BLND - Blend Labs: Burning Cash And Diluting Shareholders

2023-12-12 10:06:04 ET

Summary

- Blend Labs, Inc. is facing financial challenges with high interest expenses, negative operating income, and cash burn.

- The company operates in two segments, Blend Platform and Title365, serving the financial services industry.

- Despite positive growth projections, the lack of margin improvement and uncertainty make it a risky investment, leading to a sell rating.

Investment Rundown

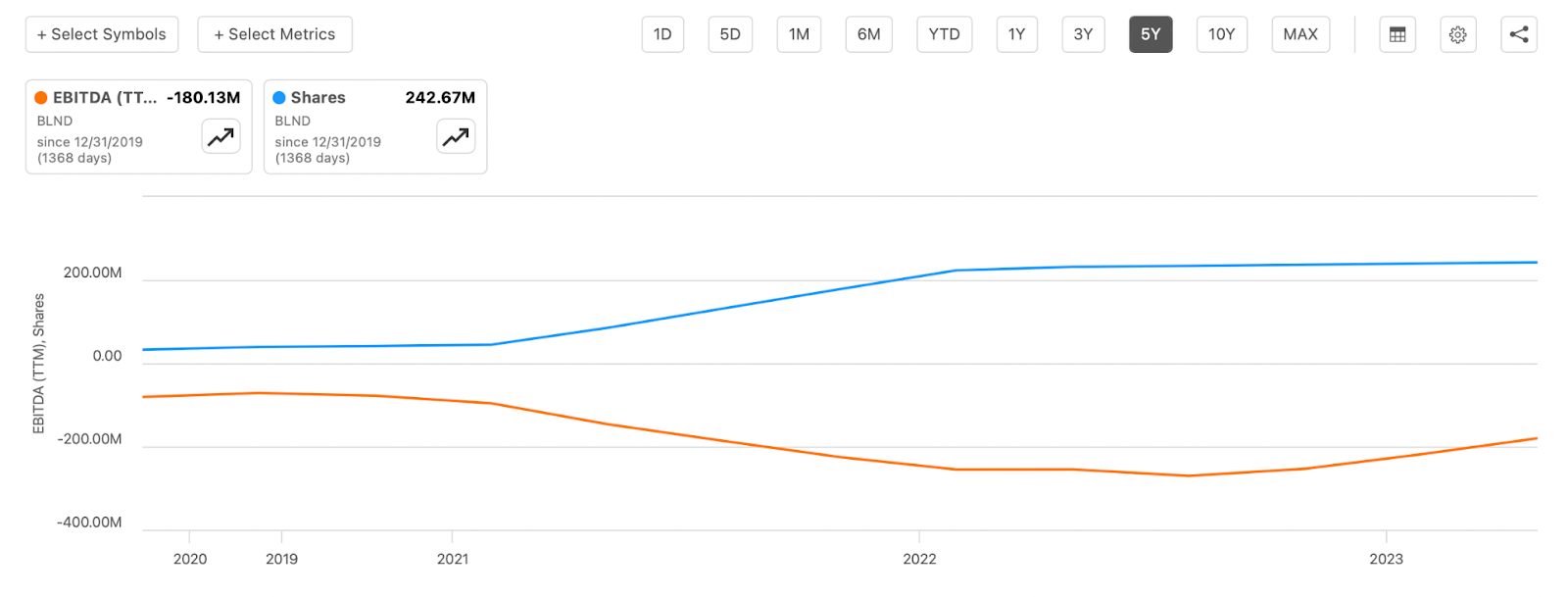

The tech industry has been under a lot of pressure as interest rates seeing as many of the companies are often taking on debt to rapidly fuel growth. Blend Labs, Inc. ( BLND ) is no different here and the company has seen a rapid rise in interest expenses, now reaching over $30 million in the last 12 months, with the potential of over $40 million should rates stabilize here. With already negative operating income because of high staff costs and R&D expenses, it has put BLND in a tough spot right now. The company has been bleeding cash since 2021 and investors have gotten significantly diluted as well.

Estimates for both the top and bottom line seem decently positive over the next few years, but I think given the rough shape the business seems to be in right now investors are simply better off staying away I think. The company is performing worrisome practices like diluting shareholders and quickly burning through its cash position with no significant improvements in the company margins. This all accumulates to me rating BLND a sell right now.

Company Segments

BLND is involved in offering cloud-based software platform solutions tailored for financial services firms across the United States. The company operates through two distinct segments, namely Blend Platform and Title365. Even as a business included in the tech sector, it works as a global financial services application platform. Meaning that BLND has exposure to essentially two various markets. In terms of the growth of the primary financial service market, it seems to be exhibiting a near double-digit growth number annually over the coming decade at least.

At the core of BLND services is the Blend Builder Platform, which stands as a comprehensive suite of products designed to drive digital-first consumer experiences across various financial transactions. Specifically, the platform caters to the intricacies of mortgages, home equity loans and lines of credit, vehicle loans, personal loans, credit cards, and deposit accounts.

{kind=link}

The Blend Builder Platform serves as a versatile tool, empowering financial services firms to navigate the complexities of modern consumer journeys seamlessly. By leveraging technology, Blend Labs aims to enhance and streamline the entire process for both consumers and financial institutions. The platform not only addresses the intricacies of mortgage transactions but also extends its capabilities to other key financial products, such as home equity loans, vehicle loans, personal loans, credit cards, and deposit accounts.

{kind=link}

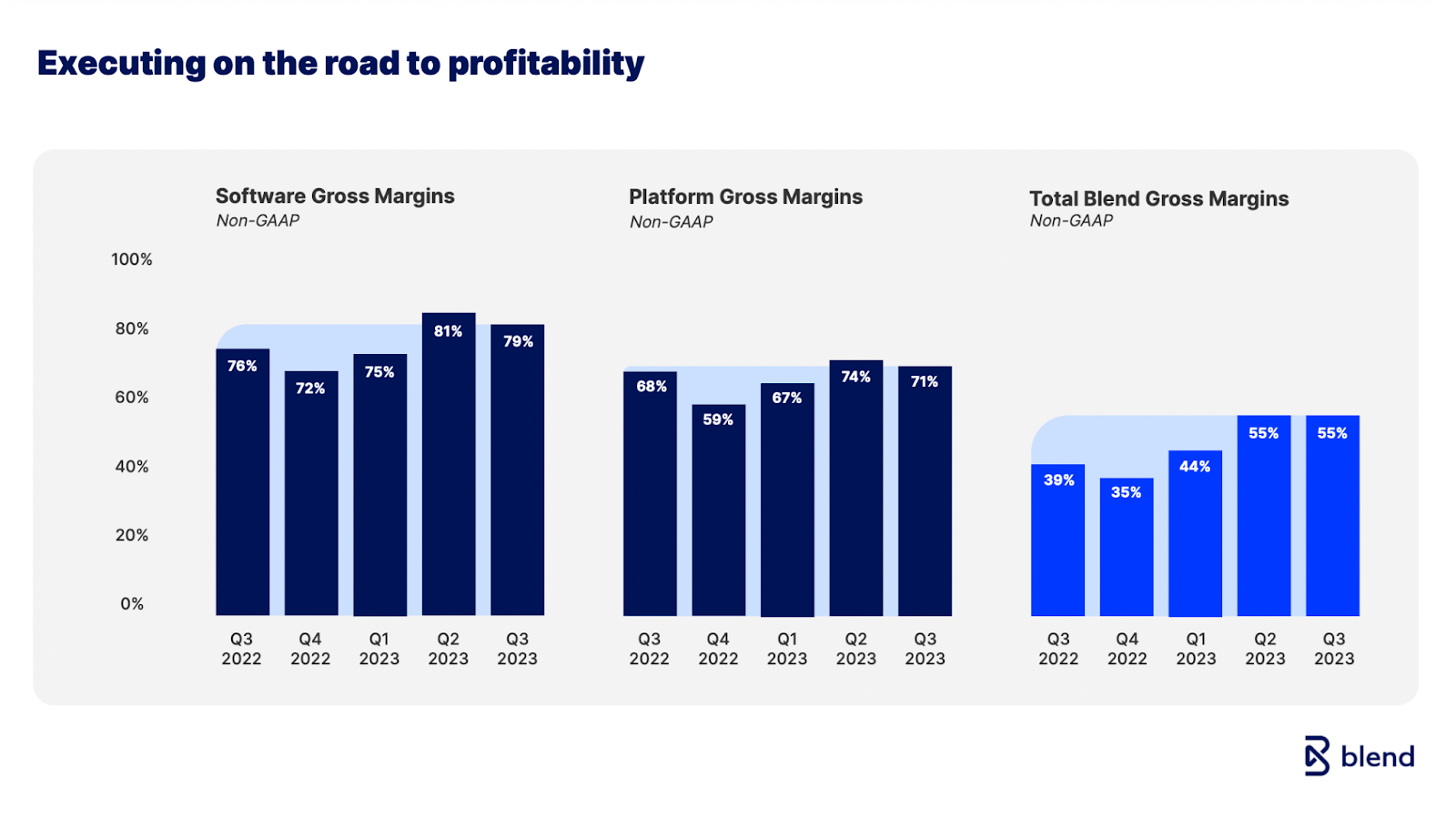

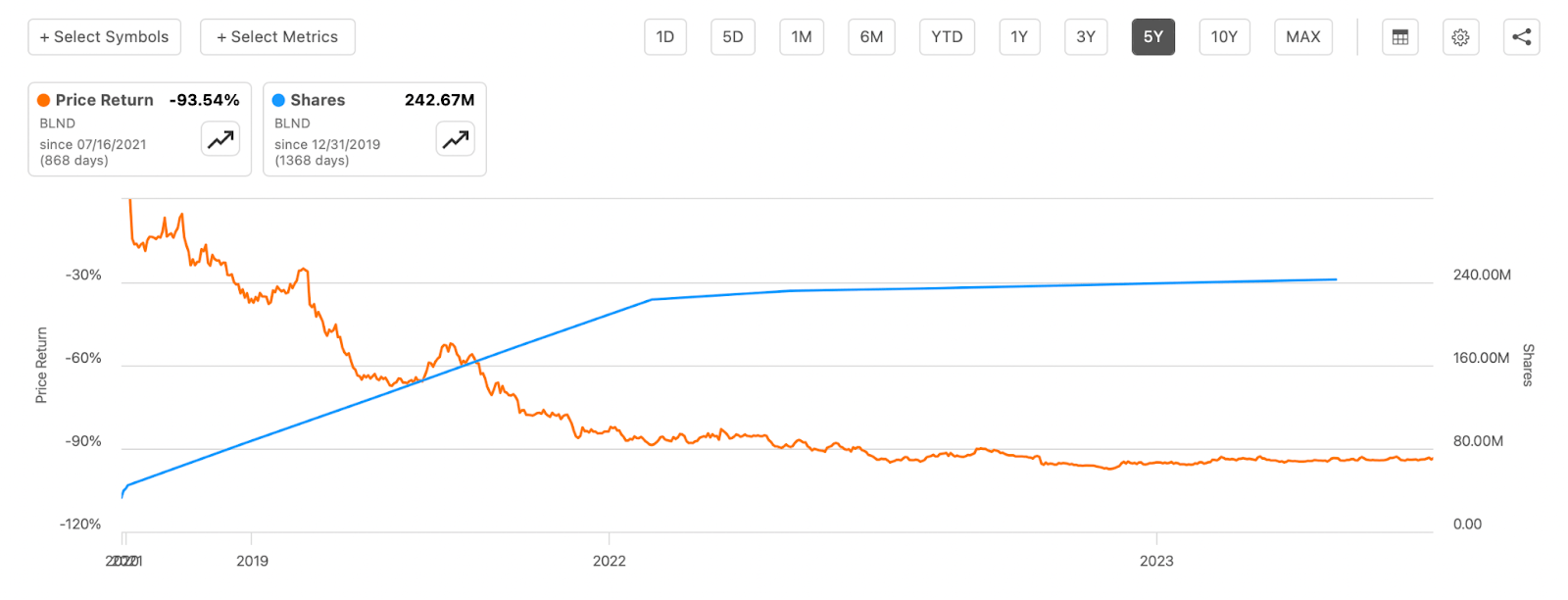

One of the challenges the company has been facing is the lack of margin improvement which has led to a continued negative operating income for the business. The EBITDA seems to be on the rise slightly right now after a significant slump during 2021 and 2022. During this period, the company continued to dilute shares and it doesn't seem to have had such a significant effect on margin improvements, which makes me very worried about the medium term. The lack of improvement and uncertainty seems to have aided in the poor stock price development over the last 12 months, staying very stagnant around the $1.3 - $1.4 mark. I don't think we will see any significant movement until BLND can showcase margin improvements rapidly.

Earnings Highlights

{kind=link}

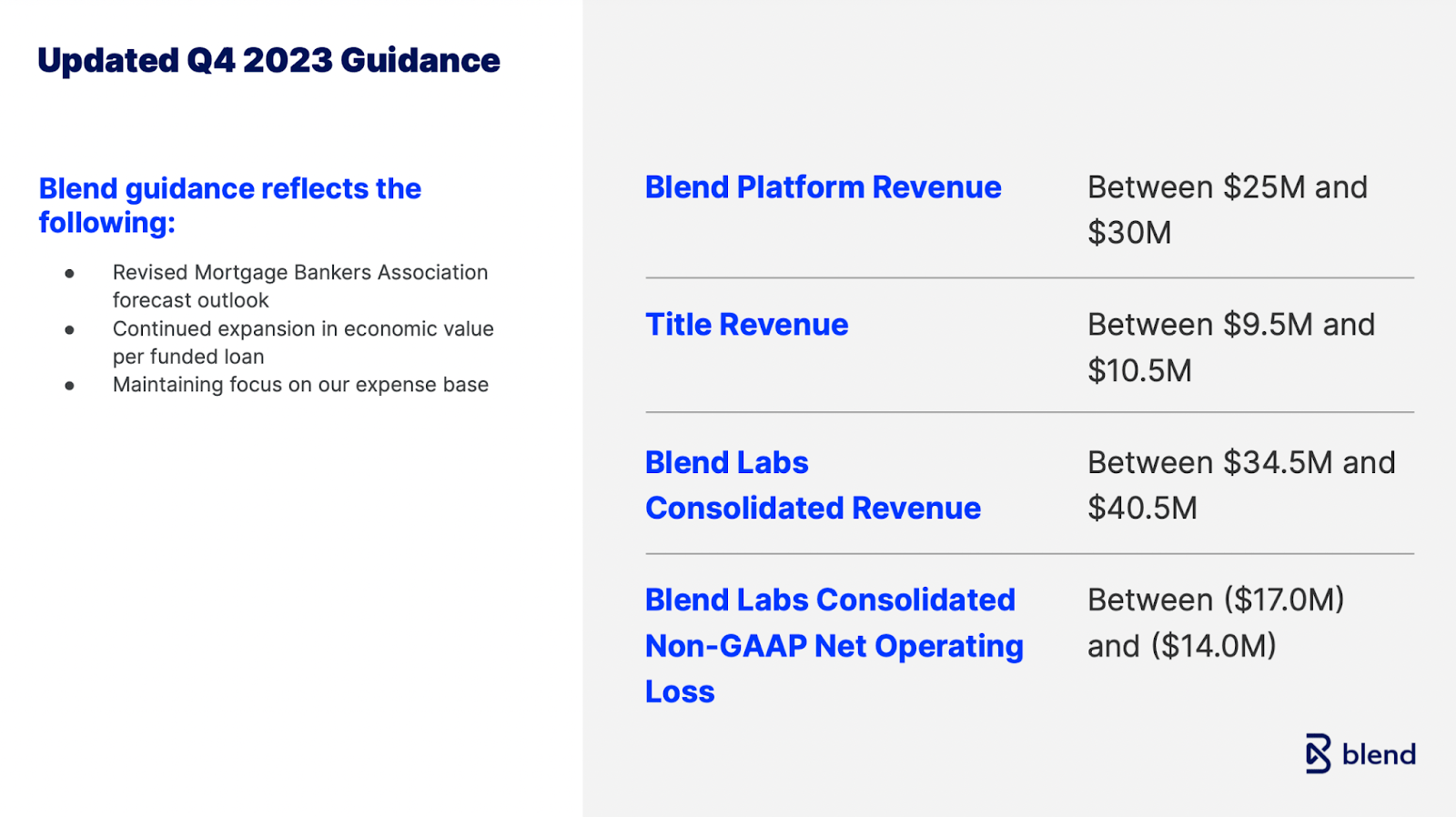

In the last earnings report by the company which was released on November 7, the management updated the guidance for Q4 2023. The updated guidance now reflects further expansions and market share growth in value per funded loan. The platform revenues are to be between $25 and $30 million now, which means to see sequential growth BLND needs to achieve the upper end of that guidance as Q3 had a revenue of $28.6 million. I think there is a significant risk that the share price may plummet should the revenues be missed there. A large portion of the company's revenues come from that source and with poor growth in that segment investors may lose interest quickly.

{kind=link}

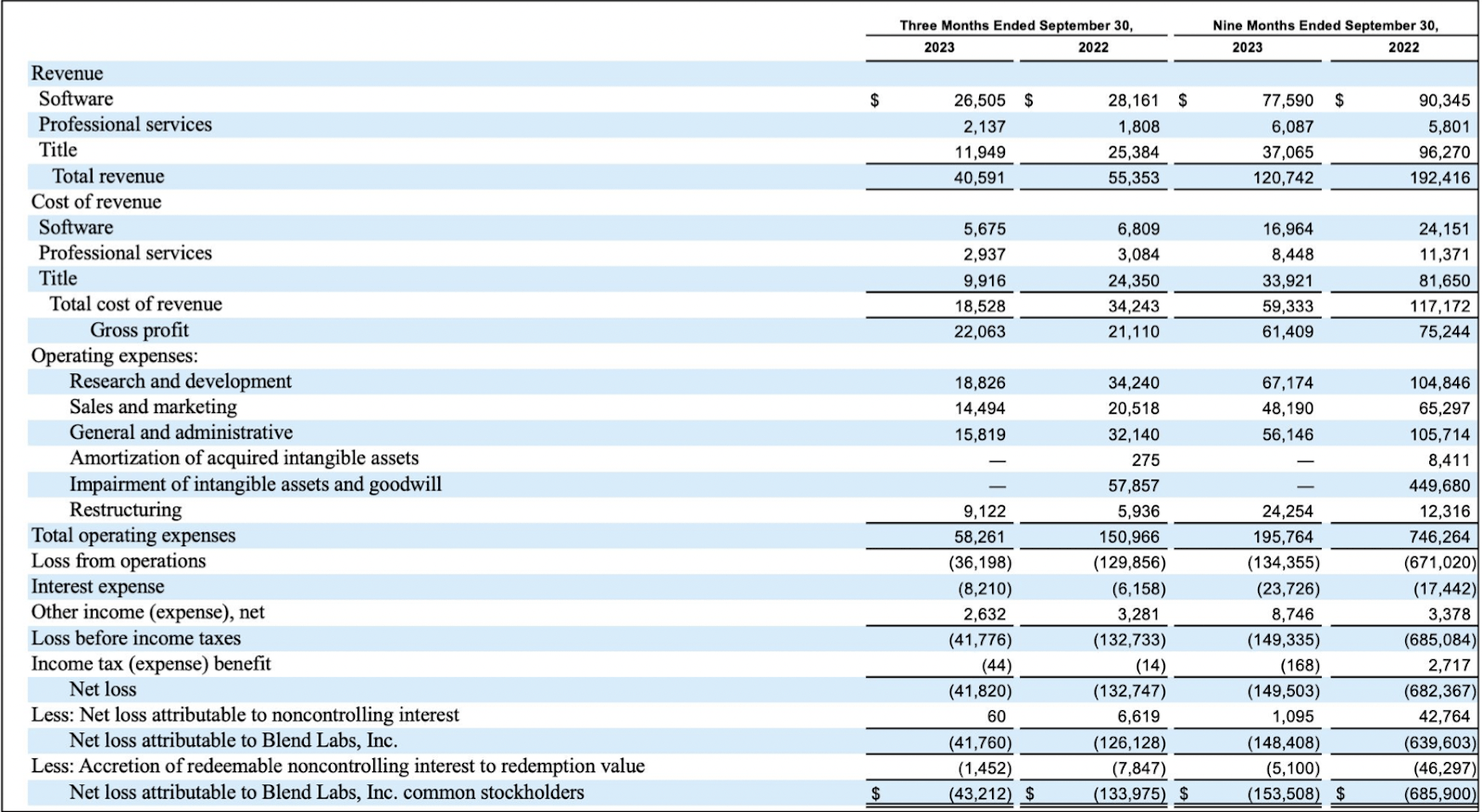

Diving deeper into the revenues of the business though we can see worrisome trends appearing, like the software revenue falling by over 16% YoY and the title revenues by over 60% in the nine months so far in 2023. This seems to be a direct result of the rise in interest rates in the last 12 months. It has impacted the spending power of companies and with BLND still being quite small and without a large customer base yet to be established volatile results like these are likely to continue.

What has been a positive trend is the improved gross profits, at least even as the total revenues declined YoY. It still hasn't meant that BLND is generating close to positive operating incomes yet. With interest expense rising by almost 30% YoY to $8 million quarterly for the business, I think we will see further bottom-line pressure for at least the next 12 months. YoY the shares rose by 4.6% and the share price wise it has risen by just under 4% in the last 12 months. This highlights the fact that investors have in reality made a loss on their investments in the last 12 months because of the dilution.

{kind=link}

On the FCF side of the report, we see a further negative margin of 64%. Furthermore, with the company unable to generate positive cash flows, they are forced to take from the cash position to pay down interest. Last quarter $7 million went that way. Should it continue in that manner then there is only cash available for 12 more quarters of paying down interest with a cash position of $84 million. That is worrisome and I think it will be shorter as cash is also going towards funding operations as well.

{kind=link}

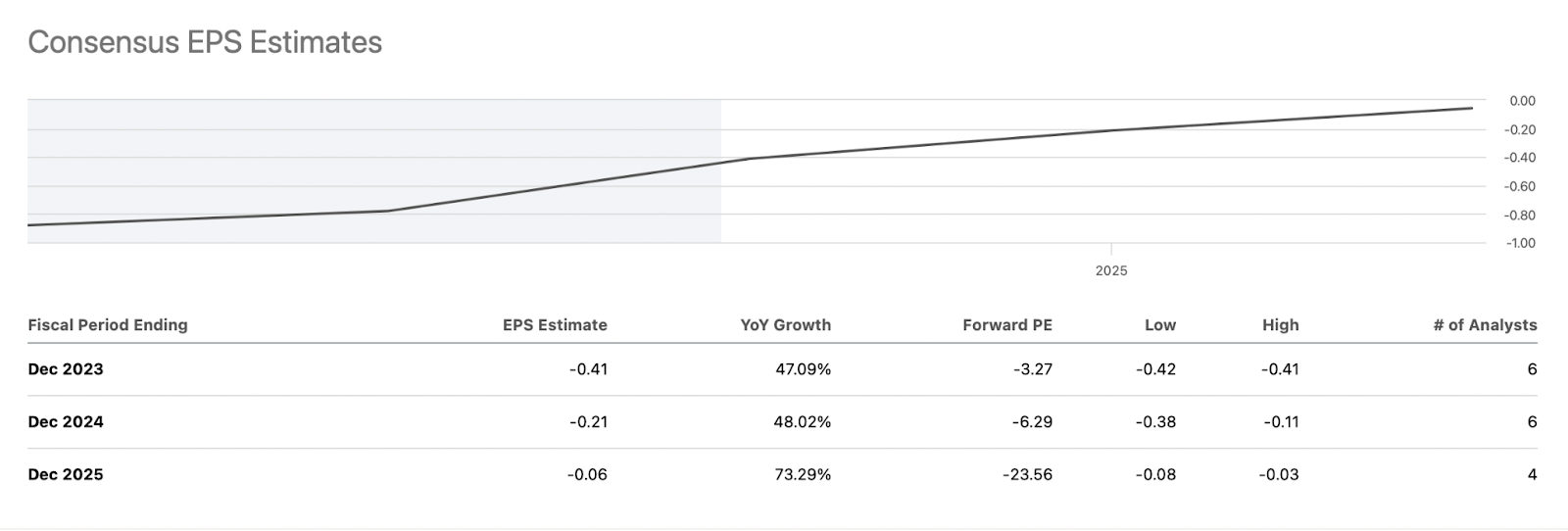

The estimates for BLND suggest that around 2026 there might be the first positive EPS posted. Anticipating a 15% YoY growth rate from 2025 onwards with the EPS we land in 2030 at EPS of $0.17. With the current share price at $1.3 that is a FWD p/e of 7.9. I will be applying the financial sector's average p/e here seeing as that is the primary market it serves even as it's a tech business essentially. Most financial companies trade around 11x earnings and that leaves an upside of 39% for BLND. Now, we are 7 years out from 2030, and dividing the upside by 7 we only get a potential CAGR of 5.5% which I think is quite lackluster. With all this said, I think investors are better off looking elsewhere and this leads me to rate BLND a sell right now.

Risks

Investors currently grappling with BLND face a prominent risk rooted in the company's struggle to achieve profitability. The stark reality is that the lack of profitability raises concerns about BLND's ability to sustain itself without resorting to measures like diluting shares. This necessity arises from the imperative need to cover operational costs and remain financially viable.

{kind=link}

Given the prevailing circumstances, a plausible scenario emerges where BLND may resort to issuing additional shares as a means of raising capital. This, however, introduces the risk of dilution for existing shareholders, potentially diminishing the value of their holdings. The anticipated continuation of share issuances could further exert downward pressure on the stock price, exacerbating the challenges faced by investors.

Final Words

Financial service companies are in a pretty tough market climate as interest rates are rising which puts pressure on company spending. We have seen these impacts on the income statement for BLND and it hasn't been good. The stock price has gone nowhere in the last 12 months and even if they reach profitability in 2026 the upside is not there I think, even if we apply a higher p/e. The company is also burning cash very quickly and shares are constantly issued as well, making the only reasonable rating here a sell in my opinion.

For further details see:

Blend Labs: Burning Cash And Diluting Shareholders