PYPL - Block Addressed Our Concerns; Rating Upgrade

2023-11-09 11:32:53 ET

Summary

- Block's stock surges by 17% following strong earnings and guidance that exceeded expectations.

- The company announced a $1 billion share buyback program to offset dilution caused by share-based compensation.

- Block's focus on efficiency and profitability improvement, as well as progress in its Square and Cash App ecosystems, leads to an upgrade in stock rating to hold.

Introduction

Block stock experienced a significant surge on a Friday morning following the company's announcement of more efficient growth targets. This notable increase mirrors a similar positive trend seen in the rival PayPal Holdings, Inc. ( PYPL ), which we rated as a strong buy, as investors seem to be turning more optimistic about payment stocks.

In this article, we will delve into the reasons behind this resurgence and explore the impact on Block and PayPal's stock values. Furthermore, we explain why we have upgraded our rating.

Block Is Looking For a Rejuvenation

Block, Inc. ( SQ ) shares shot up by 17% to reach $51.35 in premarket trading, a remarkable response to their recent earnings and guidance that exceeded expectations.

In the third quarter of 2023, Block had an outstanding financial performance. Their gross profit soared to an impressive $1.9B, showing a substantial 21% year-over-year growth. Moreover, they achieved a record-high quarterly adjusted EBITDA of $477M. This reflects Block's dedication to improving profitability.

Their adjusted operating income reached $90M, which signifies a remarkable 5% margin on gross profit, a substantial improvement from the previous year's $32M. Block's commitment to efficiency and financial stability is evident in these achievements.

SQ's Q3 shareholder letter

Buybacks and Strategy Shifts

In addition to the 'rule of 40' commitment by 2026, Block has followed in the footsteps of PayPal by committing to stock buybacks. Block announced a plan to repurchase $1B worth of shares, designed to offset the dilution caused by share-based compensation, as mentioned in the earnings call by CEO Jack Dorsey.

This was one of the points we addressed in our previous article , where we wrote the following:

With the company's stock currently trading around $45, there's a strong argument for Block to contemplate initiating a share buyback program. Repurchasing shares could be reasonable at this price point, as it can contribute to a higher stock price in the long run. This would benefit shareholders who have demonstrated confidence in the company's performance. Additionally, in a market environment where investors closely monitor how companies allocate their capital, a well-executed buyback program can be a strategic move to boost investor trust and loyalty.

Block's substantial cash balance of over $6.4B highlights the feasibility of implementing a share buyback program. This significant cash reserve gives the company the financial means to carry out such a strategy without jeopardizing its operations or future growth plans.

This strategy shift has been well-received by the investment community. This was one of the main concerns in our first article on SQ, which the company has now addressed. It also makes a lot of sense, given the sharp decline in stock price since its highs in 2021.

As such, this shows Block realized that they needed a change in strategy. This share repurchase plan and the better-than-expected results and guidance made us decide to upgrade our rating for SQ stock. While we still believe there are better stocks in the fintech space, such as PayPal and Adyen N.V. ( ADYEY ), to name a few, we can't justify our sell rating anymore on these improved results.

In addition, Block's two ecosystems, Square and Cash App, both excelled in Q3 , with Square generating $899M in gross profit, marking a 15% year-over-year increase. In the Cash App segment, they reported an impressive $984M gross profit, indicating a substantial 27% year-over-year growth.

In a strategic move, Block restructured its Buy Now Pay Later ((BNPL)) platform, integrating it into Cash App in the fourth quarter, which they revealed on their earnings call . This strategic decision aims to provide unique and seamless consumer experiences. Block also actively improves system reliability and redundancy to prevent future outages, emphasizing its commitment to a seamless customer experience.

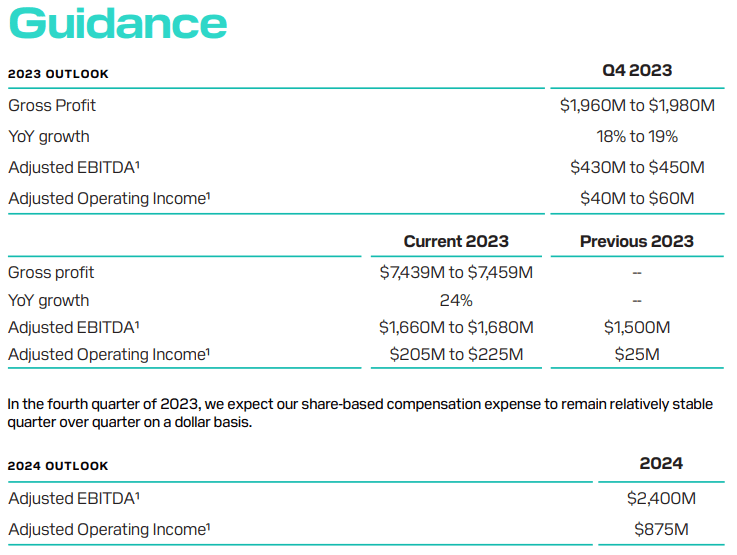

Furthermore, Block's future outlook is promising. They are shifting towards providing quarterly and annual gross profit and profit guidance. For the fourth quarter of 2023, they expect a 19% gross profit growth at the midpoint.

Block anticipates that Square's gross profit growth will improve as they compare more favorably, while Cash App's gross profit growth is expected to moderate as they lap more robust growth from the prior year.

Furthermore, Block is renewing its focus on efficiency. They have implemented an absolute cap on the number of employees and plan to reduce the team's size by the end of 2024. Their goal is to reach profitability on a GAAP operating income basis in 2024.

In addition, they also expect substantial growth in adjusted EBITDA and improved adjusted free cash flow. We have provided their guidance slide from their Q3 shareholder letter, which gives an overview of what they expect their financials to look like in the coming quarter.

{kind=link}

Net Income Is Still Negative

Despite the positive outlook, Block is still net income negative, which frustrates investors. Although it is a vast improvement from last quarter, it is still a hurdle Block needs to overcome to further satisfy and attract more investors.

From the graph below, taken from Block's Q3 letter to shareholders, it's evident that seemingly every other quarter has significant net income losses. Will that be the case in Q4 2023 as well? It's tough to say at this point.

SQ's Q3 shareholder letter

During the earnings call, Jack Dorsey explained that the company aims to boost efficiency, foster innovation, and drive growth. They're working to address internal issues, encourage collaboration, and make quicker decisions. Their ecosystem model is critical, aiming to eliminate redundancy and silos for increased effectiveness.

Despite cost constraints, they see ample room for growth, particularly in AI-driven customer service, marketing, and local sales. They prioritize clear accountability and streamlined operations while keeping customer experience intact. In addition, they are further looking into cutting costs and optimizing for profitability, which Amrita Ahuja, the CFO of Block, reiterated.

Third, within our ecosystems, as we've shared in the past, we've been identifying opportunities to continue improving our cost structure as we optimize unit economics and partnerships by leveraging our scale.

Moving to our initial outlook for profitability in 2024, which we expect to be our strongest year of profitability yet. While we are still in the planning process for next year, we expect significant margin expansion as we implement these constraints.

The growth outlook is optimistic, with plans to explore local sales, more AI tools, and banking services. They're looking to win the majority of customers' direct deposits, making Cash App their primary financial hub.

Jack Dorsey believes in Bitcoin's future role in commerce and the potential of Square's TBD initiative in the global remittance market. They aim to be disciplined and build on their early lead in understanding Bitcoin and its potential usage.

Square's Q3 report showed strong growth in vertical point of sale, with a 29% year-over-year increase in gross profit. They plan to optimize their go-to-market strategy.

Stock-based compensation is expected to remain flat in Q4, and the company aims to leverage it as a percentage of gross profit starting in 2024.

Block is open to experimenting with distribution channels, emphasizing finding what works and scaling up. Immediate experiments include contracts, local campaigns, partnerships, and referrals. This could potentially lead to many more revenue streams.

For Cash App, Square is focused on monetization and delivering value across various products, from the Cash App Card to direct deposit, ATM withdrawals, and more. They believe users are willing to pay for integrated, value-driven services and see international trends, like those in the UK, as indicators that people are willing to pay for this, reinforcing their strategy for growth and innovation.

Overall, Block's third-quarter earnings were surprising, given the picture emerging after their second-quarter earnings. However, it seems the company will do many things we want to see from them. From share buybacks to a more focused business model, there are many things to like about Block going forward.

The question remains whether or not they can execute all of it.

Valuation and Comparison To Peers

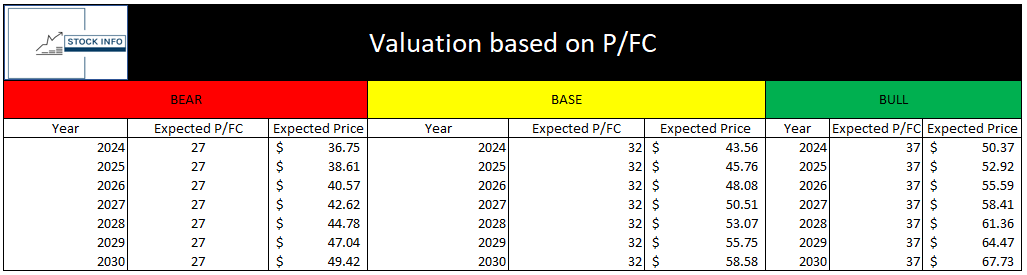

Next, we want to look at SQ's valuation, based on its current P/FC, after the market closes on Friday, November 3rd. We have also assumed that the number of shares outstanding will depreciate by approximately 3% a year, which represents the $1B share buyback program the company initiated in its Q3 earnings presentation.

In addition, we have also assumed that their free cash flow will grow by 2% a year. This is a difficult metric to model for SQ, as their free cash flow changes significantly from year to year. Therefore, we have used a very conservative estimate of 2% in our model. Furthermore, according to Seeking Alpha, SQ trades at a P/FC of approximately 32 in both TTM and FWD terms.

We have assumed three scenarios, a bear, base, and bull case, with different P/FC values SQ, could potentially trade at. Here, it is important to mention that the sector median is a P/FC of just over 6, and thus, the assumed P/FC values are still well above the median.

According to our model, even taking their share buyback program into account, it still suggests that SQ is trading a fair amount over the base price in 2024. It is closer to our assumed bull case scenario, which suggests SQ should be trading around $50 in 2024. In a bear-case scenario, we expect SQ to trade close to $37. This is, in fact, very close to the price SQ hit before its earnings came out, where it briefly touched $39.

So, what information can we take with us here? Based on our assumptions and current pricing on the market, SQ appears to be trading above what we would assume a fair price would be based on their free cash flow in TTM terms. Conversely, the market's reaction to their third-quarter earnings catapulted the price toward our assumed bull case price. Maybe investors should be on the lookout for a rally? Even so, we still think a price of $50 would be on the high end of a fair value for SQ after their recent earnings.

{kind=link}

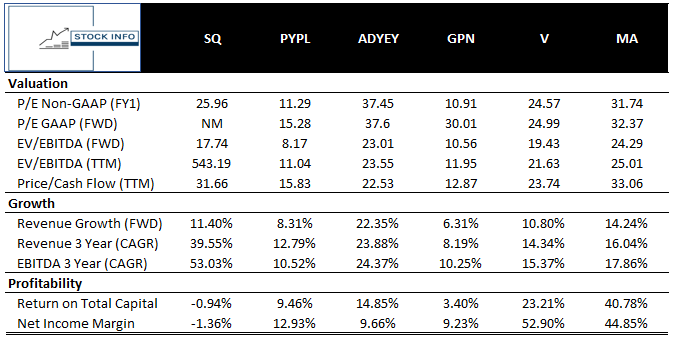

If we compare SQ to some of its closest competitors, mainly PayPal Holdings, Inc. ((PYPL)), Adyen N.V. ((ADYEY)) and Global Payments Inc. ( GPN ), most valuation metrics would suggest that SQ is currently somewhat more expensive than the other three.

We have also included Visa Inc. ( V ) and Mastercard Incorporated ( MA ) in the table below. Although they are not direct competitors to the other four tickers, as they have much more MOAT, it is still an interesting comparison as competition could become much closer in the coming years. SQ is much closer valued to Visa Inc. ((V)) and ((MA)) than PayPal ((PYPL)), except for the enormous EV/EBITDA ((TTM)).

In terms of growth, SQ is the company that has experienced the most growth in the past three years of all tickers, which, of course, is very impressive. As we mentioned earlier, this is something SQ has to keep up in the coming years, which Dorsey seems to have in focus going forward.

Lastly, and this is our bane with SQ, they are simply not as profitable as other close competitors are. SQ currently has both a negative return on total capital, as well as a negative net income margin. While this can change drastically in the next quarter, it is still not what we want to see, especially since all other peers we have included can have a positive net income.

{kind=link}

Technical Analysis: The Stock Has Jumped Through Potential Resistance

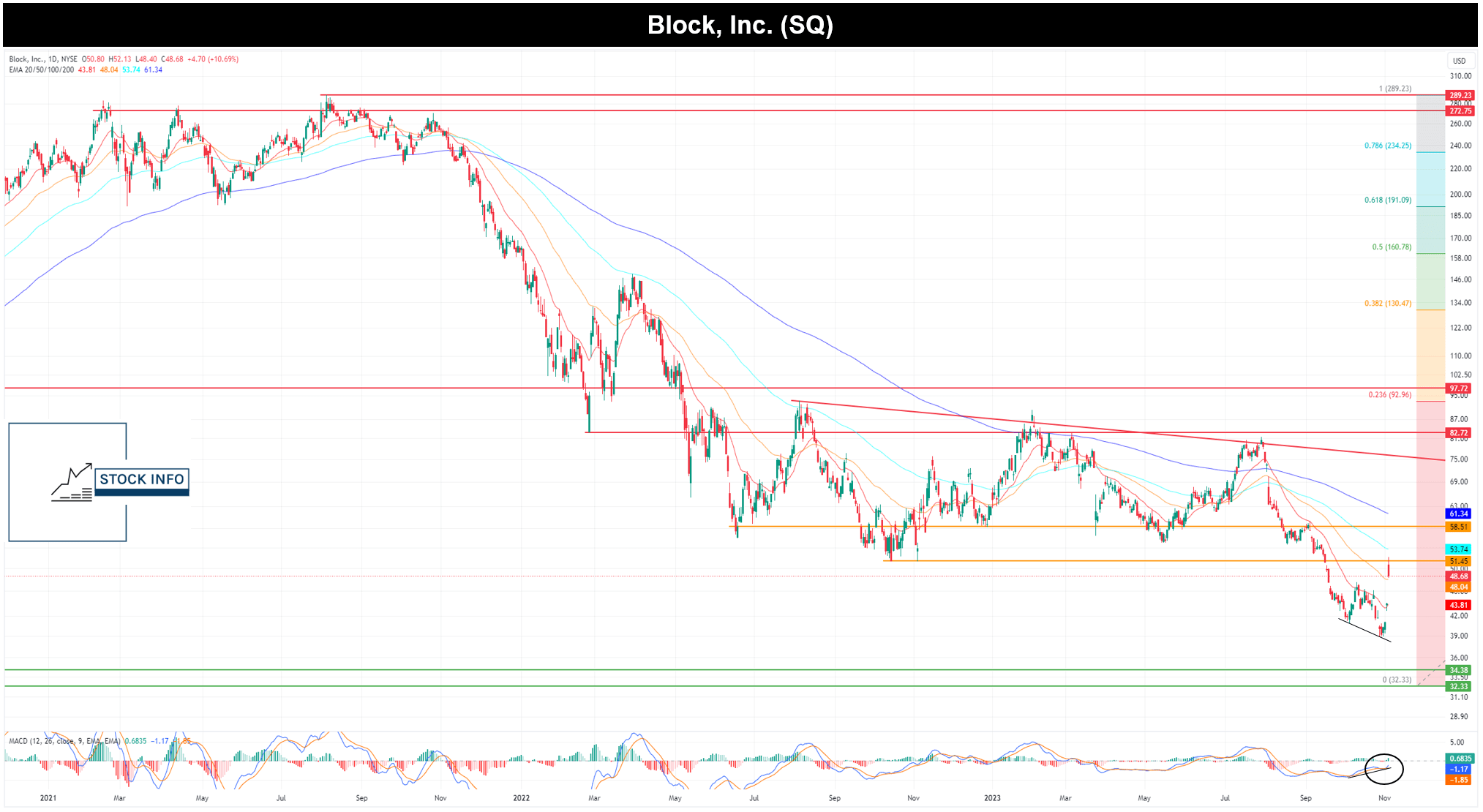

Moving on to the technical side of the stock, we first and foremost want to draw your attention to the last two trading days. Here, SQ jumped from around $40 to a high of $52.13 on Friday, November 3rd. The key here is that the stock essentially skipped past the 20 and 50 EMA's, which can provide bearish pressure to the movement of the stock. Instead, these two EMA's are underneath the current price, providing support rather than resistance.

The TA is the same as the one presented in our previous article, which is still relevant today. SQ could not move past the $51.45 level of resistance and ended up closing just above the 50 EMA on Friday. This is not a worry, though, as the stock has some cushion now moving forward. The closing price on Friday seemed to have confirmed a bullish divergence on the MACD, which could support further upward movement in the near term.

Looking ahead, the stock would have to break through the $51.45 resistance, and whereafter, the stock will meet resistance at the 100 EMA at $53.74 and $58.45.

Overall, the stock is not out of the woods yet on a technical level, as there is still a lot of pressure and levels that could trigger sellers to bid. What we want to see here is whether SQ can hold onto the 20 and 50 EMA in the near term. We would like to see a slight pullback back to the area between the 20 and 50 EMA in the coming days, which, for bulls, could present an attractive buying opportunity in the $45-$47 zone.

{kind=link}

Conclusion

To summarize, Block has delivered a strong performance in the third quarter of 2023, with impressive financial results and a strategic shift that includes a share buyback program. The company's commitment to efficiency and profitability improvement is evident, and it has made significant progress in its two ecosystems, Square and Cash App.

While the future outlook appears promising, focusing on profitability and growth, there are challenges to overcome, particularly related to achieving net income positivity.

The stock's technical analysis suggests potential bullish momentum but highlights resistance levels to watch.

Overall, Block's recent actions and results have improved its standing, leading to a reevaluation of its stock rating, although questions remain about executing its ambitious plans.

The stock is still relatively expensive compared to peers, but we feel much more comfortable holding onto SQ than before their earnings. Therefore, we have upgraded our rating to hold.

For further details see:

Block Addressed Our Concerns; Rating Upgrade