BLX - Bladex: 7% Yield And Dramatic Mispricing At This Trade Bank

Summary

- This unique Latin American trade bank is a strong buy.

- Trading around 7.5x earnings and earnings are still relatively depressed. It's closer to 6x earnings based on its normal results.

- Bladex pays a safe 7% dividend yield which could be hiked once again.

- The bank is exceedingly conservative, backed by regional central banks, and takes minimal credit risk.

I've been buying shares of Banco Latinoamericano de Comercio Exterior ( BLX ), or Bladex for short, throughout 2022. The company's name, translated to English, is the Foreign Trade Bank of Latin America which is an apt description of the company's business model.

The bank is headquartered in Panama, although it is not particularly tied to that country from a results basis; its loan book is spread all across Latin America and has little financial exposure to Panama itself.

Bladex is not a normal retail bank. It doesn't take retail deposits and then lend to the consumer for credit cards, mortgages, and so on.

Instead, Bladex is in large part owned and funded by Latin American central banks. Bladex uses those funds to extend credit primarily for trade purposes. Here's the bank's business in its own words :

Bladex provides foreign trade solutions to a select client base of premier Latin-American financial institutions and corporations, and has developed an extensive network of correspondent banking institutions with access to the international capital markets. Bladex enjoys a preferred creditor status in many jurisdictions, being recognized by its strong capitalization, prudent risk management and sound corporate governance standards [...]

The Bank’s lending and investing activities are funded by interbank deposits, primarily from central banks and financial institutions in the Region, by borrowings from international commercial banks, and by sales of the Bank’s debt securities to financial institutions and investors in Asia, Europe, North America and the Region. The Bank does not provide retail banking services to the general public, such as retail savings accounts or checking accounts, and does not take retail deposits.

The most interesting thing about Bladex is that it is essentially the bank of the Central Banks of Latin America. The Central Banks have a large ownership position in Bladex stock and central bankers make up a large portion of Bladex's board of directors. This, as the bank itself says, gives its close ties to the governments of Latin America.

It also gets other special privileges from this arrangement, such as having preferred creditor status if a borrower defaults. Not surprisingly, central bankers want their own funds to get repaid first if a queue forms.

How safe is Bladex? It's remarkably safe for an emerging market bank. That's primarily due to the structure of its business. As of Q4 2021, fully 75% of Bladex's loans mature within a year. This is trade finance, pure and simple.

Think of a Brazilian company that is shipping materials to a plant in Mexico, for example. If that transaction needs intermediate financing while the ship is carrying the goods to Mexico, that's a classic sort of trade credit scenario. Bladex, being headquartered next to the Panama Canal, is a logical provider for this sort of short-term line of shipping credit business.

In addition to making very short term loans, Bladex is also selective about its borrowers. It heavily prioritizes lending to firms which generate dollar-based revenues. This reduces foreign exchange risk. Also, Bladex's borrowers have to generate at least $200 million per year of revenues and have access to capital markets.

By making short-term loans to large companies that earn revenues in dollars, this greatly reduces risk of any loans not being repaid. To further reduce risk, Bladex avoids concentrated risk in any given country. As of Q4 '21, here is Bladex's footprint by country:

- Brazil 17%

- Colombia 13%

- Mexico 11%

- Chile 10%

- All others less than 10%.

Any one country experiencing political unrest or other negative shocks will have a modest impact on Bladex's overall loan book.

If anything, the biggest risk to an investment in Bladex is stagnation rather than sudden downside risk. This is reflected in the bank's persistently low (and now even lower) valuation ratio.

Today, the bank is trading at 0.51x book value. Historically, this is an unusually low ratio for the bank. That said, it hasn't traded meaningfully over 1.0x book value in ages:

Based on my usual rubric of paying 10x median return on equity “ROE” for a bank, BLX stock should be worth around 0.9x book value, as it has averaged a 9% ROE in recent years. This would make BLX stock worth around $25 today versus today's current price of $14. That, plus a 7.0% dividend yield is a rather attractive set-up.

And I'd argue there are several factors that could push the valuation to at least $25 if not higher.

Trade Finance: An Efficient High-Volume Operation

For one, this is a volume business, for better or worse. Bladex never makes high margins on its loans. That's the nature of the game as it relates to trade finance. A successful bank in this category is making lots of loans and frequently turning over its book.

Also, there's a strict focus on costs. Since Bladex doesn't have a retail consumer business, it has very low overhead. It averaged an efficiency ratio of 35% over the past five years (lower is better) which is phenomenal. Out of all the banks I closely follow, only Hingham Institution for Savings ( HIFS ) is more efficient. Most LatAm banks run in the 50% efficiency ratio range, meaning that Bladex is saving 1500 basis points of costs thanks to its lean structure. Big U.S.-based banks are even higher, often running closer to 60% efficiency ratios.

Given that Bladex can't cut costs much more and it earns low spreads on its loans, the bank is highly sensitive to marginal loan volumes. Bladex's earnings dropped significantly in the late 2010s as the prices of oil, iron, steel, copper, coal, and farm goods slumped. Those are key products and exports of South America, and with much lower prices, there was less business for Bladex to facilitate.

Going forward, this should reverse. Now the demand for virtually all of those commodities has surged. As more production happens in Latin America, more businesses will need short-term loans to grease the wheels of commerce. This should allow Bladex to make profitable loans more frequently.

Growth Has Returned As Commodities Soar

Additionally, recall that Bladex gets a large portion of its deposits from Latin American central banks and governments who park their funds there since it is a safe stable bank operated in part by those same central bankers. As of Q4 '21, 49% of Bladex's deposits are from central banks and another 10% are from state-owned banks, meaning that Bladex is well-funded with sticky high-quality deposits. As economic activity and tax receipts pick up, Bladex should receive more deposits as well, giving it additional funding with which to pursue a larger loan book.

We're already seeing this growth in practice. Bladex's deposits already have surpassed Dec. 2019 levels. The bank's loans, while not quite back to 2019 levels, are almost there and surged compared to 2020. Given how much commodity prices and economic growth have picked up in the region, Bladex should be able to reach a new peak size of its loan book shortly. To put one number on that, Colombia -- Bladex's second-largest market -- just reported 12.6% GDP growth this past quarter.

As mentioned, there's not much excitement with Bladex's loans, it gets low yields on these products and makes money on volume. As long as volumes are hitting new highs, earnings should follow, especially since the bank has increasing asset to deposits with which to fund further lending.

Where is the additional lending going? In 2021, the Bladex's biggest increased lines of lending were in Guatemala for its electric power sector, Chile for oil and gas, Mexico for oil and gas, and Uruguay for oil and gas. In case it wasn't obvious, higher energy prices are really good for Latin America. Bladex should have a long runway for putting capital to work in these sorts of loans given the current global energy landscape.

Oil and gas lending might sound risky. But remember, after all, the majority of these loans are for 12 months or less. Bladex is simply getting investments rolling, it's not sticking around for the life of a working oil asset.

Looking At Risk

Bladex has a high credit rating for Latin America, as you might expect for a conservatively-run bank operated by regional central bankers. Bladex also maintains 86% of its cash position at the Federal Reserve Bank of New York. This should give shareholders further security in knowing that the bank's reserves are well taken care of.

What about credit risk? Bladex's extremely short loan durations, combined with its strict lending standards, greatly reduce risk. Even in December 2020 during the height of a sharp pullback in regional economic activity, Bladex only saw 0.2% of its loans become credit impaired. That'd be impressive even in the United States and it's doubly so in Latin America where regional governments provided far less economic assistance to struggling businesses.

In my view, the bigger risk to Bladex is simply insufficient profitability rather than downside risk. The bank's average loan interest rate fell to 2.5% in 2021, down sharply from 4.6% in 2019. The bank's funding cost overall dropped from 3.1% to 1.0% over the same span so its spread stayed exactly the same.

However, there were obvious problems on the horizon. After all, a bank's funding cost can (normally) only hit 0.0% at rock bottom so there was little room left for Bladex to save money with lower deposit rates. Meanwhile, the lending side was seeing extreme pressure with countries like Colombia and Brazil having exceptionally low interest rates during the pandemic compared to their historical medians.

Needless to say, at least for the time being, we no longer need to worry about lower interest rates. The Fed is set to aggressively hike interest rates. In LatAm, the central banks are ahead of the Fed – banks such as Brazil have been on an absolute tear.

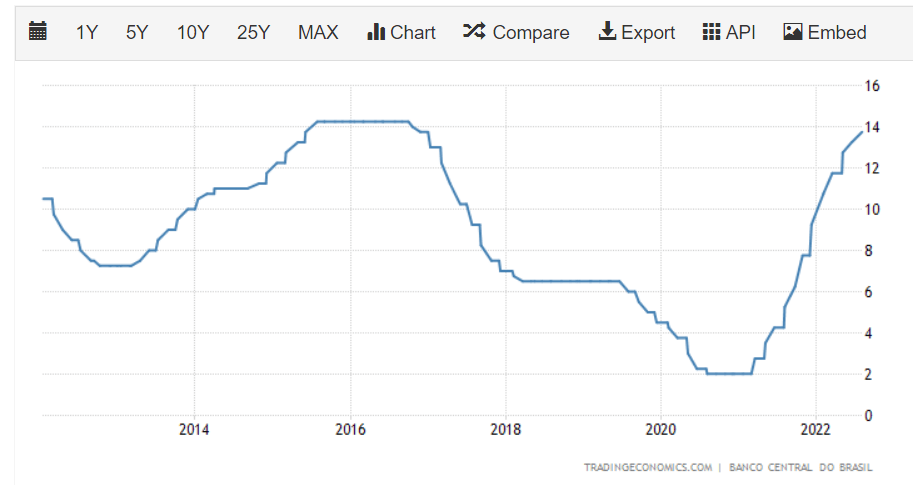

{kind=link}

Brazilian central bank rate (Trading Economics)

Brazil's central bank has gone from a 2% to 14% interest rate since 2021. Bladex should be able to hammer out a little more yield on its loans to Brazilian borrowers.

Since Bladex is lending is to high-quality borrowers on a short-term basis, it's never going to generate huge spreads. Its loan book was only pulling 4.6% in 2019 during a more normal economic period. This isn't your typical LatAm bank that is out charging double-digit rates on standard home mortgages or anything like that. Bladex makes its money from having cheap deposits, high-quality customers, and close relations with central banks, it doesn't make money from fat interest rate spreads.

Valuation & Capital Return

Additionally, and this gets toward valuation, Bladex has had little interest in growth historically. Given that its loans are short-term, it is always having to put its capital immediately back to work. This limits how much money it can reasonably deploy in its business. Instead of retaining profits to dramatically build its loan book, Bladex instead pays out most of profits to shareholders.

Indeed, a look at Bladex's long-term chart shows a pretty uninspiring result. Over the past 20 years, for example, BLX stock is up 255% which is hardly a breathtaking result given how much other Latin American stocks appreciated in the early 2000s. However, with dividends added in, BLX's return jumps from 255% to more than 1,000% over the same stretch.

This huge disparity is because the bank has typically paid out at least 60% of profits to shareholders as dividends and often closer to 100%. Incentives are well-aligned here. Remember that Latin American central banks own a bunch of BLX stock and make up a large part of its Board of Directors. By paying an outsized dividend, the central bankers are returning a lot of capital to themselves.

---

However, there was an interesting shift in the strategy in 2021. The bank, which had paid out at least 71% of earnings as dividends each of the past five years, instead pivoted to a share buyback.

After years of not buying back stock, BLX made an aggressive move as its share price hit unusually low valuation levels.

For the first time in ages, Bladex repurchased a major chunk of its stock, buying back $60 million of shares. This made a big dent in the company's overall outstanding share count, dropping it from 40 million to less than 37 million.

With the stock around half of book value, this was immediately and sharply accretive to remaining shareholders. On top of that, the bank is at less than 8x trailing earnings, which means Bladex has been getting something like a 12% earnings yield on its share repurchases. While investors primarily own BLX stock for its fat dividend, this sort of opportunistic buyback can add a lot to total shareholder return.

Even with big share repurchase, the bank ended 2021 with a 19.1% Tier 1 capital ratio, far in excess of what is needed to operate the bank. This leaves plenty of room for additional buybacks and/or a dividend increase in addition to funding loans if the opportunity arises.

Even if the dividend is held here at $1.00 instead of being increased, shares currently yield 7.0%. And, it should be noted, Panama has no withholding tax on dividends so there's no hit to foreign holders on that yield.

The Upside Scenario As Inflation Takes Hold

That's plenty good on the yield as things stand today. But let's assume Latin America's economy picks up to 2011-13 levels of activity. The prices of oil, copper, coffee, and various other commodities are roughly as high or higher today than they were then. So this 2012 seems like a reasonable baseline for where LatAm could be in 2023 or 2024.

In 2012, Bladex was earning a 1.6% net interest margin as opposed to 1.2% last year. That sounds like a small difference, but it has a huge impact. In 2012, Bladex earned a 12% ROE, whereas it only did 6% last year.

In 2012, Bladex earned $2.44 per share and this supported a dividend in the $1.50 per share range. Last year, the bank earned $1.62 and paid out $1.00. Moving earnings back to 2012 levels puts the stock at 6x earnings. And the return of a $1.50 per share annual dividend would be a greater than 10% yield on the current share price.

Additionally, thanks to the recent share buyback, there is now less Bladex stock outstanding than there used to be, adding some additional juice to those calculations. In any case, the value proposition should be clear; at $14 with a 7% starting dividend it doesn't take much to go right here to make money. And the bank has various options – such as another share buyback or a dividend increase – to immediately boost the stock price.

And sure, you can find a lot of banks trading at single digit P/E ratios at the moment. However, few banks have so little downside risk. Since Bladex doesn't make many long-term loans and because it is backed by the region's governments and central banks, it takes miniscule credit risk. Just 0.2% of its loans soured in 2020 even with commodity prices through the floorboards; its loan losses should be near zero now that the regional economy is rapidly expanding.

Even the bear case scenario here just looks like the bank continuing to spit out the 7% dividend while trading at a large discount to fair value. Not the end of the world. And on the upside, Bladex could easily trade back to book value – $28 per share – while hiking the dividend dramatically over the next year as the LatAm economy revs up.

If you want to profit off the rise of oil, coal, lithium, soybeans, steel, iron ore and other regional exports without actually having to own cyclical commodity mining or agriculture companies, Bladex is a great way to get that exposure and a massive dividend to boot.

For further details see:

Bladex: 7% Yield And Dramatic Mispricing At This Trade Bank