BLDE - Blade Air Mobility: A Strong Business With Solid Potential

2023-09-01 14:34:33 ET

Summary

- Blade Air Mobility, is a valuable investment opportunity in the eVTOL and transport sector, offering near term potential for positive net income and exposure to revolutionary changes in aerial mobility.

- The company's revenue growth is impressive, driven by the MediMobility Organ Transport business and the acquisition of Blade Europe.

- Blade has a strong financial standing with low debt and a significant cash position, positioning them well for near-term profitability and future growth in the eVTOL market.

In our assessment, Blade Air Mobility, Inc. ( BLDE ) stands on firm ground, representing a valuable investment opportunity in the dynamic eVTOL and transport sector. At its present valuation, one isn't just investing in a business with a promising trajectory towards positive net income but is also getting a front-row seat to the revolutionary changes eVTOL promises to bring. We view Blade as an under-the-radar powerhouse in the aerial mobility space, making it an essential addition to any forward-thinking transport portfolio. Our stance is a resounding 'Strong Buy' at the current market rate. Given the appealingly low Implied Volatility ((IV)), we're not only inclined to buy shares but are also strategizing a synthetic long position utilizing options. With the potential for a substantial return on investment, our strategy leans towards reinvesting gains into accumulating more shares rather than merely lowering our cost basis. In the following article we will walk through why we believe this a must buy.

Overview

Blade Air Mobility, Inc., commonly referred to as "Blade" offers a technology-driven global air mobility solution. This platform presents consumers with a time-saving and cost-efficient alternative to traditional ground transport, especially in traffic-heavy routes. In the U.S. and beyond, Blade's Passenger division coordinates both charter and individual-seat flights using a variety of aircraft, including helicopters, jets, turboprops, and amphibious seaplanes.

Meanwhile, Blade's Medical division specializes in facilitating the aerial transportation of human organs within the U.S. This service provides comprehensive logistics support for transplant centers and organ procurement entities, leveraging helicopters, jets, turboprops, and land vehicles. Operating with an asset-light strategy, Blade collaborates with a network of partnered aircraft operators, ensuring they neither own nor directly operate any aircraft.

Impressive Revenue Growth but Challenges Ahead

{kind=link}

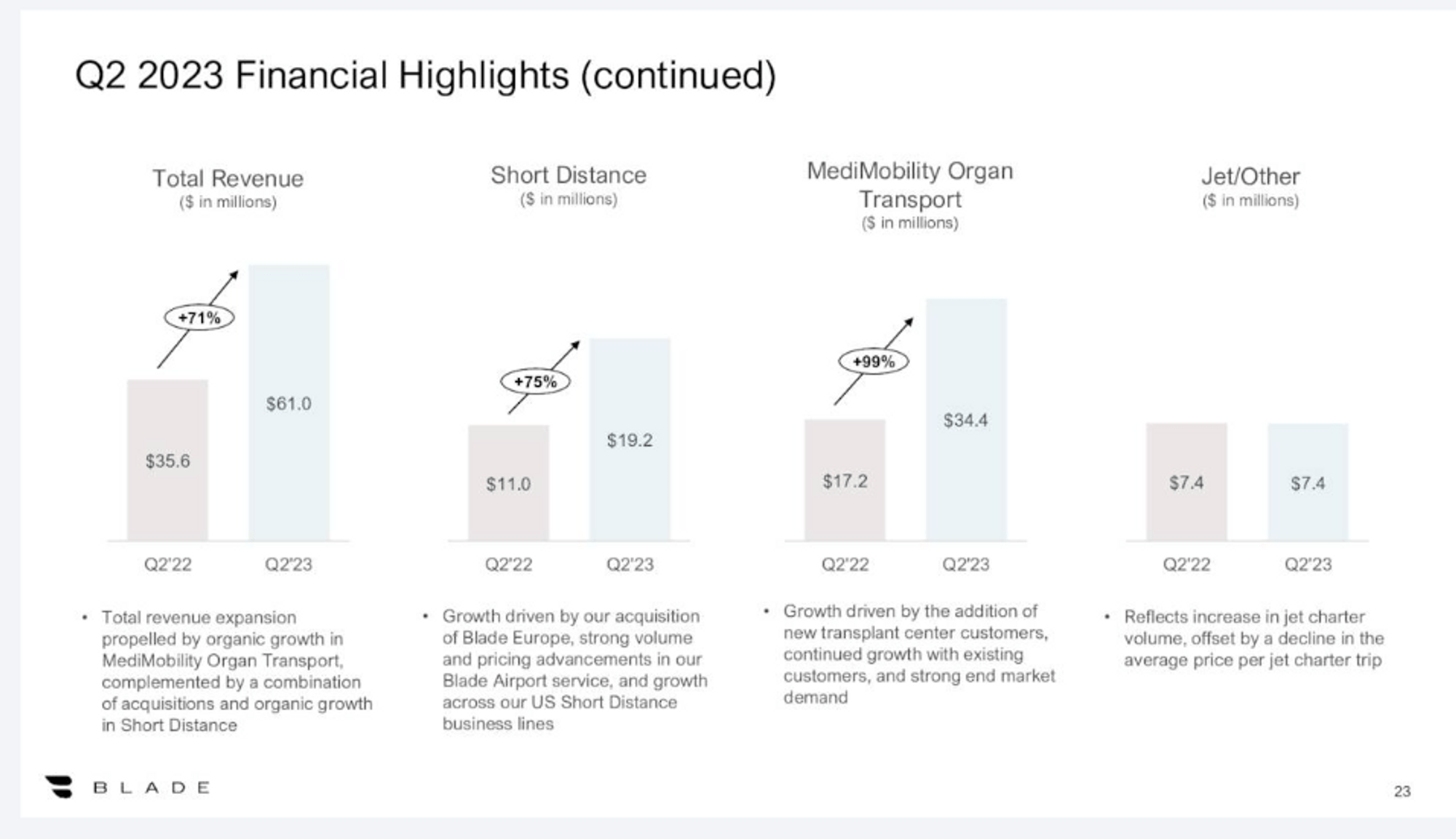

Blade Air Mobility's revenue growth is undeniably impressive. A 71% surge, bringing revenue to $61 million from $35.6 million the previous year, is no small feat. The primary drivers of this growth were the MediMobility Organ Transport business, which alone saw a staggering 99% organic growth, contributing $17.2 million of the $25.4 million of growth for revenue. What's important to highlight is that all the MediMobility's Revenue growth came organically while the Short Distance segment growth came from the acquisition of Blade Europe.

{kind=link}

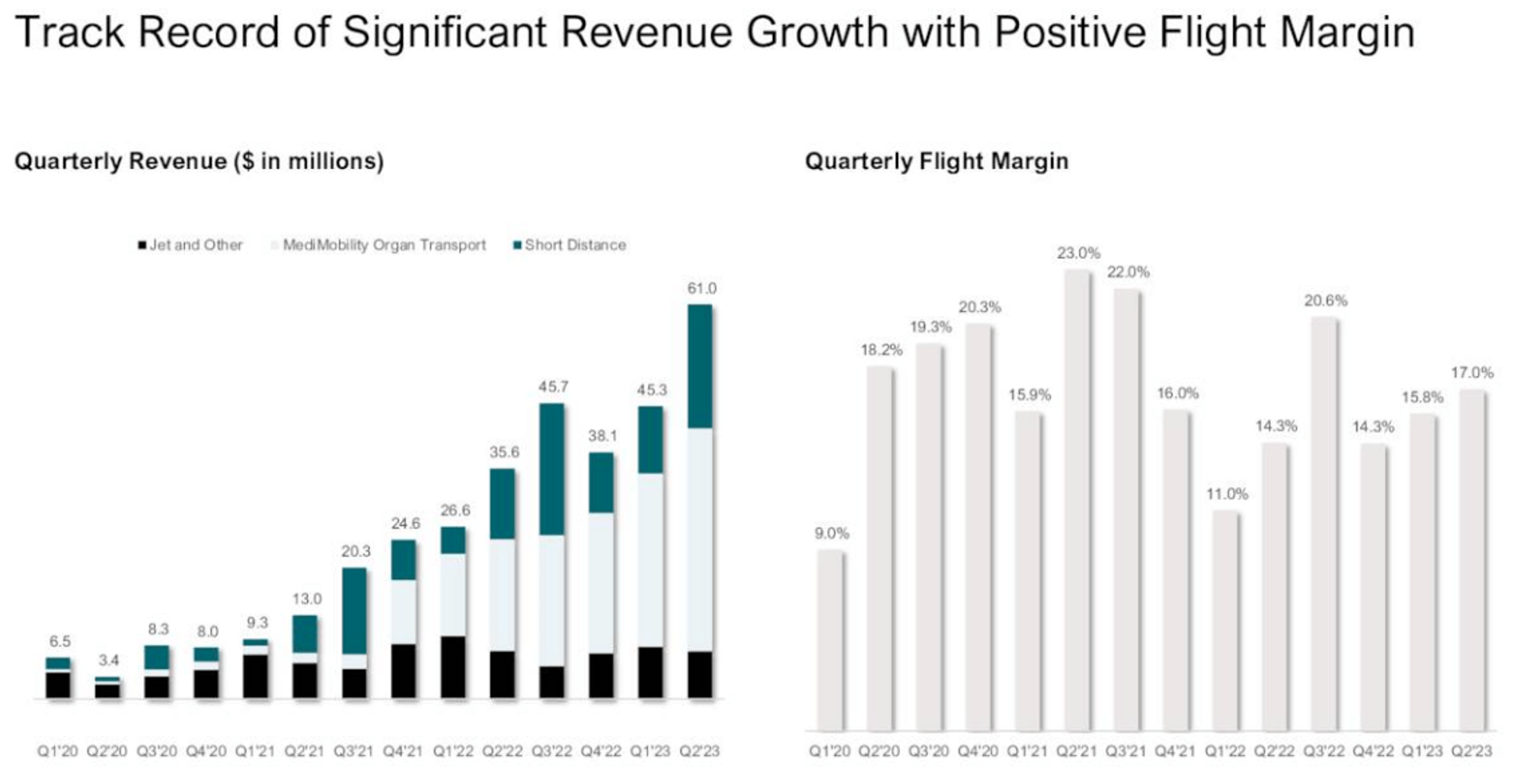

The percentage of Sales attributable to Short Distance, Jet & Other continue to decrease. Margin is climbing from a low in Q4 '22 but still has not reached their recent flight margin of 20.6% seen in Q3 '22. We believe we will continue to see this trend with more and more sales being attributed to MediMobility growth and less so for the other segments. The only factor that we believe will reverse this trend will potentially come from more affordable and profitable options from eVTOLs like those offered by Archer Aviation ( ACHR ) and other eVTOL manufacturers.

Blade's Sales Growth and Operational Control

{kind=link}

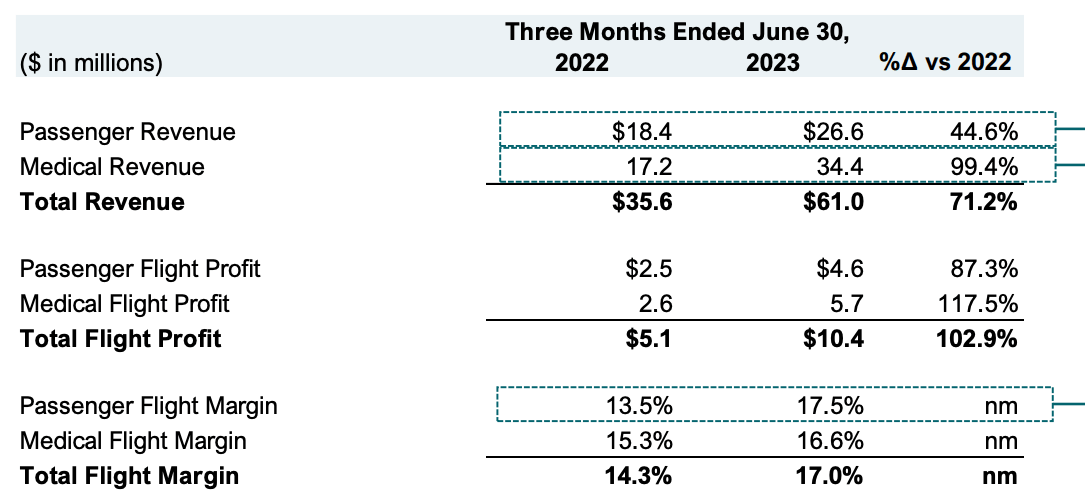

A standout feature of the company is its robust financial standing. In Q2 2023, the flight profit soared by 103%, reaching $10.4 million, up from $5.1 million in the same quarter of the previous year. Furthermore, the flight margin grew from 14.3% in Q2 2022 to 17% in Q2 2023. While the adjusted EBITDA for Q2 2023 was a negative $4.4 million, it represents a notable improvement from the negative $6.1 million reported in Q2 2022.

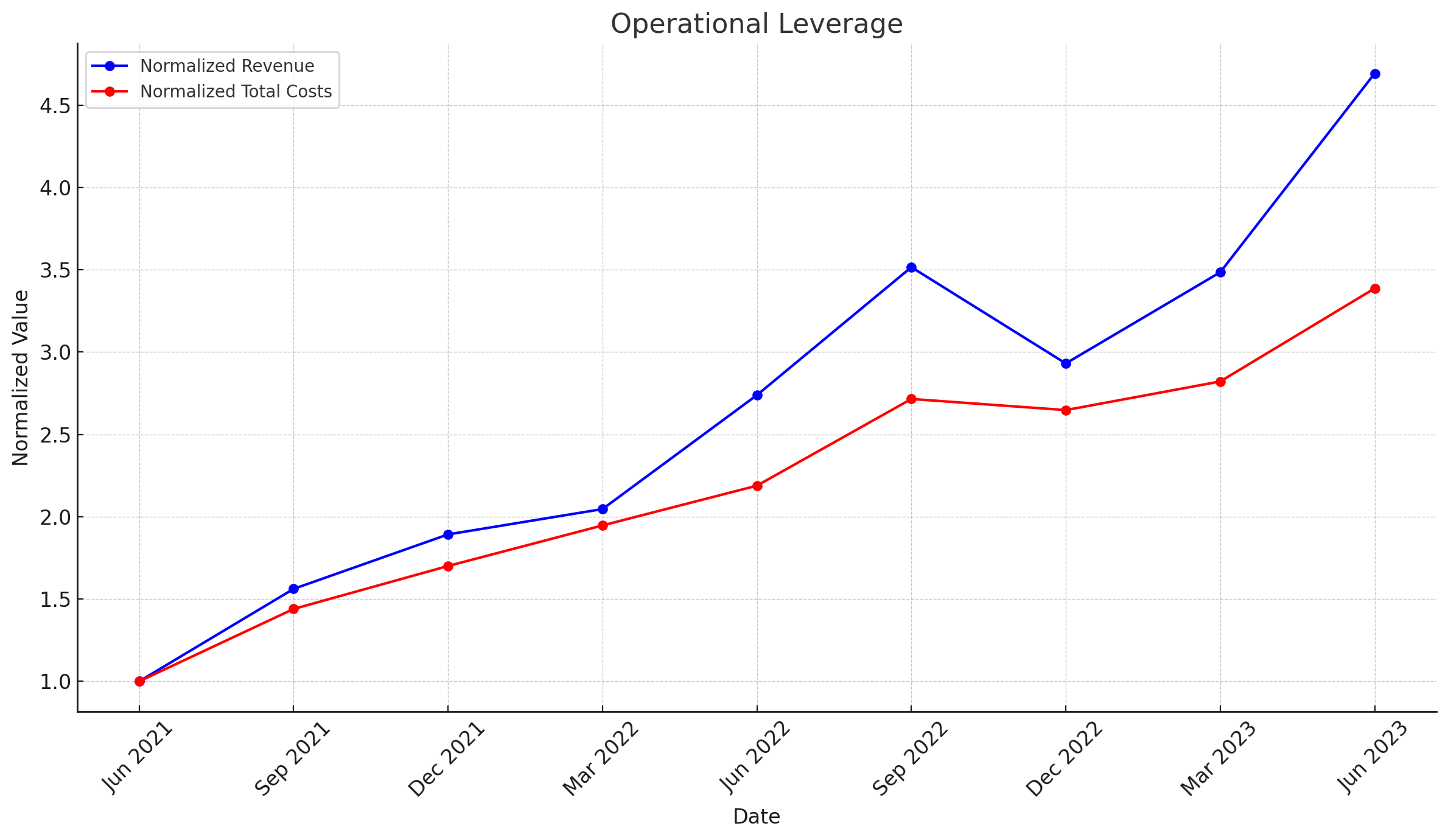

Normalized Cost and Revenue Growth (Author)

{kind=link}

For a growing business it is important to have a high degree of operational leverage. We have highlighted the importance of this in another one of our articles on the company Chewy ( CHWY ). High sales growth does not matter if operating expenses grow at the same or a higher rate. The chart above plots Revenue Growth vs. Total Costs (Opex + Cost of Revenue) both normalized to June 2021. As we can see Revenue has 4x'd while Total costs are up ~3.5x. This shows that there is operational leverage within the business. While a lot of this leverage comes from consolidating acquisitions it is good to see this level of cost control.

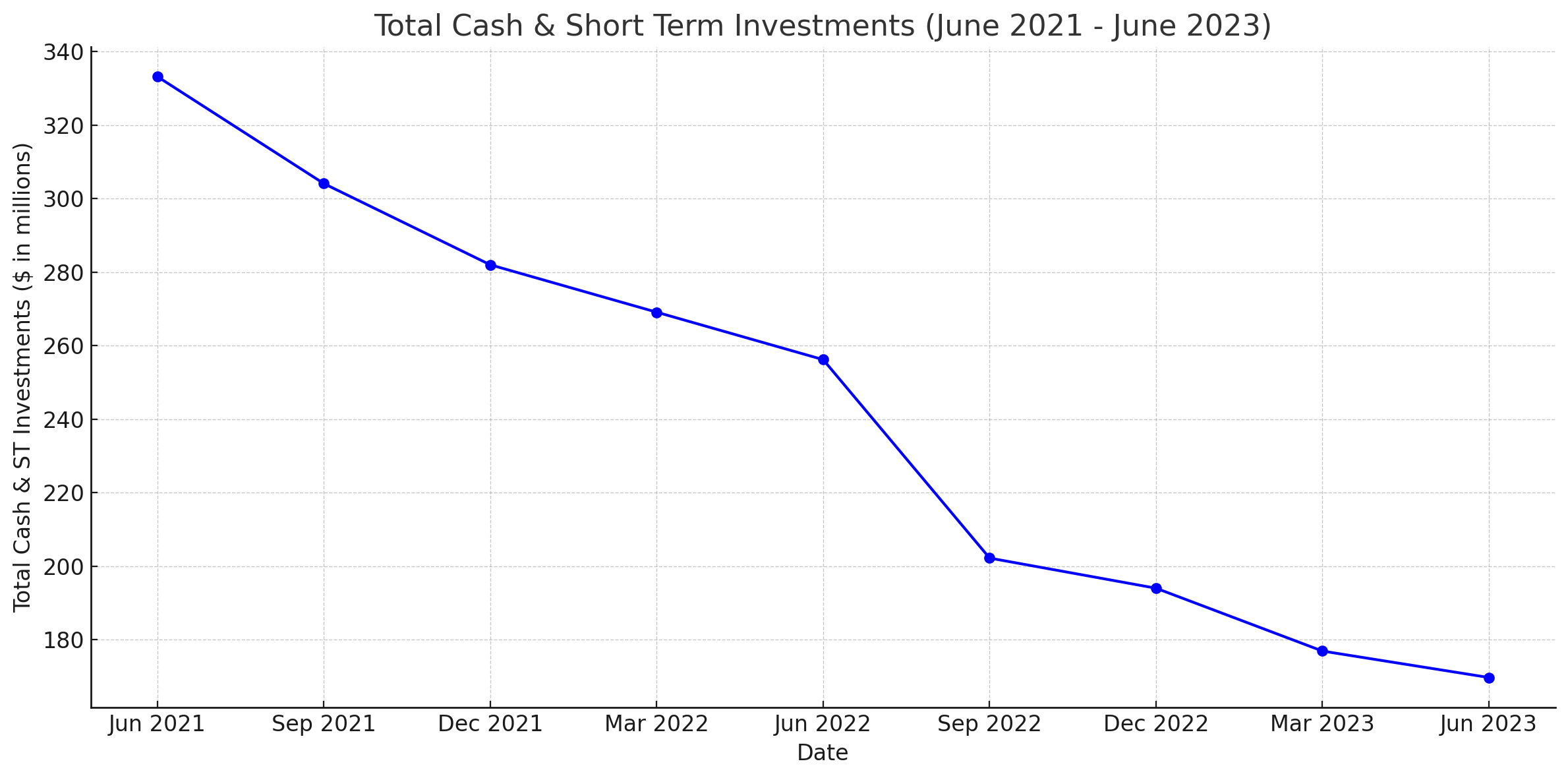

Blade's Balance Sheet

{kind=link}

The silver lining here is BLDE's cash position. With zero debt and approximately $170 million in cash and short-term securities as of Q2 2023, the company stands on a financially solid ground. A majority of the changes in their cash position has come from acquisitions and negative net income impacts.

{kind=link}

All the merger transactions since June 2021 have totaled $83 million which accounts for ~45% of their cash burn over that same period. At current levels cash and short-term investments on hand can cover 10 quarters of current cash burn of ~$12 million. With ongoing cost reductions and increased sales we believe BLDE is well positioned for near-term profitability with large upside from favorable eVTOL economics in 2024 and beyond. We expect to see operating income profitability in the next 4 quarters with a high likelihood of it occurring in Q1 '24. If profitability is not reached we at least expect to see cash burn continue to decline as more operational leverage is applied to all aspects of the business.

Innovation and The Future

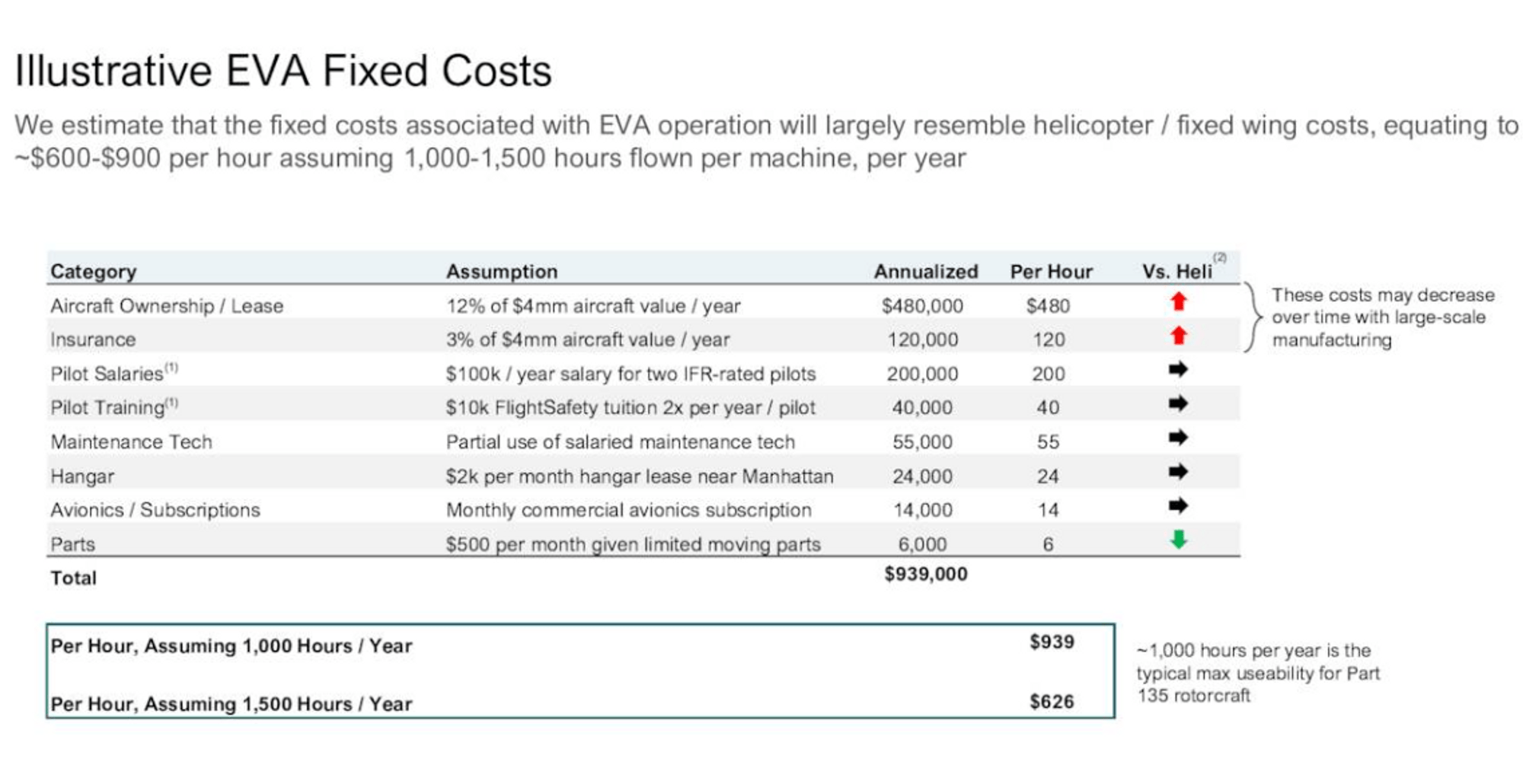

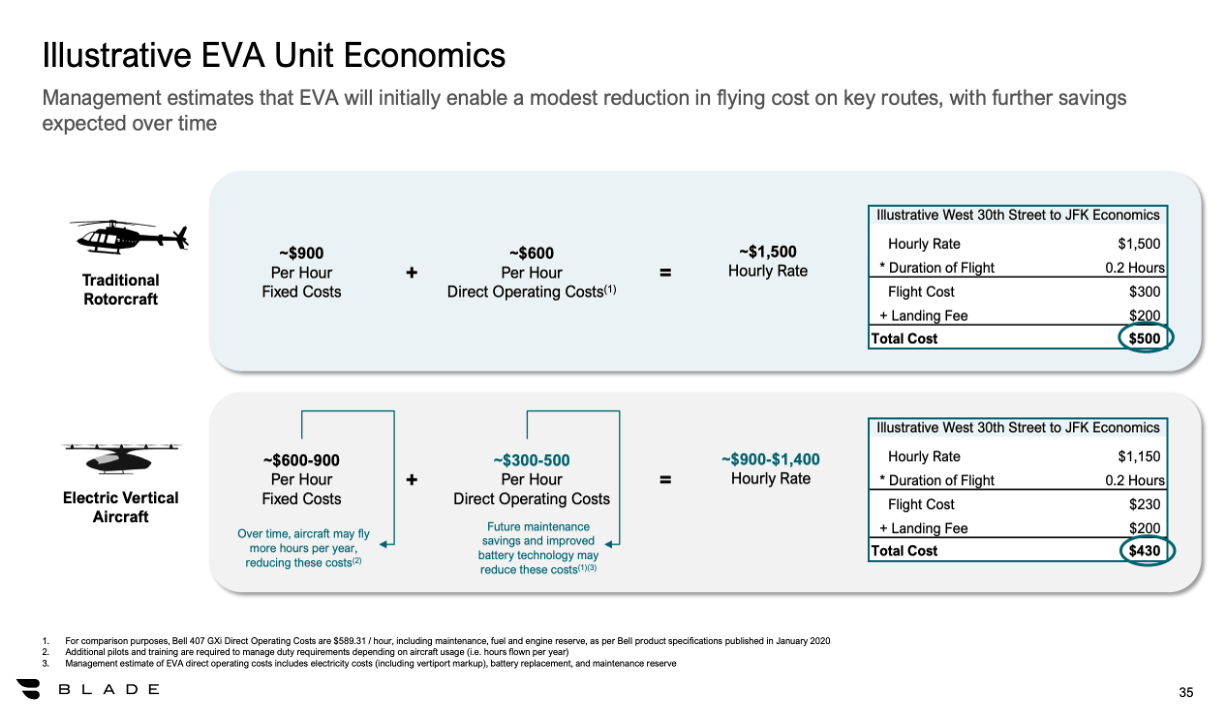

BLDE's proactive approach towards the future of mobility is evident. Their interest in Electric Vertical Aircraft and Electric Vertical Take-Off and Landing (eVTOL) technology resonates with the industry's trajectory, aligning with the Federal Aviation Administration's plan for its introduction by 2028. Moreover, BLDE's commitment to being equipment agnostic-partnering with various industry players-underscores its dedication to innovation, safety, and allows them maximum flexibility in the space. They do not own the equipment, so they will always be able to work with the eVTOL manufacturer/operators that offer them the most upside.

{kind=link}

{kind=link}

BLDE has provided a detailed analysis of what they see the benefit of eVTOLs being. As can be seen a majority of the benefits of comes from lower per hour direct operating costs as well as a potential reduction in per hour fixed costs. We see electric aircraft being significantly cheaper from a parts perspective due to the simplicity of these airframes relative to traditional helicopters. Similar to the difference between ICE cars and Electric cars there will be a massive reduction in moving parts which will lead to lower maintenance costs as there will be less parts to maintain and replace. We believe lowering costs and high levels of competition for BLDE's customers from the variety of eVTOL partners should lead to lower prices being offered to customers.

Risks

{kind=link}

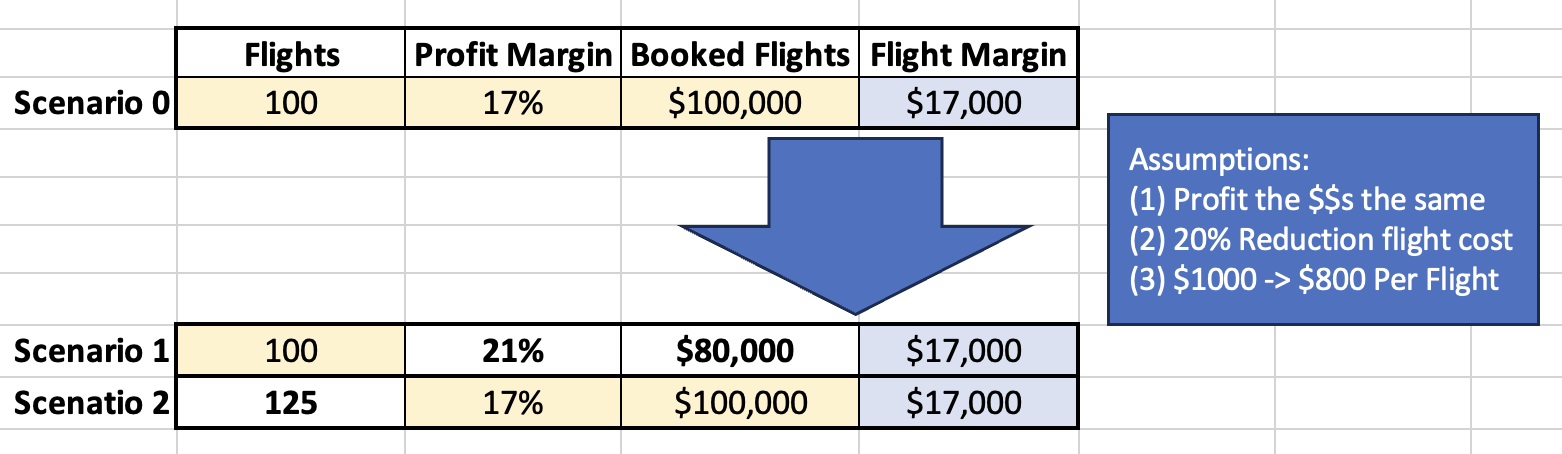

The primary concern we have for Blade is the potential for revenues to decline at a rate that outpaces any comparative increases in volume or improvements in margins. Should the savings from eVTOL implementation be directly transferred to consumers, the company would need to bolster either volume or margin to sustain their current earnings.

In our analysis, we've factored in a 20% price reduction for customers once eVTOLs are rolled out. To maintain consistent earnings amid this revenue shift, two potential scenarios emerge:

Scenario 1: If the flight volume remains unchanged, margins would need to enhance significantly. Specifically, a 20% drop in flight prices would necessitate a 25% surge in flight margins.

Scenario 2: Alternatively, the second scenario centers around an uptick in flight volume while assuming a consistent profit margin of 17%. In this scenario again we see the need for a 25% surge but this time in flights.

Valuation

With Blade not owning any vehicles and primarily being a software/chartering business we believe that any valuation should be focused around EV/Gross Profit. Currently, BLDE has an EV of $97 million and has a TTM Gross Profit of $31.8 million.

Seeking Alpha

The EV to Gross Profit valuation stands at 3.05X. Given the current growth trajectories in the Medical Flight segment, the prospective uplift from eVTOL implementations, and our anticipation of near-term operating income profitability, we find this valuation compelling. We see them as only benefiting from any developments in the eVTOL space with little to no downside due to them being manufacturer agnostic.

eVTOL is the "sexy" side of the business that will get the most attention both publicly and by investors on earnings call, but the current business driver here is the Medical Transport Business. If we take out the contributing earnings from Passenger Flights and annualize the Profits from Medical Flight we get a EV to Gross Profit Valuation of 4.24X. With the significant growth rates we see in Medical Flight we believe that at current prices we are getting the Medical Business for a significant discount and that the Passenger side of the business comes along for free.

Conclusion

We believe there is a solid foundation here with Blade Air Mobility, Inc. We believe that at current prices you are buying a proven business with potentially near-term positive Net Income and massive catalysts from the eVTOL space. We believe this is a hidden gem in the eVTOL space and is a must add for any future transport portfolio. We are a 'Strong Buy' at current prices and due to the low Implied Volatility (IV) we plan to purchase shares as well as initiate a synthetic long by purchasing Feb. 2024 $2-$4 Call Options and selling Feb. 2024 $3 Put Options. We see significant upside and will be using any profits from this trade to purchase further shares instead of simply using profits to lower our cost basis.

For further details see:

Blade Air Mobility: A Strong Business With Solid Potential