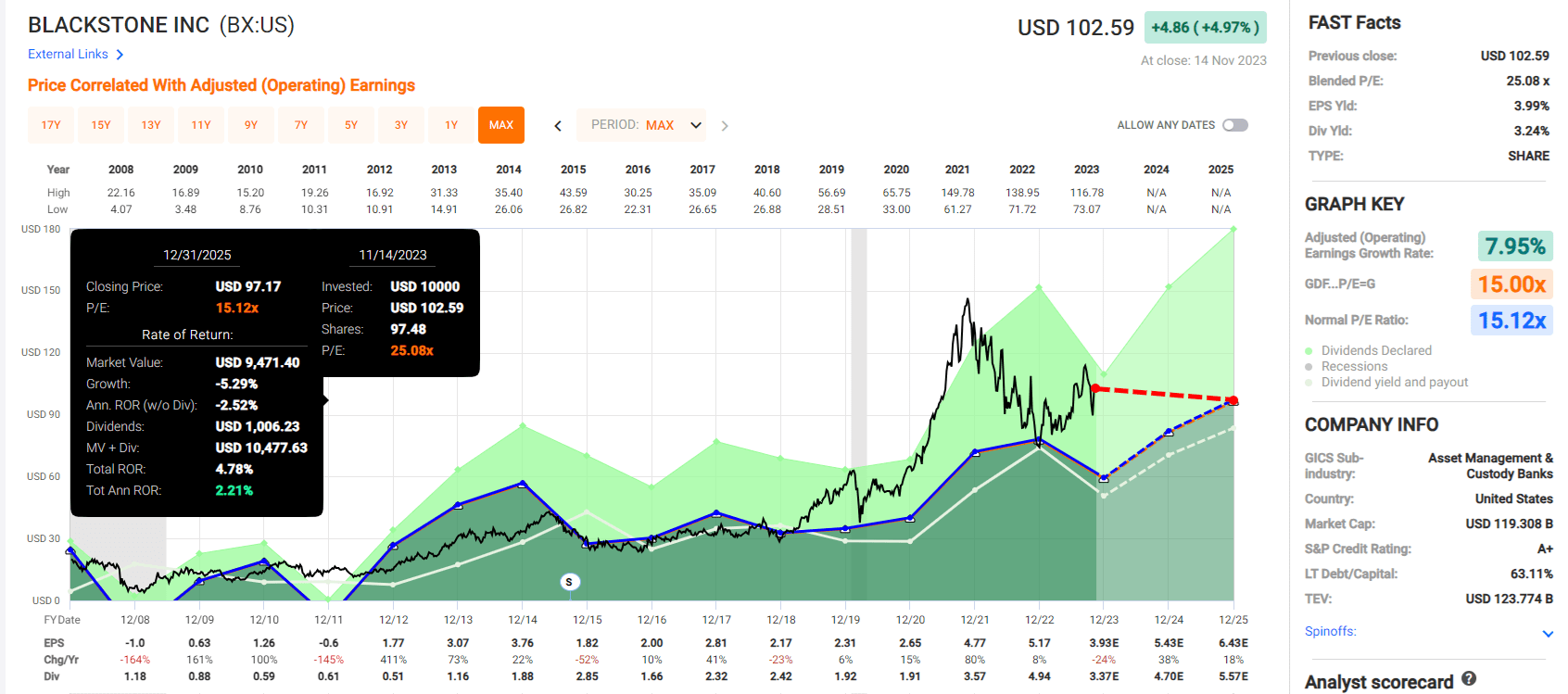

BX is growing fast, but 20% is historically overvalued.

Remember that it flew off into a bubble in the Pandemic mania.

BX was trading at 33X earnings in the Pandemic stimulus mania, and it's still trading around 25X, meaning that it's pricing in all the expected growth of the next two years.

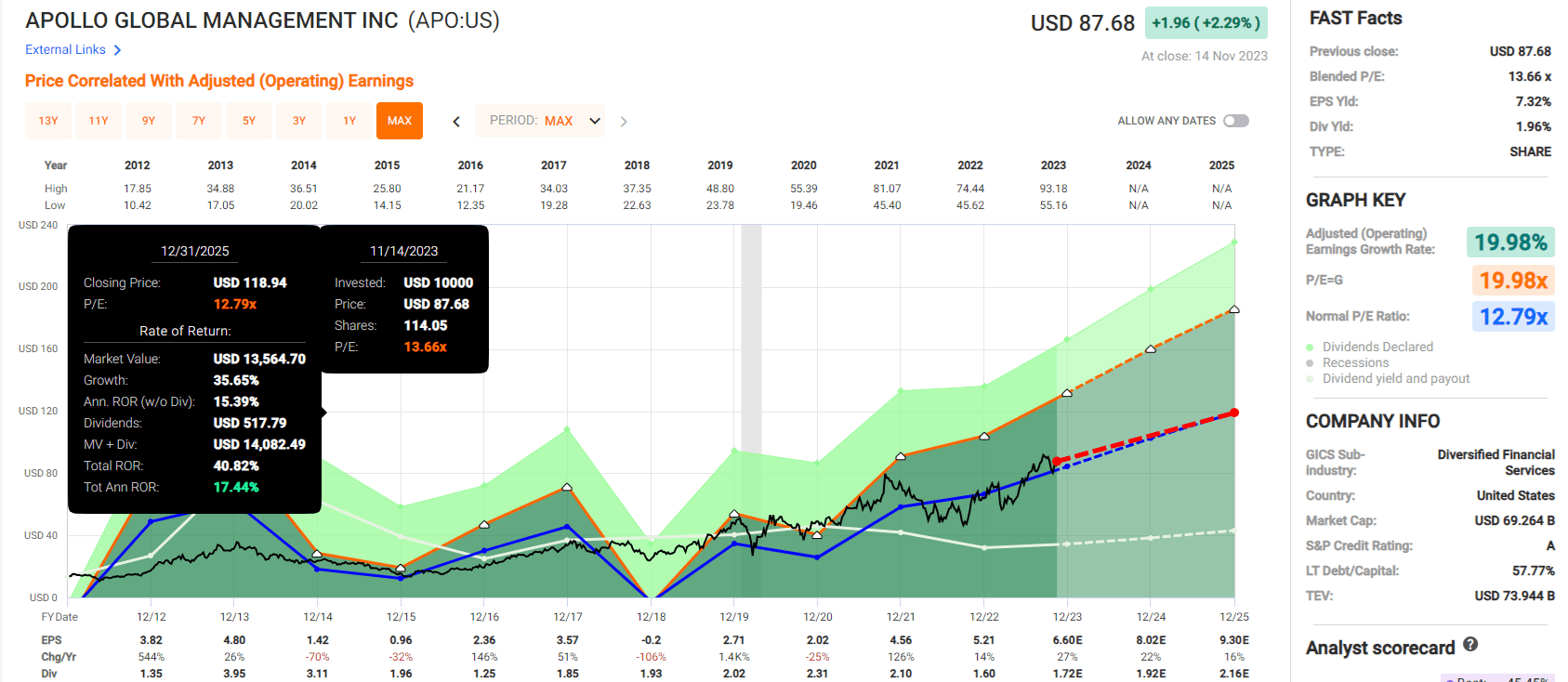

{kind=link}

Apollo is trading at fair value and growing like a weed, offering about 17% annual return potential through 2025, twice that of the market and 4X better than Blackstone.

Income Growth History: Winner Blackstone

Here's why it's worth owning alternative asset managers if you're an income investor. Yes, the dividends can be volatile in any given year...but they grow over time at a rate that makes most aristocrats blush with envy.

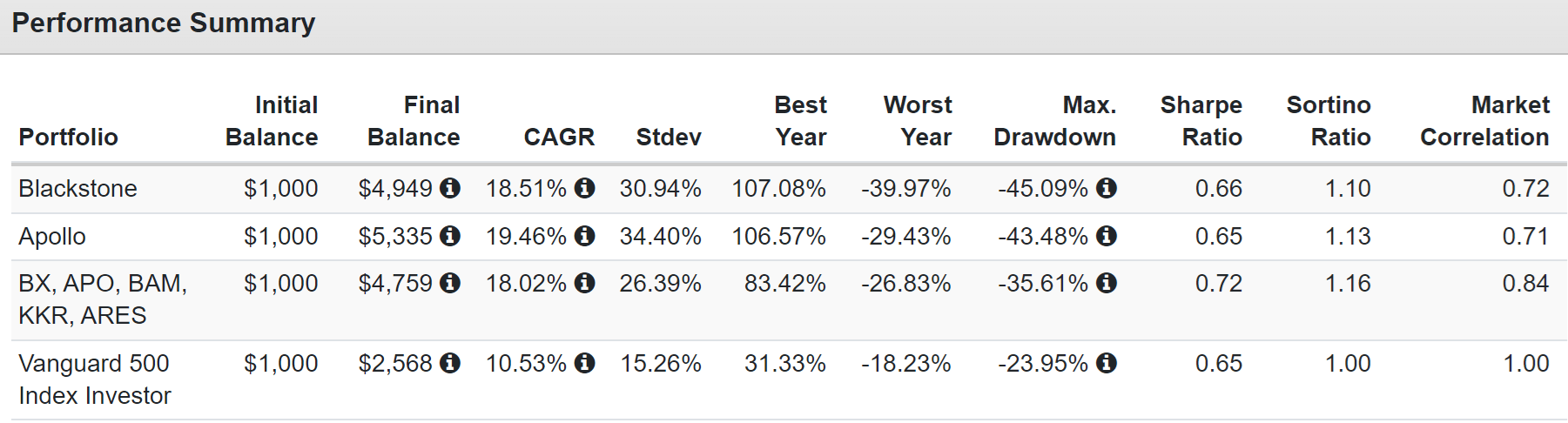

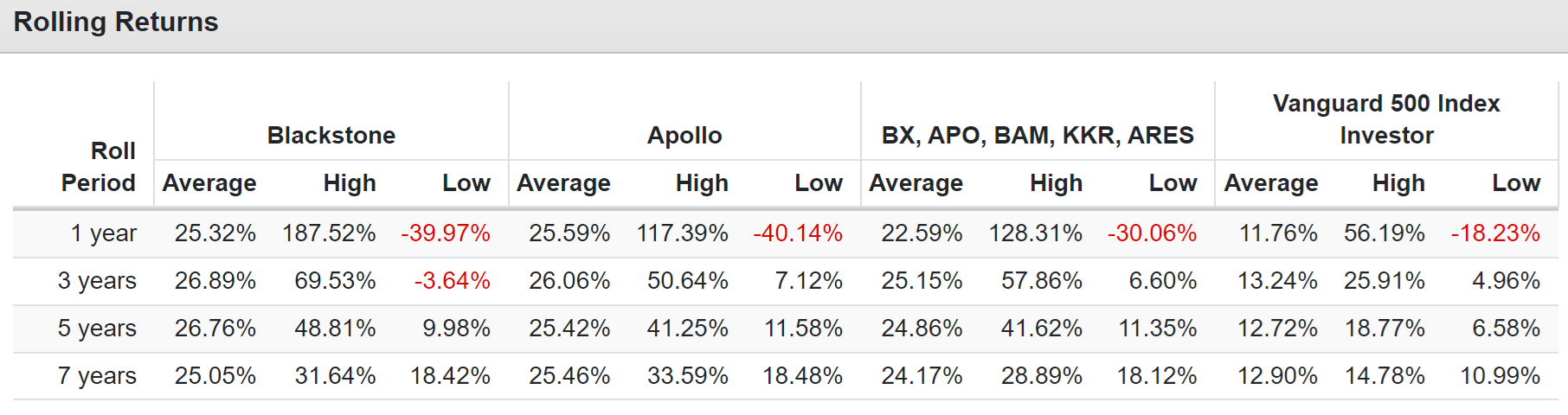

Total Returns Since 2014

{kind=link}

The entire alternative asset industry has been booming for the last decade, and investors in the Big 5, BX, or APO got Buffett-like returns that smoked the S&P and even the Nasdaq.

{kind=link}

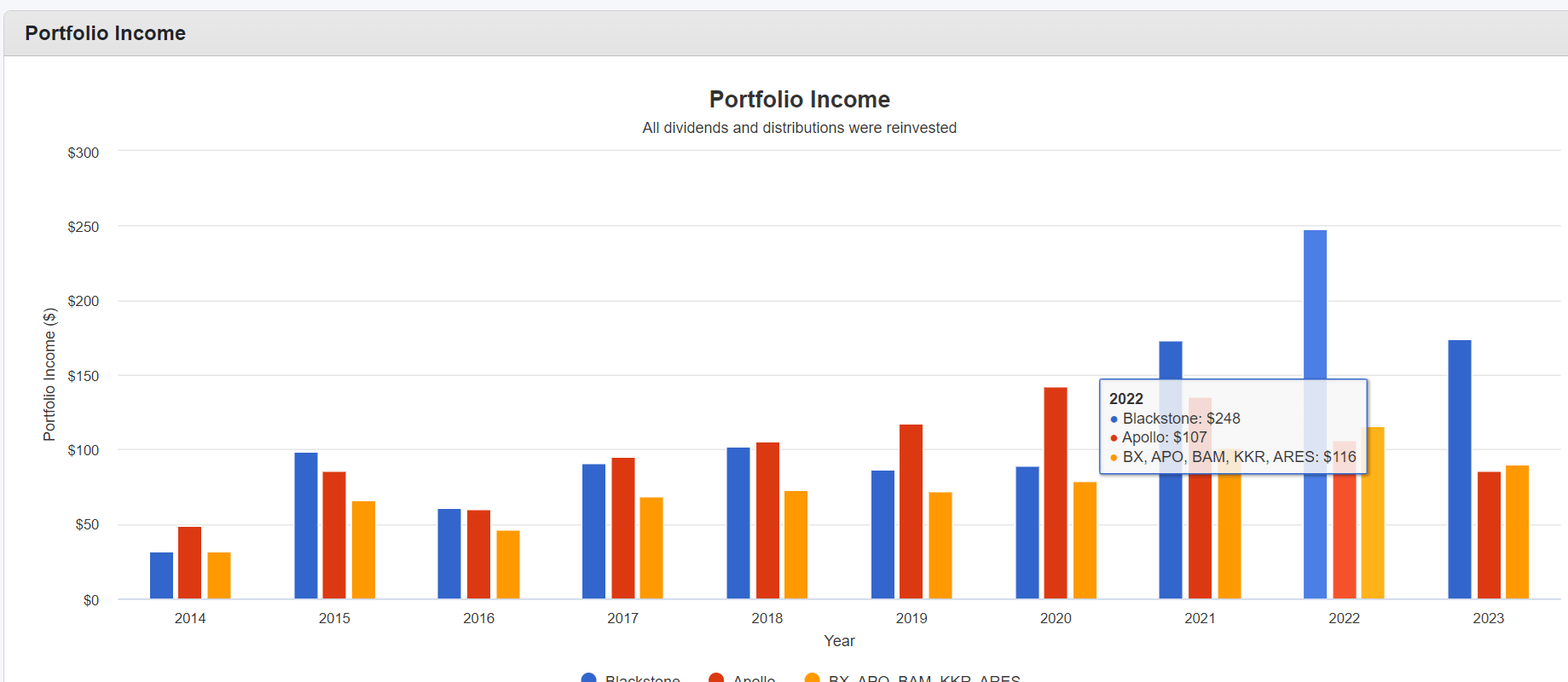

And here's the result of all that growth in terms of dividends.

{kind=link}

In the last eight years:

- BX 14% annual income growth

- APO: 3% annual income growth

- Big 5 Alt Managers 9% annual income growth.

Apollo hasn't done well in terms of generating consistent dividend growth.

Bottom Line: Apollo Is The Winner...But

So, in a final score of 4 to 3, Apollo edges out Blackstone for several reasons.

First, APO is a faster-growing A-rated master of private credit markets. Its Athene annuity business has been a massive profit engine, and analysts think it will do even better in a higher-rate world.

Apollo's valuation is also far better than BX's, giving it 4X better return potential in the next two years.

However, high-yield investors seeking stable income will likely find BX a far nicer choice.

It historically has offered much better dividend stability, courtesy of being 45% owned by founders who want to get paid steady income.

With 13% long-term return potential from Blackstone Inc., slightly more than the Nasdaq, and a good history of income growth (despite its variable nature), I would not hesitate to tell high-yield investors who own BX to stick with it.

When you ride with Blackstone, you're riding with Stephen Swartzman, the legendary king of alternative asset management.

I own a lot of stock, and I invest in all of our funds, so the firm is my family office," Schwarzman, 76, said at an industry conference this year...

His heir apparent as CEO, Blackstone President Jon Gray, collected $479.2 million in 2022. That included $182.7 million from dividends tied to a roughly 3% stake in the firm. That is an increase from the prior year. " - Fortune.

The two men who run Blackstone own 23% of the company and are eating their own cooking.

What happens when Jon Gray, age 53, finally retires in 30 years or so?

Let me put it this way: Blackstone has a deep bench, and no other asset manager on Wall Street pays better.

So whoever replaces Gray will be a legend of Wall Street, and likely, BX will continue to generate impressive income growth for investors.

But Apollo is so impressive that I'll add them to the Dividend Kings Master List.

I like the Athene annuity business, and it's hard not to like their expertise in private credit.

For further details see:

Blackstone Vs. Apollo: The Winner Might Shock You